Testimony of James Horney on Addressing the Nation's Financial Challenges

Chairman Carper, Senator Coburn, Members of the Committee, thank you for the opportunity to appear here today to talk about the long-term fiscal problems facing the United States.

My name is James Horney. I am the Director of Federal Fiscal Policy at the Center on Budget and Policy Priorities, which is a non-partisan, non-profit research institute with a particular interest in programs that assist low- and moderate income Americans. The Center receives no funds from the federal government. I should note that in a previous job I was responsible for coordinating the Congressional Budget Office’s baseline budget projections.

I also should note that the Center also has a strong interest in, and long history of, promoting fiscally responsible federal budget policies, in part because of our concern that if such policies are not implemented, future resources to fund programs we believe make a vital contribution to the social fabric of the nation will be severely limited.

I want to make four points here today:

- First, as suggested by the Statement of Social Insurance included in the 2007 Financial Report of the U.S. Government, the federal budget is on a path that will eventually lead to unsustainable increases in debt;

- Second, the keys to the long-term federal budget problem facing us are the growth of federal expenditures for health care and the level of revenues available to finance federal programs;

- Third, the key to bringing federal health care expenditures under control is limiting the growth of health care costs system wide — private as well as public; and,

- Fourth, that real progress toward sustainable fiscal policies will require a bipartisan consensus about the priority of deficit reduction, and the willingness of the President and both parties in Congress to put everything on the table — revenues and program spending — and negotiate balanced deficit reduction packages.

Let me explain why I come to these conclusions.

Current Policies Will Eventually Lead to Unsustainable Increases in Debt

Although the Statement of Social Insurance is limited to just a few programs (most importantly, Social Security and Medicare), the message one takes from the statement — current policies are unsustainable – is consistent with the conclusions of other analyses that take a more comprehensive approach in addressing the long-term prospects of the entire U.S. budget. Those analyses — including those undertaken by the Congressional Budget Office, the Office of Management and Budget, the Government Accountability Office, and the Center on Budget and Policy Priorities — conclude that unless current policies are changed, total federal spending is likely to exceed total federal revenues by growing amounts in coming decades, eventually leading to an explosion in debt that would seriously harm the economy. All of the institutions that have undertaken these analyses have noted the high level of uncertainty about projections of federal spending and revenues over a period of thirty to fifty years and more, but they all agree that it would be highly imprudent for policymakers to maintain current policies in the hope that outcomes will be substantially more favorable than these current projections suggest.

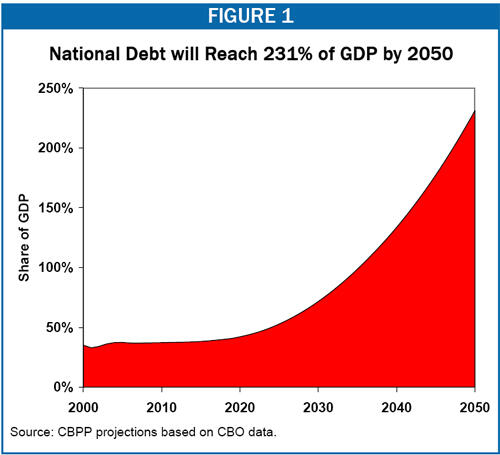

Figure 1 shows the growth of federal debt as a share of Gross Domestic Product (GDP) in long-term projections the Center published in January 2007.[1] (We are in the process of updating the projections, but are confident that the basic conclusions will not change.) The projections show that if current polices are continued (e.g., if current laws governing Medicare, Social Security, and other programs remain unchanged, the 2001 and 2003 tax cuts are made permanent, and relief from the Alternative Minimum Tax is continued), deficits will reach about 20 percent of GDP by 2050, and the national debt will climb to about 230 percent of GDP by that year, or more than twice the size of the U.S. economy. Debt-to-GDP ratios in this range are unprecedented in the United States. At the end of World War II, the national debt was only slightly above 100 percent of GDP.[2]

Projections by others such as CBO and GAO differ in detail from ours, but the overall conclusion is the same. Without changes in current policies, the path of the federal budget is unsustainable: growing deficits will push the debt-to-GDP ratio ever higher. The President and the Congress need to take action to prevent this from happening. As CBO concluded in its most recent report on the long-term problem, “To prevent deficits from growing to levels that could impose substantial costs on the economy, revenues must rise as a share of GDP, or projected spending must fall — or some combination of the two outcomes must be achieved.”[3]

One thing I would like to note, however, is that the rapid increase in the national debt is not projected to occur until after 2020. We are not facing an immediate budget “crisis,” but beginning to deal with the long-term problem in a serious way as soon as possible is highly desirable. Having said this, we also should remember that there is time to make sure that we take a sensible and sustainable approach to deficit reduction. The world will not come to an end if we do not take steps in the next year or two that promise to fully eliminate the long-term fiscal imbalance. We need to be careful not to adopt hastily considered measures that may prove unsustainable or unwise in later years.

Rising Health Care Costs and the Level of Revenues Are Key

Some budget observers have suggested that the long-term problem is the result of an “entitlement” crisis. This is misleading both in suggesting that entitlement program spending in general is projected to rise rapidly in coming decades and in implying that revenue policies do not play a role in the long-term problem.

Health Care, Not Entitlements in General or Even Social Security, Drive Big Increase in Spending

The Center projects that, under current policies, entitlement spending will grow significantly faster than the economy over the next 40 years and beyond. But entitlement spending outside of Social Security, Medicare, and Medicaid is projected to grow more slowly than the economy over that period.[4] This is consistent with CBO’s most recent 10-year baseline projection that spending for all other entitlements — i.e. other than the “Big Three” — will shrink from 2.7 percent of GDP in 2008 to 2.0 percent in 2018.

It is worth noting also that long-term projections by the Center and others assume that discretionary spending for defense and domestic programs will not grow faster than the economy. This means that Social Security, Medicare, and Medicaid are responsible for all of the projected growth of non-interest spending relative to the economy in coming decades (actually more than all, since other spending is expected to decline as a percent of GDP under current policies).

As almost everyone knows, the projected growth of Social Security expenditures is an important contributor to the long-term problem. With the retirement of the baby-boom population, the number of Social Security beneficiaries is expected to grow to about 86 million by 2030 according to CBO, up from about 50 million today. As a result, Social Security spending is expected to rise from 4.3 percent of GDP in 2007 to 6.1 percent of GDP by 2030 according to CBO. The trend will level off in subsequent years, so that expenditures for Social Security are then expected to rise only to 6.4 percent of GDP by 2082.

The increase in Social Security spending by an amount equal to nearly 2 percent of GDP over the next two decades or so is a problem for the budget, but Medicare and Medicaid have a larger impact on the budget because spending for those programs is expected to increase by more than 2 percent of GDP by 2030 and is expected to continue to grow significantly faster than GDP in years after that. CBO projects that Medicare and Medicaid spending could grow from 4 percent of GDP in 2007 to 19 percent of GDP in 2082.

The reason that Social Security poses less of a challenge than Medicare and Medicaid is that the growth in Social Security spending relative to GDP is driven entirely by demographics — by the increase in the number of beneficiaries relative to the number of working-age Americans (which is a key determinant in the growth of GDP). The demographic pressures subside with time, and Social Security spending then begins to grow more in line with the economy.

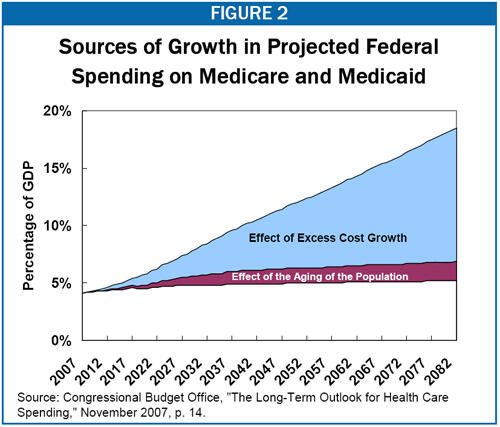

Medicare and, to a lesser extent, Medicaid (because only a portion of Medicaid spending goes for care of the elderly), are subject to these same demographic pressures. But they are subject to another, stronger force — the rising per-person cost of providing health care in the United States. CBO estimates that real per capita spending on health care — private as well as public — grew at an average annual rate of 4.2 percent over the thirty years from 1975 to 2005, significantly faster than the growth of the economy.[5] CBO estimates that, on average, total per capita spending on health care grew 2.1 percentage points a year faster than GDP over this period. Medicare and Medicaid expenditures grew at about the same rate as overall health care costs, with “excess growth” averaging 2.4 percentage points for Medicare and 2.2 percent for Medicaid.

After considering the factors contributing to the growth of overall health care costs over the last three decades, CBO concludes that:

“The most important factor contributing to the growth of health care spending in recent decades has been the emergence, adoption, and widespread diffusion of new medical technologies and services. Major advances in medical science allow providers to diagnose and treat illnesses in ways that were previously impossible. Many of those innovations rely on costly new drugs, equipment, and skills. Other innovations are relatively inexpensive but add up quickly as growing numbers of patients make use of them. Although technological innovation can sometimes reduce spending, in medicine such advances and the resulting changes in clinical practice have generally increased it.”[6]

CBO and almost all other health care and budget experts assume that, without significant changes in the U. S. health care system, these forces will continue to cause the growth of per capita health care spending to exceed the growth of GDP. Figure 2 shows clearly how much impact this has on projected Medicare and Medicaid costs relative to the demographic effects of the aging of the population.

Revenues

In claiming that the growth of entitlements is the cause of the long-term fiscal problem, some commentators seem to suggest that revenues are not a major factor in long-term deficits. But deficits obviously are the result of revenues that fall short of expenditures just as much as they are the result of expenditures that exceed revenues. It is also important to note that the President and the Congress will be faced in the next two years with a decision about revenues that will have a major impact on the size of the long-term problem.

As everyone is well aware, the 2001 and 2003 tax cuts are scheduled to expire under current law at the end of 2010. The decision whether to extend some or all of them, and whether to pay for the cost of any tax cuts that are extended, will have a big effect on projected deficits. One measure of the size of the long-term deficits is the so-called “fiscal gap,” which is the net present value of past deficits and projected future deficits excluding payments of interest on the debt. (The fiscal gap tells you how much, on average, spending must be reduced, or revenues increased, or some combination of the two, in order to keep the budget on a sustainable path over the period for which the gap is measured.) The Center’s long-term projections in 2007 produced an estimated fiscal gap for the period through 2050 equal to 3.2 percent of GDP if the tax cuts are made permanent without any offsets, relief from the Alternative Minimum Tax continues to be granted, and other policies remain unchanged, as described above. According to estimates by the Joint Committee on Taxation and CBO, the cost of extending the 2001 and 2003 tax cuts without any offsets would be equal to 2 percent of GDP. Thus, not extending the tax cuts — or paying for any extensions with increases in other taxes or cuts in spending — would reduce the size of the fiscal gap through 2050 by more than half. I should note that, because of the continued growth of health care costs after 2050, the fiscal gap is larger over any measured period that extends beyond 2050. Although the amount of revenue associated with the 2001 and 2003 tax cuts is much smaller than the anticipated growth over time in expenditures for federal health care programs, the fact that the decision on the fate of the tax cuts affects revenue levels by a full 2 percent of GDP starting in the next few years, rather than by an amount that is initially small and grows gradually, means that the added revenue would produce interest savings that would compound from an early date.

I am not trying to start a debate about whether the tax cuts should be extended, but I do want to make it clear that that decision as well as other decisions about taxes will have a major impact on long-term deficits. Revenues definitely must be part of the debate over the long-term budget. I believe it will be impossible for the federal government to meet crucial existing and future needs without revenue levels above those seen today and in recent years. It is important to note that revenues at the level experienced over the previous 30 years — 18.4 percent of GDP (which is higher than the 17.9 percent of GDP CBO has projected for this year) — would have been insufficient to balance the budget in any of the last 30 years.

System-Wide Health Care Reform is Necessary

As indicated above, the “excess growth” of Medicare and Medicaid spending has closely tracked that of total health care spending, both public and private. That shows that the growth of those programs is not the result of any flaws in the structure or administration of those programs, but is instead the result of fundamental features of our whole health care system and of changes in medical knowledge and technology.

This also makes clear that slowing the growth of Medicare and Medicaid — which is ultimately crucial in dealing with the long-term budget problem — cannot sensibly and fairly be accomplished without making system-wide changes that slow the growth of private and public spending.

In his previous role as Comptroller General of the United States, David Walker said:

“[F]ederal health spending trends should not be viewed in isolation from the health care system as a whole. For example, Medicare and Medicaid cannot grow over the long-run at a slower rate than cost in the rest of the health care system without resulting in a two-tier health care system.”[7]

CBO Director Peter Orszag agrees with that assessment:

“Many analysts believe that significantly constraining the growth of costs for Medicare and Medicaid over long periods of time, while maintaining broad access to health providers under those programs, can occur only in conjunction with slowing cost growth in the health care sector as a whole.

Ultimately, therefore, restraining costs in Medicare and Medicaid requires restraining overall health care costs.”

This does not imply that no steps should be taken to reduce Medicare and Medicaid costs until major changes in the health care system have been completed. It would make sense, for instance, to immediately enact the Medicare reforms that have been recommended by Congress’s Medicare Payment Advisory Commission (MedPac), including the recommendation to level the playing field by eliminating overpayments to Medicare Advantage providers (which alone would save an estimated $150 billion over 10 years). There is also the potential for Medicare to take the lead in some cost-saving efforts that would then be adopted in the private sector. But it is clear that it will not be possible to reduce the growth of Medicare and Medicaid spending anywhere close to as much as is needed to help solve the long-term problem and maintain the important role those programs play in providing care to the elderly and the needy without making system-wide cost-saving changes in the way we deliver and finance health care.

Solutions Must Be Balanced, Fair, and Bipartisan

The task of putting the federal budget on a sustainable course is daunting, but not impossible. It will, however, require a bipartisan consensus among the President and Congressional leaders of both parties that making the changes needed to curb the deficits we are facing under current policies is a high priority — a high enough priority that it is worth compromising on other strongly held goals in order to achieve fiscal sustainability. Progress has been made in the past — for instance, with the 1983 reforms that made Social Security solvent for about 60 years and the 1990 negotiations that led to deficit reduction of nearly $500 billion over five years — when the President and Republicans and Democrats in Congress were willing to put everything on the table — taxes and programs — and compromised on a balanced set of policies that increased revenues and reduced programs. Those compromises did not totally suit anyone, but they moved the country in a fiscally responsible direction.

There is no substitute for the commitment to work together in a balanced way to reduce projected deficits. Suggested shortcuts, such as establishing a blue-ribbon deficit-reduction panel and forcing Congress to vote up-or-down on its recommendation or putting so-called triggers and automatic cuts in place to try to force policymakers to address the problem, are no substitute for the commitment of a wide array of policymakers to work together to accomplish the goal.

The 1983 Social Security commission — the Greenspan commission — is often cited as a commission that was successful in achieving a difficult fiscal goal. But it is important to remember that the commission did not convince policymakers to compromise. President Reagan, House Speaker Tip O’Neill, and other Congressional leaders were already committed to working together to extend the solvency of Social Security when the commission was appointed (by executive order after consultation with Congressional leaders, not by statute) specifically to facilitate the negotiations needed to develop a bipartisan plan and to help build public support for the eventual plan. It is also important to remember that the commission’s recommendation went through the normal Congressional process, with Committee markups and floor amendments considered and adopted in the House and Senate. In fact, one of the key elements of the plan ultimately adopted — delaying the normal retirement age — was not in the commission proposal, but was added in an amendment adopted in the House.

It is also important to remember the failed history of attempts to put in place automatic budget procedures that are intended to force the President and the Congress to work together to enact deficit reduction whether they are committed to doing that or not. The 1985 enactment of the Gramm-Rudman-Hollings fixed deficit targets (with a balanced budget required by 1991) enforced by automatic cuts in federal spending was intended to force the President and Congress to address the large deficits facing the nation at that time. In a 1993 report, CBO explained what actually happened:

“… agreement could not be reached on enough real, permanent deficit reduction to lower the deficit to the statutory level. Instead, the legal requirement to meet the targets was satisfied by using overly optimistic economic assumptions and outright budget gimmickry, such as shifting military pay dates between fiscal years and moving costly spending off budget.”[8]

The actual deficits exceeded the targets by growing amounts every year. In 1990, the last year the deficit targets were in effect, the actual deficit exceeded a revised target enacted in 1987 by $121 billion. Gramm-Rudman-Hollings was repealed in 1990 and replaced by the Budget Enforcement Act procedures. That Act included a statutory pay-as-you-go rule and discretionary caps, which were intended to keep the President and Congress from undoing the deficit reduction they had enacted in the same bill. Those new budget procedures were not intended to force them to reach an agreement in the future. In its 1993 report, CBO concluded:

“The experience under Gramm-Rudman-Hollings demonstrated that if the President and the Congress are unwilling to agree on a painful deficit reduction package, it is unlikely that any budget procedure can force them to agree. Instead, budgetary legerdemain is likely to be used to meet the letter of the law, and the hard decisions that would achieve real, permanent deficit reduction will still be avoided.”[9]

Since there is no substitute for the strong commitment of the President and leaders of both parties in Congress to work together to put the country on a fiscally sustainable path, every effort should be made to help engender such a commitment by educating policymakers and the public on the need to make tough choices rather than spending time considering and enacting new commissions or budget procedures that may give the false impression of progress toward the goal of fiscal responsibility but are doomed to failure if policymakers are not ready to make them work.

End Notes

[1] Richard Kogan, Matt Fiedler, Aviva Aron-Dine, and James Horney, “The Long-Term Fiscal Outlook is Bleak: Restoring Fiscal Responsibility Will Require Major Changes to Programs, Revenues, and the Nation’s Health Care System,” Center on Budget and Policy Priorities, January 29, 2007.

[2] Moreover, the debt at the end of WWII was held almost entirely by Americans — almost none was held by foreign governments or foreign citizens — and mush of the debt had been borrowed at a 2 percent interest rate and so was a far smaller burden than it would otherwise have been.

[3] “The Long-Term Budget Outlook,” Congressional Budget Office, December 2007, p. 1.

[4] See Richard Kogan and Aviva Aron-Dine, “There is No General “Entitlement Crisis”: In Coming Decades, Medicare, Medicaid, and Social Security Will Grow Rapidly, But Other Entitlements Will Shrink As a Share of the Economy,” Center on Budget and Policy Priorities, January 29, 2007.

[5] “The Long-Term Outlook for Health Care Spending,” Congressional Budget Act, November 2007.

[6] Ibid, p. 6.

[7]Comptroller General David Walker, “Long-Term Fiscal Issues: The Need for Social Security Reform,” Testimony before the Committee on the Budget, U.S. House of Representatives, February 9, 2005, p. 18.

[8] Congressional Budget Office, “The Budget Process and Deficit Reduction,” Chapter Six of The Economic and Budget Outlook: Fiscal Years 1994 – 1998, January 1993, p. 87.

[9] Ibid.