Some Recent Reports Overstate the Effect on State Budgets of the Medicaid Expansions in the Health Reform Law

Under the Affordable Care Act (ACA), states are required to expand their Medicaid programs to cover all non-elderly adults and children with incomes up to 133 percent of the federal poverty line ($29,400 for a family of four) starting on January 1, 2014. According to estimates from the Congressional Budget Office (CBO), the cost to states of this expansion will be very modest. That is because the federal government will pick up 96 percent of the costs of the Medicaid expansion over the next 10 years. As a result, between 2014 and 2019, states would see their Medicaid costs rise by only 1.25 percent compared to what they were projected to spend in the absence of health reform.[1] Estimates from the Urban Institute have produced similar results.[2]

Several states whose officials have been highly critical of health reform, however — like Indiana, Mississippi and Nebraska — have commissioned studies that report significantly greater costs to states.[3] These studies, however, conducted by the consulting firm Milliman, Inc., have serious flaws. They produce overstated estimates of the costs of the Medicaid expansion because they rely on a number of problematic assumptions, including:

- Participation-rate assumptions for eligible individuals that generally are inconsistent with decades of experience in means-tested programs. These assumptions, particularly the “full-participation rate” scenarios, result in overstated estimates of Medicaid enrollment increases.

- Assumptions concerning “crowd out” rates among people who otherwise would have private insurance that are inconsistent with historical experience and the research in the field; and

- Estimates of the costs per newly enrolled Medicaid beneficiary that the data show to be substantially overstated.

In addition, the Milliman estimates do not take into account other elements of the Affordable Care Act that will lower state costs or otherwise benefit states financially.

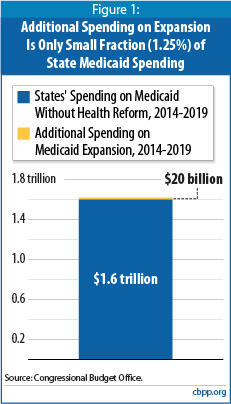

Federal Government Will Pick Up a Vast Majority of the Medicaid Expansion’s Costs

State critics of health reform claim that the Medicaid expansion will impose substantial financial burdens on states. Such claims do not withstand scrutiny. According to estimates from CBO, in its first six years (2014-2019), the Medicaid expansion will increase state costs by $20 billion, increasing states’ overall Medicaid expenditures by just 1.25 percent compared to what those expenditures would be in the absence of health reform. (This includes the costs of enrolling individuals who already are eligible for Medicaid but remain uninsured, as well as the costs of enrolling people becoming newly eligible in 2014.) CBO projects that as a result of the expansion, Medicaid (and the Children’s Health Insurance Program, or CHIP) will cover an estimated 16 million more low-income adults and children, most of whom would otherwise be uninsured. [4]

States are expected to see only a modest increase in costs because, in order to minimize the financial burden on states, the federal government will pay for the overwhelming share of the cost of covering individuals who will become newly eligible to Medicaid as a result of the expansion. The federal government will finance 100 percent of these costs for the first three years, with the federal share phasing down to 90 percent by 2020 and remaining at that level thereafter.[5] CBO estimates that the federal government will pay a total of 96 percent of the cost of expanding Medicaid over the next ten years.[6] This is much higher than the regular federal Medicaid matching rate, which, on average, is 57 percent.

State critics have argued that states will see large cost increases because they have to cover people who currently are eligible for Medicaid but not enrolled, for whom the enhanced federal matching rates would not apply. However, as noted, the CBO estimates include the costs of enrolling both newly eligible and currently eligible individuals. Moreover, while the requirement to purchase insurance, along with new outreach efforts to get people covered, will result in somewhat higher participation among those who already are eligible for Medicaid but are not enrolled, the vast majority of the new enrollees are expected to be individuals who would not have qualified for Medicaid without the enactment of health reform. This is likely to be the case especially in states such as Alabama, Arkansas, Louisiana, Mississippi, and Texas, where current income eligibility limits for parents are very low. For example, in Louisiana, unemployed parents are eligible for Medicaid only if their income is below 11 percent of the poverty line, about $2,400 a year for a family of four. In Mississippi, a working single parent with two children must earn less than about $8,000 a year (44 percent of the poverty line) to qualify for Medicaid. Given the very low income eligibility limits for parents in such states, most new enrollees in 2014 are likely to be adults who would not have been eligible for Medicaid without health reform — people for whom the enhanced federal match will apply.[7]

The Milliman Estimates of Increased State Medicaid Costs

According to Milliman’s estimates, during the 2014 through 2019 state fiscal years, state expenditures for Medicaid will increase by more than 10 percent in Mississippi and Nebraska and by more than 15 percent in Indiana, relative to what these states would have expended in the absence of health reform (see Table 1). These increases are 10 to 12 times higher than the overall increase in state spending that CBO estimates. [8] These estimates are seriously flawed, as explained below.

Estimates Rely on Unrealistically High Participation Rates

In its reports, Milliman produced estimates of the cost to several states of the Medicaid expansion under different scenarios, some of which rest upon inflated estimates of participation rates among eligible individuals. One scenario assumes that all individuals who would be eligible for Medicaid will participate, and from the first day of the Medicaid expansion starting in 2014. Such assumptions are extremely unrealistic. Previous experience shows that no means-tested public program has ever achieved a 100 percent participation rate. A variety of other means-tested programs, such as the Medicare Savings Programs, the Supplemental Nutrition Assistance Program (formerly Food Stamps) and the Earned Income Tax Credit, have participation rates of 43 percent to 86 percent.[9] Even Medicare, which is a highly popular and universal social insurance program, has a participation rate of 96 percent for Part B. And while a mandate to have health insurance or pay a penalty, and the publicity and outreach efforts surrounding the expansion, should produce somewhat higher participation rates than has been typical of means-tested programs, the evidence is overwhelming that the participation rate will simply not be 100 percent. [10] As a result, this first scenario is simply not credible. Although vocal critics of health reform have latched on to the full-participation scenario estimates that Milliman has produced, research and historical experience demonstrate that these estimates should not be taken seriously.[11]

| TABLE 1: MILLIMAN ESTIMATES OF INCREASED STATE MEDICAID COSTS UNDER HEALTH REFORM ARE INFLATED Estimated Increase in State Medicaid and CHIP Spending from State Fiscal Years 2014 through 2019 (in $ millions) | |||||

| State Spending without Reform | Full Participation Scenario | Mid-Range Participation Scenario | |||

| Additional Spending | Increase from Baseline | Additional Spending | Increase from Baseline | ||

| Indiana | 17,581 | 2,715 | 15.4% | Details unavailable | -- |

| Mississippi | 11,581 | 1,208 | 10.4% | 927 | 8.0% |

| Nebraska | 5,336 | 573 | 10.7% | 387 | 7.2% |

| Source: Milliman estimates of the state costs of the Affordable Care Act’s Medicaid provisions. | |||||

Milliman’s “mid-range” scenario assumes that 80 to 85 percent of newly eligible uninsured adults and parents, and 70 to 80 percent of parents and children who are currently eligible but uninsured, will sign up. These relatively high estimates of participation are also unrealistic, particularly for the first years of the Medicaid expansion. Milliman argues that these mid-range participation rate assumptions are consistent with Medicare participation as well as with Medicaid and CHIP participation among children. For a number of reasons, however, they are not appropriate benchmarks.

As noted, unlike Medicaid, Medicare is a universal social insurance program that does not set eligibility based on income like means-tested programs. Moreover, Medicare enrollment does not require extra action on the part of individuals. People who qualify for Medicare are automatically enrolled into the program when they turn 65.[12] Medicaid, on the other hand, requires individuals to submit an application, and applicants must submit additional paperwork, such as pay stubs, to demonstrate that they meet the various Medicaid eligibility criteria. It is therefore not surprising that Medicaid, just like other means-tested programs, has a lower participation rate than Medicare. As noted, 96 percent of eligible beneficiaries participate in Medicare Part B — even though most beneficiaries must pay premiums to do so — whereas 82 percent of children, on average, participate in Medicaid even though it is free (i.e., has no premiums). [13] Medicare’s participation rates thus are irrelevant to the Medicaid context.

It is also inappropriate to assume that adults, particularly those without dependent children, who generally are ineligible for Medicaid today unless they are disabled, will participate in Medicaid at close to the same rate as children participate in Medicaid and CHIP. Children have been covered through Medicaid or CHIP at higher income levels than adults for many years, and the relatively high participation rate among children is the result of an intensive, decade-long campaign to simplify eligibility procedures and perform outreach to families so that more eligible children are enrolled in coverage. Before 1997, when CHIP was enacted, participation among eligible children in Medicaid was only 72 percent, and in the first few years of CHIP implementation, only half of CHIP-eligible children enrolled. Today, an average of 82 percent of eligible children participate in Medicaid and CHIP.[14]

Simply put, it is highly improbable that adult participation rates in Medicaid will be in the 80 to 85 percent range from the first day that the coverage expansion takes effect. Indeed, most credible analyses have assumed lower initial participation and incorporated a ramp-up period. For example, CBO reportedly assumed an initial participation rate of about 50 percent among newly eligible adults. While a higher participation rate is certainly a critical goal for successful implementation and the lessons of children’s coverage indicate that it should eventually be achievable in Medicaid, it will likely take a number of years of intense outreach, education, and simplification of the enrollment process to maximize participation among these individuals. Any reasonable estimate of Medicaid costs would assume relatively modest participation initially, ramping up over time to a higher level, but never to 100 percent.

Estimates Assume Costs that the Health Reform Law Does Not Impose

The health reform law requires that, in 2013 and 2014, state Medicaid programs must raise the fee levels they pay for primary care services to the fee levels that Medicare pays. The federal government will bear 100 percent of this increased cost. Milliman’s projections assume that states will maintain these increased fee levels beyond 2014, with states bearing a substantial share of that cost themselves (i.e., by paying their normal share of Medicaid expenditures for these increased costs). There is no reason to believe, however, that the federal government will mandate that states maintain these increased fee levels. States could elect to do so after 2014, but that would not be consistent with past Medicaid payment practices in most states.

The assumption that states will incur these added costs thus seems dubious. Moreover, at least in its estimates for Nebraska, Milliman went farther and assumed that the state also will raise its Medicaid payment rates for all care provided by all physicians, including specialty services, even though the health reform law does not raise those payment rates even in 2013 and 2014.

In some more recent reports, Milliman has seemed to acknowledge that its full-participation rate scenario is improbable. In a report for the state of Indiana it issued in May, Milliman included only a full participation rate scenario. In the report for Nebraska it issued in August, Milliman added its “moderate participation scenario.” And in October, in a report that Milliman produced for the state of Mississippi, it added a new “low participation” scenario that assumes an average participation rate of 50 percent, which produced an overall cost estimate roughly half that produced under the full participation scenario. Milliman concedes in the Mississippi report that expected enrollment is more likely to approximate the enrollment levels projected under the low and moderate participation scenarios.

Crowd-Out Effect Is Also Overstated

A related problem concerns the assumptions used in the Milliman reports about how many people with private insurance will drop their coverage to enroll in Medicaid, a phenomenon known as “crowd out.” The Milliman analyses adopt an unrealistic assumption that all or a substantial proportion of insured individuals who become eligible for Medicaid will drop their coverage to enroll in the program. Because of this assumption, Milliman estimates that between 35 percent and 45 percent of all new Medicaid enrollees in Mississippi, Nebraska, and Indiana will be people who drop private coverage to enroll in Medicaid. Research indicates, however, that “crowd-out” rates of the magnitude assumed in the Milliman analyses are very unlikely.

If expanding Medicaid really “crowds out” private insurance to such a large degree (that is, if most or all people who would have had private coverage would enroll instead in Medicaid if made eligible), then states that have already expanded their Medicaid programs to cover adults at somewhat higher income levels should have significantly lower rates of private coverage among low-income adults than states that have not instituted such expansions. But the experience of a dozen states that expanded Medicaid coverage to adults with incomes at or above the poverty line does not support this. In these dozen expansion states, an average of 23 percent of adults with incomes that qualify them for Medicaid have private coverage rather than Medicaid; in other states that have not expanded Medicaid, 22 percent of such adults do. Moreover, relative to non-expansion states, the 12 expansion states have a much higher proportion of low-income residents enrolled in Medicaid (53 percent versus 40 percent) and a much lower proportion of low-income residents who are uninsured (21 percent compared to 30 percent). This demonstrates that the expansions are covering the uninsured, rather than merely substituting Medicaid for existing private coverage.

Nor do these results simply reflect underlying insurance coverage conditions that existed in these two groups of states before the Medicaid expansions went into effect. Consider the examples of Arizona and New York, which expanded Medicaid coverage to poor adults in 2000 and 2001, respectively. In these two states, the decline in private coverage over the decade since the expansions were implemented has not been any steeper than the decline in non-expansion states. What has occurred in these two states is that Medicaid coverage growth has been more robust, and the increase in the number of uninsured low-income adults has been smaller, than the increase in non-expansion states. These findings further indicate that expanding Medicaid reduces the rate of uninsurance without significantly undermining private coverage.[15] The assumption in the Milliman studies are at odds with these findings.

In addition, several research studies have looked at whether Medicaid crowds out private health insurance coverage, focusing primarily on state expansions in the 1990s of children’s Medicaid eligibility to income levels similar to those that will apply to adults under health reform. [16] The most common estimates from these studies suggest that if a Medicaid coverage expansion increases enrollment by 100 children, 80 to 90 of them will have been uninsured, while 10 to 20 will have shifted from employer-based insurance. (The estimated size of the crowd-out effect varies from study to study because of methodological differences; some studies find no statistically significant evidence of crowd-out, while others find some crowd-out.)

Based on these studies, the best estimate is that between 10 percent and 20 percent of new Medicaid enrollees previously had private coverage. This is well below the 35 percent to 45 percent rates Milliman assumes in its Indiana, Mississippi, and Nebraska reports under all of its participation-rate scenarios. Indeed, the estimates of the cost of the Medicaid expansion to Indiana would be 28 percent to 38 percent lower if the analysis assumed a crowd-out rate that reflected the research findings. For Nebraska, the cost estimates would be 20 to 35 percent lower due to this one factor alone. For Mississippi, the estimates would be 18 percent to 37 percent lower.[17]

It also may be noted that the number of low-income people substituting public coverage for private coverage tends to be modest in part because relatively few such people have access to affordable private coverage to begin with. In 2005, only 34 percent of non-elderly workers with incomes below the poverty line were offered coverage through their job, and many who were offered coverage do not take it because the premiums were not affordable for them.[18]

Assumed Costs Per Newly Enrolled Medicaid Beneficiary Are Excessive

Milliman’s assumptions concerning the cost of covering new enrollees also are highly problematic. For example, in its Indiana analysis, Milliman based the per-person cost of covering newly eligible adults and parents in Medicaid on the cost of covering uninsured adults through the Healthy Indiana Plan. HIP is the state’s existing Medicaid waiver program that provides coverage to uninsured parents and adults without dependent children who are not eligible for Medicaid and who have incomes below 200 percent of the poverty line.[19] Using the average cost per beneficiary in HIP as the average cost under the forthcoming Medicaid expansion is not valid, as explained below.

Only 35,000 previously uninsured people — only 5 to 10 percent of the eligible uninsured individuals in the state — signed up for HIP. A separate analysis that Milliman conducted found that HIP enrollees were likely to be in poorer health — and thus to use more health care — than typical enrollees in commercial health insurance plans.[20] In short, HIP suffered greatly from the problem of adverse selection: by and large, the only people willing to enroll in it, given the cost of enrolling and the limited coverage that HIP provided, were people with the greatest medical needs.

As noted, the analysis of the costs of expanding Medicaid in Indiana assumes that everyone who qualifies for Medicaid will enroll, including everyone who already has insurance and healthy individuals along with those in less good health. If this occurred, the per person cost would clearly be substantially less than the cost of covering adults in HIP, because those who enrolled in Medicaid would include a mix of healthy and less-healthy individuals. (Moreover, the uninsured tend overall to be in better health than those with coverage.) Even if more realistic participation-rate assumptions are used, the mix of individuals who would enroll in Medicaid would have significantly lower costs on average than the average costs of the HIP enrollees, who, as noted, constitute only 5 to 10 percent of eligible individuals and consist disproportionately of less healthy people who are more costly to insure. Thus, using the per person costs under HIP — which Milliman’s own analyses show covers sicker people — is not appropriate.

The per person estimates of the cost of covering new enrollees in other states appear to be too high as well. For Mississippi, Milliman estimates that if the expansion were in effect in 2009, the cost would be $4,540 per beneficiary for the adult expansion population, and $2,421 for children. But estimates from the Urban Institute for the Kaiser Commission on Medicaid and the Uninsured indicate that per-capita costs for the adult and child populations in Mississippi’s Medicaid program in 2009 were $2,612 and $1,798 respectively.[21] Milliman’s per capita cost estimates should not be 35 to 74 percent higher than the Urban Institute’s estimates, which are based on actual data reported by these states. Similarly, for Nebraska, Milliman’s estimate of the cost per beneficiary of covering newly eligible parents in 2009 is $4,881, 74 percent higher than the Urban Institute estimate of an actual cost of $2,812.

Recent CMS Action on Prescription Drug Rebates Would Further Lower Milliman Estimates

The Milliman estimates also cite increased costs to states resulting from the Affordable Care Act’s changes to the Medicaid prescription drug rebate. Action that the Centers for Medicare and Medicaid Services (CMS) took in September 2010, however, (after some of the Milliman studies were completed) substantially limits any such cost increases.

Under federal law, as a condition for Medicaid coverage of their products, drug manufacturers must pay rebates to the federal government and the states for outpatient prescription drugs that Medicaid dispenses to beneficiaries. These rebates effectively lower the price that state Medicaid programs pay for prescription drugs.

Prior to passage of the ACA, the rebate for brand-name drugs equaled the higher of the minimum rebate of 15.1 percent of the Average Manufacturer Price (AMP) — the price that manufacturers charge to wholesalers — or the difference between the AMP and the lowest price or “best price” offered to any private purchaser. The ACA increases the minimum rebate level from 15.1 percent to 23.1 percent of AMP for most brand-name drugs. For other brand-name drugs and generics, there is a smaller increase in the minimum rebate amount. The ACA provides that the amount of savings resulting from the increase in the minimum rebate percentages will go entirely to the federal government.

Initial guidance released by the federal CMS in April indicated that the federal government would “recapture” any rebates paid between 15.1 percent of AMP and 23.1 percent of AMP. That effectively meant that if state Medicaid programs received rebates based on best price that were higher than the old minimum of 15.1 percent, states would lose part of the share of the rebates that they were already receiving under prior federal law.

New CMS guidance issued in September, however, changes the April guidance and makes clear that the federal government will only recapture rebates above prior-law levels: the old minimum (15.1 percent) or the best price rebate level, whichever was greater. Thus, if a state previously received an 18 percent rebate based on best price for a particular drug, it will keep its full share of the savings up to that level.

This means that when combined with other provisions in the health care law around drug rebates (i.e., the extension of the rebates to drugs dispensed to Medicaid managed care beneficiaries, from which states will get new savings), states could reap some net savings under the drug rebate provisions of the ACA.

Estimates Do Not Incorporate State Savings Included Elsewhere in the Health Reform Law

In addition to the fact that the state analyses include significantly inflated estimates of the cost of health reform’s Medicaid expansion, they do not account for several ways in which the health reform law’s coverage expansions will help to alleviate some state and local budget burdens. Many individuals who will become newly eligible for Medicaid already receive state and local-funded health services, such as mental health treatment or hospital treatment. Because of health reform, Medicaid will now cover many of those services, so the federal government will pick up half or more of the cost of services (depending on a state’s Medicaid matching rate) for which the state is now bearing all of the cost. For example:

- The law will immediately allow states that cover low-income childless adults through state-funded programs (such as Connecticut and Minnesota) to cover these adults through Medicaid instead, thereby reducing state expenditures.

- The law will dramatically reduce the number of people with no health insurance over time, so state obligations to fund hospital care for the uninsured will necessarily decline.[22] In 2008, state and local governments shouldered $10.6 billion, or nearly 20 percent, of the cost of caring for uninsured people in hospitals, according to Urban Institute research. [23] Urban Institute researcher John Holahan notes that states’ savings from no longer having to finance as much of the cost of providing uncompensated care to the uninsured may fully offset the small increase in Medicaid costs resulting from the Medicaid expansion.[24]

- By reducing the percentage of people who are uninsured, the new law also will reduce state costs in providing mental health services to the uninsured. State and local governments provide 47 percent of the funding for state mental health agencies, amounting to $14.7 billion in 2006. [25]

Thus, a portion of the $20 billion that CBO estimates states will incur in additional state Medicaid costs under the new law will be offset by state savings in other areas, as a result of more people being insured.[26] In other words, some of the additional state spending on Medicaid will be substituting for existing state spending, and such spending now will qualify for federal Medicaid matching funds for the first time.

Milliman says it did not include these savings because the goal of the reports was to provide estimates of the states’ Medicaid budget exposure, rather than to conduct as assessment of the health reform law’s overall fiscal or economic impact on the states. From a state budgeting perspective, however, one cannot overlook savings that would accrue to other parts of the state budget as a result of the Medicaid expansion. States do not budget for Medicaid or other programs in isolation. If the Medicaid expansion results in savings elsewhere, those savings should be reflected, as they will affect states’ overall budget picture.

Health reform also may bring other, non-budgetary benefits to states. For example, the Medicaid expansions, new subsidies, and insurance-market reforms will improve access to health insurance for large numbers of individuals. The resulting increase in the number of people with health insurance should help reduce the number of state residents with preventable illnesses, which should contribute to healthier, and hence somewhat more productive, state workforces.

End Notes

[1] January Angeles and Matthew Broaddus, “Federal Government Will Pick Up Nearly All Costs of Health Reform’s Medicaid Expansion,” Center on Budget and Policy Priorities, Revised June 18, 2010.

[2] John Holahan and Irene Headen, “Medicaid Coverage and Spending in Health Reform: National and State-by-State Results for Adults at or Below 133% FPL,” Kaiser Commission on Medicaid and the Uninsured, May 2010.

[3] Robert Damler, “Letter to Anne Murphy, Secretary of the Indiana Family and Social Services Administration, on the Patient Protection and Affordable Care Act With House Reconciliation – Financial Analysis,” Milliman, Inc., May 6, 2010; John Meerschaert, “Financial Impact Review of the Patient Protection and Affordable Care Act As Amended by H.R. 4782, The Reconciliation Act of 2010 on the Mississippi Medicaid Budget,” Milliman, Inc., October 1, 2010; and Robert Damler, “Letter to Vivianne Chaumont, Director of the Nebraska Division of Medicaid and Long-Term Care, Department of Health and Human Services, on the Patient Protection and Affordable Care Act with House Reconciliation – Financial Analysis,” Milliman, Inc., August 10, 2010.

[4] Congressional Budget Office, “Letter to the Honorable Nancy Pelosi Providing an Estimate of the Direct Spending and Revenue Effects of an Amendment in the Nature of a Substitute to H.R. 4872, the Reconciliation Act of 2010 (Final Health Care Legislation),” March 20, 2010.

[5] States that have already expanded coverage to parents and childless adults with incomes up to the poverty line through either Medicaid or a separate state-funded program will receive these enhanced matching rates for covering childless adults through Medicaid, starting in 2014.

[6] Congressional Budget Office, op cit. A study conducted by the Urban Institute for the Kaiser Commission on Medicaid and the Uninsured has similar findings. According to that study, the federal government will finance 95 percent of the cost of the Medicaid expansion over the next 10 years. While Medicaid enrollment will increase by 27.4 percent, state costs will only increase by 1.4 percent relative to what states would have otherwise spent. See John Holahan and Irene Headen, “Medicaid Coverage and Spending in Health Reform: National and State-by-State Results for Adults at or Below 133% FPL,” Kaiser Commission on Medicaid and the Uninsured, May 2010.

[7] Nationally, the median income eligibility limit is 38 percent of the poverty line for unemployed parents and 64 percent of the poverty line for working parents. Donna Cohen Ross, Marian Jarlenski, Samantha Artiga, and Caryn Marks, “A Foundation for Health Reform: Findings of a 50 State Survey of Eligibility Rules, Enrollment and Renewal Procedures, and Cost-Sharing Practices in Medicaid and CHIP for Children and Parents During 2009,” Kaiser Commission on Medicaid and the Uninsured.

[8] Milliman’s estimates of the cost to states of the Medicaid coverage expansion include two costs that the CBO estimates do not include. First, Milliman assumes that states will incur costs as a result of a drug-rebate provision in the health reform law. As the box on page 9 explains, this assumption was valid at the time that Milliman issued its initial reports but is no longer valid, as a result of an HHS ruling in late September that largely eliminates these new state costs. Second, Milliman assumes that a provision of the law that increases Medicaid payment rates for primary care services in 2013 and 2014, at full federal expense, will continue beyond 2014 with states having to pick up a share of the cost in those years. As explained in the box on page 6, this assumption is dubious; it goes well beyond what the law requires. These two factors account, however, for only a relatively minor share of the overall costs estimated in the Milliman reports.

[9] Dahlia Remler and Sherry Glied, “What Other Programs Can Teach Us: Increasing Participation in Health Insurance Programs,” American Journal of Public Health, January 2003.

[10] Sherry Glied, Jacob Hartz, and Genessa Giorgi, “Consider It Done? The Likely Efficacy of Mandates for Health Insurance,” Health Affairs, November/December 2007.

[11] For example, Mississippi Governor Haley Barbour has said that he “fully expect[s] more than 400,000 new individuals will be added to the Medicaid rolls,” referencing Milliman’s analysis that the state’s Medicaid program would enroll an additional 408,000 individuals under the full participation scenario. See Letter to Mississippi State Legislators from Governor Haley Barbour, October 8, 2010.

[12] Individuals automatically receive their Medicare card by mail three months before their 65th birthday. Those who do not wish to participate in Part B must actively opt out.

[13] The participation rate is defined as the number of eligible children who are enrolled in Medicaid or CHIP as a percentage of the sum of the number of children who are enrolled and the number who are eligible for Medicaid and CHIP but are uninsured. The denominator does not include eligible children who have private insurance. Counting all eligible children in the denominator, regardless of their insurance status, would result in a much lower participation rate. Genevieve Kenney, Victoria Lynch, Allison Cook, and Samantha Phong, “Who and Where Are the Children Yet to Enroll in Medicaid and the Children’s Health Insurance Program?” Health Affairs, Volume 29, Number 10

[14] Kenney, Lynch, Cook, and Phong, op cit, and Thomas Selden, Julie Hudson, and Jessica Banthin, “Tracking Changes in Eligibility and Coverage Among Children, 1996-2002,” Health Affairs, Volume 23, Number 5.

[15] January Angeles and Matthew Broaddus, “Medicaid Expansion in Health Reform Not Likely to ‘Crowd-Out’ Private Insurance,” Center on Budget and Policy Priorities, June 22, 2010.

[16] See, for example, Gestur Davidson, Lynn Blewett, and Kathleen Call, “Public Program Crowd-out of Private Coverage: What Are the Issues,” The Synthesis Project, Robert Wood Johnson Foundation, June 2004; Lisa Dubay, “Expansions in Public Insurance and Crowd Out: What the Evidence Says,” Kaiser Family Foundation, October 1999; and Anna Sommers, Steve Zuckerman, Lisa Dubay, and Genevieve Kenney, “Substitution of SCHIP for Private Coverage: Results from a 2002 Evaluation in Ten States,” Health Affairs 26:529-537, March/April 2007.

[17] These estimates are based on a Center on Budget and Policy Priorities (CBPP) analysis that applies crowd-out rates of between 10 percent and 20 percent to Milliman’s estimates of the Medicaid expansion costs under the different participation scenarios. The full participation scenario in Milliman’s Indiana, Mississippi and Nebraska analyses assumes that 100 percent of those with private insurance who become newly eligible for Medicaid will drop such coverage and shift to Medicaid. This clearly is a highly implausible assumption.

[18] Bianca DiJulio and Paul D. Jacobs, “Change in Percentage of Families Offered Coverage at Work, 1998-2005,” Kaiser Family Foundation, 2007.

[19] In Indiana, parents are only eligible for Medicaid if their income is below 22 percent of the poverty line, and there is no Medicaid coverage for adults without dependent children.

[20] Rob Damler “Experience under the Healthy Indiana Plan: The Short-Term Cost Challenges of Expanding Coverage to the Uninsured,” Milliman Inc., August 2009.

[21] The Urban Institute and Kaiser Commission on Medicaid and the Uninsured estimates based on data from Medicaid Statistical Information System (MSIS) and CMS-64 reports from the Centers for Medicare and Medicaid Services (CMS), 2010. Data provided were for 2007. Estimates were adjusted to 2009 dollars using the National Health Expenditure Survey’s estimate of the per capita growth in medical expenditures between 2007 and 2009.

[22] The Affordable Care Act would reduce federal assistance to hospitals that disproportionately serve the uninsured provided through the Medicaid Disproportionate Share Hospital (DSH) program on the assumption that hospitals will be providing less uncompensated care.

[23] Jack Hadley, et al., “Covering the Uninsured in 2008: Current Costs, Sources of Payment, and Incremental Costs,” Health Affairs, August 25, 2008.

[24] The Urban Institute estimates of the cost to states of the Medicaid expansion do not take into account the savings to states from no longer having to subsidize the same level of uncompensated care. Kaiser Family Foundation, Transcript for Briefing on “Medicaid Expansion in Health Reform: National and State Estimates of Coverage and Cost,” May 26, 2010.

[25] National Association of State Mental Health Program Directors Research Institute, Inc., “SMHA-Controlled Mental Health Revenues, By Revenue Source and by State, FY 2006,” accessed April 6, 2010 at http://www.nri-inc.org.

[26] States are also expected to receive a portion of the savings from applying the rebates that drug manufacturers pay the Medicaid program for prescriptions provided through Medicaid managed care plans.

More from the Authors