“Generational Accounting” Is Complex, Confusing, and Uninformative

Generational accounting purports to compare the effects of budget policies on people born in different years, but it suffers from numerous problems of complexity, logic, and validity. It’s hard to interpret and easily misunderstood, and including it in regular budget reports and cost estimates, as the proposed Intergenerational Financial Obligations Reform (INFORM) Act would require, would be a mistake.[1]

Developed by a group of economists in the early 1990s, generational accounting was supposed to provide useful information that standard budget presentations did not — with some proponents even advocating that generational accounting replace those standard presentations. But, in fact, generational accounting provides little valuable information, and few budget analysts have made use of this approach. While analyses from the Congressional Budget Office (CBO) and other leading budget analysts illustrate the long-run path of taxes and spending both in total and by major categories, showing what’s driving our fiscal challenges, generational accounting doesn’t do that.

Instead, generational accounting calculates “lifetime net tax rates” for each one-year cohort of the population through at least age 90 and a separate lifetime net tax rate for all future generations combined. Those measures are supposed to reflect the burden for each generation of taxes minus transfer payments (such as Social Security and Medicare) under existing budget policies. To calculate those measures, generational accounting projects such key variables as population growth, labor force participation, earnings, health care costs, and interest rates through infinity.

Yet budget experts recognize that projections grow very iffy beyond a few decades, and virtually no one tries to make them beyond 75 years. In addition, generational accounting relies on highly unrealistic assumptions that skew the results. For instance, its calculations of lifetime net tax rates assume there would be no changes whatsoever in current law for taxes or transfer policies for anyone alive — extending for the rest of their lives. Thus, it assumes that, to address the nation’s fiscal challenges, a President and Congress would apply all tax increases and spending cuts only to people not yet born.

Policymakers have never done that in the past, and they almost certainly will not in the future. Not surprisingly, this misleading approach understates the budget pressures facing people who are now alive while overstating the budget pressures facing those not yet born.

Moreover, the lifetime net tax rate of generational accounting is more complex than, and not comparable to, standard measures of tax burdens. Rather than measure total taxes as a percent of the economy or of household income, it measures net taxes as a percent just of labor income — which is only part of the economy and which makes tax burdens appear greater than they are. Furthermore, under the concept of net taxes, a reduction in Social Security or other transfer benefits translates into a higher net tax rate, which most people will find confusing. Also, generational accounting’s authors often express lifetime net tax burdens in raw dollars, which is especially misleading because it fails to relate those net taxes to lifetime income or some other measure of ability to pay. People could easily but mistakenly compare that lifetime net cost to their own (or the nation’s) current annual income, leading to an exaggerated view of the long-term budget problem.

Adding to these problems, generational accounting rigidly categorizes all government spending as a purchase or a transfer, a distinction that arbitrarily assigns burdens and benefits, often with little regard to their true distribution. Generational accounting also doesn’t account for the benefits that spending can have for future generations (for example, education and infrastructure spending that raises living standards), and it ignores the fact that the future economy will be larger. Future generations will have higher living standards and more disposable income even if they bear a reasonable increase in their net tax burden.

What Is Generational Accounting?

Economists Alan Auerbach, Jagadeesh Gokhale, and Lawrence Kotlikoff developed the concept and methods of generational accounting over 20 years ago.[2] It enjoyed some time in the spotlight in the 1990s but, for a host of legitimate reasons, it has not become a common part of the budget analyst’s toolkit.

Generational accounting starts with the reality that all government spending must be paid for by someone — by past, current, or future generations. That is, over the infinite future, taxes must be sufficient to pay for all government purchases of goods and services, transfer payments, and debt service.[3] Economists dub that the “inter-temporal budget constraint.” (For more on that concept, see Appendix 1.)

Auerbach, Gokhale, and Kotlikoff extend that logic to calculate what they call the lifetime net tax rate, which tries to measure the burden of taxes minus transfer payments on a generation over its lifetime. They calculate a lifetime net tax rate separately for current and future generations — a rate for each one-year age cohort from newborns through at least age 90, and a single composite rate for all future generations not yet born. Each of these lifetime net tax rates reflects a generation’s tax payments made minus transfers received, displayed as a percentage of its lifetime labor income. All of these calculations are on a present-value basis, which means that future spending and revenues that occur over many decades are converted into a single figure, in today’s dollars, called a “lump-sum equivalent.”

In addition, the calculations assume that current budgetary policies continue for the rest of a person’s life for anyone who is already alive — that the President and Congress make no changes in current tax and transfer policies for those people. The lifetime net tax rate for future generations — those not yet born — then flows from that assumption; it shows how much future generations would have to pay if all those who are already alive are wholly exempt for the rest of their lives from any changes in fiscal policies.

Generational accounting presumes that “generational balance” is an important standard — that the net tax rate for current and future generations should be the same. If the net tax rate for future generations exceeds the net tax rate for newborns, the proponents of generational accounting conclude that fiscal policy is out of generational balance.[4] But as we explain below, this criterion does not make sense.

The earliest generational accounts attempted to estimate the lifetime net tax rate necessary to finance all levels of government (federal, state, and local) and projected lifetime net tax rates on future generations at extremely high levels — as high as 80 or 90 percent.[5] Some more recent analyses cover only the federal government and more thoroughly incorporate future changes in spending and tax policy that are already scheduled in law. They project net tax rates at a dramatically lower level.

For instance, a 2011 staff paper from the International Monetary Fund (IMF) provides the most recent generational accounting estimates for the federal budget.[6] Based on CBO’s June 2010 long-term budget outlook, the IMF paper showed two fiscal scenarios — one following current law, including the assumption that policymakers would let the 2001 and 2003 tax cuts expire, as the law then dictated, and the other based on CBO’s more pessimistic alternative that assumed, among other things, that policymakers would act to make all of those tax cuts permanent.[7] Under the former scenario (with the tax cuts expiring), the IMF staff estimated that the lifetime net tax rate on future generations would be 10 percent, compared to 6 percent on newborns (the youngest current generation). These figures are far below the earliest 80-percent or 90-percent projections cited above.

But, although policymakers subsequently extended most of those tax cuts, calculations of net tax rates today would probably be still lower than the IMF’s figures. That’s because the IMF staffers made these calculations before a series of important legislative and other changes that will significantly reduce the nation’s fiscal challenges. Those changes include the 2011 Budget Control Act, which constrains future discretionary spending, and the recent slowdown in health care cost growth.

Finally, in recent papers, Gokhale and Kotlikoff present their estimates of net taxes in dollars.[8] Dollar estimates are especially uninformative, because they do not provide essential context. It’s one thing to say, for instance, that someone owes $10,000 in taxes; it’s another to put it in context by revealing the person’s income. Expressing net taxes in relation to income puts them in proper perspective. And many readers may easily miss the fact that generational accounting calculates lifetime net taxes and therefore mistakenly compare a generation’s lifetime net taxes in dollars to its (or the nation’s) current annual income, which would grossly exaggerate the tax burden.

Generational Accounting Is Complex and Hard to Understand

Early on, generational accounting’s biggest proponents greatly overstated its potential usefulness. Kotlikoff asserted that standard concepts of revenues, outlays, and deficits are “devoid of economic content” and have “repeatedly led us astray.”[9] Some backers even argued that generational accounting should replace conventional budget bookkeeping. That has not happened, because — as a 1998 staff paper for a Presidential commission noted — generational accounting “does not perform the most basic function of a budget, which is to propose and enact an allocation of resources among different programs for a specified period.”[10]

But, even to supplement standard concepts rather than replace them, generational accounting is problematic. Its methods and conclusions are not easy to understand. Even professional economists find the calculations complex and highly sensitive to sometimes arbitrary assumptions. And, as noted, they are implausible in at least one fundamental way: they unrealistically assume that Congress will impose all needed budget changes exclusively on generations not yet born, sparing every individual who’s now alive.

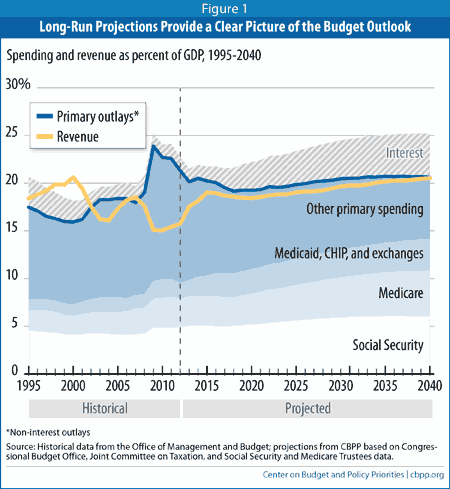

In contrast to generational accounting, the Office of Management and Budget (OMB), CBO, the Center on Budget and Policy Priorities (CBPP), and other organizations provide budget projections for both the short and long run that are relatively straightforward. They show the path of federal revenues and of major categories of spending (such as Medicare and Medicaid, Social Security, other programs, and interest). In that way, they show clearly what’s driving longer-term fiscal pressures, and when. (For an example, see Figure 1.[11])

Policymakers and citizens naturally focus on key budget decisions — tax rates, benefit formulas and eligibility rules, appropriation amounts, and so forth — for a fiscal year or for a decade. They are not used to seeing the lifetime value of important parameters summarized in a single present-value figure, and they can’t reasonably make decisions about specific future taxes and spending programs on that basis. In short, standard budget presentations — like those summarized in Figure 1 — are a far clearer way of showing long-term budget pressures than generational accounting, and are readily available. In this respect, generational accounting attempts to solve a non-existent problem, and in a way that’s very easy to misunderstand.

Image

Generational Accounting’s “Lifetime Net Tax Rate” Is Misleading

Generational Accounting’s “Lifetime Net Tax Rate” Is Misleading

The main product of generational-accounting calculations is the so-called lifetime net tax rate on current and future generations. But that tax rate has a very specialized meaning and will likely be misinterpreted.

The implication of generational accounting — that a baby born yesterday and one born tomorrow will face wildly different net tax rates — is entirely unrealistic. In reality, lawmakers typically enact budget policies that affect people alive today as well as future generations.

If, for instance, a President and Congress decided to slow the growth of debt by raising taxes, they would not impose sharply higher tax rates on people born after today, while leaving tax rates untouched for everyone now alive. The same is true of cuts in spending programs. Yet generational accounting makes precisely that assumption when it calculates the net tax rate on future generations, and that assumption is key to the calculations. That’s why some estimates put the net tax rate for future generations at such an extraordinarily high level and show such a large difference between the net tax rate for newborns and the composite rate for those yet unborn. That’s also why the results are so broadly misunderstood.

The net tax rate is also not comparable to standard measures of tax rates for another reason. OMB, CBO, and other budget analysts typically depict taxes as a percentage of the economy — as measured by the gross domestic product (GDP) — or as a percentage of a person’s or household’s income. Generational accounting, however, expresses net tax rates as a percentage of labor income. Yet labor compensation represents only about 55 percent of GDP. If, then, someone uses labor income as the denominator in calculating net tax rates, the net tax burden will look artificially high.

Moreover, under calculations of net tax rates, benefit reductions in Social Security or Medicare or other transfer programs show up as an increase in the net tax rate. That’s because, as previously noted, generational accounting defines net taxes as taxes minus transfers. Readers will find it hard to grasp that cutting government programs increases the net tax rate. And policymakers will have a very hard time deciding what to do if they think that the net tax rate on future generations is too high and want to reduce it.

In short, the lifetime net tax rate is abstract, unfamiliar, and misleading, and it’s difficult to see how policymakers can put it to practical use.

Projections Through Infinity Are Not Valid

Generational accounting requires its practitioners to project the future size of the population, labor force participation and earnings, taxes, transfers, government purchases, interest rates, and many other variables through infinity — that is, forever. Technically, the calculations are simple enough with today’s computing power. The problem is that making projections over an infinite horizon has serious pitfalls.

The further out one looks, the more uncertain projections become. That’s why budget experts generally agree that projections grow very iffy after a few decades and virtually nobody projects beyond 75 years. The Social Security actuaries, for example, estimate with 80 percent confidence that Social Security outlays will be between 5.4 and 6.9 percent of GDP in 2038 and between 3.7 percent and 7.7 percent of GDP in 2087.[12] For the major health-care entitlements, CBO estimates that the debt-to-GDP ratio in 2038 could differ by 30 percentage points if annual excess cost growth (that is, the amount by which the growth of health care costs per beneficiary exceeds the growth of GDP per person) were 0.5 percent lower or 0.5 percent higher than CBO’s central assumption.[13] “Because the uncertainty of budget projections increases the farther the projections extend into the future,” CBO writes, “this report focuses on the next 25 years.” So, too, does CBPP’s most recent report on long-run projections.

The American Academy of Actuaries cautions that even the 75-year Social Security projections are highly uncertain and that infinite-horizon projections are largely useless:

With regard to the infinite-time-period estimates, the [Academy’s Social Insurance Committee] begins its analysis by noting that the results of the 75-year statutory valuation are themselves subject to extreme uncertainty. Consider the situation of actuaries or economists in the year 1928 attempting to project demographic and economic parameters 75 years into the future — to 2003. They likely would have missed the Great Depression, World War II, the baby boom, the influx of women into the labor force, etc. Nobody, no matter how intelligent or educated, could have anticipated these very significant events . . . . Given the uncertainty of projections 75 years into the future, extending the projections into the infinite future can only increase the uncertainty, rendering the results of limited value to policymakers.[14]

For generational accounting, the projections require that practitioners choose levels or growth rates for many interdependent variables, with sensitive implications. One critical variable is the discount rate, or interest rate, which converts future dollar flows into present-value terms.

The choice of a discount rate, though largely arbitrary, significantly affects the estimated net tax rate on future generations.[15] Early practitioners of generational accounting generally used a real interest rate — that is, a rate in excess of inflation — of 6 percent; more recent ones have generally used 3 percent, which is close to the rate that the Social Security actuaries assume. Relatively small differences between the discount rate and the growth rate of earnings and of per-capita health care costs can have profound effects on the net tax rate, yet no one can project those variables with confidence.

In short, budget and economic forecasts are highly uncertain — and spinning them out to infinity makes them dramatically more so. That’s why CBO and other leading budget analysts focus on the next three decades or so for long-run budget estimates, which amply documents future fiscal pressures and presents a reasonable horizon for policymakers.

Generational Accounting Ignores Benefits of Government Spending

Generational accounts categorize all government spending either as a purchase or a transfer. The distinction is often arbitrary — for example, public support to elementary and secondary education is a purchase, while a direct grant, loan, or tax credit to a college student is a transfer, though all such spending can boost younger generations’ earning power and reduces what they (or their parents) pay for their education. Yet the distinction matters greatly for generational accounting because, as previously noted, generational accounting calculates the lifetime net tax rate by subtracting transfer payments but not government purchases from tax payments. The arbitrary nature of this distinction, which we have illustrated, is another reason to be skeptical of the estimates produced by generational accounting.

Government spending in one year can substantially benefit younger generations. Spending on education, infrastructure, and research and development can promote economic growth. Spending on national defense, environmental protection, law enforcement, and financial regulation can provide Americans with extra security. Spending on income security and health care for the young can boost their economic opportunities, while such spending for the old insures them against economic risk and against dependence on their children. Social Security and Medicare make it less likely that children will have to help pay their parents’ medical or other bills. Generational accounting misses this interdependence. For example, if Social Security benefits were cut for both present and future generations, the benefit cut for people now alive would show up as a reduction in the net tax rate for unborn generations. But the costs of supporting the elderly in their retirement would not disappear; future children would have a correspondingly greater need to support their parents from their own resources.

By mechanically calculating the net tax rates of different generations, generational accounting fails to consider the benefits of government spending for different and interdependent generations. Generational accounting also ignores other private and public activities through which earlier generations improve the living standards or quality of life of later ones — for example, parents’ investment in their children’s education or government regulations that protect the environment.[16]

To be fair, the proponents of generational accounting do not deny these effects, but they make no effort to allocate them between generations. As former CBO director Rudolph Penner put it, generational accounting “counts only what is easily countable. . . . Thus, for example, the ‘greatest generation’ — the generation that won World War II — gets no credit for its contribution to the welfare of future generations.”[17]

Nobel-prize winning economist Peter Diamond offers even more sweeping criticism: “Since the [generational accounting] framework does not value [government] services but only recognizes the cost of producing them, this is an inadequate picture of intergenerational fiscal relations… I do not think that generational balance calculated as it is currently is a good basis by itself for identifying either equitable policies or good ones.”[18]

Generational Accounting Ignores Future Increases in Living Standards

In estimating the tax burden that we are passing on to our children and grandchildren, generational accounting ignores the fact that, as a whole, they will be richer than we are and, thus, better positioned to pay somewhat higher taxes.

Social Security tax rates, for example, have risen from 2 percent of earnings in 1937 to 12.4 percent today (for employees and employers, combined). Yet nobody would dispute that an average worker is much better off today than at Social Security’s start, over 70 years ago, even after taxes. And under the Social Security trustees’ assumptions, the average worker will be almost 50 percent better off — in real terms — in 2040 than the average worker was in 2013, and twice as well off by 2070.[19] Future workers will have much higher after-tax income even if policymakers ask them to pay somewhat higher payroll taxes to support the program. Social Security is very popular, and poll respondents of all ages and incomes express a willingness to help support it through higher taxes.

Health costs are driving our long-term budget challenges far more than Social Security, and both budget projections and generational-accounting calculations are highly sensitive to the assumed growth in health spending. But as people — and societies — grow richer, they tend to devote a larger share of their income to health care; that’s because as we satisfy our material needs, what we value most is more years and better health in which to enjoy them with our children and grandchildren. That helps to explain why we should expect that government and private spending on health care would increase as living standards rise. And that, in turn, explains why it’s not necessarily unfair if future generations bear a somewhat higher net tax rate than the net tax rate for current generations. (Nevertheless, we should root out waste and inefficiency in the health care system wherever we can.)

Generational accounting, however, creates the impression that any increase in the net tax rate on a later generation leaves that generation worse off than earlier ones. Yet the opposite could well be true. A more meaningful comparison would be between the average real standard of living of one generation and another — a comparison that would include changes in both pre- and post-tax income and in health status.

Kotlikoff argues that “Generational balance is a prescription for stabilizing net tax rates across generations, so it will be a feature of a long-run social optimum. . . . [Tax rates] can’t forever rise or fall.”[20] But although tax rates certainly can’t rise forever, the nation and its people can assume manageable tax increases, including those from curbing unproductive or low-priority tax expenditures, that would help stabilize our fiscal outlook and still leave U.S. tax levels well below those of other advanced countries.[21]

Conclusion

Policymakers should care about how their decisions affect future generations. Fiscally responsible lawmakers raised such concerns when President Bush and Congress decided — by enacting the 2001 and 2003 tax cuts, fighting the Iraq and Afghanistan wars with borrowed money, and adding a new prescription-drug benefit to Medicare without fully paying for it — to push the bill to future generations. But policymakers widely understood the budgetary effects of those decisions at the time, using standard budget analyses. They didn’t need generational accounting to corroborate it. And there’s no reason to think that policymakers would have decided differently if generational accounting estimates were also available.

Policymakers have many tools to gauge long-run fiscal sustainability and assess generational equity that are more straightforward and understandable than generational accounting. CBO produces an annual assessment of the long-run budget outlook, including projections of the major categories of spending and revenues and calculations of the so-called fiscal gap. (See Appendix 2.) CBO and the programs’ actuaries prepare long-run estimates of Social Security and Medicare taxes and spending. CBO’s estimates of major budget proposals — such as the Affordable Care Act and immigration reform — often include analyses of their impact over several decades.

Generational accounting may be an interesting academic exercise, but it provides little, if any, solid, useful information beyond what’s available in long-range budget projections. Moreover, generational accounting’s lifetime net tax rates are based on arbitrary assumptions, hard to understand, inherently misleading, and likely to be misunderstood and misused. Generational accounting should not be part of the regular budget outlook or of major cost estimates, and enactment of the INFORM Act would be a mistake.

Appendix 1

WHAT IS THE “BUDGET CONSTRAINT”?

Generational accounting relies on what economists call the “inter-temporal budget constraint.” Simply put, that is:

Present value of future net taxes

= Current net government debt + Present value of future purchases

In this depiction:

- Present value means that future dollar streams — projected through infinity — are expressed (or “discounted”) as their lump-sum equivalent in today’s dollars. The Treasury’s interest rate is used to calculate the lump-sum equivalent of future dollar streams because the budget constraint applies to payments to and from the Treasury over time.

- Net taxes are all taxes collected in the future, minus the value of transfer payments made by programs such as Social Security, Medicare, and Medicaid.

- Net government debt is government financial liabilities — in the case of the federal government, essentially debt held by the public — minus the government’s financial assets.

- Purchases are government spending for everything other than transfer payments — for example, for defense, scientific research, public education, infrastructure, law enforcement, and national parks.

In a nutshell, the budget constraint means that, over time, the government must collect enough taxes to pay for government purchases and transfers and to service its debt.

Appendix 2

WHAT IS THE "FISCAL GAP"?

The fiscal gap is a way to express — in a single figure — the government’s budget imbalance over some period of time. It tells us how large the policy changes would have to be, over those years, to keep debt at the end of the period from exceeding today’s level of debt as a percentage of the gross domestic product, or GDP.

In its latest long-term projections, issued in September 2013, CBO puts the fiscal gap for the next 25 years at 0.8 percent of GDP. Over the next 50 years, it’s 1.5 percent of GDP, and over 75 years, 1.7 percent of GDP. That growth, while of concern, cannot be characterized as explosive. (CBO emphasizes the 25-year projection because longer-run extrapolations are so uncertain.)

Unlike generational accounts, the fiscal gap doesn’t require complex and speculative projections through infinity. And it’s relatively straightforward to translate into policy implications. For example, CBO has noted that closing the 0.8-percent-of-GDP fiscal gap through 2038 would call for a 4½ percent increase in revenues, a 4½ percent reduction in non-interest spending, or some equivalent combination. That’s ambitious but attainable. And those estimates are far easier to understand than generational accounting’s lifetime net tax rates.

Closing the fiscal gap isn’t an ironclad budgetary requirement. The calculation of a fiscal gap simply assumes that the target debt at the end of the period matches today’s level as a percent of GDP. CBO’s latest calculation of the fiscal gap assumes that debt would be held to 73 percent GDP, its approximate value in 2013, at the end of 25, 50, or 75 years. In reality, it may be acceptable to have a somewhat higher debt ratio, as long as it eventually stabilizes. And it would be preferable to end with a lower debt level (as long as the policies enacted to achieve that reduction do not jeopardize economic recovery or long-term economic growth or harm vulnerable families and individuals).

The INFORM Act would direct that the fiscal gap be calculated over an infinite time horizon. In that special case, the fiscal gap is simply another way of expressing the inter-temporal budget constraint (see Appendix 1), but it shares all the pitfalls of budget and economic projections over such an absurdly long period.

End Notes

[1] H.R. 2967, introduced by Rep. Aaron Schock (R-IL), and S. 1351, introduced by Sen. John Thune (R-SD).

[2] Alan J. Auerbach, Jagadeesh Gokhale, and Laurence J. Kotlikoff, “Generational Accounts: A Meaningful Alternative to Deficit Accounting,” in Tax Policy and the Economy, Volume 5 (Cambridge: MIT Press, 1991), http://www.nber.org/chapters/c11269.

[3] Generational accounting does not assume that future generations ever have to pay off the debt, but it does assume that they have to keep up the interest payments. In present-value terms, those are equivalent.

[4] Jagadeesh Gokhale, Benjamin R. Page, and John R. Sturrock, “Generational Accounts for the United States: An Update,” in Generational Accounting Around the World (Chicago: University of Chicago Press, 1999), http://www.nber.org/chapters/c6703.pdf.

[5] Congressional Budget Office, Who Pays and When? An Assessment of Generational Accounting, November 1995, http://www.cbo.gov/sites/default/files/cbofiles/attachments/Genacct.pdf.

[6] Nicoletta Batini, Giovanni Callegari, and Julia Guerreiro, An Analysis of U.S. Fiscal and Generational Imbalances: Who Will Pay and How?, International Monetary Fund Working Paper WP/11/72, April 2011, http://www.imf.org/external/pubs/ft/wp/2011/wp1172.pdf.

[7] CBO’s pessimistic alternative assumed that most of the 2001 and 2003 tax cuts would be continued, revenues in the long run would not exceed 19 percent of gross domestic product (GDP), spending for programs other than the major entitlements would remain constant as a share of GDP, and certain cost-control provisions of health reform would not remain in effect after 2020. See Congressional Budget Office, The Long-Term Budget Outlook, June 2010. Under that pessimistic case, the IMF calculated that net tax rates would rise from a negative 5 percent for newborns (indicating that they would collect more from government than they would pay in taxes) to positive 17 percent for future generations.

[8] Jagadeesh Gokhale, Fiscal and Generational Imbalances and Generational Accounts: A 2012 Update, Cato Institute Working Paper, November 2012, http://www.cato.org/publications/working-paper/fiscal-generational-imbalances-generational-accounts-2012-update; Giovanni Callegari and Laurence J. Kotlikoff, “Estimating the U.S. 2013 Fiscal Gap,” The Can Kicks Back, August 2013, http://d3n8a8pro7vhmx.cloudfront.net/tckb/pages/284/attachments/original/1378836788/EstimatingThe_U.S._2013_Fiscal_Gap_-_The_Can_Kicks_Back.pdf?1378836788.

[9] Lawrence J. Kotlikoff, quoted in William A. Niskanen, “Book Review, Generational Accounting: Knowing Who Pays, and When, for What We Spend,” Cato Journal, Fall 1992, http://www.cato.org/sites/cato.org/files/serials/files/cato-journal/1992/11/cj12n2-14.pdf.

[10] Staff Paper Prepared for the President's Commission to Study Capital Budgeting, April 21, 1998, available at http://clinton2.nara.gov/pcscb/staf_genacc.html.

[11] Richard Kogan, Kathy A. Ruffing, and Paul N. Van de Water, Long-Term Budget Outlook Remains Challenging, But Recent Legislation Has Made It More Manageable, Center on Budget and Policy Priorities, June 27, 2013, https://www.cbpp.org/cms/index.cfm?fa=view&id=3983.

[12] The 2013 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, May 2013, http://www.socialsecurity.gov/OACT/TR/2013/index.html, Table VI.E1, and personal communication from the Social Security Administration’s Office of the Chief Actuary.

[13] CBO, The 2013 Long-Term Budget Outlook, September 2013.

[14] Eric J. Klieber to Trustees of the Social Security System, December 19, 2003, http://www.actuary.org/pdf/socialsecurity/tech_dec03.pdf. The Academy stated that such infinite-horizon projections would be useful chiefly if they were “used exclusively to identify an ultimate reversal of an apparent trend demonstrated in the 75-year projection,” which is clearly unlikely.

[15] Dean Baker, Robbing the Cradle? A Critical Assessment of Generational Accounting, Economic Policy Institute, 1995.

[16] It also ignores the bequests that people leave to later generations. See Willem H. Buiter, “Generational Accounts, Aggregate Saving and Intergenerational Distribution,” Economica, Vol. 61, No. 256 (November 1997), pp. 605-626.

[17] Rudolph G. Penner, “What Is Generational Accounting?” Rudolph G. Penner, “What Is Generational Accounting?” Tax Policy Briefing Book, Urban Institute-Brookings Institution Tax Policy Center, September 10, 2007, http://www.taxpolicycenter.org/briefing-book/background/taxes-budget/generational-accounting.cfm.

[18] Peter A. Diamond, “Generational Accounts and Generational Balance: An Assessment,” National Tax Journal, December 1996.

[19] Kathy A. Ruffing, What the 2013 Trustees’ Report Shows About Social Security, Center on Budget and Policy Priorities, June 18, 2013,https://www.cbpp.org/sites/default/files/atoms/files/6-18-13ss.pdf.

[20] Lawrence J. Kotlikoff, “Reply to Diamond and Cutler’s Reviews of Generational Accounting,” National Tax Journal, June 1997, p. 307.

[21] Chuck Marr, “Thinking About Tax Policy, Part 2: Taxes Today Are Low,” Center on Budget and Policy Priorities, Off the Charts blog, April 11, 2012, http://www.offthechartsblog.org/thinking-about-tax-policy-part-2-taxes-today-are-low/.

More from the Authors

Areas of Expertise

Areas of Expertise