Tax Reform and Poverty

The tax system has a pervasive impact on poverty, both directly through its role in the distribution of society’s resources and indirectly through its effects on the incentives for economic decisions like working and saving. The two most important facets of the tax system for low-income families are payroll taxes and the Earned Income Tax Credit (EITC), the former of which levies a tax on earned income and the latter provides a tax credit for earned income.

Attention to the impact of tax reform on low-income families is especially important in light of the persistence of poverty, wage stagnation at the bottom, and the growth of income inequality. In 2004, 37 million Americans were below the official poverty line, including 13 million children.[2]

Underlying the persistence of poverty has been wage stagnation at the bottom. From 1973-2003, real hourly wages for men at the 10th percentile of the earnings distribution fell 3 percent. At the same time, median wages fell 1 percent and wages for workers at the 90th percentile rose 22 percent. The economic blow for families at the bottom of the income spectrum was partially cushioned by several expansions in the EITC which more than account for the entire 7 percent growth in after-tax incomes for the bottom quintile over this period.

The causes of wage stagnation and rising inequality have been much debated. Many of the potential causes, like skill-biased technological change, a shift to a winner-take-all society, and increased competition undermining the bargaining power of labor, do not lend themselves to direct policy solutions. Regardless of the cause, however, further reforms and changes in the tax system have the potential to continue to ameliorate some of the underlying economic trends and ensure that all income groups share in the continued strong productivity growth.

President Ronald Reagan once called the EITC “the best anti-poverty, the best pro-family, the best job creation measure to come out of Congress.” Although some conservatives criticize the EITC, it continues to maintain substantial bipartisan support and frequent calls for its expansion. Recently, for example, New York Times columnist David Brooks stated, “we should raise the earned-income tax credit to lessen [low-income families’] economic stress.”[3] Kevin Hassett of the American Enterprise Institute (AEI) also noted that, “low wages generally in some sectors of the economy may be a legitimate policy challenge. A correct response might be to expand the earned income tax credit.”[4]

Rarely, however, do proponents spell out what they would actually do to expand the EITC. This note proposes two potential versions of tax reform to expand and improve the EITC. The first builds on current law, changing the parameters of the EITC to make it more effective at reducing poverty (by expanding it for families with three or more children and increasing it for childless workers) and reducing the marriage penalty.

The second proposal is a more thorough tax reform, recasting the EITC as part of a broader consolidation and simplification of tax incentives for children. This is in the spirit of proposals originally made by David Ellwood and Jeffrey Liebman and by Robert Cherry and Max Sawicky and most recently endorsed by the President’s Advisory Panel on Federal Tax Reform.[5]

Current Law EITC

The EITC provides a refundable tax credit for working families that can either offset income taxes or be provided as a tax credit directly to the family. It was established in 1975 and significantly expanded by legislation in 1986, 1990, and 1993. In addition, 19 states (including the District of Columbia) offer EITCs that generally build on the federal credit.[6]

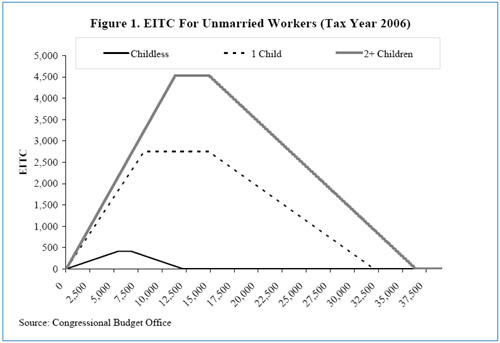

For a single mother with two children, the EITC provides a tax credit of 40 percent for every dollar earned up to $11,340 in tax year 2006.[7] A family earning between $11,340 and $14,810 will receive the maximum credit of $4,536. Thereafter, the EITC is reduced by 21.06¢ for each dollar earned until it is eliminated for earners above $36,348. The maximum EITC for families with one child is $2,747 and for childless workers is $412. Figure 1 shows the EITC as a function of income for households headed by an unmarried worker with various numbers of children.

In addition, the child tax credit is partially refundable – the so-called “additional child tax credit,” augmenting the EITC. In tax year 2006, families making over $11,300 are eligible for the additional child tax credit.

In 2003, 22.1 million households received $39.2 billion in EITCs — or an average of $1,782 per household (or $2,100 for a family with children).[8] Census data show that without the EITC, everything else being equal, an additional 4.4 million people would have been in poverty, including 2.4 million children. According to the Center on Budget and Policy Priorities, “Census data show that the EITC lifts more children out of poverty than any other single program or category of programs.”[9]

Just as important as the direct effect of the EITC is the indirect effect: studies have consistently found that the EITC increases labor force participation substantially for single mothers. The EITC can increase the reward for working by several thousand dollars. From 1984 to 1996, the employment rate for single mothers with children jumped 9 percentage points at the same time that the employment rate for single women without children fell slightly. Bruce Meyer and Dan Rosenbaum found that the expansions in the EITC explained more than 60 percent of the increased participation of single mothers.[10] Nada Eissa and Liebman found a similarly large increase in participation by single mothers following the 1986 expansion in the EITC.[11] The most recent and comprehensive study, by V. Joseph Hotz, Charles Mullin and John Karl Scholz, also finds substantial participation effects.[12]

In contrast, Eissa and Hilary Hoynes found that the EITC reduced labor force participation by married women, a group much more likely to be in the phase-out range of the EITC.[13] Whether a potential secondary earner chooses to work or provide childcare and other home services, however, is less significant for poverty than the work decisions by single mothers. In addition, overall, the EITC appears to increase labor force participation, because of the larger effects on single women with children and the fact that the credit primarily affects unmarried filers.

There is little evidence showing that the EITC reduces hours worked among those that do work. Roughly one half of single parents and three-quarters of married parents are in the phase-out range of the EITC, facing marginal tax rates as high as 46 percent (or even higher when the phase-out of transfer programs is considered).[14] In theory this, together with the income effect from the larger EITC, should lead to a reduction in hours worked. In practice, Eissa and Liebman and other studies have not found this effect, possibly because the hours worked decision is less tax sensitive than the participation decision or because workers do not understand the complex phase-out rules.

Limitations of the EITC for Reducing Poverty

The EITC has several limitations that could easily be addressed by strengthening the credit.

Poverty in Families with Three or More Children

The poverty rate for children in families with three or more children is 26 percent, more than twice the 12 percent poverty rate for families with one or two children. In total, although 37 percent of all children are in families with three or more related children, 55 percent of all children living in poverty are in such families.

The structure of the EITC is poorly designed to address this pattern of child poverty. According to the official Federal poverty line, a family with a third child would require an additional $4,004 to escape poverty. In addition, families with more children face larger childcare expenses if the parent or parents went to work. The principal child-related provisions in the tax code, the child tax credit and the dependent exemption, are provided on a per child basis. They are grounded in the philosophy that each additional child reduces a families ability to pay taxes, or increases its needs, by the same amount. In contrast, the EITC does not increase for families that have three or more children. Furthermore, the child tax credit itself is only refundable in a limited manner and thus does not provide additional assistance for families with three or more children until their income exceeds about $20,600, which is just below the poverty line.

| Table 1: | ||

|

| Official Poverty Rate (Money Income) | Poverty Rate After Taxes, EITC, and Near-cash Transfers |

| 1 child | 11.8% | 9.5% |

| 2 children | 12.5% | 9.3% |

| 3 children | 20.2% | 15.5% |

| 4 children | 34.6% | 29.5% |

| Total | 17.2% | 13.6% |

|

|

|

|

| Memo |

|

|

| 1-2 children | 12% | 9% |

| 3+ children | 26% | 21% |

| Source: Calculations using Current Population Survey data. | ||

In the absence of the EITC and other poverty-reducing tax and transfer programs, the poverty rate for families with two children would be slightly higher than for families with one child. But after accounting for taxes and transfers, which are more favorable to larger families, families with two children actually have a slightly lower poverty rate than families with one child. In contrast, although the tax and transfer system lifts many families with three or more children out of poverty, it does so for proportionately fewer of these families than for families with one or two children. As a result, the tax and transfer system increases the percentage gap between the poverty rate for larger families relative to the poverty rate for smaller families.

The EITC and Childless Adults

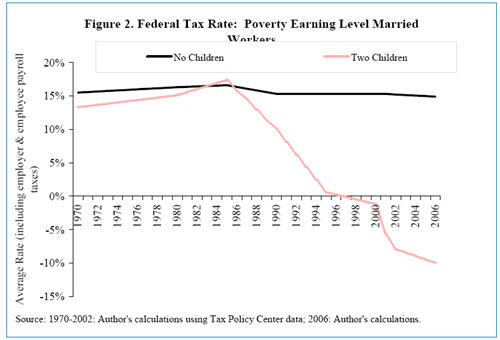

As the EITC and child tax credits have been expanded over the past twenty years, the disparity between taxes for families with children and childless families has grown dramatically. Figure 2 shows that married couples earning a poverty-level wage paid similar taxes – about 15 percent in total including the employer and employee share of payroll taxes – from 1970 through the mid-1980s. Since then, however, several rounds of EITC expansions and a partially refundable child tax credit have more than offset the increase in the payroll tax rate, cutting the married couple with two children’s tax rate by 25 percentage points – to -10 percent. At the same time, the payroll tax increase roughly offset income tax cuts leaving the childless family paying roughly the same share of its income in taxes.

Part of the widening disparity reflects several rounds of expansions of the EITC for families with children while the EITC for childless families remains relatively limited: it is available to childless adults between 25 and 64 and provides a credit of up to $412, phasing out entirely for single filers making over $12,120 (or married filers making over $14,120). Only 2 percent of the EITC goes to childless workers, totaling less than $1 billion in 2002.

As a result, childless adults – primarily young men – do not have anything resembling the incentives the EITC provides to join the paid workforce. In fact, childless adults pay positive taxes starting with their first dollar of earnings, as the EITC only offsets half of their payroll taxes (this statement reflects the standard assumption that workers ultimately bear the burden of both the employee and employer shares of the payroll tax). A single person without children making $8,500 will start to pay income taxes as well.

Failing to provide adequate incentives for low-income men to join the workforce contributes to poverty, crime, and other social problems.

The EITC Marriage Penalty

Individuals eligible for the EITC often face substantial marriage penalties. As a result of marrying, the family’s combined income could go up dramatically. In the relatively uncommon case where the mother was not working, this increase in income would make the family eligible for the EITC and thus provide a marriage bonus. More typically, the increase in income would move the family along the phase-out range of the EITC and thus reduce its benefits. Ellwood simulated the EITC for families surveyed by the Panel Survey on Income Dynamics (PSID) and found that 55 percent of them would have experienced EITC marriage penalties while 17 percent of families would experience marriage bonuses.[15] Janet Holtzblatt and Robert Rebelein also found substantial EITC marriage penalties.[16]

| Table 2 | |||

| Unmarried | Married |

| |

| Woman making $15,000 with two children | -$2,756| | -- |

|

| Man making $25,000 | $5,930 | -- |

|

| Total Taxes | $3,174 | $5,840 | +$2,666 |

| Source: Author’s calculations. | |||

The 2001 and 2003 tax cuts eliminated the marriage penalties facing most middle-class couples (and increased marriage bonuses) while reducing EITC marriage penalties. In a progressive tax system that levies identical taxes on families with identical incomes, it is not possible to eliminate all marriage penalties and bonuses. Eliminating the EITC marriage penalty entirely would be very expensive and would greatly increase marriage bonuses. A sensible policy has to strike some sort of balance in terms of fairness. In the case of the EITC, the marriage penalties are substantially more prevalent and relatively more severe than the marriage penalties facing middle-class taxpayers, suggesting that further reduction is warranted.

For example, Table 2 shows a hypothetical example that, based on the numbers estimates by Ellwood and Holtzblatt and Rebelein, is not atypical. The woman has two children and makes $15,000 annually. As a result, she gets a net federal tax credit of $2,756 (including the employee and employer share of payroll taxes) in 2006. A man makes $25,000 and pays $5,930 in federal taxes. When they get married their combined income puts them above the eligibility for the EITC and, as a result, their combined taxes are $5,840 – or $2,666 higher as a result of marrying. In this case, the marriage penalty leads to a 7 percent reduction in this family’s after-tax income.

The marriage penalty is related to the only evidence that the EITC has any negative impact on work incentives: the fact that it may reduce labor supply by married women.

The EITC, Complexity, and the Error Rate

Finally, the EITC is relatively complex. IRS Publication 596, which explains the EITC, is 56 pages long. GAO found that 14 percent of eligible taxpayers with children did not claim the EITC in 1999, although this estimate is imprecise.[17] This represents a higher take-up rate than most public programs, but is likely lower than, say, the “take-up rate” for dependent exemptions and other aspects of the tax system. Furthermore, the EITC suffers from some errors and overpayments, although these errors have probably been reduced in recent years and the current magnitude is not known. Finally, according to the IRS, 68 percent of EITC recipients use paid preparers, a higher fraction than for the population as a whole.[18]

Expanding and Improving the EITC

One approach to the issues addressed in the previous section would be to expand and simplify the EITC. Specifically:

Add a Third Tier for Families with Three or More Children

The first option would be to increase the EITC for families with three or more children. The phase-in rate for these families could be raised to 50 percent while keeping the other EITC parameters the same. For a woman with income at or above the phase-in threshold ($11,340 in tax year 2006) that would mean an additional $1,134. Even this amount would fall well short of the additional $4,004 the Federal poverty line assumes it takes for a single mother to raise a third child above the poverty line.

About 3 million families would benefit from this expansion for an average annual cost of $3 billion. As these families are among those most likely to be in poverty, this reform would be well targeted. Families with three children making less than $11,340 would see a reduction in their marginal rates (or, technically, even more negative marginal tax rates) while the only increase in marginal rates would be for families making between $36,350 and $41,730 (for singles or somewhat higher for married couples), a relatively small group and one unlikely to have much effect on work behavior.

Expand the EITC for Childless Workers

The EITC for childless workers currently provides a 7.65 percent tax credit on up to $5,380 of earnings. This proposal would double the credit to 15.3 percent to cover all payroll taxes and allow it on earnings up to $8,080, the same phase-in threshold for families with one child. The EITC would start phasing out at $10,000 for singles and $10,000 plus the marriage adjustment (discussed below) for married couples and would phase-out at a 15.3 percent rate.

In total, the maximum EITC would triple to $1,236 — an amount that appears large enough to lead to a meaningful increase in participation. About 4 million people would get a tax cut averaging $750 — for a total annual cost of $3 billion.

Reduce the EITC Marriage Penalty

EGTRRA increased the starting point of the phase-out of the EITC for married couples, raising it by $3,000 beginning in tax year 2008. For a family in the phase-out range of the EITC, this reduces the marriage penalty by $632. This is well below the typical marriage penalties estimated by Holtzblatt and Rebelein, providing motivation to raise the phase-out point by an additional $2,000. This would provide a tax cut of about $400 to roughly 3 million married couples, at a total cost of about $1.2 billion annually.

Simplify the EITC

In addition to these expansions, steps should be taken to simplify the EITC, although this paper does not address this issue in the context of the regular EITC.

Creating a Family Credit

An alternative approach, which has garnered an increasing amount of attention and support recently, is to consolidate the existing child tax benefits into one unified credit. Ellwood and Liebman proposed a set of plans, emphasizing eliminating the “middle-class parent penalty,” largely through tax cuts for middle-class families that reduced marginal rates and marriage penalties. Cherry and Sawicky proposed a similar plan. The expansion of the child tax credit to $1,000 by EGTRRA in 2001 accomplished some of what these plans proposed in terms of reducing taxes for families with children and reducing the “middle-class parent penalty.” The legislation did not, however, enact any of simplifications or consolidations.

In 2005, the President’s Advisory Panel on Tax Reform proposed an even more sweeping consolidation, incorporating the standard deduction, personal exemptions, child tax credit, additional child tax credit, 10 percent bracket, and EITC into two integrated credits: a work credit and a family credit.[19] The new structure was designed to replicate the existing distribution of tax burdens for moderate-income families, a goal it largely achieved.[20] The proposal would have simplified the existing tax structure and improved the take-up and compliance of refundable credits.

The Tax Panel’s proposal was not designed to address any of the issues discussed in this paper, like reducing child poverty. In addition, the Panel’s proposal is integrated into a framework that eliminates the distinction between the standard deduction and itemized deductions. While this may be a sensible component of a tax reform (in general it will increase horizontal equity at the expense of simplification), some may choose to separate out this element of the proposal from the other elements. This paper, therefore, proposes an alternative that maintains most of the simplifications and reforms of the Panel’s proposal while incorporating the expansions in the EITC described in the previous section and maintaining the distinction between the standard deduction and itemized deductions.

Specifically, this proposal would eliminate the dependent exemption and replace it with a child tax credit of $1,500.[21] The tax credit would be phased out for married couples starting at $200,000, along the lines of the existing dependent exemption.[22] The child tax credit would be refundable up to 34 percent of earnings for someone with one child, 40 percent of earnings for someone with two children, and 50 percent of earnings for someone with three or more children. In addition to the child credit, a simple work credit would roughly replicate the additional benefits of the EITC, including the childless EITC. Ideally, this framework should be designed in such a way that it would continue to facilitate the state EITCs which are based on the federal system.

In total this framework would reduce revenues (or increase costs) by less than $10 billion annually relative to current law and would provide many of the benefits discussed above, including more incentives for work, reduced poverty for larger families, and marriage penalty relief.

Broader Issues in Tax Reform and Poverty

Any reduction in taxes for moderate-income families, or any means-tested transfer program, has to confront a tradeoff. A well-targeted, cost-effective plan will necessitate higher marginal rates as the tax cuts/transfers are phased out. An alternative approach would be to reduce the already high marginal rates already embedded in the tax and transfer system, but this would do relatively little for lower-income families. Or, it is possible to reduce taxes and increase transfers for families at the bottom without increasing marginal rates, but this approach is very expensive and poorly targeted.

Everything else being equal, of course, lower marginal rates are preferable and the increased attention to the marginal rates caused by the phase-outs of various tax and transfer programs is useful. Ultimately, however, the best evidence suggests that at least some of the tradeoff between providing resources cost effectively and having to phase those programs out is worthwhile. As noted, the literature on the EITC finds scant evidence that the high marginal rates – nearly 50 percent for the tax system alone – reduce hours worked. Also, in an admittedly crude simulation, Jonathan Gruber and Emanuel Saez found that the optimal tax system would actually have larger transfers to low-income families (an $11,000 demogrant) and higher marginal rates as this demogrant was phased out (68 percent for the lowest-income taxpayers).[23]

Low-income issues should be an important part of other aspects of the tax debate, including ensuring fairness and efficiency by shifting social policies conducted through the tax code (like education, health, and retirement savings) to progressive, refundable tax credits. Ultimately, of course, tax reform will only be one part of a broader set of policies to address poverty and ensure that all Americans share in the enormous benefits of productivity growth.

End Notes

[1] Non-Resident Senior Fellow, Center on Budget and Policy Priorities and Visiting Scholar, NYU Wagner Graduate School of Public Service.

[2] Note, the official poverty statistics do not include the EITC, other taxes, or non-cash transfers like food stamps.

[3] David Brooks, March 9, 2006, “Both Sides of Inequality,” New York Times.

[4] Kevin Hassett, December 19, 2005, “Unions Wage Vicious, Misguided War on Wal-Mart,” Bloomberg.

[5] Robert Cherry and Max Sawicky, April 2000, “Giving Tax Credit Where Credit is Due,” Economic Policy Institute; David Ellwood and Jeffrey Liebman, 2001, “The Middle-class Parent Penalty: Child Benefits in the U.S. Tax Code,” James Poterba (ed.), Tax Policy and the Economy, MIT Press; and President’s Advisory Panel on Tax Reform, November 2005, Simple, Fair & Pro-Growth: Proposals to Fix America’s Tax System.

[6] Ami Nagle and Nicholas Johnson, 2006, “A Hand Up: How State Earned Income Tax Credits Help Working Families Escape Poverty in 2006,” Center on Budget and Policy Priorities.

[7] Unless noted otherwise, all estimates are for tax year 2006.

[8] IRS data.

[9] Robert Greenstein, August 17, 2005, “The Earned Income Tax Credit: Boosting Employment and Aiding the Poor,” Center on Budget and Policy Priorities. Although the EITC is second to Social Security in its reduction of the poverty gap for children, that is the total dollar shortfall from the poverty line. See Arloc Sherman, May 2, 2005, “Social Security Lifts 1 Million Children Above the Poverty Line,” Center on Budget and Policy Priorities.

[10] Bruce Meyer and Dan Rosenbaum, 2001, “Welfare, the Earned Income Tax Credit, and Labor Supply of Single Mothers,” Quarterly Journal of Economics, 116:3.

[11] Nada Eissa and Jeffrey Liebman, 1996, “Labor Supply Response to the Earned Income Tax Credit,” Quarterly Journal of Economics, 111:2.

[12] V. Joseph Hotz, Charles Mullin and John Karl Scholz, January 2006, “Examining the Effect of the Earned Income Tax Credit on the Labor Market Participation of Families on Welfare,” NBER Working Paper 11968.

[13] Nada Eissa and Hilary Williamson Hoynes, 2004, “Taxes and the Labor Market Participation of Married Couples: the Earned Income Tax Credit,” Journal of Public Economics, 88.

[14] Eissa and Hoynes, op cit.

[15] David Ellwood, December 2000, “The Impact of the Earned Income Tax Credit and Social Policy Reforms on Work, Marriage, and Living Arrangements,” National Tax Journal, 53:4.

[16] Janet Holtzblatt and Robert Rebelein, December 2000, “Measuring the Effect of the EITC on Marriage Penalties and Marriage Bonuses,” National Tax Journal, 53:4.

[17] GAO, December 14, 2001, “Earned Income Tax Credit Eligibility and Participation.”

[18] IRS, August 3, 2003, “Earned Income Tax Credit (EITC) Program Effectiveness and Program Management FY 2002 – FY 2003.”

[19] President’s Advisory Panel, op. cit.

[20] The one exception is moderate-income families with four or more children. This, however, could be easily and inexpensively remedied while simplifying the Tax Panel’s proposal. See Aviva Aron-Dine and Joel Friedman, 2006, “Effects of the Tax Reform Panel’s Proposals on Low-and Moderate-income Households,” Center on Budget and Policy Priorities. This paper also describes some other technical issues and potential improvements to the Tax Panel’s proposal.

[21] In addition, it would be preferable if the dependent exemption for non children were replaced with a $500 tax credit.

[22] In the context of a broader tax reform that raised marginal rates at the top, the phase-out would be neither necessary nor desirable.

[23] Jonathan Gruber and Emanuel Saez, 2000, “The Elasticity of Taxable Income: Evidence and Implications,” NBER Working Paper No. 7512.

More from the Authors