Testimony of Robert Greenstein, President, Center on Budget and Policy Priorities, Before the Senate Committee on Budget

Chairman Conrad, Ranking Member Sessions and members of the Budget Committee, thank you for the opportunity to appear before you today to discuss tax expenditures, tax reform, and what role they might play in deficit reduction. I am Robert Greenstein, president of the Center on Budget and Policy Priorities, a policy institute here in Washington. I also had the privilege of serving as a commissioner on the Bipartisan Commission on Entitlement and Tax Reform chaired by then-Senators Kerrey and Danforth in 1994.

As you all know, the budget is on an unsustainable path. If we continue current policies, the national debt will grow to nearly the size of the economy by the end of the decade and continue to rise after that. The question for policymakers to consider is not whether to address our fiscal problems — we clearly need to do so — but how to do that in a way that is effective, responsible and equitable.

How Did We Get Here?

To understand the difficult choices that will be required to right our fiscal ship, it is useful to recall how we arrived at our current situation. Ten years ago, various policymakers — and even the Federal Reserve chairman — appeared before Congressional committees warning that our projected budget surpluses were too large. They knew of the aging of the population and the rise in health care costs, but even after taking those factors into account, the Congressional Budget Office and the Office of Management and Budget projected large surpluses for decades to come.

Many factors have led to the sharp reversal in our fiscal fortunes. Tax policy was one of them and played a significant role. The tax cuts enacted over the past decade contributed to a marked decline in federal tax revenues, which, even before the recession, had fallen to their lowest level as a share of the economy in a half century. Moreover, the tax cuts — along with increases in expenditures — have led to large increases in the national debt and hence to the rising interest costs that play a major role in putting us on an unsustainable path.

Whatever one’s view on the continuation of the current tax cuts after 2012, there can be little question that they have a large fiscal impact. Alan Greenspan, Martin Feldstein, and Peter Orszag all have recommended that the tax cuts enacted in 2001 and 2003 be allowed to expire on schedule at the end of 2012 — or that policymakers pay for any of these tax cuts which they wish to extend — because of the difficult fiscal situation we face, as well as the large improvement in the fiscal outlook such a step would make. The latest Congressional Budget Office projections show this one step alone would nearly halt the growth in the debt as a share of the economy over the coming decade.

The CBO estimates show if all current policies remain in effect — the tax cuts, AMT relief, SGR relief, etc. — and no deficit reduction measures are taken, the deficit will stand at 6.1% of GDP in 2021. Allowing the tax cuts to expire — or paying for those we wish to extend — would slice the projected deficit nearly in half to 3.6% of GDP in 2021, not a sufficiently low level itself but one that would, in conjunction with other deficit reduction measures, get us to primary budget balance and stabilize the debt. Of course, beyond the coming decade, the relative impact of the tax cuts will be overtaken by rapidly rising health care and debt service costs as the major drivers of federal budget deficits, and substantial additional steps would be needed, especially steps to slow the growth of health care costs throughout the U.S. health care system.

Image

Everything On the Table

Everything On the Table

I raise this simply to note that both taxes and spending are implicated in the fiscal problems we face. Both will need to be part of the solution. Addressing our long-term fiscal imbalances will require difficult changes in federal programs. But our budget math cannot be solved on the spending side alone.

This is a widely shared view. Bipartisan majorities on each of the major recent deficit reduction panels — the Bowles-Simpson commission, the Rivlin-Domenici commission, and a panel convened by the National Academy of Sciences — agreed that a balanced approach consisting of both program and tax reforms, each of which contributes to deficit reduction, will be required. This has been done before; the last big bipartisan deficit-reduction agreement signed into law — the 1990 budget agreement reached by President George H.W. Bush and Congressional leaders of both parties — was a balanced mix of program reductions and new tax revenues.

Tax Expenditures: A Target of Opportunity

As this testimony will discuss, tax expenditures offer a particular target of opportunity. I recall the moment in 1994 when Alan Greenspan testified to the Commission that, in examining entitlements, we needed to look at what he called the “tax entitlements.” Greenspan’s terminology was illuminating; many tax expenditures are, essentially, spending entitlements that are delivered through the tax code.

Take child care as an example. If you are low- or moderate-income, you may get a subsidy to help cover your child care costs, and the subsidy is provided through a spending program. If you are higher on the income scale, you still get a government subsidy that reduces your child care costs, but it is delivered through the tax code via a tax credit. Moreover, if you are a low or modest income parent with child care costs, you may miss out because the spending programs that provide child care subsidies are not open ended and can only serve as many people as their capped funding allows. By contrast, if you are a higher income household (and there is no limit on how high your income can be), your child care subsidy is guaranteed, because the tax subsidy you get operates as an open-ended entitlement. It doesn’t make much sense to make the tax-code subsidy sacrosanct and the program subsidy a deficit reduction target merely because one is delivered through a “spending” program and the other is delivered through the code.

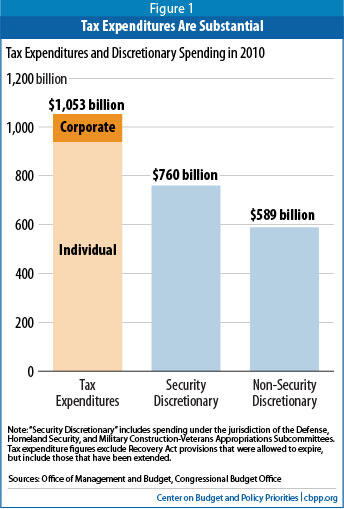

The costs of tax expenditures are large. In 2010, individual tax expenditures totaled nearly $1 trillion, and total tax expenditures — both individual and corporate — amounted to $1.05 trillion. This greatly exceeded the cost of Medicare and Medicaid combined ($719 billion), Social Security ($701 billion), and non-security discretionary programs, which stood at $589 billion, a little over half of the cost of tax expenditures.

Keeping the Goal of Shared Prosperity in Mind

The economist Kenneth Rogoff recently warned of the consequences of widening and historic inequalities of income, wealth, and opportunity. Rogoff cautioned that the ability of countries to create opportunities for their citizens and to address inequality could be the key factor that “could separate the winners and losers in the next round of globalization” and could emerge as the “big wildcard in the next decade of global growth.” [1]

Public policy in general and tax policy in particular have a role in helping to mitigate the human consequences of the global trends that have played a large role in suppressing wage growth among lower- and middle-class Americans. Unfortunately, our country’s recent record on this matter has not been stellar. For example, under the tax cuts enacted in 2001 and 2003, people making over $1 million a year are receiving an average tax cut of more than $125,000 a year, according to the Urban Institute-Brookings Tax Policy Center. This is more than 140 times the average tax cut that households in the middle 20 percent of the income scale are receiving.

The Bowles-Simpson report set forth a basic principle here, stating that “Though reducing the deficit will require shared sacrifice, those of us who are best off will need to contribute the most. Tax reform must continue to protect those who are most vulnerable and eliminate tax loopholes favoring those who need help least.”

A Closer Look at Tax Expenditures

Consistent with the goals of reducing budget deficits, increasing economic efficiency and growth, and protecting our most vulnerable citizens, both the Bowles-Simpson and the Rivlin-Domenici proposals place their focus in the revenue area on reforming and scaling back tax expenditures.

The Budget Act of 1974 defines tax expenditures as revenue losses attributable to any provisions in federal tax law that provide special benefits to particular taxpayers or groups of taxpayers. Although accomplished through the tax code, most experts believe these provisions should actually be viewed as a form of government spending. According to the Joint Committee on Taxation, tax expenditures “may be considered to be analogous to direct outlay programs, and the two can be considered as alternative means of accomplishing similar budget policy objectives.” In addition, as tax expert Leonard Burman and others have pointed out, tax expenditures impose the same “opportunity costs” as federal spending programs in terms of higher tax rates, reduced federal resources for national priorities, and/or higher deficits and national debt.

GAO Recommends Scrutinizing Tax Expenditures

The much-discussed GAO report released last week on overlap and duplication in government programs highlights tax expenditures as an area in which policymakers can find significant savings.a The GAO report states:

“Improving tax expenditure performance or eliminating tax expenditures could reduce revenue losses, potentially by billions of dollars. For example, improved designs may enable individual tax expenditures to achieve better results for the same revenue loss or the same results with less revenue loss. Also, reductions in revenue losses from eliminating ineffective or redundant tax expenditures could be substantial depending on the size of the eliminated provisions.”

The GAO adds that “tax expenditures do not compete overtly with other priorities in the annual budget, and spending embedded in the tax code is effectively funded before discretionary spending is considered. Many tax expenditures are not subject to Congressional reauthorization. Therefore, Congress lacks the opportunity to regularly review their effectiveness.”

a Government Accountability Office, “Opportunities to Reduce Potential Duplication in Government Programs, Save Tax Dollars, and Enhance Revenue,” March 2010

If these provisions were classified as spending rather than as tax benefits, tax expenditures would constitute the single largest category of federal spending. As noted, they consume more resources annually than Social Security, than Medicare and Medicaid combined, and than either security or non-security discretionary spending. Martin Feldstein, a former Chairman of the Council of Economic Advisers under President Reagan, wrote in the Wall Street Journal last summer that “If Congress is serious about cutting government spending, it has to go after many of these [tax expenditures].” Feldstein added “Cutting tax expenditures is really the best way to reduce government spending.”

One reason Feldstein reached this conclusion is that tax expenditures are not only costly, but often also economically inefficient. Although some tax expenditures are intended to adjust the amount of taxable income so as to better measure economic income or to reflect differences in ability to pay taxes, most tax expenditures are designed for another purpose — to subsidize certain desired activities — and often do so in inefficient ways that can detract from economic growth.

In cases where certain economic actions are believed to generate benefits shared by society at large, there may be strong arguments for designing the tax code to actively encourage these activities. But there are numerous ways to incentivize various desired activities, and the efficiency of any given tax incentive is heavily affected by how it is designed. Existing tax expenditures vary greatly in their effects on economic efficiency; some reduce economic efficiency by distorting investment or other economic decisions. Feldstein has observed that curbing various tax expenditures “would also increase overall economic efficiency by removing incentives that distort private spending decisions.”

Adding to their inefficiency, many tax expenditure provisions — principally deductions, exemptions, and exclusions — tie the tax subsidies they provide to the marginal tax rate of the beneficiary. The amount of the tax benefit provided increases with income, with the wealthiest households receiving the largest tax subsidies.

From an economic perspective, such a structure makes sense only if higher-income people need a substantially greater monetary incentive to take the desired action and wouldn’t take it without the tax incentive. Yet, as a number of tax experts and economists from across the political spectrum have explained, the reality is frequently the reverse; high-income families generally would send their children to college, make sure they have assets for retirement, and buy a home with or without the current costly tax incentives. Financially constrained families, by contrast, often would fail to engage in the socially desired activity without significant financial incentives.

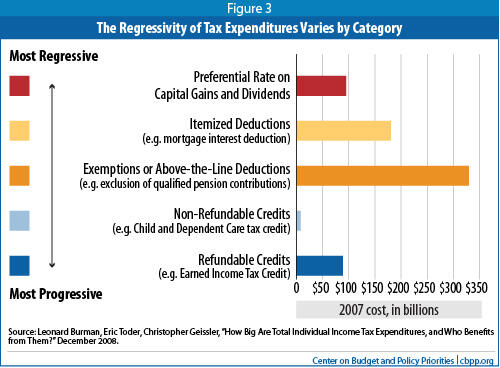

| Table 1: Regressivity of Tax Expenditures Varies by Category (Percent Change in After Tax Income, by Income Quintile) | ||||||||

| Lower rates on capital gains and dividends | Itemized deductions | Tax Exclusions | Above-the-line deductions | Non-refundable credits | Refundable credits | All Provisions | ||

| Bottom 20 percent | 0.00% | 0.02% | 0.54% | 0.01% | 0.05% | 5.49% | 6.52% | |

| Second 20 percent | 0.01% | 0.11% | 2.99% | 0.06% | 0.28% | 5.00% | 8.16% | |

| Middle 20 percent | 0.04% | 0.38% | 3.79% | 0.09% | 0.33% | 2.20% | 6.76% | |

| Fourth 20 percent | 0.12% | 1.09% | 3.68% | 0.11% | 0.23% | 1.99% | 6.79% | |

| Top 20 percent | 2.11% | 2.91% | 4.74% | 0.08% | 0.06% | 0.25% | 11.36% | |

| Top 1 percent | 5.87% | 3.24% | 2.90% | 0.06% | 0.00% | 0.00% | 13.53% | |

| Total Cost | $96 billion | $154 billion | $326 billion | $6 billion | $8 billion | $89 billion | $761 billion* | |

| * Takes into account interaction among individual tax expenditure provisions Source: Leonard Burman, Eric Toder, Christopher Geissler, “How Big Are Total Individual Income Tax Expenditures, and Who Benefits from Them?” December 2008. | ||||||||

That is why a number of liberal, conservative, and centrist experts alike have characterized key parts of our tax incentive structure as being “upside down” — we spend money providing the largest tax incentives to people in the top income tax brackets despite the fact that tax incentives generally have a much smaller effect on whether those individuals will send their children to college, become homebuyers, and put income aside for retirement. As tax experts Lily Batchelder (an NYU tax expert who now serves as chief tax counsel for the Senate Finance Committee), Fred Goldberg (who served as Assistant Secretary of the Treasury for Tax Policy and IRS Commissioner under President George H. W. Bush) and former OMB director Peter Orszag wrote in 2006, “[P]roviding a larger incentive to higher-income households is economically inefficient unless policymakers have specific knowledge that such households are more responsive to the incentive or that their engaging in the behavior generates larger social benefits.” [2]

In this respect, tax credits differ significantly from tax deductions and exclusions. Credits reduce the price of the desired activity by an equal amount for most households, although tax credits that are not refundable aren’t available to the roughly one third of American families who owe no individual income taxes during that year. (These households generally do have positive tax liability when other forms of individual taxation — including payroll taxes, state and local taxes, and excise taxes — are considered, and even more so when tax liabilities are considered over periods longer than a single year.) Tax credits that are refundable provide the same price adjustment to all households that engage in the desired behavior, regardless of their income or tax liability during the year in question.

Because tax credits do not link the tax incentive to households’ marginal tax brackets and generally reduce the costs of the economically desired activity by an equal percentage for all affected households, they are often more economically efficient than deductions. Batchelder, Goldberg, and Orszag concluded that refundable tax credits often would be the most efficient type of tax expenditure: “If policymakers wish to use the tax system to create incentives for certain socially-valued behavior, it makes no sense to exclude more than a third of American individuals and families from their reach … absent evidence that those Americans would be relatively unresponsive [to the tax incentive] or that their behavior generates fewer societal benefits.”

Despite the economic efficiency advantages of flat-percentage tax credits, the large majority of tax expenditures operate today through tax deductions, exemptions, or exclusions and thereby provide tax subsidies that mount sharply as income rises. Approximately 70 percent of the amount we spend every year on individual tax expenditures is provided through deductions, exemptions, or exclusions that link the value of the tax break to an individual’s marginal tax bracket.

Our tax code provides this benefit structure despite that fact that many of the activities that tax expenditures are designed to encourage involve costs that are borne most easily by wealthier families even in the absence of the tax break.

Moreover, it is dubious whether many Americans would think that if the government is to provide a subsidy to individuals and families, it should provide the biggest subsidies to those who need them least. Consider, for example, how the tax code affects two different households with respect to a decision to buy a new home. The government effectively pays 35 percent of the interest costs on the first $1 million of the mortgage on an investment banker’s home. In contrast, a nurse or a welder receives a subsidy that defrays only 15 percent of the mortgage interest he or she pays on the modest home that he or she owns.

Another example involves the tax treatment of retirement saving. Under current law, employer and employee contributions to qualified pension plans are excluded from taxable income until they are paid out in retirement. This tax preference is designed to encourage retirement saving by reducing the marginal cost of contributions to retirement accounts. But as is the case with the mortgage interest deduction, high-income individuals receive the largest immediate benefit of the exclusion even though they are the people most likely to save anyway in the absence of a government tax subsidy.

Economists William Gale, Jonathan Gruber, and Peter Orszag have noted that high-income individuals are often able to respond to current retirement tax incentives “by reshuffling their existing assets … to take advantage of the tax breaks, rather than by increasing their overall level of saving.” [3] In Congressional testimony, Orszag added that our current tax expenditures for retirement saving provide the strongest monetary incentives to higher-income households “who are the most likely to use pensions as a tax shelter rather than a vehicle to raise saving.” Similarly, the Congressional Research Service has reported that “because higher earners would save much of their income even without tax incentives to do so, a substantial share of the revenue lost through the deduction for contributions to retirement plans does not result in a net increase in national saving.”[4]

Middle-income families receive significantly smaller subsidies for retirement saving and families with no federal income tax liability receive no tax incentive to put aside money for retirement. In 2007, just 17 percent of workers in the bottom quartile participated in a defined contribution retirement plan.[5]

If policymakers intend to increase overall national saving rather than simply to provide windfall gains for saving that would have occurred anyway, it would seem that current pension tax preferences are, in fact, upside down.

These weaknesses in the structure of various tax incentives offer policymakers an opportunity. By converting various tax deductions into flat-percentage credits, policymakers can improve economic efficiency by increasing the effectiveness of the tax incentives in boosting national saving, college attendance, and the like, even as they achieve deficit reduction and improve the progressivity of the tax code.

The Earned Income Tax Credit and the Child Tax Credit

Erskine Bowles and Alan Simpson have called for deficit reduction to improve economic efficiency and to protect low-income families and have strongly indicated that tax reform should protect the Earned Income Tax Credit and the refundable portion of the Child Tax Credit. [6] These credits are vital to the standard of living of low-income working families, to “making work pay,” and to promoting work over welfare.

Furthermore, these credits lower marginal tax rates for many low-income workers who otherwise face some of the highest marginal tax rates of any group of Americans (because they receive benefits from means-tested programs that are phased down as income increases). This is why, in calling for various tax expenditures to be curbed, Feldstein wrote that he was not including the EITC, “which,” he explained “acts largely as a tax rate reduction.” Numerous academic studies have shown that the EITC has a powerful effect in increasing work, particularly among single parents with children. [7]

There is a longstanding bipartisan principle in this town that people who work full time should not have to raise their children in poverty. There are two main ways to accomplish this: the minimum wage and the Earned Income Tax Credit (EITC). The best course is to use a balanced combination of the two. Relying too heavily on the minimum wage would be burdensome for employers, particularly small businesses, and likely have negative effects on employment. Relying too heavily on the EITC and other tax credits would be burdensome for the government. By balancing these two approaches, as federal policy now does, policymakers can ensure that people who work full time can be protected from poverty without placing too much pressure on either private employers or taxpayers.

Accordingly, in past deficit reduction negotiations, there has been a commitment to protecting low-income households — and to shielding the EITC. In fact, the EITC was expanded as part of the 1990 bipartisan deficit reduction agreement, and the Child Tax Credit was itself established as part of the bipartisan 1997 agreement. Both the Bowles-Simpson and Rivlin-Domenici commissions, as well, would protect these credits. Congress should maintain this commitment and assure that the benefits that the EITC and refundable Child Tax Credit provide are protected in any agreements on deficit reduction and tax reform.

Thanks to the combined effect of these refundable tax credits and the minimum wage, full-time workers with children are no longer taxed into, or deeper into, poverty. However, low-wage workers who are not raising minor children face a different story. They receive no Child Tax Credit and only a very small EITC at best. The maximum EITC for childless workers is less than one-sixth the maximum credit for workers with a child, and childless workers who work full time at the minimum wage are ineligible for the credit altogether because they earn too much. The result is that childless workers are the one group of American workers below the poverty line who can owe net federal taxes based on employment and who thus can be taxed into, or deeper into, poverty.

Conclusion

Recent policy developments suggest a growing view that tax expenditures should be scrutinized and reformed. Both the Bowles-Simpson and Rivlin-Domenici panels — as well as President Bush’s 2005 tax reform panel — called for bold reforms of itemized deductions and other tax expenditures.

Furthermore, as long as we continue to use the tax code as a vehicle for advancing social policy, we should take steps to ensure that the tax incentives provided through the code are efficient, effective, and fair. And if we are going to step up to the plate and pursue deficit reduction, all parts of the budget — including the tax code — should be on the table and should contribute. As the Bowles-Simpson and Rivlin-Domenici plans indicate, given the gravity of the fiscal challenges we face, tax reform cannot be deficit-neutral today.

Finally, if we seek to reduce less-efficient government spending, tax expenditures are a key place to focus. If done responsibly and well, tax expenditure reform has the potential to reduce budget deficits, promote economic efficiency, and make the tax code more progressive at the same time.

End Notes

[1] Kenneth Rogoff, “The Inequality Wildcard,” Project Syndicate, February 14, 2011

[2] Lily L. Batchelder, Fred T. Goldberg Jr., Peter R. Orszag, “Efficiency and Tax Incentives: The Case for Refundable Tax Credits,” Stanford Law Review, Vol. 59, No. 23, 2006

[3] William Gale, Jonathan Gruber, and Peter R. Orszag, “Improving Opportunities and Incentives for Saving by Middle- and Low-Income Households,” Hamilton Project Discussion Paper, April 2006. Gale, Gruber, and Orszag wrote: “By providing incentives for contributions through tax provisions that are linked to the marginal tax rates that people owe, current incentives deliver their largest immediate benefits to higher-income individuals in the highest tax brackets. These high-income individuals are precisely the ones who can respond to such tax incentives by reshuffling their existing assets into these accounts to take advantage of the tax breaks, rather than by increasing their overall level of saving. As a result, the tens of billions of dollars in tax expenditures associated each year with 401(k) and IRA contributions could be targeted more effectively to increase overall savings.”

[4] Congressional Research Service, “401(k) Plans and Retirement Savings: Issues for Congress,” January 2011

[5] Congressional Research Service, 2011

[6] Chairman’s Mark, p. 5, http://www.fiscalcommission.gov/sites/fiscalcommission.gov/files/documents/CoChair_Draft.pdf .

[7] For a review of this literature, see John Karl Scholz, “The Earned Income Tax Credit and the U.S. Low-Wage Labor Market,” Economic and Social Research Institute, June 2010.