The Fiscal and Economic Risks of Territorial Taxation

Many policymakers say they want to reform the U.S. system of taxing multinational corporations so that it better promotes growth and helps reduce budget deficits. Unfortunately, one proposal that has received significant attention would take the tax code in an ill-advised direction, creating serious economic and fiscal risks. The proposal — to create a so-called “territorial” tax system — would create greater tax incentives for multinational corporations to invest and move profits overseas rather than in the United States, which would risk hurting domestic businesses, boosting deficits over the long run, and weakening the economy.

Countries impose international tax systems that range between “worldwide” and “territorial.” In a worldwide system, a country taxes a corporation’s total income, whether the corporation generated it in that country or not (and the country generally gives the corporation a tax credit for the foreign taxes that it has already paid). In a territorial system, a country taxes only the income that the corporation generated in that country, leaving other countries to tax the income generated elsewhere.

The current U.S. tax system, which is often described as worldwide, actually has elements of both systems. That is, the U.S. system taxes U.S.-based multinational corporations on a worldwide basis so that, for instance, General Electric owes U.S. tax on the income it generates at home as well what it generates as in Europe, Asia, and so on. The U.S. system also gives U.S.-based multinationals a credit for the foreign taxes they pay on their foreign income so that multinational aren’t taxed twice on the same income. But, in a major nod toward a territorial system, the United States does not tax foreign profits at all until corporations “repatriate” them — that is, bring them back to the United States. Corporations can keep those profits overseas, deferring U.S. tax indefinitely, as many of them do.

The proposal to move the U.S. system to a territorial one would create several major problems:

First, a territorial system would create greater incentives for U.S.-based multinationals to invest and book profits overseas rather than at home. Under a territorial system, U.S.-based multinationals would face a top tax rate (currently 35 percent before they lower their taxes by using deductions and credits) on their domestic income and a zero or very low tax rate on their foreign income. That would give U.S.-based multinationals a strong incentive to shift their operations from the United States to low-tax countries or so-called “tax havens,” or to artificially shift their profits by using what are known as “earnings stripping” techniques (see the box on p. 13). Moreover, a territorial system would spread its tax benefits unevenly, favoring a relatively small number of U.S.-based multinationals, in such industries as pharmaceuticals and software, that can more easily move their investments and profits overseas. (For more on this issue, see “Creating More Incentives to Invest Overseas, Not at Home,” p. 4.)

Second, by encouraging capital to flow overseas, a territorial system would risk reducing wages at home. If a lower U.S. tax rate on foreign profits encourages capital to move offshore, basic economic theory predicts that the returns to U.S. capital would rise but that the wages of U.S. workers would fall. As Jane Gravelle, a leading tax economist at the Congressional Research Service (CRS), testified before Congress, “[Moving to a territorial system] would make foreign investment more attractive. That would cause investment to flow abroad, and that would reduce the capital which workers in the United States have, so it should reduce wages. A capital flow reduces wages in the United States [and] increases the wages abroad.”[1] (For more on this issue, see “The Risk of Hurting Workers and the Economy,” p. 8.)

Third, a territorial tax system would risk higher budget deficits by draining revenues from the corporate income tax.The more a territorial system encouraged U.S.-based multinationals to shift profits overseas, the less the income of such multinationals would face any U.S. tax. That’s because a territorial system would enable the United States to tax only the income that a U.S.-based multinational generated at home. The Treasury Department estimates that a simplified territorial system — one that lacked rules to mitigate these revenue losses — could cost the federal government roughly $130 billion in lost revenue over ten years.[2] (For more on this issue, see “Effect on Federal Tax Revenues,” p. 10.)

Fourth, a territorial system would risk higher taxes on smaller businesses and domestic businesses.If policymakers sought to offset the lost revenues from a territorial system (and any cut in the U.S. corporate tax rate), they would likely do so by broadening the business tax base. Business base broadening would have to rely on reducing large tax breaks for domestic activity (since overseas activity would be largely or entirely free of U.S. tax), thereby reducing incentives for domestic investment. Thus, even if policymakers cut the top statutory tax rate as they adopted a territorial system, smaller domestic businesses could well face higher taxes. (For more on this issue, see “Pressure to Raise Taxes on Domestic Investment,” p. 14.)

In a sense, a territorial system would amount to a permanent version of the failed “repatriation tax holiday” of 2004; Edward Kleinbard, former chief of staff to Congress’ Joint Committee on Taxation (JCT), called a territorial system “repatriation on steroids.”[3] (See the box on page 7.) During the holiday, U.S.-based multinationals were permitted to bring their overseas profits to the United States and pay just a 5 percent tax rather than the statutory 35 percent rate. (That’s not unlike the low tax that, under a territorial system, U.S.-based multinationals would pay on their overseas profits in low-tax countries.) Supporters of the repatriation holiday claimed that, by attracting funds back to the United States, the holiday would help the U.S. economy by spurring investment and creating jobs.

During the holiday, multinationals did indeed repatriate a huge chunk of their profits. But studies have conclusively demonstrated that despite the corporations’ predictions, the repatriated profits did not boost domestic investment or economic growth. As would likely also occur with a territorial tax system, a handful of firms got the bulk of the tax benefits. And the firms that that took advantage of the holiday mostly used the repatriated earnings not to invest in U.S. jobs or growth but for purposes that Congress had sought to prohibit such as repurchasing their own stock and paying bigger dividends to their shareholders. Many firms actually laid off large numbers of U.S. workers even as they reaped multi-billion-dollar benefits from the tax holiday and passed them on to shareholders.

Moreover, massive profit shifting followed the holiday, previewing what a territorial tax system would encourage on an even larger scale. Before the holiday, the firms that benefited from it had shifted substantial profits overseas largely to avoid U.S. taxes (rather than to take advantage of investment opportunities); IRS data shows that 77 percent of profits repatriated during the holiday came from countries that the Government Accountability Office identified as tax havens.[4] In addition, a 2010 study by Thomas J. Brennan of Northwestern University strongly suggests that firms, anticipating a second holiday, aggressively shifted profits overseas after 2004; Brennan reported that “since the holiday window, there has been a dramatic increase in the rate at which firms add to their stockpile of foreign earnings kept overseas.” A territorial tax system would give multinationals even more incentive to book profits in low tax countries in order to enjoy the permanently low or zero U.S. territorial tax rate on those profits.

U.S.-based multinationals argue that a territorial system would not just deliver tax savings to a few large companies but benefit the economy as a whole. But, at best, a territorial system would increase the return of dividends to the United States only modestly, and (as with the 2004 tax holiday), there is no evidence that those dividends would go for investment or spending that improves U.S. growth. Furthermore, a territorial system is not likely to make it more attractive for multinationals to set up headquarters here: large U.S. multinationals already have lower effective worldwide tax rates than their European counterparts. Finally, multinationals’ claims that, even if a territorial system prompted them to expand offshore, they would also create more jobs in the United States as a consequence don’t withstand scrutiny.[5]

U.S.-based multinationals argue that many countries have territorial systems. The reality is much more complicated. Other countries’ territorial tax systems are much tougher than is often understood and frequently include significant “worldwide” elements, although multinationals nevertheless game them to avoid tax. Many countries that supposedly have territorial systems actually have hybrid systems, under which the countries tax substantial portions of the overseas profits of their multinationals on a worldwide basis. These hybrid elements are commonly coupled with other “tough” elements intended to reduce the ability of multinationals to “game” a pure territorial system by artificially shifting their profits to tax havens and other low-tax countries and therefore avoiding taxation.

In addition, even the “tough” territorial systems have still confronted serious corporate profit shifting and tax avoidance problems, and European nations are now considering steps to address the reality that many multinationals are generating billions of dollars of revenue in Europe while paying no tax there. The Organisation for Economic Co-operation and Development is even calling for its member countries to review the “fundamentals” of their predominantly territorial tax systems. (For more on this issue, see “Confronting the Reality of ‘Leaky’ Territorial Systems in Other Countries,” p. 15.)

In short, a territorial tax system would create unnecessary economic and fiscal risks and move the tax code in an undesirable direction.

A good first step in the right direction would be President Obama’s fiscal year 2013 budget proposals to reform international taxation, which would reduce incentives for corporations to shift profits and investments overseas and raise more than $168 billion over ten years[6] . A key provision would prevent companies from deducting their interest expenses associated with loans that support overseas investments as long as they are deferring U.S. tax on the income they derive from those investments.

A further step in the right direction is the proposal in the President’s “Framework for Business Tax Reform” for a minimum tax on foreign profits,[7] which would reduce the incentive for multinationals to stockpile foreign profits offshore and — unlike a territorial system — discourage firms from shifting investments overseas in the first place. Policymakers should also consider options for restricting the ability of multinational companies to defer U.S. tax on overseas profits.[8]

Creating More Incentives to Invest Overseas, Not at Home

The current U.S. system of taxing corporate income provides significant incentives for U.S.-based multinationals to invest overseas rather than at home. Because (under what is known as “deferral”) multinationals don’t pay U.S. tax on their overseas profits until they bring them to the United States, multinationals often keep those profits overseas indefinitely. That will cost the federal government roughly $42 billion in lost revenue in 2013, according to the Treasury Department.[9]

This and other features of the corporate tax code enable many U.S.-based multinationals to pay much lower taxes on their overseas profits than on their domestic profits. Large corporations (those with assets over $10 million) paid an average combined tax (U.S. and foreign) on their foreign income of 15.7 percent in 2007 — well below the 26 percent average rate on their domestic income.[10]

Looking ahead, a key test of any corporate tax reform effort should be whether it reduces the tax code’s bias toward overseas investments.[11] A territorial tax system, however, would make that bias worse.

A very low or zero U.S. tax rate on foreign profits — as a territorial system would provide (see Table 1) — would give U.S.-based multinationals more incentive to book their profits in tax havens and low-tax countries.[12] Companies could use accounting techniques to shift some of the profits that they generate from their U.S. operations to other nations in which they have operations, reducing their total tax burdens and draining U.S. tax revenues (as discussed below).

| Table 1 Statutory Tax Rates Under Simplified Territorial and Worldwide Tax Regimes (assuming no corporate rate changes) | |||

| Territorial | Current | Worldwide | |

| U.S. profits | 35% in year earned | 35% in year earned | 35% in year earned |

| Foreign profits | 0% (or very low rate when repatriated) | 35% but only when repatriated | 35% in year earned |

Separate and apart from such profit-shifting, a territorial system also would create an incentive for U.S.-based multinationals to invest more of their capital offshore. That’s because the profits would face little or no U.S. taxes and, in many places, a relatively low tax rate in a foreign country — reducing the after-tax cost of a corporation’s offshore production. As Preston Padden, the former executive vice president of government relations at the Walt Disney Company, put it:

A territorial tax system would essentially codify the deferral regime and enhance its benefits by allowing earnings to be repatriated to the U.S. tax-free. So why on earth would Washington, D.C., adopt a system that continues to reward companies that shift operations and jobs offshore and continues to penalize companies that maintain their U.S. operations and workers? . . . Clearly the U.S. tax system should encourage companies to retain their valuable stock of highly mobile intellectual property, including high-tech property, drug patents and films, in the United States. Moving to a territorial system would have the opposite effect.

Maintaining the U.S. worldwide tax system and enacting stricter anti-deferral rules would stop rewarding companies such as GE for moving jobs overseas and stop penalizing companies like Disney that keep their income-producing property and their jobs here. [13]

Box 1: Why a Territorial Tax System Has Been Called “Repatriation on Steroids”

A territorial tax system amounts to a “repatriation holiday on steroids . . . a sort of a permanent repatriation holiday,”a according to Edward Kleinbard, former chief of staff of the Congressional Joint Committee on Taxation who is now a law professor at the University of Southern California.

The 2004 “repatriation tax holiday” temporarily allowed multinational corporations to pay a statutory tax rate of 5.25 percent on the overseas profits they brought back to the United States. As a result, multinational corporations avoided paying significant U.S. corporate income tax on foreign earnings that they had accumulated overseas.

The holiday was supposed to boost domestic investment and jobs. Instead:

- The holiday did not produce the promised economic benefits. Firms mostly did not use the repatriated earnings to invest in U.S. jobs or growth but for purposes that Congress had sought to prohibit such as repurchasing their own stock and paying bigger dividends to their shareholders. Many firms actually laid off large numbers of U.S. workers even as they reaped multi-billion-dollar benefits from the tax holiday and passed them on to shareholders.b

- Most of the benefits of the holiday went to a small number of very large corporations in a few industries, particularly those that had aggressively shifted their income overseas.Just 15 companies were responsible for more than 50 percent ($160 billion) of the total repatriations under the discounted repatriation tax rate in 2005: Pfizer, Merck, Hewlett-Packard, Johnson & Johnson, IBM, Schering-Plough, DuPont, Bristol-Myers Squibb, Eli Lilly, PepsiCo, Procter & Gamble, Intel, Coca-Cola, Altria, and Oracle.c Half of all repatriations came from companies in the technology and pharmaceutical industries, which have been particularly aggressive in shifting income abroad because they rely on intellectual property, which is relatively easy to shift to other countries as a tax avoidance strategy. A stunning 77 percent of repatriations came from tax-haven countries.d

Like a repatriation tax holiday, a territorial tax system would enable companies to pay little (or no) U.S. tax on their foreign profits — but on a permanent basis. Also like a repatriation holiday, the tax benefits would likely be concentrated among a small group of large multinationals that can aggressively shift profits and investment offshore.e

a Center on Budget and Policy Priorities, “Kleinbard on the Flawed Case for a Corporate ‘Repatriation’ Tax Holiday,” Off the Charts blog, October 17, 2011, http://www.offthechartsblog.org/kleinbard-on-the-flawed-case-for-a-corporate-%E2%80%9Crepatriation%E2%80%9D-tax-holiday/.

b Chuck Marr and Brian Highsmith, “Tax Holiday for Overseas Corporate Profits Would Increase Deficits, Fail to Boost the Economy, and Ultimately Shift More Investment and Jobs Overseas,” Center on Budget and Policy Priorities, revised June 23, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3441 and Chuck Marr, Brian Highsmith, and Chye-Ching Huang, “Repatriation Tax Holiday Would Increase Deficits and Push Investment Overseas: Proponents Are Distorting Joint Tax Committee Analysis,” Center on Budget and Policy Priorities, revised October 11, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3593.

c United States Senate Permanent Subcommittee on Investigations, Committee on Homeland Security and Governmental Affairs, “Repatriating Offshore Funds,” Majority Staff Report, p.8 http://levin.senate.gov/download/repatriating-offshore-funds.

d Melissa Redmiles, “The One-Time Received Dividend Deduction,” IRS Statistics of Income Bulletin, Spring 2008, http://www.irs.gov/pub/irs-soi/08codivdeductbul.pdf and Government Accounting Office, “International Taxation: Large Corporations and Federal Contractors With Subsidiaries in Jurisdictions Listed as Tax Havens or Financial Privacy Jurisdictions,” Report GAO-09-157, December 2008, http://www.gao.gov/new.items/d09157.pdf.

e See also Citizens for Tax Justice, “Fortune 500 Corporations Holding $1.6 Trillion in Profits Offshore,” Citizens for Tax Justice, December 13, 2012. CTJ finds that of the 290 Fortune 500 companies for which information was available, 20 held half of the $794 billion in profits held offshore at the end of 2011. These companies (9 of which were in the top 15 repatriating companies under the 2004 tax holiday) with large accumulated foreign profits would likely be among the biggest beneficiaries of a territorial tax system.

The Risk of Hurting Workers and the Economy

Basic economic theory suggests that a territorial tax system would reduce the domestic capital stock, and so reduce U.S. workers’ productivity and real wages.

Along with CRS’ Jane Gravelle (cited above), other tax experts have advised that greater incentives for foreign investment would tend to depress wages at home. For instance, University of Michigan economist Joel Slemrod, widely regarded as one of the nation’s leading tax policy experts, has written, “[F]or a U.S. multinational company a territorial tax system improves the relative attractiveness of investing in (low-tax) foreign countries investment relative to a U.S. investment, and so the net effect on the incentive to invest and hire workers domestically might be negative.”[14]

If a territorial system were to attract capital away from the United States, the returns to the owners of the remaining U.S. capital would likely rise relative to what they would have been because domestic capital would be scarcer.[15] There is no sound evidence, however, that a territorial system would benefit workers or boost U.S. economic growth.

U.S. multinationals argue that the current U.S. tax system encourages them to stockpile their profits overseas to defer U.S. tax and that a territorial system would encourage them to repatriate those profits (i.e., bring them to the United States). But policymakers could eliminate the incentive to stockpile profits offshore by moving in the oppositedirection: toward a worldwide tax system in which firms’ overseas earnings face the U.S. tax in the year they are earned, without a corporate option for deferral.[16] (As under the current tax system, companies would continue to get a tax credit for the taxes they paid overseas on the same income.) Further, recent studies suggest that a territorial tax system would likely increase permanent repatriations only modestly.[17] In addition, as Gravelle notes, “even if repatriations increase under a permanent territorial tax, those repatriations may not result in additional investment, but are likely to be paid out as dividends, or substitute for borrowing by the parent company.”[18]

U.S. multinationals also argue that a territorial tax system would improve U.S. competitiveness.[19] But their definition of “improve competiveness” often primarily means improving the returns to their shareholders, which does not necessarily strengthen overall U.S. job creation or economic growth.

Some proponents of a territorial system say that it would encourage more companies to incorporate (and set up headquarters) in the United States by cutting the effective worldwide tax rate of U.S.-incorporated companies. That, they say, would benefit the U.S. economy and increase the number of high-quality headquarters jobs in the United States. But, a recent study shows that the average effective worldwide tax rate of the 100 largest U.S.-based multinationals is already below that of the 100 largest European Union-based multinationals.[20] Moreover, there is no evidence that the current U.S. tax system is either persuading significant numbers of U.S. firms to change nationalities (to “invert”) to take advantage of other countries’ territorial tax systems[21] or discouraging firms from incorporating in the United States. Nor is there evidence that territorial taxation would encourage more firms to incorporate in the United States.

Some proponents also argue that even if a territorial system encourages U.S.-based multinationals to expand their offshore operations, that expansion creates jobs in the United States as well. But, Gravelle cautions that this argument rests on a shaky foundation.[22] For example, proponents often cite the finding of a prominent study by Professors Desai, Foley, and Hines that U.S. multinationals’ investment abroad correlates with more investment by those multinationals in the United States. [23] Gravelle notes, however, that this is only a correlation and that the study does not show that overseas investment by multinationals causes them to expand their domestic investment. As Gravelle explains, a rise in foreign demand could have caused both U.S. and foreign investment to grow at the same time.[24] Furthermore, as the Desai, Foley, and Hines study notes, other studies have found that increased investment by multinationals offshore is associated with less investment in the United States.

In considering the complex issue of international taxation, policymakers should recognize that the interests of U.S.-based multinationals may differ from those of U.S.-based domestic businesses, which in turn may differ from those of U.S. workers. Policymakers should remember as well that the real wages of production workers have stagnated in recent decades due to a confluence of global and domestic factors.[25]

Effect on Federal Tax Revenues

A territorial tax system would likely increase the budget deficit in two ways:

- U.S.-based multinationals would pay little or no tax on their foreign profits.

- A territorial tax system would encourage such firms to shift profits overseas that they would otherwise report in the United States and pay U.S. tax on, either by actually moving investments offshore or by changing on paper where they report the profits.

Policymakers would be hard-pressed to stanch such a revenue loss. They would find it virtually impossible to prevent multinationals from shifting their real investments to take advantage of a territorial system, and they would find it extremely difficult to prevent multinationals shifting their profits on paper (see Box 2 on page 13). Many multinationals already shift where they report profits from the United States to low-tax and tax haven countries to delay paying taxes under the current tax code, according to an abundance of evidence, a practice that a territorial system would make still more lucrative.[26]

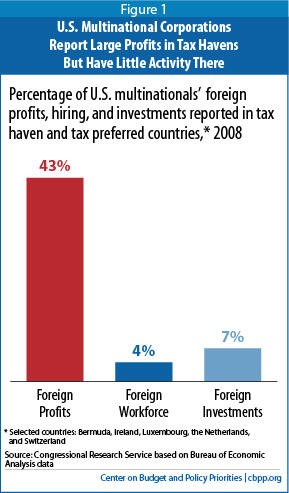

For example, a new CRS analysis finds (as Figure 1 shows):

…American companies reported earning 43% of overseas profits in [tax preferred or tax haven countries of] Bermuda, Ireland, Luxembourg, the Netherlands, and Switzerland in 2008, while hiring 4% of their foreign workforce and making 7% of their foreign investments in those economies. In comparison, the traditional economies of Australia, Canada, Germany, Mexico and the United Kingdom accounted for 14% of American MNCs [multinational corporations’] overseas’ profits, but 40% of foreign hired labor and 34% of foreign investment. This report also shows that the discrepancy between where profits are reported and where hiring and investment occurs, as examples of business activity, has increased over time.[27]

A territorial regime would magnify the incentive to shift profits overseas to low-tax jurisdictions because doing so would not just delay U.S. corporate taxpaying but enable corporations to largely avoid it altogether. Tax Policy Center (TPC) Co-Director Eric Toder notes that “cuts in the residual [U.S.] tax rate on foreign-source-income [encourage] U.S.-based companies to report a larger share of their profits to foreign jurisdictions, including tax havens.”[28] A territorial tax system would permanently cut that residual US tax rate to zero or a very low rate.

In theory, policymakers could design a territorial system that collected more revenue than the current system. To do so, however, they likely would have to scale back the types of income that are eligible for deferral and deny territorial taxation to those types of income. For example, such a system could end deferral for certain types of income derived from intellectual property or income reported in countries with (or by companies otherwise subject to) extremely low rates of foreign tax. Thus, a “tough” territorial system would tax many types of income at the full U.S. corporate tax rate when the income is earned rather than when it is repatriated. In the end, a tough territorial system would operate like a worldwide system for much foreign income and rely heavily on elements of a worldwide system to raise revenue.

Even then, any increase in tax revenues under a territorial system would likely be “crucially dependent” on prohibiting U.S. companies from taking deductions for activities related to foreign investment.[29] For example, while a territorial system without any such “expense allocation rules” would cost about $130 billion over ten years compared to current tax policy, a territorial system that denies deductions for overhead expenses allocated to foreign income would raise about $76 billion over ten years.[30] (That means that simply denying immediate deductions for overhead expenses related to foreign income — such deductions are currently allowed even if a corporation defers tax on that income — without moving to a territorial tax system would raise significantly more than $76 billion over ten years.)

Similarly, a territorial tax system that denied deductions for interest expenses related to foreign income that’s subject to the territorial exemption from U.S. taxation would likely lose revenues compared to the President’s proposal to prohibit such immediate deductions whilecontinuingto tax foreign profits (albeit on a deferred basis).[31]

The fiscal costs of proposals to create a territorial tax system are easy to overlook, for two reasons. First, proposals to transition to a territorial system often include a one-time tax on foreign profits that companies are now holding offshore (companies may be allowed to pay the tax over a number of years).[32] This initial, temporary revenue bump means that a territorial tax system may increase deficits by much less or even reduce them over the first ten years than over a longer period, when the revenue from this one-time tax increase has faded. Put another way, this one-time tax can mask the longer-term revenue-losing effects of the proposal, producing the same effect as a timing gimmick. Second, policymakers may bundle a territorial tax system with other corporate tax reforms that help to offset its cost. But such reforms would almost inevitably mean raising taxes on domestic firms’ profits in order to pay for the rate cut on multinationals’ foreign profits, as explained below.

Box 2: The Difficulty of Preventing Profit Shifting Under a Territorial Regime

Under a territorial system, profits booked in offshore tax havens or low-tax countries would face little or no U.S. tax and very low rates of foreign tax. This would give multinationals a strong incentive to artificially shift their profits into low-tax jurisdictions using two common “earnings strippings” techniques:a

“Transfer pricing.” A U.S. multinational company could transfer — at as low a price as possible — intellectual property (a patent, for example) to a subsidiary in a low-tax jurisdiction such as Ireland. It would then pay the Irish subsidiary royalties — set as high as possible — for the rights to use the intellectual property worldwide. The Irish subsidiary would book large profits on the royalty payments, and those profits generally would not be subject to U.S. tax under a territorial system. (The U.S. company may also be able to deduct the inflated royalty payments, thereby reducing the amount of its U.S. profits subject to the U.S. corporate tax.)

Transfer pricing can be particularly effective for intangible property because it is very difficult for tax authorities to value intellectual property and hence to challenge the “transfer price” that members of a multinational group pay for the intra-group transfer or use of their property. This seems to be why companies in the technology and pharmaceutical industries have been particularly aggressive at avoiding or minimizing U.S.-tax by shifting income abroad.

“Thin capitalization.” In a related strategy, the U.S.-based parts of a multinational corporation hold as much of the corporation’s debt as possible, becoming highly leveraged. Lightly leveraged subsidiaries in low-tax and tax-haven jurisdictions may receive interest payments on loans to the U.S. parent; those interest payments would boost their profits. (U.S. companies in a multinational corporate group might also be able to deduct their interest payments on that debt, reducing their U.S.-reported profits and taxes.)

The University of Michigan’s Joel Slemrod has warned that trying to prevent earnings stripping in a territorial tax system would require even more complex and onerous rules than under the current hybrid system:b

[A]s long as the U.S. has a high statutory corporate rate relative compared to [sic] many other countries (including tax havens), moving to a territorial system will greatly increase the incentive for outward taxable income shifting. While under a worldwide system shifting taxable income from the U.S. to a low-tax country in principle only postpones the residual U.S. tax liability until repatriation, under a territorial system it would be lost forever. Defending our revenue base, which is a component of prosperity, would require vigilant enforcement and more onerous rules than now in place.

Similarly, Edward Kleinbard, former chief of staff to Congress’ Joint Committee on Taxation, notes that it is “unrealistic to expect that enhanced administration can ever adequately address the transfer pricing challenge that modern, tightly integrated multinational enterprises with high-value intangible assets would pose to a territorial tax system.”c He concludes that all territorial tax systems create the prospect of “stateless income” that is taxed nowhere in the world or at very low rates in countries where it was not earned.

A recent territorial tax proposal from the House Ways and Means Committee majority staff sets out three alternative measures to prevent earnings stripping. But Harvard Law Professor Stephen Shay, an expert on international taxation and former Treasury official, dismisses them, saying, “Those of us who have been doing this business for 30 years on the legal side” would find ways to avoid such a tax, and that, “When [lawmakers] don't fully understand that and the companies come in and say it won't happen, I'm here to tell you it will happen.”d

a Edward D. Kleinbard, “The Lessons of Stateless Income,” Tax Law Review, Vol. 65 (2012), pp. 99-172, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1791783##.

b Joel Slemrod, “Competitive Tax Policy,” American Enterprise Institute, September 23, 2011, http://www.aei.org/files/2011/09/29/Slemrod%20-%20AEI%20Competitiveness%20092311%20submitted.pdf.

c Kleinbard “Throw Territorial Taxation From the Train,” Tax Notes, Feb 5, 2007 at 555 , http://faculty.law.wayne.edu/tad/Documents/Research/Kleinbard%20Territoriality%20article.pdf.

d See David Van Den Berg, "Territorial Tax Systems Can Be Beaten, Shay Says," 223 Tax Notes 7, Nov. 16, 2012. Also see Steven Shay, “Unpacking Territorial”, New York University School of Law, 2012, http://www.law.nyu.edu/ecm_dlv2/groups/public/@nyu_law_website__academics__colloquia__tax_policy/documents/documents/ecm_pro_072076.pdf.

Pressure to Raise Taxes on Domestic Investment

Proponents of a territorial tax system often propose it along with a lower domestic corporate tax rate that, they claim, would reduce the incentive for U.S.-based multinationals to shift their profits and investments offshore and take advantage of the new zero or low territorial tax rate on foreign profits.[33] Cutting the corporate tax rate would be costly, however.[34] To prevent corporate tax reform from boosting deficits, policymakers would have to offset both the large reduction in tax rates on foreign profits and the smaller reduction in tax rates on U.S. profits by substantially broadening the business tax base — that is, by substantially scaling back or ending corporate and business tax breaks. The existing business tax breaks — outside of deferral — mainly benefit domestic income. So, in this scenario, policymakers would be raising taxes on domestic investments to pay for cutting taxes on foreign profits, giving foreign income an even larger tax advantage over domestic income.

As Toder, the TPC’s Co-Director, has explained:

A revenue neutral combination of lower corporate tax rates, a broader tax base, and a territorial system… would reduce the incentive to invest in the Untied States, compared with current law….Although some variants to territorial systems could raise money, a territorial system, without other reforms, will lose revenue, both by eliminating the existing residual tax on foreign source [income] and encouraging more corporate income, both real and reported, to shift overseas. So if the entire proposal is to be revenue neutral, the combination of a lower rate and broader domestic tax base must raise revenue. Put another way, the cut in taxes on foreign source income, in a revenue neutral proposal, must necessarily lead to an increase in the taxation of investment based in the United States.[35]

In 2012, the largest business tax expenditure was accelerated depreciation for machinery and equipment, which businesses claim mainly for assets that they use in domestic production.[36] After deferral, which is the second largest tax expenditure, the third and fourth largest are the domestic production activities deduction and the tax credit for research and experimentation,[37] both of which are available only for U.S. activity and investment. (Both corporate and non-corporate businesses, such as partnerships, can claim many of these business tax breaks, but only corporations would benefit from a territorial tax system or from a cut to the domestic corporate tax rate.)

If policymakers ended or sharply curtailed such business tax breaks — even if they coupled such action with a lower domestic U.S. corporate tax rate — the combination of changes would raise the average effective U.S. tax rate on domestic profits. Alternatively, policymakers could finance a territorial tax system by boosting deficits, raising individual taxes, cutting domestic investments in priorities such as infrastructure, or cutting social insurance programs like Medicare and Social Security.

Confronting the Reality of “Leaky” Territorial Systems in Other Countries

Some U.S. corporations argue that they are at a competitive disadvantage because other developed countries have territorial tax regimes and the United States does not. In reality, few countries have the sort of free-rein territorial system that those multinationals often promote; Kleinbard, the former JCT chief of staff, terms their description of overseas tax systems a “cartoon version of the territorial tax policies followed by other nations.”[38] Other nations attempt to prevent companies from shifting income to foreign tax havens to evade domestic taxes. Thus, countries with territorial tax systems typically include “tough” elements to prevent unfettered profit-shifting.[39]

Many countries with territorial systems tax large amounts of the foreign profits of their multinational companies on a current, worldwide basis through “controlled foreign company” (CFC) rules — which target profits that will likely face little or no tax in the source country. Countries may impose their own corporate tax rate on, for instance, “passive” profits (from investments in things like stocks and bonds) that firms can easily shift overseas, profits from countries with low statutory or effective tax rates, and profits that were taxed very lightly in the source country. This means that while the tax systems of other countries are often labeled “territorial,” they are in fact hybrid systems with significant worldwide elements. In fact, as the Congressional Budget Office observed of other countries’ territorial tax systems, “Strong anti-abuse rules can result in systems that effectively tax foreign income in a way that is much closer to a worldwide approach.”[40]

For example, Japan’s new corporate tax system is often described as “territorial.” If, however, a foreign subsidiary of a Japanese multinational faces an effective tax rate on its foreign profits of less than 20 percent or has its headquarters office in a jurisdiction with no income tax, the subsidiary’s income is not eligible for territorial tax treatment and is immediately subject to Japan’s domestic corporate tax rate.

The U.S. tax system has CFC rules as well, which deny the tax benefit of deferral to certain “passive” profits. The University of Michigan Law School’s Reuven Avi-Yonah notes, however, that U.S. CFC rules are weaker than those of major European Union (EU) countries with territorial taxation (United Kingdom, Germany, Italy, France), because those countries:[41]

…take into account the effective tax rate in the source country in deciding whether to tax income from a CFC, and . . . take into account whether the CFC has a real presence in the source country. Under the EU rules, for example, a bank earning interest income in a tax haven is likely to be subject to current tax because the effective tax rate in the haven is low and the bank does not have a real presence in the haven. Under [the U.S. rules] the income will likely qualify for [deferral].

Territorial countries often couple stricter CFC rules with tougher rules to prevent multinationals from using transfer pricing and leverage strategies to shift their profits to tax havens. For example, German parent companies of multinational groups may not take interest deductions in Germany that exceed 30 percent of their earnings.

Finally, to prevent large revenue losses, some territorial countries — such as Japan, France, Germany, and Italy — simply tax at the domestic corporate rate a set percentage (often 5 percent) of dividends that corporations pay out of foreign profits that would otherwise be exempt from domestic taxation.

Generally, U.S.-based multinationals that lobby for a territorial system do not acknowledge the problems that territorial regimes can cause. Territorial countries have found that even “tough” provisions do not prevent substantial profit-shifting. Multinationals even sometimes exploit the differences between countries’ rules on determining where they locate profits to make some of their profits completely “stateless” — that is, not subject to tax in any country. [42] In recent weeks, political leaders in countries including the UK, France, Germany, and Italy have been “cracking down on U.S.-based multinational companies such as Google, Apple, Facebook and Amazon, claiming they pay paying little or no tax in Europe in spite of generating billions in revenue there.”[43] British Prime Minister David Cameron has promised to use his country’s year-long presidency of the G8 group of large economies (which includes the United States) to target tax avoidance and prevent international firms from avoiding tax.[44]

Apparently in part due to these problems, the EU is considering strengthening member states’ territorial tax systems by adopting “formulary apportionment,”[45] which would create a single set of rules for the EU that companies would use to determine where to report their income. These rules would ensure that all corporate income would be sourced to some country. Under formulary apportionment, a multinational corporation that is operating in multiple EU countries would apportion where it books its profits (or losses) among those countries based on a formula that takes into account where it locates its assets, labor force, and sales — factors of production that are harder to artificially shift through accounting maneuvers than things like intellectual property or financing expenses. Each country could then tax its share of the profits at its corporate tax rate. This method would ensure that 100 percent of the profits earned in Europe by a multinational corporation that’s operating in the EU would be counted.

That kind of approach for confronting the problems of “leaky” territorial taxation regimes is possible only when a country can coordinate its rules for determining the source of corporate income with its major trading partners. Even then, corporations can find ways to “game” formulary apportionment. For example, a software company might buy a supermarket chain with many employees in a tax haven company so that it can apportion more of its software business profits to that low-tax jurisdiction.[46]

In fact, any rules for sourcing corporate income, no matter how “tough” or coordinated internationally, may be inherently defective. In a global economy where production occurs across countries, apportioning the profits of a global corporation among individual countries will inevitably be somewhat arbitrary, making it harder for lawmakers to get the source rules right and easier for companies to manipulate them. Worldwide tax systems avoid this problem by focusing instead on where a company resides (based either on its place of incorporation or where management makes its decisions), which is usually much more clear cut than determining the geographic source of income.[47]

A strikingly direct November 2012 release from the Organisation for Economic Co-operation and Development (OECD) highlights these problems and presses developed countries to fundamentally rethink their (predominantly territorial) tax rules. In its release, the OECD questions whether the “rules developed in the past are still fit the purpose [sic] in today’s business environment.” It notes that current international tax rules and their underlying policy assumed that “one country would forgo taxation because another country would be imposing tax,” but “in the modern global economy, this assumption is not always correct, as planning opportunities may result in profits ending up untaxed anywhere.” The OECD suggests that to address base erosion and profit shifting by corporations, “a reflection on the very fundamentals of the current rules also appears to be warranted.”[48]

A Better Direction

A territorial tax system would provide tax cuts to large U.S.-based multinational corporations, particularly those that can most aggressively move their profits and investments offshore. The current U.S. tax code already favors foreign over domestic investment, and a territorial system would create still more incentives for large multinationals to move operations and profits overseas. Among the risks, real U.S. wages could fall, federal budget deficits could rise, and tax burdens on domestic companies could increase. Meanwhile, the economic benefits that proponents of a territorial system promise would not likely materialize.

The failed dividend repatriation tax holiday of 2004 and the “leaky” territorial systems of other countries highlight the risks of territorial taxation. The tax holiday did not boost investment or economic growth, but it did put a large tax break mostly in the hands of a few large multinational corporations and rewarded and encouraged aggressive profit shifting offshore. Developed countries in Europe and elsewhere are finding that multinationals can game even “tough” territorial tax systems, and they are starting to look to more far-reaching measures, including coordinated international tax laws, or, as the OECD urges, even a rethinking of the fundamentals of their current predominantly territorial tax rules.

U.S. policymakers should move in a different direction: toward revenue-raising international corporate tax reform that helps level the playing field between domestic and foreign investment. A good place to start is President Obama’s fiscal year 2013 budget proposals to reform international taxation, which would raise more than $168 billion over ten years[49] and reduce incentives for corporations to shift profits and investments overseas. Another good place to look is the proposal in the President’s “Framework for Business Tax Reform” for a minimum tax on foreign profits,[50] which would reduce the incentive for multinationals to stockpile foreign profits offshore and discourage firms from shifting investments overseas in the first place. Policymakers should also consider options to further restrict the tax-reduction strategy known as deferral.[51]

End Notes

[1] Statement of Jane G. Gravelle, Senior Specialist in Economic Policy, Congressional Research Service, before the House Ways and Means Committee, May 12, 2011, http://waysandmeans.house.gov/UploadedFiles/Gravelle.pdf. See also Jane G. Gravelle, “Does the Concept of Competition Have Meaning in Formulating Corporate Tax Policy?” Congressional Research Service, November 2011 http://www.americantaxpolicyinstitute.org/pdf/Jane%20Gravelle%20paper.pdf.

[2] The President’s Economic Recovery Board, “The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation,” August 2010, http://www.treasury.gov/resource-center/tax-policy/Documents/PERAB-Tax-Reform-Report-8-2010.pdf. The Treasury presumably estimated this assuming a 35 percent top corporate rate; see and Stephen Shay, “Unpacking Territorial,” New York University School of Law, Colloquium on Tax Policy and Public Finance, Spring 2012, footnote 100, http://www.law.nyu.edu/ecm_dlv2/groups/public/@nyu_law_website__academics__colloquia__tax_policy/documents/documents/ecm_pro_072076.pdf.

[3] Center on Budget and Policy Priorities, “Kleinbard on the Flawed Case for a Corporate ‘Repatriation’ Tax Holiday,” Off the Charts blog, October 17, 2011, http://www.offthechartsblog.org/kleinbard-on-the-flawed-case-for-a-corporate-%E2%80%9Crepatriation%E2%80%9D-tax-holiday/.

[4] List of tax haven countries comes from Government Accountability Office, “International Taxation: Large U.S. Corporations and Federal Contractors with Subsidiaries in Jurisdictions Listed as Tax Havens or Financial Privacy Jurisdictions,” GAO-09-157, December 2008, http://www.gao.gov/new.items/d09157.pdf. Data on source of repatriated dividends are from Melissa Redmiles, “The One-Time Dividends-Received Deduction,” Internal Revenue Service Statistics of Income Bulletin, Spring 2008, http://www.irs.ustreas.gov/pub/irs-soi/08codivdeductbul.pdf.

[5] Jane G. Gravelle, “Moving to a Territorial Income Tax: Options and Challenges,” Congressional Research Service, July 25, 2012, pp. 13-16, http://www.fas.org/sgp/crs/misc/R42624.pdf.

[6] Joint Committee on Taxation, “Estimated Budget Effects Of The Revenue Provisions Contained in the President’s Fiscal Year 2013 Budget Proposal,” March 12, 2012, https://www.jct.gov/publications.html?func=startdown&id=4413.

[7] U.S. Department of the Treasury and the White House, “The President’s Framework for Business Tax Reform,” February 2012, http://www.treasury.gov/resource-center/tax-policy/Documents/The-Presidents-Framework-for-Business-Tax-Reform-02-22-2012.pdf.

[8] See pp. 38-41 in Jane G. Gravelle, “Moving to a Territorial Income Tax: Options and Challenges,” Congressional Research Service, July 25, 2012, http://www.fas.org/sgp/crs/misc/R42624.pdf.

[9] Office of Management and Budget, Table 17-2, 2012, http://www.whitehouse.gov/omb/budget/Supplemental.

[10] Melissa Costa and Jennifer G. Gravelle, “Taxing Multinational Corporations: Average Tax Rates” forthcoming in Tax Law Review, http://www.americantaxpolicyinstitute.org/pdf/Costa-Gravelle%20paper.pdf. As the Tax Policy Center notes, “[Deferral] and other incentives also encourage firms to locate physical assets, production, and jobs in [foreign] countries.” Tax Policy Center, “International Taxation: What are the Consequences of the US International Tax System?” The Tax Policy Briefing Book: A Citizens’ Guide for the Election, and Beyond, revised October 17, 2007, http://www.taxpolicycenter.org/briefing-book/key-elements/international/consequences.cfm. Multinational corporations often can shift reported profits to low-tax countries through complex transactions (typically involving the transfer of intangible property or the strategic location of expenses) that reduce the effective tax rates on these investments.

[11] Chuck Marr and Brian Highsmith, “Six Tests for Corporate Tax Reform,” Center on Budget and Policy Priorities, updated February 24, 2012, https://www.cbpp.org/cms/index.cfm?fa=view&id=3411.

[12] As discussed below, even if the U.S. top statutory tax rate on domestic profits fell significantly below 35 percent at the same time, the effect still would likely be an increase in the tax burdens of domestic businesses or an increase in budget deficits.

[13] Preston Padden, “Padden: Tax Code Hurts Firms That Keep Jobs in US,” Roll Call, September 6, 2011, http://www.rollcall.com/issues/57_23/tax_code_hurts_firms_that_keep_jobs_in_united_states-208463-1.html.

[14] Joel Slemrod, “Competitive Tax Policy,” American Enterprise Institute, September 23, 2011, p.26. http://www.aei.org/files/2011/09/29/Slemrod%20-%20AEI%20Competitiveness%20092311%20submitted.pdf.

[15] Toder notes that any such capital outflow may be offset in part by foreign capital investing in the US. “International Taxation and Competitiveness,” Conference Sponsored by the American Tax Policy Institute, http://www.americantaxpolicyinstitute.org/pdf/InternationalTaxationandCompetitivenessrev080911.pdf.

[16] Under a pure territorial system, no U.S. corporate tax would ever be paid on foreign profits qualifying for territorial treatment. In a worldwide system, U.S. corporate tax on foreign profits would be paid in the year in which the profits are earned, irrespective of when they are repatriated to the U.S.

[17] Jane G. Gravelle, “Moving to a Territorial Income Tax: Options and Challenges,” Congressional Research Service, July 25, 2012, pp. 13-16, http://www.fas.org/sgp/crs/misc/R42624.pdf.

[18] Ibid. pp. 15-16

[19] “International Taxation and Competitiveness,” Conference Sponsored by the American Tax Policy Institute, http://www.americantaxpolicyinstitute.org/pdf/InternationalTaxationandCompetitivenessrev080911.pdf.

[20] Reuven S. Avi-Yonah and Yaron Lahav “The Effective Tax Rate of the Largest U.S. and E.U. Multinationals,” University of Michigan Law and Economics, Empicial Legal Studies Center Paper No. 11-015, October 25, 2011 http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1949226.

[21] See Eric Allen and Susan Cleary Morse ATPI “Firm Incorporation Outside the U.S.: No Exodus Yet,” Hastings College of Law, May 28, 2012, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1950760.

[22] Jane G. Gravelle, “Does the Concept of Competitiveness Have Meaning in Formulating Corporate Tax Policy?” Congressional Research Service, November 2011, at p. 24, http://www.americantaxpolicyinstitute.org/pdf/Jane%20Gravelle%20paper.pdf.

[23] Mihir A. Desai, C. Fritz Foley, and James R. Hines, “Domestic Effects of the Foreign Activities of U.S. Multinationals,” American Economic Journal: Economic Policy Vo. 1 no. 1, Feb. 2009, pp. 181-203.

[24] Jane G. Gravelle, “Does the Concept of Competitiveness Have Meaning in Formulating Corporate Tax Policy?” Congressional Research Service, November 2011, at p. 25, http://www.americantaxpolicyinstitute.org/pdf/Jane%20Gravelle%20paper.pdf.

[25] Current Employment Statistics Survey, “Table B-8: Average Weekly Earnings of Production and Nonsupervisory Employees,” 2010, http://www.bls.gov/webapps/legacy/cesbtab8.htm.

[26] See, for example, testimony of Martin A. Sullivan before the House Committee on Ways and Means, July 22, 2010, http://waysandmeans.house.gov/media/pdf/111/2010jul22_sullivan_testimony.pdf. Also see ,“Repatriation Tax Holiday Would Increase Deficits and Push Investment Overseas: Proponents Are Distorting Joint Tax Committee Analysis,” Center on Budget and Policy Priorities, revised October 11, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3593.

[27] Mark P. Keightley, “An Analysis of Where American Companies Report Profits: Indications of Profit Shifting,” Congressional Research Service, January 18, 2013.

[28] “International Taxation and Competitiveness,” Conference Sponsored by the American Tax Policy Institute at 10:00, http://www.americantaxpolicyinstitute.org/pdf/InternationalTaxationandCompetitivenessrev080911.pdf.

[29] Jane G. Gravelle, “Reform of US International Taxation Alternatives,” Congressional Research Service, December 17, 2010, p. 13 https://opencrs.com/document/RL34115/.

[30] Congressional Budget Office, “Options for Taxing U.S. Multinational Corporations,” January 2013, p. 18.

[31] Ibid.

[32] See Camp proposal, http://waysandmeans.house.gov/taxreform/.

[33] President’s Council on Jobs and Competitiveness, “Roadmap to Renewal: Invest in Our Future, Build on Our Strengths, Play to Win,” 2011 Year-end Report, pg. 47. http://files.jobs-council.com/files/2012/01/JobsCouncil_2011YearEndReport1.pdf; President’s Export Council, Letter to the President, December 9, 2010, http://www.trade.gov/pec/docs/PEC_Tax_Letter_120910.pdf; Diana Furchtgott-Roth, Yevgeniy Feyman, “The Merits of a Territorial Tax System,” Manhattan Institute, Issues 2012: No. 29, October 2012, http://www.manhattan-institute.org/html/ir_29.htm#.UQgq1GdZMg8.

[34] The Joint Committee on Taxation found that repealing most corporate tax expenditures — excluding deferral — would pay for cutting the corporate rate only to 28 percent, and that such a rate cut would add to deficits outside the 10-year budget window. See Joint Committee on Taxation, Revenue Memorandum, October 27, 2011, http://democrats.waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/media/pdf/112/JCTRevenueestimatesFinal.pdf.

[35] “International Taxation and Competitiveness,” Conference Sponsored by the American Tax Policy Institute, http://www.americantaxpolicyinstitute.org/pdf/InternationalTaxationandCompetitivenessrev080911.pdf.

[36] Shay, 2012, Footnote 103.

[37] Office of Management and Budget, Table 17-2, 2012. http://www.whitehouse.gov/omb/budget/Supplemental.

[38] Edward D. Kleinbard, “The Lessons of Stateless Income,” Tax Law Review, Vol. 65 (2012), pp. 99-172, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1791783##.

[39] Ibid.

[40] Congressional Budget Office, “Options for Taxing Multinational Corporations,” January 2013, p. 4.

[41] “International Taxation and Competitiveness,” Conference Sponsored by the American Tax Policy Institute, http://www.americantaxpolicyinstitute.org/pdf/InternationalTaxationandCompetitivenessrev080911.pdf.

[42] Edward D. Kleinbard, “The Lessons of Stateless Income,” Tax Law Review, Vol. 65 (2012), pp. 99-172, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1791783##; Brent Wells and Cym Lowell, “Tax Base Erosion and Homeless Income: Collection at Source is the Linchpin,” 65 Tax Law Review 535, July 18, 2011 http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1888397&http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1888397.

[43] Lori Hinnant, “Europe Takes on Tech Giants and Their Tax Havens,” Associated Press, December 3, 2012, http://bigstory.ap.org/article/europe-takes-tech-giants-and-their-tax-havens-0.

[44] Robert Hutton & Thomas Penny, “Cameron Says ‘Smell the Coffee’ as He Vows Tax Fight, Trade Push,” Bloomberg, January 24, 2013 http://www.bloomberg.com/news/2013-01-24/cameron-says-smell-the-coffee-as-he-vows-tax-fight-trade-push.html.

[45] Edward D. Kleinbard, “The Lessons of Stateless Income,” Tax Law Review, Vol. 65 (2012), pp. 99-172, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1791783##.

[46] Ibid.

[47] Ibid., at pp. 160-162.

[48] Organisation for Economic Co-operation and Development, “The OECD Work on Base Erosion and Profit Shifting,” Background Brief, November 20, 2012, http://www.oecd.org/ctp/BEPS_Background_Brief.pdf.

[49] Joint Committee on Taxation, “Estimated Budget Effects Of The Revenue Provisions Contained in the President’s Fiscal Year 2013 Budget Proposal,” March 12, 2012, https://www.jct.gov/publications.html?func=startdown&id=4413.

[50] U.S. Department of the Treasury and the White House, “The President’s Framework for Business Tax Reform,” February 2012, http://www.treasury.gov/resource-center/tax-policy/Documents/The-Presidents-Framework-for-Business-Tax-Reform-02-22-2012.pdf.

[51] See pp. 38-41 in Jane G. Gravelle, “Moving to a Territorial Income Tax: Options and Challenges,” Congressional Research Service, July 25, 2012, http://www.fas.org/sgp/crs/misc/R42624.pdf.

More from the Authors

Areas of Expertise

Areas of Expertise