House Health Bill’s High-Income Surcharge: A Reasonable Approach

Impact on Small Businesses Would Be Modest

Reforming the health care system to provide universal health coverage is an urgent priority. But, facing huge projected budget deficits that have the nation on an unsustainable fiscal path, the White House and Congress must enact a health reform plan that is also fully financed and that reduces the growth rate of health care costs over the long term.

Policymakers have been considering two major proposals to help finance health care reform that represent sound tax policy: (1) limiting the tax exclusion for employer-provided health benefits, and (2) capping the value of itemized deductions at 28 percent or a somewhat higher level. Capping the exclusion has the added benefit of helping slow the growth of health care costs. House Democrats have now advanced a third major proposal that also represents sound tax policy: imposing a graduated surcharge on high-income taxpayers.[1]

The House surcharge proposal is reasonable and well-targeted. In recent decades, incomes have grown disproportionately for households at the top of the income scale, while their tax burden has fallen substantially. Moreover, despite charges to the contrary, the proposal would have only a small impact on small businesses. The congressional Joint Tax Committee estimates that it would have no impact at all on 96 percent of small business owners — broadly defined as any taxpayer with as little as $1 of business income — and that only half of the 4 percent of small business owners who would be affected derive more than a third of their income from a business.[2] At the same time, the House plan would enhance the ability of small businesses to offer affordable, quality health insurance to their employees (see box, p. 5).

High-Income Households Have Far Outpaced Others in Recent Decades

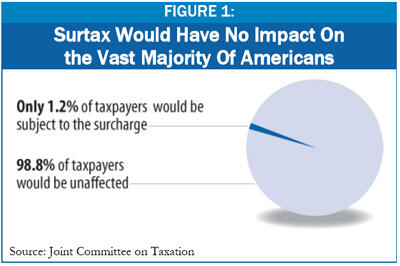

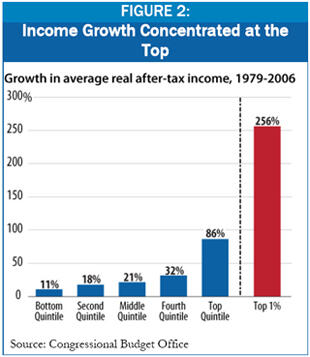

The surcharge would affect only the highest-income 1.2 percent of taxpayers, according to the Joint Tax Committee. Very high-income households have benefited handsomely — both absolutely and compared to the rest of the population — from both recent trends in pre-tax incomes and recent changes in tax policy. Congressional Budget Office data show that between 1979 and 2006 (the most recent year for which these data are available): [3]

- The before-tax income of the top 1 percent of U.S. households increased by 226 percent, on average (after adjusting for inflation), compared to an increase of just 15 percent for families in the middle fifth of the income spectrum.

- The effective federal tax rate for the top 1 percent of households — i.e., the share of their income that they owe in taxes — fell substantially, from 37 percent to 31.2 percent.

- The after-tax income of the top 1 percent of households increased by 256 percent, after adjusting for inflation, compared to an increase of 21 percent for families in the middle income quintile.

- As a result, the share of the nation’s total after-tax income going to the top 1 percent of households more than doubled, from 7.5 percent in 1979 to 16.3 percent in 2006. Altogether, households in the top 1 percent of the population had $617 billion more income in 2006 (or $656 billion more if measured in 2009 dollars) than they would have had if the 1979 income distribution still prevailed.

The Joint Tax Committee estimates that the surcharge would raise $81 billion in 2019.[4] The Administration estimates that the tax increases for high-income households proposed in its budget[5] would raise $96 billion in 2019.[6] Thus, the combined effect of the Administration’s proposal to let tax cuts enacted in 2001 and 2003 expire at the end of 2010 for people with incomes over $250,000 and the House Democrats’ new surcharge proposal would be to raise $177 billion from high-income households in 2019 ($153 billion when measured in 2009 dollars).

This means that the revenue raised from high-income households as a result of the surcharge plus the other Obama tax proposals would amount to less than a quarter of the $656 billion in after-tax income that has shifted to this group since 1979.[7]

Tax Levels for Top Households Would Remain Well Below Pre-Reagan Levels

If Congress enacted both the surcharge and the President’s tax proposals — and also allowed the tax rate on dividends to return to 39.6 percent when the 2001 tax law expires (which almost certainly will not happen, given that the President has proposed to set the top tax rate on dividends at 20 percent) — the top 1 percent of households would face an effective federal tax rate of 34.4 percent, according to the Urban Institute-Brookings Institution Tax Policy Center.[8] While well above the 31.2 percent effective tax rate that these households faced in 2006, this level would be well below the 37 percent effective rate that prevailed in 1979. [9]

Thus, the surcharge combined with tax measures that the Administration has proposed would leave the top 1 percent of households with a federal tax burden (measured in the percentage of income paid in federal taxes) roughly halfway between its level just prior to President Reagan and its level after President George W. Bush’s tax cuts were enacted. In other words, these policies would reverse only part of the large reduction in tax burdens that very high-income households have enjoyed over the last three decades.

Surcharge Would Have Modest Impact on Small Businesses

Critics of the surcharge have exaggerated its potential impact on small businesses.

- More than nine in ten small businesses would feel no impact whatsoever. Some 96 percent of taxpayers with business income would not owe the surcharge, according to both the Joint Tax Committee on Taxation and the Tax Policy Center. [10]

The 4 percent of remaining “small businesses” affected by the surcharge include taxpayers that stretch the definition of the term. Most Americans would not describe the nation’s wealthiest 400 people as “small businesses.” But with lots of money to invest, these “Top 400” receive a substantial amount of business income. In 2006 (the most recent year for which we have data), the Top 400 had more than $15 billion in S corporation and partnership income, according to the IRS. [11]

Along with many of the wealthiest 400 taxpayers in America, the following types of individuals also meet the definition of “small business”:- a partner in a large law or accounting firm;

- a wealthy individual who rents out his or her vacation home (given that such rental income is filed under Schedule E); and

- a Wall Street bond trader who receives a multi-million dollar bonus and invests some of it in an investment partnership.

- Only a small share of those paying the surcharge would be small businesses. Claims that most affected taxpayers would be small businesses are incorrect. Just 23 percent of taxpayers who would pay the surcharge derive more than half of their income from a business (or businesses), according to the Tax Policy Center. (Note that just 1.4 percent of tax filers who have any business income both derive more than half of their total income from business sources and would face the surcharge, according to the Tax Policy Center). [12]

- During the current recession, small businesses are receiving tax cuts from the federal government, not tax increases. The economic recovery package that the Administration and Congress enacted in February includes tax cuts specifically aimed at small businesses. For example, the net operating loss provision of the recovery package applies only to small businesses and allows them to use losses they incurred in 2008 to secure refunds for taxes that they paid going back five years, instead of the usual two years. Meanwhile, the surcharge proposal, which would affect just a tiny share of small businesses as noted above, would not go into effect until 19 months from now, in 2011.

- Businesses can choose to be either a “pass-through entity” or a C corporation. Some critics have asserted that the surcharge would place so-called “pass-through entities” (Subchapter S corporations, sole proprietorships, and partnerships) at a tax disadvantage compared to Schedule C corporations, since only the former would potentially owe the surcharge. But firms often organize themselves as pass-through entities in order to reduce their tax liability, and they could choose to organize themselves as Schedule C corporations instead if the surcharge made that preferable from a tax standpoint.

- Recent history contradicts the claim that raising taxes on high-income households weakens small-business job growth. Critics of proposals to increase taxes on upper-income households often argue that they would harm middle-income households by placing their jobs at risk. Critics of President Clinton’s economic plan made this argument in the early 1990s. Subsequent history, however, contradicted this claim: small-business job growth was more than twice as strong during the Clinton years, when Congress raised taxes on high-income households, than during the George W. Bush years, when Congress cut them. This experience shows that many factors affect job growth besides tax rates on high income individuals.[13]

Several Elements of House Plan Designed to Help Small Businesses

The House plan would enhance the ability of small businesses to offer affordable health insurance to their employees. At present, smaller firms are much less likely than large firms to offer health benefits to their workers. When they do offer health benefits, the plans tend to provide less comprehensive benefits and impose higher deductibles. Moreover, workers with family coverage in small firms typically contribute significantly more to the cost of insurance than workers in large firms. The House plan would:

- Eliminate insurers’ ability to increase premiums for small businesses based on their workers’ health status and other factors. In many states, insurers currently can vary the premiums they charge small businesses based on a number of factors, such as firm size, industry, geographic location, and the characteristics of their employees. If a small business has a disproportionate number of older workers (or if even a single employee incurs unusually high health expenses), it may find that quality health insurance is unavailable or is priced out of reach. The House plan would prohibit insurers from varying premiums due to health status and other factors, and it would sharply limit their ability to increase premiums for firms with older workers.

- Allow small businesses to buy health coverage through a new health insurance exchange in order to lower administrative costs and ensure access to quality plans. At present, small employers pay more and get less for their health insurance dollars than large corporations do, in part because their administrative costs for health insurance are considerably greater. Allowing small businesses to purchase health insurance for their workers through the new health insurance exchange, as the House plan would do, would significantly reduce their administrative costs. The plan would also require all plans purchased through the exchange to meet certain minimum benefit standards. As a result, the exchange would make it easier for small businesses to find more comprehensive health plans at a more affordable price than is the case today.

- Provide tax credits for the smallest firms to help them offer coverage. The smallest businesses, particularly those with larger shares of low-wage workers, tend to be least able to offer health coverage. The House plan would provide a tax credit of 50 percent of a small employer’s health insurance costs — a significant subsidy for very small firms.

In addition, the House plan’s requirement that employers provide health insurance or otherwise contribute to the cost of coverage for their workers should not have a major effect on small businesses. As the Congressional Budget Office has explained, employers would largely pass through the cost of meeting this type of requirement to their employees in the form of lower wages than the firm otherwise would pay, just as firms that do offer coverage pass through the costs to their workers. Because employees rather than employers would bear most of the cost, CBO finds that this type of requirement would have only a relatively minor effect on employment.a For the same reason, such a requirement should not substantially affect employers’ bottom line.

a Congressional Budget Office, “Effects of Changes to the Health Insurance System on Labor Markets,” July 13, 2009.

End Notes

[1] For a couple, the surcharge would represent 1 percent of income between $350,000 and $500,000; 1.5 percent of income between $500,000 and $1 million; and 5.4 percent of income in excess of $1 million. For an individual, the surcharge would represent 1 percent of income between $280,000 and $400,000; 1.5 percent of income between $400,000 and $800,000; and 5.4 percent of income in excess of $800,000. If the health cost savings the bill projects do not materialize, the 1 percent rate would rise to 2 percent and the 1.5 percent rate would rise to 3 percent.

[2] According to House Ways and Means Committee Fact Sheet, “Health Care Surcharge Would Not Affect 99% of Households,” July 14, 2009, http://waysandmeans.house.gov/media/pdf/111/healthcs.pdf.

[3] Congressional Budget Office, “Data on the Distribution of Federal Taxes and Household Income,” April 2009, http://www.cbo.gov/publications/collections/taxdistribution.cfm.

[4] “Estimated Effects of the Revenue Provisions of H.R. 3200, The “America’s Affordable Health Choices Act of 2009,’” Fiscal Years 2010 – 2019, JCX-31-09, July 14, 2009, http://jct.gov/publications.html?func=startdown&id=3570.

[5] The Administration proposals are to reinstate the 36 and 39.6 percent tax brackets, reinstate the personal exemption phaseout and limitation on itemized deductions, and impose a 20 percent rate on capital gains and dividends on taxpayers earning more than $250,000 (married) and $200,000 (single).

[6] Office of Management and Budget, Updated Summary Tables, Budget of the U.S. Government, Fiscal Year 2010, May 2009, p. 22, available at http://www.whitehouse.gov/omb/budget/fy2010/assets/summary.pdf.

[7] CBPP calculations based on Congressional Budget Office and IRS Statistics of Income data.

[8] Tax Policy Center Table T09-0348, “America's Affordable Health Choices Act of 2009 Surcharge on High Income Individuals,” July 14, 2009, http://www.taxpolicycenter.org/numbers/Content/PDF/T09-0348.pdf.

[9] Congressional Budget Office, “Effective Federal Tax Rates for All Households, by Comprehensive Household Income Quintile, 1979-2006,” April 2009, http://www.cbo.gov/publications/collections/tax/2009/effective_rates.pdf .

[10] According to House Ways and Means Committee Fact Sheet, “Health Care Surcharge Would Not Affect 99% of Households,” http://waysandmeans.house.gov/media/pdf/111/healthcs.pdf; Tax Policy Center Table T09-0351, “Distribution of Tax Units with Business Income, by Modified Adjusted Gross Income Level, 2011,” July 14, 2009, http://www.taxpolicycenter.org/numbers/displayatab.cfm?Docid=2426&DocTypeID=7 .

[11] IRS, “The 400 Individual Income Tax Returns Reporting the Highest Adjusted Gross Incomes Each Year, 1992-2006,” p. 4, http://www.irs.gov/pub/irs-soi/06intop400.pdf.

[12] Tax Policy Center Table T09-0351, “Distribution of Tax Units with Business Income, by Modified Adjusted Gross Income Level, 2011,” July 14, 2009, http://www.taxpolicycenter.org/numbers/displayatab.cfm?Docid=2426&DocTypeID=7 .

[13] Jason Levitis and Chuck Marr, “History Contradicts Claim That President’s Budget Would Harm Small Business Job Creation,” Center on Budget and Policy Priorities, March 26, 2009, https://www.cbpp.org/cms/index.cfm?fa=view&id=2742.

More from the Authors