Timing Gimmicks Pose Threat to Fiscally Responsible Corporate Tax Reform

Savings in First Decade Need to Continue in Second Decade

A key goal of tax reform should be to generate new revenue as part of a balanced deficit-reduction package that replaces sequestration and reduces long-term deficits.[2] Revenue savings can come from paring back costly and inefficient tax deductions, exclusions, and other tax breaks, known collectively as “tax expenditures.” And given that the nation faces long-term fiscal challenges, policymakers should design tax reform to ensure that the savings achieved during the first decade continue in the following decade.

That’s the standard Congress imposed in crafting health reform legislation in early 2010 and that the Senate recently used for immigration reform: the fiscal target for the first ten years must also be met for the second ten years.

Tax reform should be held to the same standard. Policymakers must resist using timing shifts that accelerate revenue from subsequent decades into the first ten years, as well as one-time revenue raising measures, to help meet their fiscal target for the initial decade — especially if such tax changes are coupled with rate reductions and other policies that have permanent costs. Such a combination would erode savings over time and could result in swelling long-run deficits.

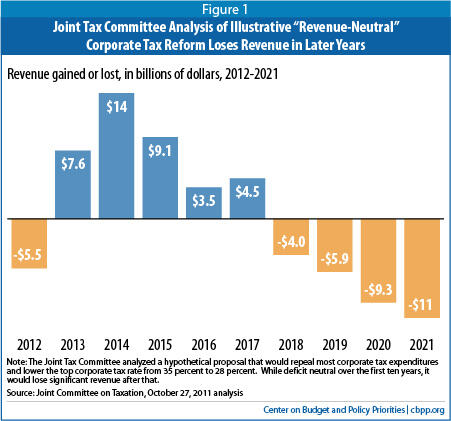

The temptation to use timing gimmicks is particularly serious in corporate tax reform, because many corporate tax subsidies are structured in such a way that scaling them back would generate much larger savings in the first ten years than over the long run.[3] As a result, a tax reform package that paired such cuts in corporate tax subsidies with permanent corporate rate cuts, which grow more costly over time, might shrink deficits initially but expand them significantly thereafter. For example, an analysis that the Joint Committee on Taxation (JCT) issued in 2011 found that a potential corporate tax-reform package that was revenue neutral over the ten-year budget window would produce annual revenue losses that would start before the end of the decade and grow over time.[4] (See Figure 1.) Timing gimmicks pose a danger in individual tax reform as well (see box).

Policymakers should therefore insist on holding tax reform to a fiscal standard that extends beyond just the first decade.

Such a fiscal standard is not new. Congressional Democrats revised the health reform bill at the end of the legislative process in early 2010 to trim subsidies to purchase health coverage in the exchanges and to tighten the excise tax on high-cost health insurance plans, in order to ensure that the legislation would reduce the deficit in the second ten years as well as the first ten, under Congressional Budget Office (CBO) estimates. Likewise, the Senate “Gang of 8” designed the immigration bill that the Senate recently passed so that CBO would find that the bill would reduce deficits in the second decade as well as the first.

Timing Gimmicks Also a Danger in Individual Tax Reform

While most large corporate tax expenditures are structured in such a way that eliminating or scaling them back raises significantly less revenue after the first decade, this is not the case for most individual income tax expenditures. Nevertheless, some individual tax reforms could be used as timing gimmicks to hit tax reform’s revenue goals in the first decade but not after that.a A provision of January’s American Taxpayer Relief Act (ATRA) dealing with employer-sponsored retirement accounts is a clear example.

Amounts deposited in employer-sponsored retirement accounts like 401(k)s and 403(b)s are exempt from income tax when the deposits are made, but withdrawals in retirement are taxable. Some employers also offer “Roth” accounts, in which contributions are taxed up front but withdrawals in retirement are tax free. Prior to ATRA, taxpayers could shift money from accounts like a 401(k) into a Roth account only in very limited circumstances.

ATRA loosened the rules, allowing individuals to shift large sums (even their entire balances) from 401(k) and 403(b) accounts to a Roth account at any time. They would have to pay tax on the amounts shifted, but all subsequent earnings in the Roth accounts — and all withdrawals in later years — would be tax free. This maneuver raises revenue in the early years because people making the shift would pay income tax on the amounts that they moved to the Roth accounts — but loses revenue, and in larger amounts, outside the ten-year budget window. Only people who conclude they would pay less total tax over time will take advantage of this option, so the long-run effect will be a significant revenue loss.

This is not the first time that policymakers have adopted such a timing gimmick to disguise an individual income tax cut as a tax increase. Similar changes were made in 2006.b A future tax reform package could use changes in retirement savings rules and other provisions as timing gimmicks.

a See Chye-Ching Huang and Nathaniel Frentz, “Four Timing Gimmicks That Could Disguise Fiscally Irresponsible Individual Tax Reform,” Center on Budget and Policy Priorities, October 30, 2013, https://www.cbpp.org/cms/index.cfm?fa=view&id=4041.

b Joel Friedman and Bob Greenstein, “Joint Tax Committee Estimate Shows That Tax Gimmick Being Designed To Evade Senate Budget Rules Would Increase Long-Term Deficits,” Center on Budget and Policy Priorities, Revised April 26, 2006, https://www.cbpp.org/cms/?fa=view&id=220.

To illustrate the risk that timing gimmicks pose to fiscally responsible tax reform, this paper briefly discusses three prominent corporate tax reform options: ending accelerated depreciation, ending “last-in, first-out” accounting (LIFO), and adopting a territorial tax system. Proposals in these areas could raise significant revenue initially, but the savings would fade outside the ten-year budget window (and a territorial system could cause large and growing revenue losses).

By itself, the fact that the savings from a given set of tax changes may diminish over time doesn’t mean the changes aren’t worth doing. The key issue is what policymakers do with the savings — whether they offset tax changes that lose revenue and grow in cost over time, creating a mismatch that can lead to higher deficits over the long run. When considering a given package of reforms, policymakers must take account of both its short- and long-term budgetary impacts.

Joint Tax Committee Analysis Highlights Risk of Timing Gimmicks

Eliminating nearly all major corporate tax expenditures would save $964 billion over 2012 to 2021, according to a 2011 JCT analysis. JCT stated that policymakers could use the savings to lower the corporate tax rate from 35 percent to 28 percent without adding to deficits in the first decade. However, JCT also found that this package would add significantly to deficits in later decades.

As Figure 1 (based on the JCT analysis) shows, the new revenues generated by eliminating corporate tax expenditures more than offset the cost of lower corporate tax rates for the first few years.[6] But, starting in the seventh year, the package would cause a net revenue loss that would grow each year — and would continue over the long run.

The JCT analysis explains that many of the corporate tax breaks eliminated to fund the rate cut would raise more revenue in the first ten years than in any later decade. These tax expenditures allow corporations to delay paying tax; eliminating them boosts revenues initially, as corporations pay taxes earlier, but savings decline after that initial burst of tax revenues. John Buckley has explained, “Today, there is only one large corporate tax preference that is not a timing change and that’s the deduction for the manufacturing sector.”

Accelerated Depreciation

The largest business tax subsidy, accelerated depreciation, allows businesses to deduct over time the cost of investments such as new equipment more quickly than those assets actually lose value. JCT’s analysis estimated that ending accelerated depreciation (so that businesses’ deductions would more closely reflect the rate at which assets deteriorate) would save $507 billion over the first ten years, or 53 percent of the total base-broadening savings in the JCT analysis. A number of prominent tax-reform plans — including the illustrative plan from Fiscal Commission co-chairs Erskine Bowles and Alan Simpson, the plan from former Office of Management and Budget and CBO director Alice Rivlin and former Senator Pete Domenici of the Bipartisan Policy Center, and the plan from Senators Ron Wyden and Dan Coats — rely on ending or scaling back accelerated depreciation to generate revenues for corporate rate cuts or deficit reduction.[7]

If policymakers ignored the long-run impacts, a corporate rate cut that policymakers could pay for in the first ten years by ending accelerated depreciation would raise deficits in the long run. Similarly, any deficit reduction achieved by ending accelerated depreciation would be significantly smaller in the long run than in the first ten years.

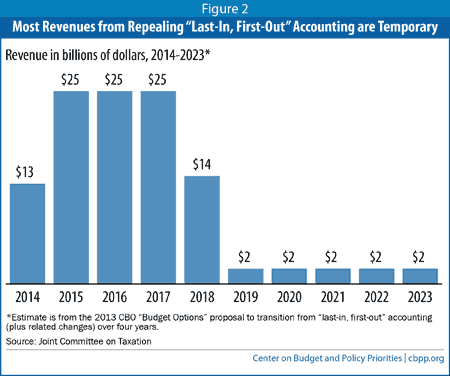

Last-In, First-Out Accounting (LIFO)

To calculate their taxable profits, businesses subtract from the income that they earn by selling goods what it cost them to produce or purchase these goods. “Last-in, first-out” accounting (LIFO) allows businesses generally to assign a higher cost to their goods for these purposes than other accounting methods do. This means that businesses using LIFO accounting can generally report lower taxable profits and therefore pay less in taxes.[10]

If policymakers repealed LIFO, these businesses would have to switch to the “first-in, first-out” (FIFO) accounting method. This would cause a large, one-time increase in their taxable income by forcing them to assign a new, lower cost to their existing inventories (that is, to the goods they have in stock but have not yet sold). To keep this one-time tax increase from causing some businesses cash-flow problems, proposals to repeal LIFO typically allow firms to spread the increase over a number of years.[11]

A Congressional Budget Office proposal to repeal LIFO would raise $112 billion over 2014 to 2023.[12] But, it also showed that the tax increase resulting from companies’ revaluation of their existing inventories is temporary. The change in valuing new stock in their inventories would produce only modest savings beyond the first five years, as Figure 2 shows.

International Tax Reform

The 2011 JCT analysis did not consider any changes to the international tax system, but policymakers could also use such changes as a timing gimmick.

The second-largest business tax expenditure, known as deferral, allows multinational corporations to delay paying U.S. taxes on their foreign profits until they choose to bring those profits back to the United States. This tax break cost $48.3 billion in 2013, according to JCT.[13] U.S.-based multinationals hold about $2 trillion[14] of foreign profits offshore, thereby deferring U.S. tax on these earnings.

Multinational corporations are calling for the United States to adopt a territorial tax system, which would give foreign profits even more favorable U.S. tax treatment by largely exempting them from U.S. taxation. The revenue loss from this change would grow over time because a territorial system would encourage multinationals to shift more profits and operations offshore.[15]

However, policymakers could temporarily mask this revenue loss: proposals to move to a territorial system often include a one-time tax on the $2 trillion of foreign profits that companies are now holding offshore (though companies may be allowed to pay that tax over a number of years).[16] This temporary revenue bump means that a territorial tax system might cost much less over the first ten years than over a longer period and might even raise revenue over the initial decade, despite losing significant revenues over the long term.

Even if policymakers were to enact an economically sound international tax reform that saved revenues over the long run — such as by adopting a minimum tax on foreign profits at an adequate tax rate, or ending or limiting deferral[17] — the transition to such a system could include a one-time tax on profits currently held offshore that could make tax reform look more fiscally sound than it actually is in the long run.

Conclusion

By using timing shifts or one-time tax savings, policymakers could assemble a tax reform package that meets the revenue targets for reform over the ten-year budget window but falls well short of those targets in subsequent decades. That would put greater pressure on future deficits. (It also would cause any revenue contribution to deficit reduction to dissipate in the long run, even as the contribution from entitlement cuts likely continued to grow.)

It is critical that policymakers hold tax reform to the same standard as major health and immigration reform proposals, so that the fiscal target that the proposal must achieve over the first ten years is also achieved during the subsequent decade.

End Notes

[1] Brandon Debot provided valuable research assistance.

[2] Chuck Marr and Brian Highsmith, “Six Tests for Corporate Tax Reform,” Center on Budget and Policy Priorities, Updated February 24, 2012, https://www.cbpp.org/sites/default/files/atoms/files/2-28-11tax.pdf.

[3] For a discussion of timing gimmicks in individual tax reform, see: Chye-Ching Huang and Nathaniel Frentz, “Four Timing Gimmicks That Could Disguise Fiscally Irresponsible Individual Tax Reform,” Center on Budget and Policy Priorities, October 30, 2013, https://www.cbpp.org/cms/index.cfm?fa=view&id=4041.

[4] Joint Committee on Taxation, Revenue Estimates Memorandum, October 27, 2011, http://democrats.waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/media/pdf/112/JCTRevenueestimatesFinal.pdf. The JCT analysis retained one major tax break on foreign profits along with some other smaller corporate tax expenditures for which cost estimates were not available.

[5] Tax Analysts Roundtable Discussion on Taxes and Small Business, Washington, D.C. Friday, January 20, 2012

[6] JCT estimated that revenue would decline in the first year, likely because of corporations’ initial response to tax-reform changes. For instance, companies losing tax breaks in tax reform would likely claim as many of those tax breaks as possible before the reforms took effect, which would diminish the revenue gained from base broadening in the first year.

[7] See: Bowles-Simpson illustrative plan: http://www.fiscalcommission.gov/sites/fiscalcommission.gov/files/documents/TheMomentofTruth12_1_2010.pdf; Rivlin-Domenici proposal: http://bipartisanpolicy.org/sites/default/files/files/BPC%20FINAL%20REPORT%20FOR%20PRINTER%2002%2028%2011.pdf; Wyden-Coats proposal: http://www.wyden.senate.gov/download/joint-committee-on-taxation-estimated-score-of-the-bipartisan-tax-fairness-and-simplification-act-of-2010

[8] James B. Mackie III and John Kitchen, “Slowing Depreciation in Corporate Tax Reform,” Tax Notes Special Report, April 29, 2013.

[9] This rough estimate, which combines estimates from Mackie and Kitchen, the Joint Committee on Taxation, and the Tax Policy Center, is intended to be illustrative rather than precise.

[10] Businesses can deduct from their income what it costs them to produce or purchase the goods that they sell. When businesses sell goods from their inventories, LIFO allows them to deduct an amount that is equal to the cost of the items that they added to their inventories most recently — those that are “last in.” When prices are rising, these “last-in” goods are typically more costly than those added to the inventory earlier, allowing for a larger deduction. Under “first-in, first-out” accounting, in contrast, businesses value items in their inventory based on the cost of the oldest items in their inventory, which were typically less costly. For a detailed analysis of why LIFO is dubious policy, see Edward D. Kleinbard, George A. Plesko, and Corey M. Goodman, “Is It Time to Liquidate LIFO?” Tax Analysts,October 16, 2006.

[11] The estimated savings from repealing LIFO for C and S corporations that are shown in JCT’s analysis of a potential corporate tax reform package are identical to the estimated savings shown in President Obama’s fiscal year 2012 budget for his proposal to repeal LIFO, which allowed the tax increase to be spread over ten years (see http://www.gpo.gov/fdsys/pkg/BUDGET-2012-BUD/pdf/BUDGET-2012-BUD.pdf, and the Department of the Treasury’s “General Explanations of the Administration’s Fiscal Year 2012 Revenue Proposals” http://www.treasury.gov/resource-center/tax-policy/Documents/General-Explanations-FY2012.pdf). The President’s fiscal year 2013 and fiscal year 2014 budgets include the same proposal.

[12] Congressional Budget Office, “Options for Reducing the Deficit: 2014 to 2023,” November 2013, p. 154, http://www.cbo.gov/sites/default/files/cbofiles/attachments/44715-OptionsForReducingDeficit-2_1.pdf.

[13] Joint Committee on Taxation, “Estimates of Federal Tax Expenditures for Fiscal Years 2012-2017,” February 1, 2013, https://www.jct.gov/publications.html?func=startdown&id=4503.

[14] Richard Rubin, “Offshore Cash Hoard Expands by $183 Billion at Companies,” Bloomberg, March 8, 2013,

http://www.bloomberg.com/news/2013-03-08/offshore-cash-hoard-expands-by-183-billion-at-companies.html.

[15] For a discussion of the risks of switching to a territorial system of taxation, see: Chye-Ching Huang, Chuck Marr, and Joel Friedman, “The Fiscal and Economic Risks of Territorial Taxation,” Center on Budget and Policy Priorities, January 31, 2013, https://www.cbpp.org/cms/?fa=view&id=3895.

[16] See proposal by House Ways and Means Chairman Dave Camp, http://waysandmeans.house.gov/taxreform/.

[17] See: Chye-Ching Huang, Chuck Marr, and Joel Friedman, “The Fiscal and Economic Risks of Territorial Taxation,” Center on Budget and Policy Priorities, January 31, 2013, https://www.cbpp.org/cms/?fa=view&id=3895.

More from the Authors

Areas of Expertise