Two High Income Tax Cuts Not Yet Fully in Effect Will Cost Billions Over the Next Five Years Freezing the Tax Cuts at 2007 Levels Would Yield Significant Savings

On January 5, the House of Representatives voted to reinstate the “Pay-As-You-Go” (PAYGO) budgeting rule, and Democratic leaders have promised that the Senate will follow suit. Because PAYGO requires that legislation that increases entitlement spending or reduces revenues be paid for, the rule increases the need to find offsets to pay for high priority legislation and to carefully consider the tradeoffs inherent in any particular entitlement expansion or tax cut.

In this new context, policymakers should give careful consideration to two provisions of the 2001 tax cut that began to take effect in 2006 and will phase in fully over the next few years. These tax cuts gradually eliminate two existing tax provisions that limit the benefits of the personal exemption and itemized deductions for very high-income households (see box on page 3). In 2006 and 2007, the provisions are scaled back by one third; in 2008 and 2009, they will be scaled back by two thirds; and in 2010, they will be repealed altogether.

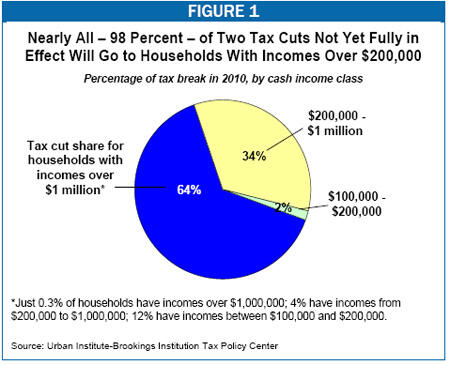

According to the Joint Committee on Taxation, these tax cuts will cost about $30 billion over the next five years (2007-2011). According to the Urban-Brookings Tax Policy Center, when these two tax cuts are fully in effect, almost two-thirds of their benefits will go to households with annual incomes above $1 million; some 98 percent of the tax-cut benefits will go to households with incomes above $200,000 (see Figure 1).

In light of the cost and distribution of the two tax cuts, policymakers should consider rolling them back, in order to pay for higher priority initiatives or to reduce the federal deficit. If members of Congress are reluctant to undo tax cuts households are already receiving, they could nonetheless realize significant savings simply by freezing the two tax cuts at their 2007 levels. The Tax Policy Center estimates that such a policy — which would merely prevent even larger tax cuts for high-income households from taking effect in future years — would save about $13 billion (2007-2011).

As a point of comparison, that amount is about what is needed to fill the shortfall in the State Children’s Health Insurance Program through 2012. (The shortfall is the gap between the funding allocated to the program in the Congressional Budget Office baseline and the funding needed to continue to insure the number of children currently covered by the program.) This means that policymakers could freeze at 2007 levels two tax cuts overwhelmingly benefiting households with incomes above $200,000 and use the savings from keeping the already-generous tax cuts for high-income households from growing even larger to ensure that SCHIP is not forced to cover fewer children in the years ahead.

Vast Majority of Households Would Be Unaffected By Revisiting These Provisions, and High-Income Households Still Would Receive Large Tax Cuts

According to the Tax Policy Center, virtually no households with incomes below $100,000 would be affected by scaling back the two tax cuts (that is, freezing the tax benefits at their 2007 levels instead of allowing them to increase over the next few years). Households with incomes between $100,000 and $200,000 would lose an average of $7 apiece in 2010, while households with incomes between $200,000 and $500,000 would lose an average of $190.

Those most affected by the change would be households with incomes above $1 million, the 0.3 percent of all households who would receive 64 percent of the benefits of the two tax cuts if they took full effect in 2010.

| Table 1: | ||

| Households With Annual Incomes: | If the Two Tax Cuts Take Full Effect: | If the Two Tax Cuts Remain at 2007 Levels: |

| Less than $100,000 | $0 | $0 |

| $100,000 — $200,000 | $11 | $4 |

| $200,000 — $1 million | $650 | $220 |

| Over $1 million | $17,500 | $5,800 |

| Source: Urban-Brookings Tax Policy Center | ||

What Are “Pease” and “PEP”?

The 2001 tax cut gradually eliminates two provisions that were enacted as part of the 1990 deficit-reduction package.

The first provision (sometimes referred to as the “Pease” provision, after former Representative Don Pease) limits the value of itemized deductions for taxpayers with high incomes. The tax code allows taxpayers to reduce their taxable income either by the amount of the standard deduction or by an amount equal to the sum of their itemized deductions. About two-thirds of taxpayers use the standard deduction, and one-third itemize their deductions. High-income taxpayers are much more likely to itemize than are middle-income taxpayers. The Pease provision reduces the value of deductions for those who itemize and have incomes above $156,400 (in 2007; the phaseout thresholds grow each year with inflation).

The second provision is known as the “personal exemption phase-out” (or “PEP” for short). The tax code allows taxpayers to claim a personal exemption ($3,400 in 2007) for each member of their household. They can subtract their personal exemptions from their adjusted gross income before calculating their taxes, thus reducing their tax liability. Under PEP, the personal exemption phases out for those with high incomes; in 2006, the exemption begins phasing out at an income level of $234,600 (for married couples) and $156,400 (for singles).

The complaint most often levied against the Pease and PEP provisions is that they add to the complexity of the tax code. In fact, complying with Pease and PEP involves a few simple calculations. Moreover, to the extent that the provisions do create complexity, they impose it on those households that are typically best able to cope with it: high-income taxpayers who most often have professionals calculate their taxes or use a software package that would automatically handle the Pease and PEP calculations.

If the tax cuts were held at 2007 levels, these households still would receive tax breaks averaging $5,800 from the two measures in 2010 (see Table 1). Moreover, these sizable tax cuts would be piled on top of the far larger tax cuts that households with incomes above $1 million receive from other provisions of the 2001 and 2003 tax cuts. According to the Tax Policy Center, these households will receive average tax reductions of about $140,000 in 2010 from other tax cuts enacted in 2001 and 2003 (as compared with the $158,000 they will receive if these two tax cuts take full effect).

Revisiting These Two Tax Cuts in Light of Budget Realities Is Particularly Appropriate

The two tax cuts in question gradually eliminate the provisions known as the personal exemption phaseout (“PEP”) and the phaseout of itemized deductions (“Pease”) (see box above). These provisions were originally signed into law by the first President Bush in 1990 as part of a bipartisan budget agreement intended to address disturbingly high deficits. (PAYGO budget rules also were first instituted in 1990, as part of the same budget agreement.)

The current President Bush did not propose elimination of the two provisions; this was added to the 2001 tax-cut package on Capitol Hill. To keep the total cost of the 2001 tax-cut package within prescribed budget limits, the two provisions were not eliminated immediately; instead, they were phased out between 2006 and 2010. (Like the other provisions of the 2001 tax cut, the repeal of Pease and PEP is slated to expire at the end of 2010.)

When the Pease and PEP provisions were enacted in 1990, the idea was to raise needed revenue to help reduce the deficit by phasing down deductions and exemptions for those who could most afford to lose them. That rationale is even more valid today, in light of the massive income-tax cuts that households at very high income levels have received in recent years. With budget pressures intensifying, and with pre-tax income inequality again on the rise,[1] it does not make sense to fully phase out the Pease and PEP provisions over the next three years and pile costly new tax cuts for very high-income households on top of the large tax cuts they are already receiving.

End Notes

[1] Arloc Sherman and Aviva Aron-Dine, “New CBO Data Show Income Inequality Continues to Widen: After-Tax Income for Top 1 Percent Rose by $146,000 in 2004,” Center on Budget and Policy Priorities, January 23, 2007.

More from the Authors