What the 2007 Trustees' Report Shows about Social Security

Executive Summary

On April 23, the Social Security Board of Trustees released the 67th annual report on the program’s financial and actuarial status. The report projects that Social Security’s trust fund reserves will be exhausted in 2041, one year later than in last year’s projection. In 2041, Social Security will be able to pay 75 percent of scheduled benefits, rather than full benefits.

This CBPP analysis highlights several points about the trustees’ report:

-

The trustees’ report reaffirms that Social Security does not face a near-term crisis and can continue to pay full benefits for more than three decades but will eventually face a significant imbalance. A sizeable shortfall between Social Security income and Social Security benefits should not be acceptable to the public or policymakers, and action is needed to restore the program’s long-term solvency.

-

The trustees’ report finds a slight improvement from last year’s projections in Social Security’s financial status, largely as a result of updates in program data and minor changes in methods and assumptions. The year that the trust fund will be exhausted moved back to 2041, from 2040 in last year’s projections, and the actuarial shortfall declined to 1.95 percent of taxable payroll (compared with 2.02 percent in last year’s projections). The program will be able to pay 75 percent of full benefits when the trust fund is exhausted in 2041 (compared with 74 percent in 2040 in last year’s projections). Social Security also will still be able to pay 70 percent of full benefits at the end of the 75-year projection window in 2081.

-

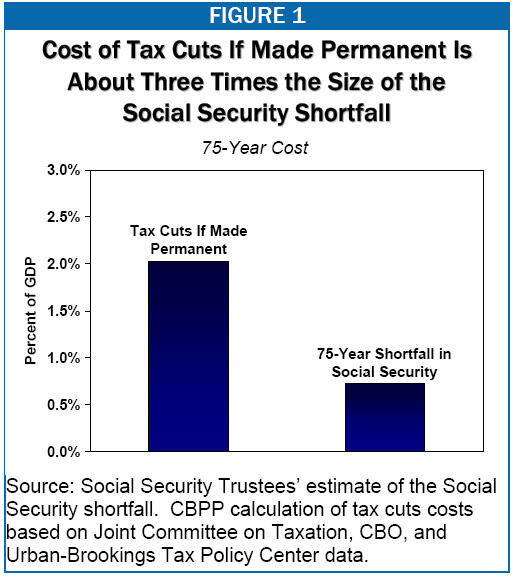

Anyone concerned about Social Security’s long-term shortfall ought to be equally if not more concerned about the long-term fiscal impact of extending the 2001 and 2003 tax cuts. Making the tax cuts permanent will cost about three times as much, over the next 75 years, as the 75-year shortfall in Social Security (see Figure 1). Any attempt to address the looming fiscal challenges should include Social Security, Medicare (and the U.S. health care system as a whole), and overall government revenues.

An Overview of the Projections in the New Trustees’ Report

The new trustees’ report contains several key figures that document the challenge Social Security faces:

- The trustees project that in 2017, benefit payments will begin to exceed Social Security’s tax revenues. At this point, Social Security will start using some of the interest it earns on its trust fund bonds to pay benefits. Nevertheless, the trustees project that in 2017, the trust fund will have $4.7 trillion in assets, and that these assets will increase by another $1.3 trillion over the following nine years.[1]

- The balances in the trust fund will peak in 2026. After that date, Social Security will start redeeming the bonds in the trust fund in order to raise the additional funds needed to pay full benefits. The combination of tax revenues, interest earnings, and proceeds from redeeming Treasury bonds will be sufficient for Social Security to pay full benefits for fifteen years after 2026.

- The trustees project that there will be no more bonds left to redeem and the Trust Fund will be exhausted in 2041. After that, the trust fund will continue to receive annual revenues from payroll taxes and from the partial taxation of the Social Security benefits that higher-income beneficiaries receive. That revenue, however, will not be sufficient to pay full benefits.

- After the trust fund is exhausted in 2041, Social Security’s tax revenue will be sufficient to pay 75 percent of promised benefits. This percentage will fall gradually to 70 percent of benefits in 2081.

- The new report places the amount of the 75-year shortfall — that is, the amount by which the trust fund’s income and revenues over the next 75 years will fall short of what is needed to pay full benefits over the period — at $4.7 trillion in net present value,[2] or 0.7 percent of GDP. The shortfall is 1.95 percent of taxable payroll.[3]

- The new report places the “infinite horizon” (i.e., through eternity) shortfall at 1.2 percent of GDP and 3.5 percent of taxable payroll, which is down slightly from last year’s estimate as a result of the same changes in methods and assumptions that produced a slight improvement in some measures of Social Security’s financial condition.

The infinite horizon measure, which was first included in the 2003 report, has been strongly criticized as a highly speculative and misleading measure by the American Academy of Actuaries and other Social Security analysts. Changes in the dollar value of the infinite horizon deficit are particularly misleading because they can be large (as they were a year ago) even when there is no meaningful change in the real financial condition of the program.[4] In addition, nearly two-thirds of the infinite horizon deficit would be incurred after 2081, making it very sensitive to small changes in assumptions and consequently of very limited reliability for policymakers.

How the Projections Compare with Those Made In Previous Years

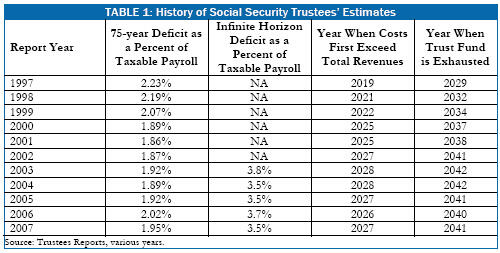

In general, the key dates and the overall financial picture in the 2007 trustees’ report represent improvement over the trustees’ 1997-2001 reports and little change from the 2002-2006 reports (see Table 1). The long-term deficit in Social Security declined from2.23 percent of taxable payroll in the 1997 report to 1.89 percent in the 2000 report and has drifted up slightly since then. The date by which the trust fund is projected to be exhausted has moved farther into the future — from 2029, as forecast in 1997, to 2041 as projected in the current report. In other words, Social Security has a long-run financing shortfall that must be addressed, but the magnitude of the challenge has not been getting appreciably worse.

The principal reason that Social Security’s underlying financial outlook changes over time is that the trustees revise their assumptions about future economic and demographic variables and their projection methodologies. Those changes interact with the purely technical fact that the mere passage of time has the effect of worsening some measures of the program’s financial condition.

The passage of time affects the 75-year deficit, for example, by bringing in another year with a relatively large deficit. Thus, in going from the 2006 to the 2007 projection, the relatively large deficit for 2081 was added. An analogous effect happens with the infinite horizon shortfall.[5]

In this year’s report, the reduction in the Social Security shortfall due to changes in methods and assumptions was large enough to more than offset the increase in the shortfall due to the passage of time. As a result, the key indicators in 2007 continue to look roughly as they did in 2002-2006. That the outlook for Social Security has been relatively stable does not negate the fact that the program faces large deficits down the road, reflecting, among other things, the retirement of the baby boom generation. But it does mean that the magnitude of the challenge we face to put the program on a sound long-term basis is not becoming unmanageable. That is especially evident when looking at measures that express the long-term shortfall as a percentage of GDP or taxable payroll (that is, relative to the resources available to meet the challenge), rather than simply in dollar terms.

Social Security’s Imbalances Are Dwarfed by the Cost of the Tax Cuts

The Social Security shortfall contributes to the government’s long-term fiscal challenge, but it is by no means the primary source of this challenge. Eliminating Social Security’s shortfall would nevertheless be an important step in addressing America’s overall fiscal challenges.

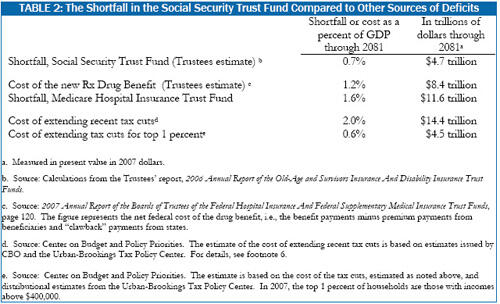

Over the next 75 years, the Social Security shortfall amounts to 0.7 percent of GDP, a relatively modest share of the total federal budget shortfall projected for this period. Recently enacted policies, particularly the tax cuts (if made permanent) and the prescription drug benefit, will have a larger impact on the long-term fiscal deficit.

- Extending the 2001 and 2003 tax cuts and other tax provisions scheduled to expire in coming years would cost 2.0 percent of GDP over the next 75 years, or $14 trillion in net present value.[6]

- This is about three times as great as the Social Security trustees’ estimate of the Social Security shortfall (see Table 2).

- The cost of extending only the tax cuts for the top 1 percent of Americans, those currently making more than $400,000, is nearly as large as the trustees’ estimate of the 75-year Social Security shortfall.

- The prescription drug benefit also will cost more than the Social Security shortfall, totaling $8.4 trillion, or 1.2 percent of GDP, in present value over the next 75 years.

Conclusion

The new trustees’ report is consistent with previous reports. It shows that Social Security faces a significant but manageable challenge. Acting sooner rather than later will help reduce the size of the eventual adjustments, but the trustees’ report indicates that Social Security does not face a deep structural crisis requiring drastic changes.

Putting the trustees’ report in a broader fiscal context suggests that the sources of the future large imbalances in the federal budget as a whole need to be addressed. The sources of these imbalances include not only Medicare and Social Security, but revenues as well. If the 2001 and 2003 tax cuts are made permanent, they will contribute far more to budget deficits than Social Security will.

In 1983, Congress and President Reagan acted on recommendations made by the Greenspan Commission and strengthened Social Security’s financial status through a combination of benefit and revenue measures. Various combinations of modest benefit reductions and revenue increases have been proposed by economists Peter Diamond and Peter Orszag, economists Henry Aaron and Robert Reischauer, former Social Security Commissioner Robert Ball, and the AARP. Such steps could restore Social Security solvency while beginning to reduce federal budget deficits and debt.

End Notes

[1] Technically, Social Security has two distinct trust funds: one for old-age and survivors benefits and one for disability benefits. This report follows the standard convention in referring to the combined balance as “the Social Security trust fund.”

[2] Net present value is the equivalent amount that today, with interest, would exactly cover the future shortfall.

[3] Note that, per the trustees’ convention, the shortfall as a share of taxable payroll includes the cost of a “target fund” — that is, a trust fund balance at the end of 2081 that would be sufficient to pay full benefits in 2082 even in the absence of any trust fund income.

[4] Illustrating the potentially misleading nature of dollar estimates, the infinite horizon estimate (and the 75-year estimate for that matter) is smaller as a percent of GDP and as a percent of taxable payroll this year than last year, yet the dollar estimate is larger. See Richard Kogan, Robert Greenstein, and Jason Furman, “Will the Administration Claim the Cost of Fixing Social Security Rose $700 Billion Because Congress Did Not Act Last Year?” Center on Budget and Policy Priorities, April 28, 2006.

[5] In moving from 2006 to 2007, every future year’s balance is discounted by one less year, which increases the size of that year’s balance in the present-value calculation.

[6] These estimates reflect the cost of extending the 2001 and 2003 tax cuts (including the portion of the cost of AMT relief created by the tax cuts) plus the cost of extending various other expiring tax provisions (commonly referred to as the “extenders”). In order to compare these costs with the Social Security shortfall, we measure the (present-value) cost of extending expiring tax provisions and display this cost as a share of (the present value of) total GDP, 2007-2081. Through the first ten years, we base our estimates on CBO and Urban Institute-Brookings Institution Tax Policy Center data. Thereafter, we assume that the cost of the tax cuts remains constant as a share of GDP. For more details on the Center’s estimate of the costs of extending expiring tax provisions, see Richard Kogan, Matt Fiedler, Aviva Aron-Dine, and James Horney, “The Long-Term Fiscal Outlook is Bleak,” Center on Budget and Policy Priorities, January 29, 2007.

More from the Authors