Tax Rate for Richest 400 Taxpayers Plummeted in Recent Decades, Even as Their Pre-Tax Incomes Skyrocketed

The effective federal income tax rate for the 400 taxpayers with the very highest incomes has declined by nearly half over the past two decades, even as their pre-tax incomes have grown five times larger, new IRS data show.[1]

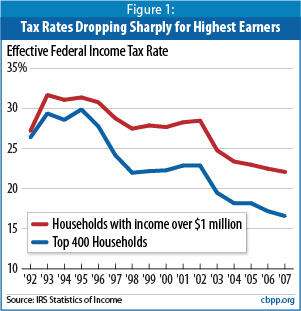

The top 400 households paid 16.6 percent of their income in federal individual income taxes in 2007, down from 30 percent in 1995. This decline works out to a tax cut of $46 million per filer in 2007, or a total of $18 billion in tax cuts for these households per year.

To make it into the top 400, a household needed an adjusted gross income of at least $35 million in 1992 (in 2007 dollars) and $139 million in 2007.

The decline in effective tax rates at the very top is due in large part to the capital gains tax cuts enacted in 1997 and 2003. The top marginal tax rate on capital gains is now 15 percent, less than half the top tax rate on wages and salaries. The top 400 taxpayers derived two-thirds of their income from capital gains and qualified dividends in 2007.

In short, the top 400 filers now pay much lower effective tax rates on vastly larger incomes.

Capital Gains Tax Cuts Played Large Role

The low effective tax rate for the top 400 filers is largely due to the fact that capital gains and qualified dividends are taxed at much lower rates than ordinary income. In 2007, the top 400 filers derived 66 percent of their income from capital gains and dividends, compared to 22 percent for filers making between $500,000 and $1 million and just 2 percent for those making under $50,000. It is not surprising that two of the largest reductions in effective tax rates for the top 400 filers occurred in two two-year periods (1996-1998 and 2002-2004) that coincided with the capital gains tax cuts enacted in 1997 and 2003 (and, to a lesser extent, the dividend tax cut enacted in 2003). [2] Additionally, these households benefited from the reduction in the top two marginal income tax rates enacted in 2001.

Currently the top marginal tax rate on capital gains and dividend income is 15 percent, less than half the top rate on wages and salaries. The Obama Administration’s FY2011 budget proposes to raise this rate to 20 percent for high-income households, still well below the 28 percent capital gains tax rate enacted under the Reagan Administration and in effect for most of the 1990s. For dividends, at 20 percent the top rate would be roughly half of what it was during the prosperous 1990s. Under the Administration’s proposal, therefore, the very highest-income filers would continue to pay income tax at very low effective rates.

Top Earners Also Enjoyed Rapid Income Gains in Late 1990s and Last Expansion

Even as their effective tax rates were declining sharply, high-income filers benefited disproportionately from economic growth, other IRS data show. During the last economic expansion (from the end of 2001 to the end of 2007), two-thirds of the nation’s total income gain flowed to the highest-income 1 percent of Americans.[3] And between 1992 and 2007, the average pre-tax income of the top 1 percent of filers more than doubled, after adjusting for inflation, rising by 114 percent. [4]

The top 400 taxpayers — 3 out of every 1 million filers — enjoyed even larger gains in pre-tax incomes. Between 1992 and 2007, their average adjusted gross income increased by over 400 percent, after adjusting for inflation: from $68 million to $345 million (in 2007 dollars). Their incomes grew rapidly between 1995 and 2000, dropped during the 2001 recession, then rose rapidly again from 2002 to 2007.

Because of the steep reduction in effective tax rates for the top 400 households, their after-tax incomes grew even faster than their pre-tax incomes. Between 1992 and 2007, their average income after federal income taxes increased by 475 percent.

Although the 2007 data reflect the height of the last economic expansion, effective tax rates on the richest 400 taxpayers will likely remain very low after the current recession, largely because the portion of its overall income this group derives from capital gains has remained relatively constant over the past decade. In the last recession, this figure dropped from 64 percent in 2000 to 55 percent in 2002, before climbing again amidst further capital gains tax cuts and a strong stock market. If the markets rebound and preferential capital gains tax rates are extended, the very highest-income filers will continue to enjoy very low effective tax rates into the future, even as budget deficits become a more serious problem.

End Notes

[1] The current IRS data series covers 1992 to 2007 and is available at http://www.irs.gov/pub/irs-soi/07intop400.pdf. The original IRS study is Michael Parisi and Michael Strudler, “The Top 400 Individual Income Tax Returns Reporting the Highest Adjusted Gross Income Each Year, 1992-2000,” IRS Statistics of Income Bulletin, Spring 2003, Publication 1136. While consistent data are not available prior to 1992, David Cay Johnston shows that the effective tax rate for the top 400 taxpayers was 42 percent in 1961. See David Cay Johnston, “Is Our Tax System Helping Us Create Wealth?” Tax Notes, December 21, 2009, 1375-1377. See also David Cay Johnston, “Tax Rates for Top 400 Earners Fell as Income Soars, IRS Data Show,” Tax Notes, February 18, 2010.

[2] Both the capital gains tax cuts took effect mid-year. As a result, they had some effect on effective tax rates in the year of enactment, but their full effects were not felt until the following year; hence, the effects of these tax cuts are reflected in the data over the 1996-1998 and 2002-2004 periods. Reductions in marginal income tax rates enacted in 2001 and accelerated in 2003 undoubtedly also had a significant impact on tax rates for this group. See also Martin A. Sullivan, “Is the Income Tax Really Progressive?” Tax Notes, December 14, 2009, 1135-1137.

[3] See Avi Feller and Chad Stone, “Top 1 Percent of Americans Reaped Two-Thirds of Income Gains in Last Economic Expansion,” Center on Budget and Policy Priorities, September 9, 2009, .

[4] See Thomas Piketty and Emmanuel Saez, “Income Inequality in the United States: 1913-1998,” Quarterly Journal of Economics, February 2003. Their most recent data set is available at http://elsa.berkeley.edu/~saez/TabFig2007.xls.

More from the Authors