2013 Is a Good Year to Repair (if Not Replenish) State Rainy Day Funds

The last decade’s roller-coaster economy has highlighted the importance of state “rainy day funds” — budget reserves for when recessions or other unexpected events cause revenue declines or spending increases. States with rainy day funds were able to avert over $20 billion in cuts to services and/or tax increases in the recession of the early 2000s. Rainy day funds also helped states avoid service cuts and tax increases in the most recent recession.

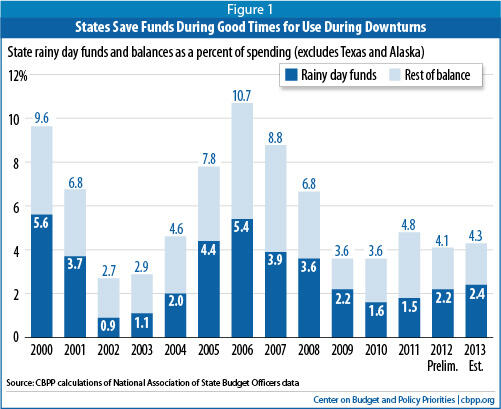

States would have weathered the storms better if those funds had been bigger. States entered the most recent recession with reserves that equaled close to 11 percent of state spending on average.[1] Those were the biggest reserves ever amassed by states, and yet they were only sufficient to fill a modest share of states’ record-setting budget gaps. In many states, it was not just a lack of foresight but poor rainy-day fund design that led to this inadequate funding.

Today, rainy day funds are much smaller. From 2008 to 2010 reserves declined to 3.6 percent of spending, and remain at roughly that level. (See Figure 1.) But right now is probably not the right time for states to focus on rebuilding those funds. Until revenues rise well above pre-recession levels and states have restored programs cut during the recession, replenishment of rainy day funds cannot be a priority.

But now is a reasonable time for states to improve the design of their rainy day funds. Fixing the design of a state rainy day fund (as opposed to actually replenishing it) costs nothing, so there is no reason to wait to address those flaws. Some states have already acted since 2009.

- Many states limit the amount that may be held in a rainy day fund, often at too low a level. Four states raised the cap on the amount of funds to be held in the rainy day fund. Georgia, Oklahoma, and Virginia all raised their caps from 10 percent to 15 percent. South Carolina acted to increase its very low cap of 3 percent to 5 percent — still far too low but a step in the right direction.

Three states — Hawaii, Massachusetts, and Washington — put new provisions in place that will improve prospects for replenishing the funds in the future. Hawaii changed a rule that previously required that any general fund ending balance that exceeded five percent of the budget be used to provide a tax refund; under the new rule, legislators can choose between providing a tax refund and depositing the funds in the state’s rainy day fund. Massachusetts now requires that any capital gains tax revenue collections that exceed $1 billion annually be deposited in the state’s reserves. Washington state voters approved a measure that requires that any “extraordinary” revenue growth — that is, growth that exceeds the 5-year average by more than one-third — be deposited in the state’s rainy day fund. - One problem with some rainy day funds is that there are barriers to their use when needed. For example, Vermont — a state with a number of different rainy day funds — did not tap these funds during the last recession thus increasing pressure for deeper cuts. Last year, the state enacted a package of reforms that should make it easier for the state to use its reserves when needed by adding a new fund — the rainy day reserve — that may be used to address budget shortfalls whatever their cause.

One of the lessons learned in recent years is that rainy day fund improvements are popular with voters. Five of the changes described above were put before voters on the November 2010 ballot. These initiatives in Hawaii, Oklahoma, South Carolina, Virginia, and Washington (which raised caps on deposits or changed deposit rules) all passed.

Before the memory of the recession fades, additional states could improve the design of their rainy day funds. In a report released in February of 2011, the Center outlined the basic provisions of state rainy day funds and identified areas for improvement.[2] The lessons of the downturn for state policymakers include the following:

- Having a rainy day fund is critical. States with rainy day funds were able to avert over $20 billion in cuts to services and/or tax increases in the recession of the early 2000s and again in this most recent recession. By contrast, five states — Arkansas, Colorado, Illinois, Kansas, and Montana — do not have designated rainy day funds. The budgets of all of these states except Montana were hit hard by the recent economic downturn, and the lack of a rainy day fund left them more vulnerable to the recession’s effects. States that do not have a rainy day fund should consider enacting one.

- States should loosen caps on the size of rainy day funds so they can build them up to adequate levels. Rainy day funds would have been even more effective in the most recent downturn if they had been larger; part of the reason they weren’t larger is that thirty-three states and the District of Columbia cap them at inadequate levels[3] . If rainy day funds are capped at an inadequate level, such as 10 percent of the budget or less, states will have difficulty accumulating sufficient reserves. States with overly restrictive caps could either remove the cap or increase it to a more adequate level, such as 15 percent of the budget.

- States should ease rainy day fund rules that make it difficult to make deposits in good times. Most states place a low priority on replenishing their funds, depositing only whatever surpluses are left over at the end of the year. States could develop a process to integrate rainy day fund transfers into the budget as part of an overall reserve policy that places a high priority on saving. For example, Massachusetts dedicates a portion of revenues to the rainy day fund in addition to transferring a share of any surplus funds.

- States also should ease onerous replenishment rules, which are counterproductive because they discourage states from using these reserves as intended. Twelve states[4] and the District of Columbia require rainy day funds to be replenished quickly after they are used, even if economic conditions have not improved. Such rules have proven to create a disincentive to use the fund and place the rainy day fund in competition with other programs for scarce resources during an economic downturn. For example, if the District of Columbia had used half of its available rainy day fund in 2009, it could have covered nearly half of its revenue shortfall for FY2009 and FY2010, rather than rely on service cuts. The rigid replenishment rule deterred lawmakers from accessing the fund. States with these replenishment rules could eliminate them.

- States should scale back limits on funds’ use. Ten states have reduced the effectiveness of rainy day funds in addressing budget deficits by requiring a supermajority of legislators to release the fund or by placing an arbitrary limit on how much of the fund can be released at any one time[5] . In some states, such as Louisiana and Missouri, this has inhibited use of the funds, leading to greater spending cuts and tax increases than otherwise would have been necessary. Limits such as a supermajority requirement have a chilling effect by discouraging legislators from even introducing measures to access these funds because of the difficulty in rounding up the necessary votes.

For more detailed information on the important role that rainy day funds have played in the last two recessions and ways in which states can improve them see the Center’s report released in February 2011.[6]

| TABLE 1 Summary of Rainy Day Fund Features to be Reformed | ||||||||

| State | No RDF | Cap of less than 15% | Cap % | Deposit Rule | Replenishment Rule | Limit on Use | Super-Majority Requirement | Type |

| Alabama* | X | 10.0/20.0 | Required Budget Allocation/Year-End Surplus | X | Both | |||

| Alaska | no cap | See Deposit Rules | X | X | Both | |||

| Arizona | X | 7.0 | Personal Income Growth Formula | X | Statute | |||

| Arkansas | X | |||||||

| California* | X | 5.0 | Required Budget Allocation | Constitutional | ||||

| Colorado | X | |||||||

| Connecticut | X | 10.0 | Year-End Surplus | Statute | ||||

| Delaware | X | 5.0 | Year-End Surplus | X | Constitutional | |||

| District of Columbia* | X | 6.0 | Required Budget Allocation | X | X | Statute | ||

| Florida | X | 10.0 | Required Budget Allocation | X | Constitutional | |||

| Georgia | 15.0 | Year-End Surplus | Statute | |||||

| Hawaii | X | 10.0 | Appropriation/Tobacco funds | X | Statute | |||

| Idaho | X | 5.0 | See Deposit Rules | X | Statute | |||

| Illinois | X | |||||||

| Indiana | X | 7.0 | Personal Income Growth Formula | X | Statute | |||

| Iowa* | X | 10.0 | Year-End Surplus/Appropriation | X | Statute | |||

| Kansas | X | |||||||

| Kentucky | X | 5.0 | Year-End Surplus | Statute | ||||

| Louisiana | X | 4.0 | Oil & Gas Revenue | X | X | X | Constitutional | |

| Maine | X | 12.0 | Year-End Surplus | Statute | ||||

| Maryland | X | 7.5 | Required Budget Allocation | X | Statute | |||

| Massachusetts | 15.0 | Year-End Surplus/Required Budget Allocation/Capital Gains Taxes | Statute | |||||

| Michigan | X | 10.0 | Personal Income Growth Formula | X | Statute | |||

| Minnesota | goal (4.0) | Allocation of Projected Surplus | Statute | |||||

| Mississippi | X | 7.5 | Year-End Surplus | Statute | ||||

| Missouri | X | 7.5 | See Deposit Rules | X | X | X | Constitutional | |

| Montana | X | |||||||

| Nebraska | no cap | Year-end Surplus | Statute | |||||

| Nevada | 20.0 | Year-end Surplus | Statute | |||||

| New Hampshire | X | 10.0 | Year-end Surplus | X | Statute | |||

| New Jersey | X | 5.0 | Year-end Surplus | Statute | ||||

| New Mexico | no cap | Year-end Surplus | Statute | |||||

| New York* | X | 5.0 | See Deposit Rules | X | Statute | |||

| North Carolina | goal (8.0) | Year-end Surplus | Statute | |||||

| North Dakota | X | 9.5 | Year-end Surplus | Statute | ||||

| Ohio | X | 5.0 | Year-end Surplus | Statute | ||||

| Oklahoma | 15.0 | Year-end Surplus | X | X | Statute | |||

| Oregon* | X | 12.5 | Required Budget Allocation/Year-end Surplus/Lottery Revenue | X | X | Both | ||

| Pennsylvania | no cap | Year-end Surplus | X | Statute | ||||

| Rhode Island | X | 5.0 | Required Budget Allocation | X | Statute | |||

| South Carolina* | X | 5.0 | Year-end Surplus/Required Budget Allocation | X | Statute | |||

| South Dakota | X | 10.0 | Year-end Surplus | X | Statute | |||

| Tennessee | X | 5.0 | Required Budget Allocation | X | Statute | |||

| Texas | X | 10.0 | Year-end Surplus/Appropriation/Oil & Gas Revenue | X | Constitutional | |||

| Utah* | X | 6.0 | Year-end Surplus | X | Statute | |||

| Vermont | X | 5.0 | Year-end Surplus/Appropriation | Statute | ||||

| Virginia | 15.0 | See Deposit Rules | X | Constitutional | ||||

| Washington | X | 10.0 | Required Budget Allocation/Appropriation | Constitutional | ||||

| West Virginia | X | 10.0 | Year-end Surplus | X | Statute | |||

| Wisconsin | X | 5.0 | Year-end Surplus | Statute | ||||

| Wyoming | no cap | Year-end Surplus | Statute | |||||

| ***Source: NASBO and NGA Fiscal Survey of States (FY 2010) *States with multiple RDFs AK: Alaska has 2 rainy day funds. Neither the constitutional Budget Reserve Fund nor the statutory Budget Reserve Fund are capped. AL: Alabama has 2 rainy day funds. The Education Trust Fund is capped at 20% of education expenditures and the General Fund Trust Fund is capped at 10% of general fund expenditures. The ETF account must be repaid within 6 years, and the General Fund account must be repaid within 10 years. CA: California has 2 rainy day funds. The Budget Stabilization Account is capped at 5% and there is no statutory cap for the Special Fund for Economic Uncertainties. There will be a measure on the ballot in 2014 that would make significant RDF changes if passed. The RDF has a "soft" cap. Prop 58 required a certain level of GF revenues to be transferred each year to the reserve — unless the transfer is suspended by the governor — until the balance of the reserve reaches the greater of $8 billion or 5% of GF revenues. At that point the transfers would not be required, although the Legislature could deposit additional GF revenues exceeding those levels if it wished to do so. CT: any surplus funds must now be used to pay down Connecticut's 2009 Economic Recovery Notes through FY2017. DC: DC has 2 rainy day funds. The Emergency Cash Reserve Fund is capped at 2% and the Contingency Cash Reserve Fund is capped at 4%. IA: Iowa has 2 rainy day funds. The Cash Reserve Fund is capped at 7.5% and the Economic Emergency Fund is capped at 2.5%. 60% approval is needed if an appropriation will reduce the Cash Reserve Fund below 3.75% of adjusted revenue estimate. If at close of previous fiscal year, it is determined that general fund is at deficit, up to $50 million from EEF can be used to fill previous year’s deficit, but must be replenished from current fiscal year. HI: transfer of Tobacco Settlement funds to rainy day fund suspended for FY12 and FY13. LA: federal money (largely from Hurricane Katrina relief) is pulled out before calculating the cap. Year-end surpluses and oil and gas revenue above a certain amount constitute rainy day fund deposits. The constitution requires replenishment, but the statute does not require replenishment. There is currently a lawsuit going on about the way lawmakers balanced last year’s budget with almost $200 million from the rainy day fund. The lawsuit claims lawmakers violated the constitution by not repaying the money back, but lawmakers are claiming the recent 2009 statutory rule does not require the money to be paid back for years. The ruling still stands with no replenishment for years. MD: transfers that would reduce the balance below 5.0% must be approved in legislation separate from the budget bill. MI: personal income growth formula determines amount to be transferred to the rainy day fund, legislature has discretion in determining actual transfer amount. MN: the goal for the budget reserve is $653 million. That works out to be about 4% of the FY 2011 annual budget. It is set in law as a dollar figure rather than a percentage of the budget. ND: has the only state-owned bank in the nation and uses its profits, along with the Rainy Day fund. NH: if the general fund operating budget deficit occurred in the most recently completed fiscal biennium and unrestricted general fund revenues for the most recently completed biennium were less than budget forecast, then a only a simple majority is required to access the RDF. If those two conditions are not met, a supermajority vote is required to stabilize the budget. NY: New York has 2 rainy day funds. The Tax Stabilization Reserve Fund is capped at 5% and the Rainy Day Reserve Fund is capped at 3%. OR: Oregon has 2 rainy day funds. The Rainy Day Fund created is capped at 5% and the Education Stability Fund is capped at 7.5%. SC: South Carolina has 2 rainy day funds. The General Reserve Fund has a floor of 3% and the Capital Reserve Fund has a floor of 2%. (Cap is currently phasing up to 5 percent.) UT: Utah has 2 rainy day funds. The General Fund Budget Reserve Account is capped at 6% of general fund expenditures and the Education Budget Reserve Account is capped at 7% of education fund expenditures. Even though the cap is 6%, that 6% limits any year-end transfers done by Finance. There is nothing in the law that would prevent the Legislature to appropriate money to the fund. The 6% does not cap the fund but only the year-end transfer. VA: Virginia's cap is applied to the average of sales and income tax revenues over the previous three fiscal years rather than spending. VT: Vermont has 3 fund known as stabilization funds (general, transportation, and education), and a “rainy day reserve” all capped at 5% of their respective appropriations. WA: funds can be withdrawn via a simple majority when the governor declares an emergency or during recessions. Otherwise, withdrawal requires a three-fifths vote. Any “extraordinary” revenue growth will be transferred to the rainy day fund. WI: in each fiscal year, if actual general fund tax revenues exceed those projected revenues, 50% of the additional tax revenues are required to be transferred to the budget stabilization fund. Also, net proceeds from the sale of any surplus property are deposited in the budget stabilization fund. WY: Wyoming recently created an extra legislative stabilization account to offset volatile mineral reserve funds. This fund has no statutory role. | ||||||||

End Notes

[1] In this paper, average figures and the graph exclude Alaska and Texas because these two states’ reserves are so much larger than those of other states — for fiscal year 2010, they made up close to half of total balances nationally — that including them would obscure the trends in typical states. The purpose of Alaska’s rainy day fund — called the Permanent Fund — is not typical of other states. A portion of oil company proceeds are deposited in the fund and paid out to residents to compensate for the use of the state’s oil reserves. The Texas fund is also a repository for oil- and gas-related revenues. High oil prices and expanded gas production resulted in large increases in the Texas fund at a time when balances in most state reserves were going down.

[2] Elizabeth McNichol and Kwame Boadi, “How and Why States Should Strengthen Their Rainy Day Funds”, Center on Budget and Policy Priorities, February 3, 2011.

[3] Alabama, Arizona, California, Connecticut, Delaware, Florida, Hawaii, Idaho, Indiana, Iowa, Kentucky, Louisiana, Maine, Maryland, Michigan, Mississippi, Missouri, New Hampshire, New Jersey, New York, North Dakota, Ohio, Oregon, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Vermont, Washington, West Virginia, and Wisconsin.

[4] Alabama, Alaska, Florida, Iowa, Louisiana, Maryland, Missouri, Nebraska, New York, Rhode Island, South Carolina, and Utah.

[5] Alaska, Delaware, Hawaii, Louisiana, Missouri, Oklahoma, Oregon, Pennsylvania, South Dakota, and Texas.

[6] Elizabeth McNichol and Kwame Boadi, “How and Why States Should Strengthen Their Rainy Day Funds”, Center on Budget and Policy Priorities, February 3, 2011. https://www.cbpp.org/cms/index.cfm?fa=view&id=3387

More from the Authors