High Cost of Thomas Proposal Reflects the Low Effective Tax Rates Estates Would Face Proposal’s Benefits Would Go Primarily to Largest Estates

On June 22, the House passed legislation to sharply reduce the estate tax, and the Senate may vote on the legislation next week. Introduced by House Ways and Means Committee Chairman Bill Thomas, the measure would exempt the first $10 million of an estate for a couple ($5 million for an individual) and would index this exemption for inflation after 2010. It would tie the estate tax rate to the capital gains rate, which is now 15 percent and is currently slated to return to 20 percent after 2010. Under the proposal, the value of a couple’s estate that falls between $10 million and $25 million would be taxed at the capital gains rate, and the portion above $25 million would be taxed at twice the capital gains rate.

The Joint Committee on Taxation finds that the Thomas plan would cost $283 billion between 2007 and 2016, with a cost of $62 billion, or 76 percent as much as full repeal, in 2016. But these Joint Tax Committee estimates assume that the capital gains rate will revert to 20 percent as scheduled in 2011. If the lower capital gains rate is extended, as the White House and the Republican Congressional Leadership intend, the Thomas plan’s cost would exceed 80 percent of the cost of repeal.

Proposal Ties to Capital Gains Rate, But the Effective Tax Rate Estates Pay is Lower

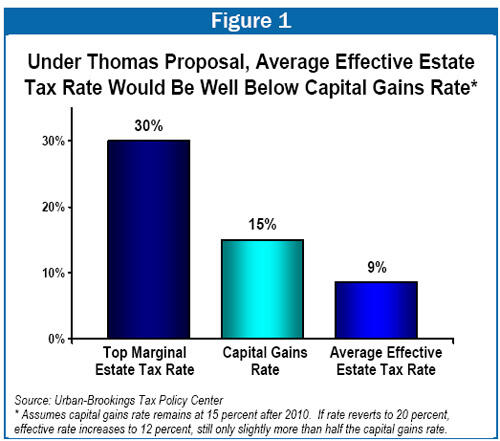

New data from the Urban Institute-Brookings Institution Tax Policy Center help to explain why the revenue losses from the Thomas proposal are so large. The data show that the fraction of an estate that is actually paid in taxes — known as the effective tax rate — would average less than one-third the top estate tax rate. Notably, this means that the effective estate tax rate would be far lower than the capital gains tax rate.

If the capital gains rate remains at 15 percent, in which case the top estate tax rate would be 30 percent, the average effective estate tax rate under the Thomas proposal would be only 9 percent (see Figure 1). Even if the capital gains rate reverts to 20 percent, producing a top estate tax rate of 40 percent, the average effective estate tax rate still would be 12 percent, or a little more than half the 20 percent capital gains rate that would be in place. The average effective estate tax rate also would be far lower than the federal payroll and income tax rates that workers typically face.

The effective estate tax rate is so far below the statutory estate tax rates because no estate tax is owed on the portion of an estate’s value that is below the exemption level. Under the Thomas proposal, a couple with an estate valued at $11 million would owe estate tax on $1 million at most. Further, some or all of the remaining value of an estate can be shielded from tax through available deductions, including for charitable bequests. (Many estates also employ planning devices to shrink the size of the estate before taxes are calculated. Such planning devices are not taken into account in the Tax Policy Center calculations, so the TPC estimates may actually understate true effective estate tax rates.) In contrast, capital gains tax is typically paid on the full value of realized capital gains.

Thus, while the Thomas proposal would tie the estate tax rate to the capital gains rate and would set the top estate tax rate at twice the capital gains rate, the average effective estate tax rate would be closer to half the capital gains rate.

Moreover, even the largest estates — those valued at more than $20 million — would pay tax at rates averaging less than the capital gains rate, even though they would face a top marginal rate equal to twice the capital gains rate. The reason is that these estates would pay the higher rate only on the value of the estate above $25 million. For example, if the capital gains rate remains at 15 percent, a couple with an estate valued at $26 million would pay no tax on the first $10 million (which is shielded by the exemption), a 15 percent rate on the value of the estate between $10 and $25 million, and a 30 percent rate only on the $1 million portion of the estate’s value that falls above $25 million. (This also helps explain why the largest estates would receive the largest tax cuts under the Thomas proposal, as discussed below.)

In order for the average effective estate tax rate to come close to the capital gains rate, a higher statutory tax rate would be needed. For instance, with a $3.5 million exemption and a 45 percent top rate — as will be in place in 2009— the average effective tax rate would be 17 percent (in between the 15 and 20 percent capital gains rates). Not surprisingly, making 2009 law permanent would preserve a far larger share of estate tax revenue than the Thomas proposal: it would cost 45 percent as much as full repeal, rather than three-quarters as much or more.

Thomas Proposal Offers Huge Tax Breaks for Wealthiest Estates

If the capital gains rate is allowed to revert to 20 percent, the Thomas proposal would cost about two-thirds more than making permanent the 2009 estate tax levels (a $3.5 million exemption — $7 million per couple — and a 45 percent rate). This additional cost — $25 billion in 2016 alone, according to the Joint Tax Committee estimates — would go toward tax breaks for the 3 of every 1,000 estates that would owe any estate tax under the 2009 levels. (Under 2009 law, the estates of 997 out of every 1,000 people who die will be entirely exempt from the tax.) If the capital gains rate remains at 15 percent, Joint Tax Committee figures suggest that the costs of the Thomas plan would exceed the cost of making the 2009 levels permanent by about $30 billion in 2016.

In either case — whether the capital gains rate remains at 15 percent or rises to 20 percent — the distribution of the tax-cut benefits of the Thomas proposal, even among the 3 in 1,000 estates that would benefit at all, is highly skewed. As Table 1 shows:

| Table 1: | ||

| Estate Value | Average Tax Cut | Share of Total Tax Cut |

| Less than $3.5 million | $0 | 0% |

| $3.5 million - $5 million | $291,000 | 5% |

| $5 million - $10 million | $738,000 | 23% |

| $10 million - $20 million | $1.9 million | 29% |

| Above $20 million | $5.6 million | 43% |

| Total | $1.4 million | 100% |

| Source: Urban-Brookings Tax Policy Center. * Table assumes that capital gains rate remains 15 percent. If it reverted to 20 percent, the distributional picture would change only slightly; see text. | ||

-

Those few estates that benefit from the Thomas proposal — relative to making the 2009 estate tax law permanent — would receive tax breaks that average $1.4 million apiece in 2011.

-

95 percent of the additional cost of the Thomas proposal (relative to the cost of making the 2009 levels permanent) would fund additional tax reductions for estates larger than $5 million, and 72 percent of the additional cost would fund additional tax reductions for estates worth more than $10 million.

-

43 percent — almost half — of the additional cost of the Thomas proposal would be spent on additional tax cuts for estates worth over $20 million. These estates (the 800-900 nationwide that would owe any tax under 2009 law — or the estates of 3 of every 10,000 people who die) would get additional tax cuts averaging $5.6 million each.

-

By contrast, only 5 percent of the added cost of the proposal would go for additional estate tax reductions for estates with a value of less than $5 million. For estates in this category, the Thomas plan adds relatively little relief relative to making 2009 estate tax law permanent.[1]

End Notes

[1] If the capital gains rate rises to 20 percent, 93 percent of the additional cost of the proposal relative to freezing 2009 law will go towards tax breaks for estates larger than $5 million and 34 percent towards providing tax cuts averaging $3.4 million to estates larger than $20 million.

More from the Authors

Areas of Expertise