A Rising Number of State Earned Income Tax Credits are Helping Working Families Escape Poverty

An Earned Income Tax Credit is a tax reduction and a wage supplement for low- and moderate-income working families. The federal government administers an EITC through the income tax. So do many states. States that enact EITCs can reduce child poverty, increase effective wages, and cut taxes for families struggling to make ends meet.

Rising Number of States Offer EITCs

In 2006, two states — Michigan and Nebraska — enacted new EITCs. New York created an enhanced state EITC for certain non-custodial working parents. Two other states — Delaware and Virginia — are implementing new EITCs enacted in previous legislative sessions. These additions bring the total number of states with EITCs (counting the District of Columbia as a state) to 20. In addition, three local governments — New York City, San Francisco, and Montgomery County, Maryland — offer local EITCs.[1]

| State Earned Income Tax Credits Based on the Federal Credit |

| Refundable Credits |

| District of Columbia |

| Illinois |

| Indiana |

| Kansas |

| Maryland |

| Massachusetts |

| Michigan |

| Minnesota |

| Nebraska |

| New Jersey |

| New York |

| Oklahoma |

| Oregon |

| Rhode Island |

| Vermont |

| Wisconsin |

| Non-refundable Credits |

| Delaware |

| Iowa |

| Maine |

| Virginia |

When the new EITCs are fully implemented, roughly one-third of recipients of the federal EITC will live in a state with an EITC. Annual state EITC benefits will exceed $1.5 billion.

State EITCs have received broad support. EITCs have been enacted in states led by Republicans, in states led by Democrats, and in states with bipartisan leadership. The credits are supported by business groups as well as by social service advocates.

Why Consider an EITC?

Several developments explain the popularity of state EITCs.

- Continued child poverty and economic hardship. In 2004, some 8.8 million children in working families remained poor. And many families with incomes modestly above the official poverty line — roughly $19,800 for a family of four — also face significant difficulty in meeting the costs of food, housing, transportation, clothing, and other necessities. Sluggish wage growth for low-earning families means that many families are likely to continue to struggle. State EITCs can help reduce poverty and hardship among families with children.

- Low wages and welfare reform. Wage and salary growth has been weaker since the current economic recovery began in 2001 than in most previous economic recoveries. This is of particular concern at the bottom of the wage scale, where the federal minimum wage of $5.15 per hour has not been adjusted for inflation in many years.

Over the last several years, several million welfare recipients have left welfare and become employed, most of them for low wages. Many other families have accepted the challenge of making ends meet on low-paying jobs without seeking public assistance. But a full-time job at the minimum wage often is not sufficient to lift a family out of poverty. Concern about low wages has led a number of states to raise their minimum wages, but even state minimum wages that are higher than the federal wage may fall short of providing a sufficient income on which to live.[2] State EITCs support families who enter and remain in the workforce.

- Tax changes. Rising revenues in many states are leading policymakers to consider enacting tax cuts. Enacting a state EITC is a way to ensure that low- and moderate-income families share in the benefits of tax cuts. This is particularly important because most state tax systems rely heavily on sales, excise, and property taxes, the burden of which falls most heavily on low- and middle-income families. Moreover, nearly half of the states impose an income tax on working-poor families, and most states levy income tax on families with incomes only slightly above the poverty line. A state EITC can help offset such taxes.

Why Model a State Credit on the Federal EITC?

The federal EITC was established in 1975 to offset the effects of federal payroll taxes on low-income families. It has been expanded several times since, providing additional assistance to welfare recipients entering the workforce and other workers supporting their families on low wages.

The effectiveness of the federal EITC both in supporting work and in alleviating child poverty has been confirmed by a number of recent studies.

- The EITC now lifts more than 4 million people — roughly half of them children — out of poverty each year; it is the nation’s most effective antipoverty program for working families.

- Research shows that the credit has contributed to a significant increase in labor force participation among single mothers.

- Interviews with EITC recipients show that many use their EITC refunds to make the kinds of investments — paying off debt, investing in education, securing decent housing — that enhance economic security and promote economic opportunity.

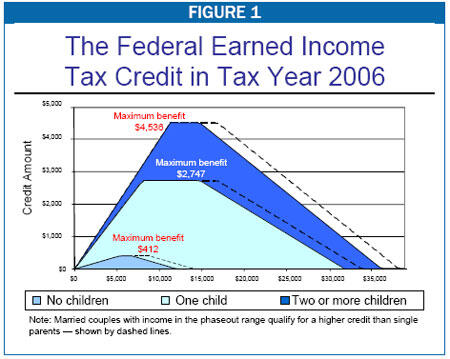

The maximum federal EITC benefit for the 2006 tax year is $4,536 for families with two or more children and $2,747 for families with one child. The greater EITC benefit for larger families reflects recognition that larger families face higher living expenses than smaller families. Workers without a qualifying child also may receive an EITC, but the maximum credit for individuals or couples without children is $412 in 2006, much lower than the credit for families with children. Figure 1 shows the EITC benefit structure for families. (As with most other provisions of the federal tax code, EITC amounts and parameters are adjusted each year by the IRS for inflation; the figures shown here are for 2006.)

The EITC benefit that an eligible family receives depends on the family’s income. For families with very low earnings, the value of the EITC increases as earnings rise. For example, families with two or more children receive an EITC equal to 40 cents for each dollar up to $11,340 earned, for a maximum benefit of $4,536. Families with one child receive an EITC equal to 34 cents for each dollar earned up to $8,080 of earnings, for a maximum benefit of $2,747. Families continue to be eligible for the maximum credit until income reaches $14,810 (or $16,810 for married-couple families).

The maximum EITC benefits go to working families with incomes below the federal poverty line, but many families with incomes well above the poverty line benefit to at least some degree. (The 2006 federal poverty line is about $20,000 for a family of four.) This is because the EITC phases out gradually as income rises above $14,810 for single-parent families or $16,810 for married couples. Single-parent families with two or more children are eligible for some EITC benefit until income exceeds $36,348, while such families with one child remain eligible for some EITC benefit until income exceeds $32,001. For married couples, the maximum eligibility levels are $38,348 for two or more children and $34,001 for one child.

Designing a State EITC

Nineteen state EITCs piggyback directly on the federal EITC; those 19 states use federal eligibility rules and express the state credit as a specified percentage of the federal credit. (The percentages are shown in Table 1.) The twentieth state with an EITC, Minnesota, also uses federal eligibility rules, and its credit parallels major elements of the federal structure.

| TABLE 1: | |||

| State | Percentage of Federal Credit (Tax Year 2006 Except as Noted) | Refundable | Workers Without Qualifying Children Eligible? |

| Delaware | 20% | No | Yes |

| District of Columbia | 35% | Yes | Yes |

| Indianaa | 6% | Yes | Yes |

| Illinois | 5% | Yes | Yes |

| Iowa | 6.5% | No | Yes |

| Kansas | 15% | Yes | Yes |

| Maine | 5% | No | Yes |

| Marylandb | 20% | Yes | No |

| Massachusetts | 15% | Yes | Yes |

| Michigan | 10% (effective in 2008; to 20% in 2009) | Yes | Yes |

| Minnesotac | Average 33% | Yes | Yes |

| Nebraska | 8% | Yes | Yes |

| New Jerseyd | 20% | Yes | No |

| New Yorke, f | 30% | Yes | Yes |

| Oklahoma | 5% | Yes | Yes |

| Oregon | 5% (to 6% in 2008) | Yes | Yes |

| Rhode Island | 25% | Partiallyg | Yes |

| Vermont | 32% | Yes | Yes |

| Virginia | 20% | No | Yes |

| Wisconsin | 4% - one child | 4% - one child | No |

| 14% - two children | 14% - two children | ||

| 43% - three children | 43% - three children | ||

| Notes: From 1999 to 2001, Colorado offered a 10% refundable EITC financed from required rebates under the state’s “TABOR” amendment. Those rebates, and hence the EITC, were suspended beginning in 2002 due to lack of funds and again in 2005 as a result of a voter-approved five-year suspension of TABOR. Under current law, the EITC is projected to resume in 2010. a Presently scheduled to expire in TY 2011. b Maryland also offers a non-refundable EITC set at 50 percent of the federal credit. Taxpayers in effect may claim either the refundable credit or the non-refundable credit, but not both. c Minnesota’s credit for families with children, unlike the other credits shown in this table, is not expressly structured as a percentage of the federal credit. Depending on income level, the credit for families with children may range from 25 percent to 45 percent of the federal credit; taxpayers without children may receive a 25 percent credit. d The New Jersey credit is available only to families with incomes below $20,000. e The New York credit would be reduced automatically to the 1999 level of 20 percent should the federal government reduce New York’s share of the TANF block grant. f Beginning in 2006, New York also allows certain non-custodial parents who are making child support payments to claim an EITC that is the greater of 20 percent of the federal EITC that they would be eligible for with one qualifying child as a custodial parent or 250 percent of the federal EITC for taxpayers without qualifying children. g Rhode Island made a very small portion of its EITC refundable effective in TY 2003. In 2006, the refundable portion was increased from 10 percent to 15 percent of the nonrefundable credit (i.e. 3.75 percent of the federal EITC). | |||

Sixteen of the 20 states with EITCs follow the federal practice of making the credit “refundable.” This means a family receives the full amount of its credit even if the credit amount is greater than the family’s state income tax liability. The amount by which the credit exceeds annual income taxes is paid as a refund. If a family has no income tax liability, the family receives the entire EITC as a refund. All low-income working families with children can participate in a refundable EITC.

The remaining four states — Delaware, Iowa, Maine, and Virginia — offer credits that are non-refundable. Such a credit is available only to the extent that it offsets a family’s state income tax. A non-refundable EITC can provide substantial tax relief to families with state income tax liability, but it provides no benefits to working families that have income too low to owe any income taxes. Thus a non-refundable credit assists somewhat fewer working-poor families with children and is likely to be less effective as a work incentive.

Another source of variation in the design of state credits is the treatment of low-income workers who do not have children living with them. Most states allow such workers to claim a state EITC (the exceptions are Maryland, New Jersey and Wisconsin), but because the federal credit for such workers is much smaller than for families with custodial children, the corresponding state credit typically is small as well. Beginning in 2006, one state — New York — is allowing such workers an enhanced, fully-refundable EITC, if they are non-custodial parents and if they remain current on their child support payments. The enhanced credit allows such parents to claim either (a) 20 percent of the federal EITC amount for which they would be eligible as the custodial parents of one qualifying child or (b) 250 percent of the federal EITC for which they are actually eligible as non-custodial parents. As a result, eligible non-custodial parents in New York may receive an EITC of up to $1,030 in 2006, substantially more than such parents can receive in other states.

Financing a State EITC

Existing refundable state EITCs cost less than 1 percent of state tax revenues each year, though their dollar cost varies considerably from state to state because of differences in the size of state economies. (Vermont’s EITC costs about $17 million per year, while New York State’s costs about $680 million.) The cost of a state EITC depends principally on four factors: the number of families in a given state that claim the federal credit, the percentage of the federal credit at which the state credit is set, whether the credit is refundable or non-refundable, and how many state residents that receive the federal credit also learn about and claim the state credit. Because state EITCs are more specifically targeted to low- and moderate-income working families than many other major tax cuts, the cost may be relatively modest.

State EITCs are financed in whole or in part from funds available in a state’s general fund — the same funding source typically used for other types of tax cuts. When an EITC is used to offset the effects of a regressive tax increase, such as a sales tax increase, a part of the proceeds of the revenue increase may be set aside for the EITC. Current federal regulations also offer the opportunity to finance a portion of the cost of a refundable credit from a state’s share of the federal Temporary Assistance to Needy Families block grant. Most states have very limited availability of such funds, however, because the value of the TANF block grant has eroded over time and because states face costly new work requirements under the most recent federal budget law. No matter how it is financed, however, an EITC can complement a state’s welfare program by assisting low-income working families with children.

Further details on state EITCs and how they can help working families escape poverty are available in the following report from the Center on Budget and Policy Priorities: “A Hand Up: How State Earned Income Tax Credits Help Working Families Escape Poverty in 2006” by Ami Nagle and Nick Johnson. The report can be found at:

.End Notes:

[1] One other state and one other city have offered EITCs in the past. The state of Colorado previously offered an EITC that was financed from required rebates under the state’s “TABOR” amendment. Those rebates, and hence the EITC, were suspended beginning in 2002 due to lack of funds and again in 2005 as a result of a voter-approved five-year suspension of TABOR. Under current law, the EITC is projected to resume in 2010. Separately, the city of Denver, Colorado piloted a local EITC beginning in 2002, which was financed from Temporary Assistance for Needy Families funds. In 2004, the program was suspended due to insufficient TANF funds.

[2] Jason A. Levitis and Nicholas Johnson, Together, State Minimum Wages and State Earned Income Tax Credits Make Work Pay, Center on Budget and Policy Priorities, https://www.cbpp.org/7-12-06sfp.htm.

More from the Authors

Areas of Expertise