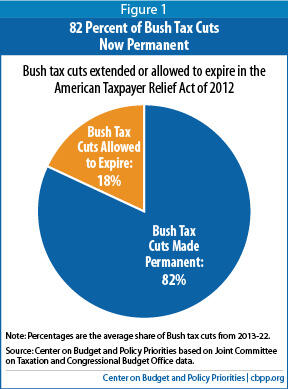

Budget Deal Makes Permanent 82 Percent of President Bush’s Tax Cuts

The American Taxpayer Relief Act of 2012 (ATRA)[1] , which President Obama signed into law last night, makes permanent 82 percent of President Bush’s tax cuts.

The Joint Committee on Taxation (JCT) and Congressional Budget Office estimate that making permanent all of the Bush tax cuts would have cost $3.4 trillion over 2013-2022.[2]

That’s the price tag for making permanent:

- all of the income, capital gains, and dividends tax cuts first enacted under President Bush;

- the estate tax at the levels that it was at in 2012; and

- the increase in the cost of “patching” the Alternative Minimum Tax (AMT), caused by the other Bush tax cuts, to ensure that more middle-income taxpayers are not subject to the AMT. The other Bush tax cuts threw more taxpayers onto the AMT. That increased the cost of indexing the AMT parameters for inflation. (Otherwise, the AMT would have cancelled out much of the value of the other Bush tax cuts.[3] The $3.4 trillion does not include the cost of indexing the AMT for inflation that would have existed even without the Bush tax cuts.)

Here’s the 18 percent of the Bush tax cuts allowed to expire:

- $453 billion over ten years comes from the expiration of cuts to the income, capital gains, and dividend tax rates for filers with taxable income above $450,000 for married couples and $400,000 for singles. These filers retain the full Bush tax-rate cuts on their first $450,000 (or $400,000) of taxable income. (Note: the taxable income thresholds of $400,000 and $450,000 translate into significantly higher threshold amounts for adjusted gross income — that is, the income before taxpayers take advantage of the credits, deductions, and other tax preferences to which they’re entitled.)

- $152 billion comes from allowing limits on personal exemptions and itemized deductions (the so-called Pease and PEP provisions) to return for filers with adjusted gross income above $300,000 for married couples and $250,000 for singles.

- $19 billion comes from raising the estate tax rate to 40 percent, from the 35 percent rate in place in 2012. The exemption amount — the value of an estate that is not subject to the estate tax — will be $5.2 million for individuals and $10.4 million for couples in 2013, with the exemption amounts rising with inflation in future years. (By comparison, returning the estate tax to its 2009 parameters of 45 percent, with a $7 million per couple exemption, would have saved $137 billion; thus, relative to the 2009 parameters, $118 billion in revenue was lost.)

End Notes

[1] The final text of ATRA is available at http://www.gpo.gov/fdsys/pkg/BILLS-112hr8enr/pdf/BILLS-112hr8enr.pdf.

[2] Congressional Budget Office, “An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022,” August 22, 2012, Expiring Tax Provisions, http://www.cbo.gov/publication/43547.

[3] Aviva Aron-Dine and Robert Greenstein, “The AMT’s Growth Was Not ‘Unintended’,” Center on Budget and Policy Priorities, November 30, 2007, https://www.cbpp.org/cms/index.cfm?fa=view&id=857.

[4] Joint Committee on Taxation, “Estimated Revenue Effects Of The Revenue Provisions Contained In An Amendment In The Nature Of A Substitute To H.R. 8, The ‘American Taxpayer Relief Act Of 2012,’ As Passed By The Senate On January 1, 2013,” JCX-1-13, January 1, 2013, https://www.jct.gov/publications.html?func=startdown&id=4497.

More from the Authors