Eliminating Estate Tax on Inherited Wealth Would Increase Deficits and Inequality

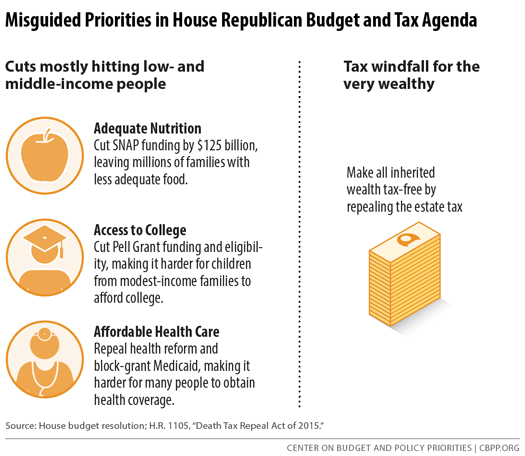

The House is scheduled to consider a bill this week to repeal the federal estate tax on inherited wealth, several weeks after approving a budget plan calling for $5 trillion in program cuts disproportionately affecting low- and moderate-income Americans.[1] Repealing the estate tax would be highly misguided — especially in the context of the House budget, which would repeal health reform and cut Medicaid deeply, causing tens of millions of Americans to become uninsured or underinsured; cut the Supplemental Nutrition Assistance program (SNAP, formerly known as food stamps), making it harder for millions of low-income families to put food on the table; and cut Pell Grants, raising the financial hurdle for people of modest means to attend college. (See Figure 1.)

Despite these and hundreds of billions of dollars in additional cuts that were largely unspecified, the House budget included no revenue increases. And while concerns of future deficits supposedly drive the budget’s harsh cuts, repealing the estate tax would significantly expand deficits.

Repeal would:

- Cost $269 billion in reduced revenues over 2016 to 2025, according to the Joint Committee on Taxation (JCT), adding $320 billion to deficits when counting additional interest on the national debt. The legislation before the House would not offset this cost, contrary to Republican calls for a balanced budget.

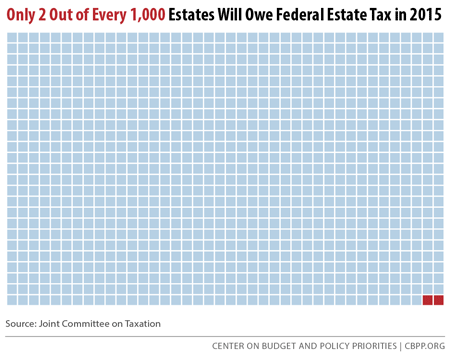

- Do nothing for 99.8 percent of estates. Only the estates of the wealthiest 0.2 percent of Americans — roughly 2 out of every 1,000 people who die — owe any estate tax. This is because of the tax’s high exemption amount, which has jumped from $650,000 in 2001 to $5.43 million per person (effectively $10.86 million for a couple) in 2015. Repeal would bestow a tax windfall averaging over $3 million apiece, or more than a typical college graduate earns in a lifetime, on the roughly 5,400 wealthy estates that will owe the tax in 2016.[2] The 318 estates worth at least $50 million (some of which are worth hundreds of millions of dollars) would receive tax windfalls averaging more than $20 million each.

-

Exacerbate wealth inequality, which has grown significantly in recent decades. In 2012, the wealthiest 1 percent of American families held about 42 percent of total wealth, new data show.[3] Large inheritances play a significant role in the concentration of wealth; inheritances account for about 40 percent of all household wealth and are extremely concentrated at the top. Repealing the estate tax would exacerbate wealth inequality by benefiting only the heirs of the country’s wealthiest estates, who also tend to have very high incomes.[4]

In addition, despite policymakers’ frequent statements about the importance of work, repeal would reduce the incentive for heirs of large estates to work.

Evidence shows the estate tax is an economically sound tax. Contrary to claims that it hurts the economy, it likely has little or no impact on wealthy donors’ savings, and it encourages heirs to work. It is an economically efficient way to raise revenue that supports public services and lowers deficits without imposing burdens on low- and middle-income Americans. Thus, the estate tax plays an important role in our revenue system, particularly given our long-term budget challenges.

Tax Affects Only Largest Estates

Only the estates of the wealthiest 0.2 percent of Americans — roughly 2 out of every 1,000 people who die — owe any estate tax (see Figure 2). This is because estate taxes are due only on the portion of an estate’s value that exceeds the exemption level, $5.43 million per person in 2015.

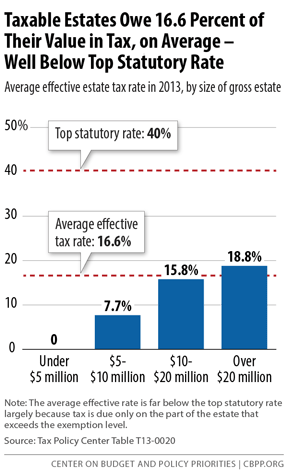

Moreover, the few estates that owe the tax generally pay less than one-sixth of their value in tax. Among taxable estates in 2013, their “effective” tax rate — that is, the percentage of the estate’s value that was paid in taxes — averaged 16.6 percent (see Figure 3).[5] The effective rate is far below the top statutory rate of 40 percent, both because of the high exemption level and because heirs can often shield a large portion of an estate’s remaining value from taxation through various deductions.

Only roughly 20 small business and farm estates nationwide owed any estate tax in 2013, the Tax Policy Center (TPC) estimates. They owed just 4.9 percent of their value in tax, on average.[6]

Repeal Would Be Costly and Benefit Only Very Wealthy Estates

The estate tax repeal bill before the House would reduce revenue by $269 billion over 2016 to 2025. Because it includes no provisions to offset this revenue loss, it would add $320 billion to deficits when counting the additional interest cost on the national debt.[7]

The roughly 5,400 estates nationwide that would face the tax in 2016 would receive tax cuts averaging more than $3 million apiece from repeal.[8] The windfalls would be staggering for the wealthiest of these estates, JCT data show:

- The 1,336 estates worth $20 million or more would receive 73 percent of the total tax cut, with each receiving a tax windfall averaging roughly $10 million.

- The 318 estates worth at least $50 million would receive tax windfalls averaging more than $20 million each.

Repeal Would Exacerbate Growing Wealth Inequality

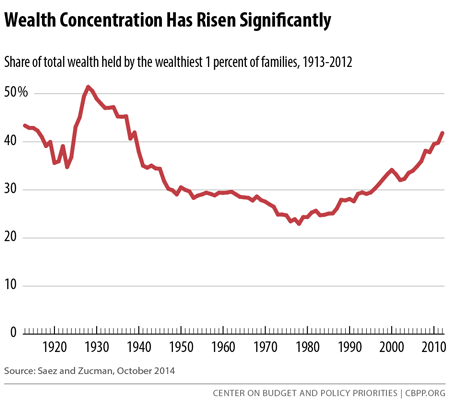

Income and wealth are becoming increasingly concentrated at the top.[9] Income concentration has risen to levels last seen more than 80 years ago, during the “Roaring Twenties.”[10] The share of the nation’s wealth held by the top 1 percent has increased markedly over the past three decades as well, new research shows (see Figure 4), driven by a rising share of wealth at the very top.[11] The wealthiest 0.1 percent of families — the main beneficiaries of estate tax repeal — saw their share of the nation’s wealth jump from 7 percent to 22 percent between 1978 and 2012.

Large inheritances play a significant role in wealth concentration. Inheritances account for about 40 percent of all household wealth and are extremely concentrated at the top. Moreover, “[d]isparities in inheritances appear to be the most significant barrier to mobility — accounting for about 30 percent of the correlation between parent and child economic outcomes,” according to testimony by leading estate tax expert Lily Batchelder.[12] She notes that the estate tax “is the most important mechanism by which the fiscal system mitigates the effects of inheritances on economic disparities and intergenerational mobility.”

Trust-Fund Loophole Means Significant Capital Gains Would Go Untaxed Without Estate Tax

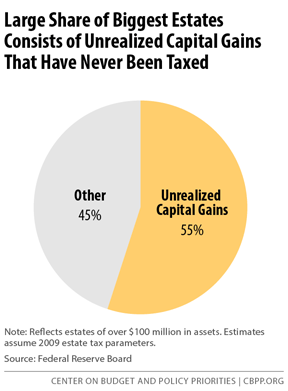

Much of the wealth that heirs inherit from wealthy estates would never face taxationif not for the estate tax. Capital gains tax is due on the appreciation of assets, such as real estate, stock, or an art collection, only when the owner “realizes” the gain, usually by selling the asset. Under the so-called “trust-fund loophole,” if a person holds an asset that grows in value until his or her death, that “unrealized” capital gain is forgiven, and neither the heir of the estate nor the deceased person ever pays tax on it. Unrealized capital gains account for a significant proportion of the assets held by estates, ranging from 32 percent for estates worth between $5 million and $10 million to about 55 percent for estates worth more than $100 million (see Figure 5).

Without the estate tax, wealthy individuals would have an even stronger incentive to hold on to appreciated assets in order to avoid paying tax on those gains, since those inheriting even the largest estates would owe neither capital gains tax nor any estate tax. This “lock-in” effect is economically inefficient — another reason why the estate tax, which reduces lock-in, is economically sound.[13]

The estate tax also serves as a modest corrective to other tax rules that provide large tax benefits to income from wealth, such as the lower tax rates for capital gains than for wages and salaries. The top 0.1 percent of taxpayers — those with incomes above $3.2 million — will receive more than half of the benefit of the preferential capital gains rates in 2015, which will be worth an average of about $500,000 apiece to these individuals.[14] Other tax rules allow part of the income of the very wealthiest to go completely untaxed, even with the estate tax.[15]

Estate Tax Is Economically Sound

The evidence indicates that the estate tax is an economically sound tax, likely has little or no impact on wealthy donors’ overall level of savings, and increases national saving — a critical determinant of the amount of capital available for private investment. It also encourages heirs to work, and it increases charitable donations.

Studies suggest that the estate tax has a small or no effect on private saving.[16] And because repeal would increase the federal budget deficit, it likely would reduce national saving (which is the net sum of private saving and government dissaving).

The reason is simple: while any effect on private saving would be small, the government would have to borrowmore to offset the lost revenue. Government borrowing “soaks up” capital that would otherwise be available for investment in the economy.[17] In the case of estate tax repeal, the added government borrowing would more than outweigh any added private saving, leaving the economy no better off and quite possibly worse off.

“[I]f the only objective [of eliminating the estate tax] were increased savings,” the Congressional Research Service has concluded, “it would probably be more effective to simply keep the estate and gift tax and use the proceeds to reduce the national debt.”[18]

The benefits of estate tax repeal would overwhelmingly go to the heirs and heiresses of the extremely wealthy estates that face the tax, since the estate tax reduces the size of their large inheritances.

Repeal of the estate tax could also lead some heirs to work somewhat less. Some wealthy donors such as Bill Gates have said they plan to give away much of their fortunes, in part to make sure their children don’t live idly on their inheritances. Gates has said his children will receive a “miniscule” portion of his wealth so they “have to find their own way.”[19] Similarly, the musician Sting commented, “I certainly don’t want to leave them trust funds that are albatrosses round their necks. They have to work.”[20] Research on the effect of wealth transfers on work supports this intuition. Treasury analyst David Joulfaian finds that “an inheritance of $1 million, other things equal, reduces labor force participation by about 11 percent.”[21] Estate tax repeal thus would likely reduce incentives for heirs to work and save.

On a related issue, empirical research finds the estate tax encourages donations to charity both during life and at death. These donations reduce the size of an estate and thus the amount subject to the estate tax.[22]

Conclusion

Repealing the estate tax would swell deficits and worsen growing wealth inequality, while providing no benefit to the overwhelming majority of Americans. Repeal would be especially indefensible in light of the House budget, whose severe budget cuts would reduce economic opportunity and increase poverty in the name of addressing deficits.

End Notes

End notes:

[1] “Statement by Robert Greenstein, President, on House Budget Chairman’s Plan,” Center on Budget and Policy Priorities, updated March 18, 2015, https://www.cbpp.org/cms/index.cfm?fa=view&id=5284.

[2] CBPP estimates based on Tiffany Julian, “Work-Life Earnings by Field of Degree and Occupation for People With a Bachelor’s Degree: 2011,” U.S. Census Bureau, October 2012, http://www.census.gov/prod/2012pubs/acsbr11-04.pdf.

[3] Emmanuel Saez and Gabriel Zucman, “Wealth Inequality in the United States since 1913: Evidence from Capitalized Income Tax Data,” NBER Working Paper 20625, October 2014, http://eml.berkeley.edu/~saez/saez-zucmanNBER14wealth.pdf.

[4] Lily Batchelder, “Reform Options for the Estate Tax System: Targeting Unearned Income,” testimony before the U.S. Senate Committee on Finance, March 12, 2008.

[5] Tax Policy Center Table T13-0020. The estimates have not been updated for years after 2013, but the average effective estate tax rate should be very similar for 2014 and 2015 because the statutory rate remains the same and the exemption level is indexed to inflation.

[6] Tax Policy Center Table T13-0020. TPC’s analysis defines a small-business estate as one with more than half its value in a farm or business and with the farm or business assets valued at less than $5 million.

[7] Joint Committee on Taxation, JCX-68-15, https://www.jct.gov/publications.html?func=startdown&id=4761; CBPP calculations of added interest cost.

[8] CBPP calculations based on Joint Committee on Taxation data available at http://democrats.waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/documents/114-0191.pdf.

[9] See Chad Stone et al., “A Guide to Statistics on Historical Trends in Income Inequality,” Center on Budget and Policy Priorities, revised February 20, 2015, https://www.cbpp.org/cms/?fa=view&id=3629.

[10] Emmanuel Saez, “Striking it Richer: The Evolution of Top Incomes in the United States,” University of California, January 25, 2013, http://eml.berkeley.edu/~saez/saez-UStopincomes-2013.pdf.

[11] Saez and Zucman, 2014.

[12] Lily Batchelder, “Reform Options for the Estate Tax System: Targeting Unearned Income,” testimony before the U.S. Senate Committee on Finance, March 12, 2008. Batchelder was a professor at New York University Law School at the time she testified; she is currently deputy director of the National Economic Council. In her testimony, she summarizes previous research, including: Thomas Piketty, “Theories of Persistent Inequality and Intergenerational Mobility,” in Handbook of Income Distribution (A. Atkinson and F. Bourguignon, eds., 1998); and Bhashkar Mazumder, “The Apple Falls Even Closer to the Tree than We Thought: New and Revised Estimates of the Intergenerational Inheritance of Earnings,” in Unequal Chances: Family Background and Economic Success (Samuel Bowles et al., eds., 2005).

[13] The President’s 2016 budget proposes to repeal this favorable treatment, also known as “step-up basis,” which would reduce the lock-in effect. In addition, the President’s budget would raise the top tax rate on capital gains to 28 percent. See Chuck Marr and Chye-Ching Huang, “President’s Capital Gains Tax Proposals Would Make Tax Code More Efficient and Fair,” Center on Budget and Policy Priorities, January 18, 2015, https://www.cbpp.org/cms/?fa=view&id=5260.

[14] Tax Policy Center Table T13-0081.

[15] Chye-Ching Huang and Chuck Marr, “Raising Today’s Low Capital Gains Tax Rates Could Promote Economic Efficiency and Fairness, While Helping Reduce Deficits,” Center on Budget and Policy Priorities, September 19, 2012, https://www.cbpp.org/cms/index.cfm?fa=view&id=3837.

[16] In fact, if a wealthy donor’s goal is to leave a certain amount after-tax to heirs, estate tax reduction or repeal might lead the donor to work or save less. But the research indicates that people save primarily for reasons other than to amass large estates, such as to ensure adequate income to meet all needs in old age and simply to accumulate wealth. (See Lily Batchelder and Surachai Khitatrakun, “Dead or Alive: An Investigation of the Incidence of Estate Taxes and Inheritance Taxes,” 3rd Annual Conference on Empirical Legal Studies Papers, October 28, 2008, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1134113.) Thus, repealing the estate tax would likely have only a small effect on private saving, if any.

[17] Foreign investors might increase investment in the United States, in which case more of the value of goods and services produced domestically would go towards paying foreign lenders.

[18] Jane G. Gravelle and Donald J. Marples, “Estate and Gift Taxes: Economic Issues,” Congressional Research Service, November 27, 2009.

[19] Caroline Graham, “This is not the way I'd imagined Bill Gates . . . A rare and remarkable interview with the world's second richest man,” Daily Mail, June 9, 2011, http://www.dailymail.co.uk/home/moslive/article-2001697/Microsofts-Bill-Gates-A-rare-remarkable-interview-worlds-second-richest-man.html.

[20] Roxanne Roberts, “Why the super-rich aren’t leaving much of their fortunes to their kids,” The Washington Post, August 10, 2014, http://www.washingtonpost.com/lifestyle/style/why-the-very-rich-arent-giving-much-of-their-fortunes-to-their-kids/2014/08/10/4a9551b4-1ccc-11e4-82f9-2cd6fa8da5c4_story.html.

[21] David Joulfaian, “Inheritance and Saving,” National Bureau of Economic Research Working Paper No. 12569, October 2006, http://www.nber.org/papers/w12569.pdf.

[22] See Congressional Budget Office, “The Estate Tax and Charitable Giving,” July 2004; Jon Bakija and William Gale, “Effects of Estate Tax Reform on Charitable Giving,” Tax Notes, June 23, 2003; Aviva Aron-Dine, “Estate Tax Repeal — or Slashing The Estate Tax Rate — Would Substantially Reduce Charitable Giving,” Center on Budget and Policy Priorities, June 7, 2006, https://www.cbpp.org/cms/index.cfm?fa=view&id=465.

More from the Authors

Areas of Expertise