Raising Today’s Low Capital Gains Tax Rates Could Promote Economic Efficiency and Fairness, While Helping Reduce Deficits

The large tax preferences that capital gains enjoy over “ordinary” income, such as salary and wages, add to budget deficits, widen income inequality, and do little if anything to promote economic growth. Recent bipartisan deficit commissions have called for eliminating or sharply reducing these tax preferences, as the landmark 1986 Tax Reform Act did. By doing so as part of a package that reduces deficits and reforms the tax code, policymakers could help put the nation’s fiscal house in order and make the tax code fairer and more efficient.

The tax code now strongly favors capital gains — increases in the value of assets, such as stocks and real estate — over ordinary income. Not only is the capital gains tax rate far below the top tax rate on ordinary income, but taxpayers can delay paying taxes until they realize their capital gains (usually when they sell assets). In many cases, taxpayers can avoid paying capital gains tax altogether; about half of all capital gains are neversubject to capital gains tax, according to the Congressional Research Service (CRS).[1]

The large preference for capital gains is economically inefficient, regressive and costly:

- Economically inefficient. As Leonard Burman, the former director of the Urban-Brookings Tax Policy Center (TPC) and one of the nation’s foremost tax policy experts, has written:

Virtually every individual income tax shelter is devoted to converting fully taxed income into capital gains. If you can transform $10 million of wages into gains, you can save over $2 million. With that kind of payoff, there is a whole industry devoted to inventing schemes [to take advantage of this tax shelter].[2]

Taking advantage of these schemes involves spending resources (on, for instance, lawyer and accountant fees) that people might put to more productive use. Burman has also commented:[Tax s]helter investments are invariably lousy, unproductive ventures that would never exist but for tax benefits. And money poured down these sinkholes isn’t available for more productive activities. What’s more, the creative energy devoted to cooking up tax shelters could otherwise be channeled into something productive. . . . Bottom line: low rates for capital gains are as likely to depress the economy as to stimulate it. [3]

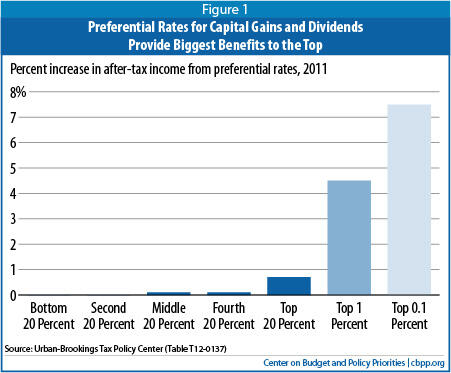

- Regressive. Capital gains are heavily concentrated at the top; the top 1 percent of taxpayers will receive 71 percent of all capital gains in 2012, according to TPC.[4] This means that the benefits of the tax breaks for capital gains flow overwhelmingly to the highest-income taxpayers, while delivering negligible benefits to the large majority of taxpayers. TPC estimates, for example, that the benefits of the preferential rates on capital gains and dividends raised the after-tax incomes of the top 0.1 percent of taxpayers by 7.5 percent — an average of $356,750 for each such taxpayer in 2011, while raising after-tax incomes among the middle fifth of households by just 0.1 percent, or an average of $23. (See Figure 1.) The tax preferences for capital gains are a key reason why the tax code violates the “Buffett rule,” which essentially says that people at the top shouldn’t face lower tax rates than middle-income households. By making the tax code less progressive, these tax preferences also worsen after-tax income inequality, which has risen to historic levels in recent decades. Between 1996 and 2006, “changes in capital gains and dividends were the largest contributor to the increase in the overall income inequality,” [5] according to CRS.Image

- Inequitable. The tax breaks for capital gains also are inequitable in another way. A taxpayer who earns most or all of his income from a salary will pay much more of it in taxes than a taxpayer who makes the same amount of income primarily in the form of capital gains. In 2011, households with incomes between $100,000 and $200,000 who got more than two-thirds of their income from investments taxed at the preferential capital gains and dividend rates owed only 5 percent of their incomes in federal income and payroll taxes, on average, TPC data show. That’s about a quarter ofthe 19.2 percent rate faced by households who earned the same total income but received less than one-tenth of it from capital gains and dividends.

- Costly. In light of the sacrifices that Americans will almost certainly have to make to reduce deficits, retaining a tax preference for high-income Americans that costs tens of billions of dollars each year should not be a priority.

The arguments that proponents make to defend tax breaks for capital gains do not withstand scrutiny.

- There is no evidence that tax breaks for capital gains contribute to economic growth at all, let alone by enough to outweigh the costs of these tax breaks. University of Michigan tax economist Joel Slemrod, another of the nation’s leading tax policy experts, has found that “there is no evidence that links aggregate economic performance to capital gains tax rates.”[6] Similarly, TPC has found no statistically significant correlation between capital gains rates and real GDP growth during the last 50 years.[7] In addition, a new CRS report analyzing capital gains tax rates and economic growth finds that “analysis of such data suggests the reduction in the top [capital gains] tax rates have had little association with saving, investment, or productivity growth”.[8]

- Capital gains tax breaks have little effect on most seniors. Despite claims that reducing the tax preferences for capital gains would hurt the elderly, most elderly households have low or moderate incomes and thus do not face the top income tax rates, so they cannot benefit from having capital gains taxed at a much lower rate than those top rates. TPC estimates that in 2011, nearly 60 percent of elderly households had cash incomes below $40,000 and, for those filers, investment income made up only 6.1 percent of their overall incomes, on average. The preferential rates on capital gains and dividends are worth less than $6 a year to these elderly households, on average (less than 0.1 percent of their after-tax incomes). [9]

For the 21 percent of elderly households with incomes between $50,000 and $100,000, average after-tax income would have been less than one-third of one percent lower in 2011, if there were no difference between the tax rate on capital gains and dividends and the tax rate on ordinary income. The average increase in taxes for those filers would have been $195. - Charges that the capital gains tax leads to double taxation of corporate profits are overblown and do not justify a blanket tax preference for all capital gains. Effective corporate tax rates are often very low, and many capital gains are never subject to capital gains tax.

- Inflation is not a sound reason for the current preferential treatment of capital gains. Some capital gains reflect inflation instead of real increases in purchasing power. But the fact that capital gains are taxed when they are realized rather than when they accrue allows taxpayers to defer payment of taxes, which helps offset the taxation of gains that merely reflect inflation. Moreover, inflation does not justify the complete exemption of many real capital gains from taxation, and the inflation component of other types of investment income, such as interest, is subject to taxation as well.

Major tax reform and deficit reduction efforts have recognized the need to reduce the tax preferences for capital gains. A key element of the landmark 1986 tax reform legislation, for example, was elimination of the differential between the capital gains tax rate and the top income tax rate. As a 1984 Treasury Department report explained about the need to reform the taxation of income from investments, including capital gains:[10]

The taxation of capital and business income in the United States is deeply flawed. . . . It contains subsidies to particular forms of investment that distort choices in the use of the nation’s scarce capital resources. It provides opportunities for tax shelters that allow wealthy individuals to pay little tax, undermine confidence in the tax system, and further distort economic choices.

More recently, the Bipartisan Policy Center’s Debt Reduction Task Force — chaired by Pete Domenici, the former Senate Budget Committee chairman, and Alice Rivlin, former director of the Office of Management and Budget and the Congressional Budget Office —stated that eliminating the preferential rates for capital gains and dividends “will establish equal treatment among taxpayers with different sources of income and eliminate the incentive to use tax shelters to convert ordinary income into capital gains.”[11] It added, “Eliminating the capital gains differential will also reduce the compliance and administrative costs associated with sophisticated tax-planning strategies.”

Similarly, the illustrative tax reform proposal in the Bowles-Simpson debt reduction plan would eliminate the differential between capital gains and ordinary income rates. (The Bowles-Simpson plan states that if policymakers choose instead to retain a lower capital gains tax rate, they should offset the cost by setting tax rates on ordinary income higher than in the illustrative plan.)

![]()

End Notes

[1] Jane Gravelle, “Limits to Capital Gains Feedback Effects,” Tax Notes 51, April 22, 1991, pp. 363-371

[2] Leonard E. Burman, “Mitt Romney’s Teachable Moment on Capital Gains”, Forbes.com, January 18, 2012, http://www.forbes.com/sites/leonardburman/2012/01/18/mitt-romneys-teachable-moment-on-capital-gains/.

[3] Leonard E. Burman, “Under the Sheltering Lie,” Marketplace Commentary, December 20, 2005, http://www.taxpolicycenter.org/publications/template.cfm?PubID=900918.

[4] Tax Policy Center Table T09-0942.

[5] http://taxprof.typepad.com/files/crs-1.pdf at page 1.

[6] Joel Slemrod, “The Truth About Taxes and Economic Growth” Interview in Challenge, vol. 46, no. 1, January/February 2003, pp. 5–14. http://www.challengemagazine.com/Challenge%20interview%20pdfs/Slemrod.pdf.

[7] Troy Kravitz and Leonard Burman, “Capital Gains Tax Rates, Stock Markets, and Growth,” Tax Policy Center, November 7, 2005. See also Leonard Burman, “Capital Gains Tax Rates and Economic Growth (or not),” Forbes blog, March 15, 2012, http://www.forbes.com/sites/leonardburman/2012/03/15/capital-gains-tax-rates-and-economic-growth-or-not/. Burman also found no statistically significant effect lagged up to five years: Leonard Burman, The Labyrinth of Capital Gains Tax Policy, Washington, D.C., Brookings Institution, 1999, pp. 81.

[8] Thomas L. Hungerford, “Taxes and the Economy: Analysis of the Top Tax Rates Since 1945,” Congressional Research Service, September 14, 2012.

[9] Tax Policy Center Tables T12-0009 and T12-0136.

[10] Treasury Department, “Tax Reform for Fairness, Simplicity, and Economic Growth,” The Treasury Department Report to the President, November 1984.

[11] Debt Reduction Task Force, “Restoring America’s Future,” Bipartisan Policy Center, November 2010, http://bipartisanpolicy.org/library/report/restoring-americas-future.

More from the Authors

Areas of Expertise