Testimony: Chad Stone, Chief Economist, Before the Joint Economic Committee

Hearing on “Spend Less, Owe Less, Grow the Economy”

Vice Chairman Brady and other members of the Committee, thank you for inviting me to testify. I feel especially privileged to be appearing as a witness before the Joint Economic Committee, which together with the President's Council of Economic Advisers — both established by the Employment Act of 1946 — provided (in stimulus language) about 14 full-time-equivalent-years of employment for me personally, but more important provided me with a valuable education in economic policymaking.

I commend the JEC for holding this hearing on the critical economic policy concern of our time — one that echoes the concerns underlying enactment of the Employment Act over six decades ago — and that is finding the right set of policies to help the economy emerge from its current deep slump and achieve sustainable economic growth with high employment and broadly shared prosperity.

U.S. policymakers must make smart choices about taxes, spending, and deficits to meet this challenge. Making smart choices requires differentiating between 1) the longer-term policies needed to produce sustainable growth and broadly shared prosperity at high levels of employment and 2) the short-term policies needed to restore high levels of employment in the wake of a deep recession. In particular, policies aimed at reducing the budget deficit are a key ingredient of longer-term policy but are likely to be counterproductive in the short run if implemented too precipitously.

This is the mainstream economic position, as enunciated by Federal Reserve Chairman Ben Bernanke a week ago, speaking at the Annual Conference of the Committee for a Responsible Federal Budget:

Fiscal sustainability is a long-run concept. Achieving fiscal sustainability, therefore, requires a long-run plan, one that reduces deficits over an extended period and that, to the fullest extent possible, is credible, practical, and enforceable. In current circumstances, an advantage of taking a longer-term perspective in forming concrete plans for fiscal consolidation is that policymakers can avoid a sudden fiscal contraction that might put the still-fragile recovery at risk. At the same time, acting now to put in place a credible plan for reducing future deficits would not only enhance economic performance in the long run, but could also yield near-term benefits by leading to lower long-term interest rates and increased consumer and business confidence.[1]

The Congressional Budget Office has made similar points in its Economic and Budget Outlook:

To prevent debt from becoming unsupportable, policymakers will have to substantially restrain the growth of spending, raise revenues significantly above their historical share of GDP, or pursue some combination of those two approaches. The longer the necessary adjustments are delayed, the greater will be the negative consequences of the mounting debt, the more uncertain individuals and businesses will be about future government policies, and the more drastic the ultimate policy changes will need to be. But changes of the magnitude that will ultimately be required could be disruptive. Therefore, policymakers may wish to implement them gradually so as to avoid a sudden negative impact on the economy, particularly as it recovers from the severe recession, and so as to give families, businesses, and state and local governments time to plan and adjust. [2]

At the Center on Budget and Policy Priorities, we have enunciated a recommended framework for measures to achieve fiscal sustainability. [3] We believe the United States should enact policies to put deficits and debt on a sustainable path, which in practical terms means reducing the budget deficit over the coming decade to no more than about 3 percent of GDP in order to stabilize the debt-to-GDP ratio. Like the Fed and CBO, we believe that policymakers should meet this fiscal stabilization goal in a reasonable period of time, but it is important to avoid a sudden negative impact on a still-fragile recovery by implementing it too precipitously.

I recognize that one of the purposes of this hearing is to highlight a different point of view from what I regard as this mainstream economic consensus. This alternative point of view appears to be based on three premises: that the United States faces an immediate debt crisis due to an unwarranted explosion of government spending; that immediate sharp reductions in government spending are necessary and could even make the economy grow faster in the short run; and that deficit reduction is more likely to be successful if it is composed largely of spending cuts rather than tax increases.

In the remainder of my testimony I will discuss why I find all three of these arguments unpersuasive, with the empirical support for them being weak and largely irrelevant to current U.S. economic conditions. In addition, I am concerned that insistence on large immediate budget cuts, and opposition to any kind of revenue-raising measures — including raising revenues by narrowing unproductive economically inefficient tax expenditures — constitutes a barrier to enacting the kind of credible, practical, and enforceable deficit reduction plan that we should be striving to implement.

The remainder of my testimony is organized into three sections that make the following key points:

- Policies enacted since the 2008 election are not the main drivers of deficits and debt . The U.S. fiscal imbalance problem is a long-term problem that has little to do with the short term imbalances that have emerged as a result of the financial crisis and Great Recession. The main driver over the long term is unsustainable growth in health care costs throughout the U.S. health care system, in the public and private sectors alike. Increases in the deficit due to policies enacted over the past few years are temporary and only their relatively modest associated interest costs add to longer term deficits.

- Large immediate cuts in government spending will hurt the still-fragile economic recovery. Economic and budget conditions in the United States are very different from those in countries deemed to have had successful fiscal adjustments. Looking at the empirical literature on "expansionary austerity," the International Monetary Fund found little empirical support for the idea that immediate sharp reductions in government spending strengthen an economic recovery. The Congressional Research Service found that fiscal adjustments beginning in a slack economy such as the United States is now experiencing have a low probability of success.

- International evidence has little to say about how much of U.S. deficit reduction should be spending cuts and how much should be revenue increases. The United States needs a long-term deficit-reduction plan and most of the empirical literature is about short-sharp fiscal consolidations under very different economic and budget circumstances from those we face. The literature on short, sharp adjustments has nothing to say about the composition of a long-term deficit reduction package or the proper size of government. It also does not come to grips with the fact that the United States is unique in the extent to which it relies on the tax code to do what other countries do directly through government spending – the so-called tax expenditures. Finally, it ignores lessons from successful longer-term deficit reduction efforts such as the United States pursued in the 1990s, when revenue measures were a significant component of the 1990 budget agreement and the deficit reduction act of 1993, which were followed by the longest economic expansion in our history and a balanced budget by the end of the decade.

What's Driving Deficits and Debt?

As Fed Chairman Bernanke said in the speech cited earlier,

The nation's long-term fiscal imbalances did not emerge overnight. To a significant extent, they are the result of an aging population and fast-rising health-care costs, both of which have been predicted for decades.[4]

CBO, we at CBPP, and other budget experts were warning that federal budget deficits and debt were on an unsustainable long-run path well before the recent financial crisis and recession and that the main driver over the long term is unsustainable growth in health care costs throughout the U.S. health care system, in the public and private sectors alike.

Most recently, the sharp increase in budget deficits and debt reflects temporary effects of the financial crisis and deep recession and the policies implemented to keep the economy from plunging into an even deeper economic hole.[5] But analysis shows that other factors are driving projected deficits and debt over the next decade. [6]

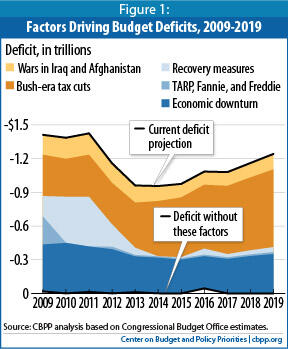

Figure 1 focuses on the projected deficit going forward. It shows that the economic downturn, tax cuts enacted under President Bush, and the wars in Afghanistan and Iraq explain virtually the entire federal budget deficit over the next ten years. The economic downturn added about $300 billion chiefly from the operation of the automatic stabilizers (declining revenue and increased outlays for unemployment insurance and other pro-cyclical spending) and associated interest costs. Both the financial-market measures enacted under President Bush and largely implemented under President Obama such as the Troubled Asset Relief Program (TARP), and the Recovery Act tax cuts and increases in spending enacted under President Obama, were important drivers of the surge in deficits in 2009-11, but those measures will largely have phased out by the end of this year, leaving only associated interest costs in subsequent years.

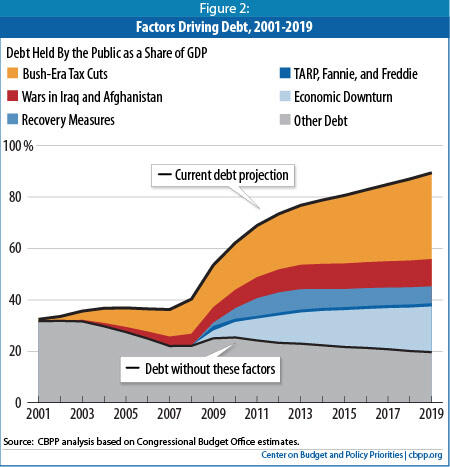

The debt chart (Figure 2) looks at debt held by the public, which reflects funds that the federal government borrows in credit markets to finance deficits and other cash needs. Debt held by the public is basically the cumulative sum of all past budget deficits minus surpluses. It's the proper measure on which to focus because it's what really affects the economy.[7] Analysts compare it to GDP because stabilizing the debt-to-GDP ratio is a key test of fiscal sustainability.

This economically and financially meaningful measure of the debt is different from the seriously flawed measures more likely to crop up in discussions of the debt problem: gross debt and its close cousin, debt subject to statutory limit. These measures are larger, and therefore perhaps viewed as more scary, than debt held by the public, because they include debt the government owes to itself, such as the money the Social Security trust fund has lent to the Treasury in years when Social Security's earmarked revenues exceeded expenditures. As CBO explained in a recent report,[8] however, gross debt "is not a good indicator of the government's future obligations," and the Treasury securities held by trust funds "represent internal transactions of the government and thus have no direct effect on credit markets."

To sum up this discussion of drivers of deficits and debt, these charts refute the notion that ongoing increases in deficits and debt arise mainly as a result of policies instituted since President Obama was elected. Take away the Bush-era tax cuts, and budget deficits are significantly smaller over the rest of this decade and the debt is stable (rising only about as fast as the economy is growing) over the second half of this decade. Of course, the serious long-term budget deficits associated with rising health expenditures and an aging population would still be there and the imperative to stabilize the longer-term deficit would remain.

The bottom line is that the recession and actions taken to combat it added temporarily to the deficit and bumped up the level of the debt, but the long term problems that were evident in 2007 remain the major drivers of the long term deficit. We could stabilize the debt-to-GDP ratio over the coming decade by taking actions like those recommended in CBPP's deficit-reduction principles paper. [9] We would still have to come to grips with rising costs throughout the U.S. health care system, however, to keep the debt-to-GDP ratio stable over a longer horizon.

The False Promise of Expansionary Austerity

Mainstream economic policy analysis has identified various clear symptoms of a debt crisis, and of economies in which excessive government spending or stimulus crowds out private economic activity. When a debt crisis hits, interest rates spike because investors are worried about financial losses on their holdings of government securities, through either inflation or outright default, and seek to liquidate their holdings or at least demand a higher risk premium. In the case of crowding out, interest rates and inflation rise due to the strain of surging aggregate demand on the economy's productive capacity.

There are numerous instances of countries experiencing one or the other (or both) of these situations, as evidenced in the large set of historical data on industrialized countries compiled by the Organization for Economic Cooperation and Development (OECD). But the United States right now is not one of them. Interest rates are very low, core inflation (which excludes volatile food and energy prices) remains low, and there is a substantial gap between the output that the economy would be able to produce with full utilization of its existing labor force and productive capacity ("potential output") and the output it is actually producing.

Under these circumstances, and with the economic recovery still struggling to gain the traction it needs for the United States to make strong progress toward restoring high levels of employment and shared prosperity, I take the warnings from Fed Chairman Bernanke and the CBO about trying to reduce budget deficits too quickly just as seriously as I take their warnings about the perils of failing to seriously address the budget deficit. We learned in the 1990s that a strong economic recovery makes deficit reduction easier. Accepting larger budget deficits in the short term in order to put the recovery on a sounder footing is fully consistent with putting in place a credible plan for achieving longer-run fiscal sustainability, although there is a tension.

That tension is absent in the conclusion that people are apt to draw from the JEC Republicans' study that gives this hearing its title or from the American Enterprise Institute paper co-authored by my fellow witness Kevin Hassett. The JEC Republican Study, "Spend Less, Owe Less, Grow the Economy" states that "a growing body of empirical studies proves that fiscal consolidation programs based predominantly or entirely on government spending reductions are far more likely to be successful" at stabilizing deficits than programs based on tax increases [emphasis added]. The report argues that "quick, decisive government spending reductions" are a key to success and that deficit-reduction programs focusing on spending cuts "may even boost the real GDP growth rate in the short term under certain circumstances."

The studies on which these conclusions are based, most prominently one by Harvard economists Alberto Alesina and Sylvia Ardagna, examine disparate countries facing disparate economic and budget situations under disparate global economic conditions. The limitations of this work, many of them self-acknowledged, deserve much greater scrutiny. I want to make the following points, which also are made in an important report on these issues that the Congressional Research Service recently issued: [10]

- Evidence that cutting spending increases GDP in the short term is very weak. The International Monetary Fund has concluded with regard to Alesina and Ardagna's study, "The idea that fiscal austerity triggers faster growth in the short term finds little support in the data."

- Evidence that a deficit-reduction program focused on spending cuts can promote short-term growth and long-term fiscal stability is slim . Alesina and Ardagna identified 107 episodes of "large" deficit-reduction programs. Among these, we count only nine that they characterized as both "successful" (i.e., the program stabilized the debt) and "expansionary" (i.e., it did not harm economic growth in the short term). All nine occurred in small, mainly Scandinavian economies: Finland, Ireland, the Netherlands, New Zealand, Norway, and Sweden. All are much smaller economies than the U.S., and the Scandinavian countries have significantly larger public sectors.

- U.S. macroeconomic and budget conditions aren't right for sharp spending cuts . When analysts began to examine the specific episodes Alesina and Ardagna found in which spending cuts boosted short-term growth, they found that none of them took place in a country still feeling the effects of a large recession as the United States is now, with substantial economic slack, low interest rates, tepid economic growth, and high unemployment. [11] The CRS study reached similar conclusions and found, in addition, that "Almost nine out of ten fiscal adjustments beginning when actual output was below potential output were unsuccessful — fiscal adjustments beginning in a slack economy (such as the current situation in the U.S.) appear to have a low probability of success." [12]

The IMF's reading of the international evidence is that immediate sharp deficit reduction harms short-term economic growth, whether it is achieved primarily through spending cuts or through tax increases. While the IMF finds that growth falls less in episodes dominated by spending cuts, that's mainly because the monetary policy response (how much interest rates are cut) has tended to be greater in such episodes than in those dominated by tax increases. That's all a far cry from saying that the best thing for the U.S. economy is to cut spending immediately or that future U.S. deficit-reduction efforts should consist mostly or entirely of spending cuts.

The countries that boosted growth could do so because falling interest rates from an expansionary monetary policy stimulated investment, because a depreciating currency stimulated net exports to cushion the drop in consumption stemming from the spending cuts, or some combination of the two. The United States does not have these options now: interest rates are already very low, and our major trading partners are still feeling the effects of the financial crisis and recession themselves.

The CRS summarizes its report this way:

The findings in the Alesina and Ardagna study that successful debt reductions were associated with higher growth when spending cuts were used was based on 9 observations out of 107 instances of deficit reduction, or less than 10% of the sample. In addition, most of the countries where debt reductions were successful were at or close to full employment, while the United States remains well below full employment, raising questions as to whether this evidence is applicable to current U.S. conditions. Thus, both methodological questions and questions of applicability to current circumstances can be raised for the Alesina and Ardagna, and similar, studies.

The claim that government spending is crowding out productive private investment at a time when the economy has considerable economic slack goes as much against mainstream economic analysis as the arguments that deep budget cuts in a weak economy will trigger stronger growth and job creation. For government spending to crowd out private spending, the workers, factories, and machines needed to meet the demand generated by the government spending would have to be diverted from other productive activities. To be sure, that can occur in a high-employment economy with no economic slack. But the current situation is very different. For example, when the government provides additional unemployment insurance (UI) benefits to workers struggling to find a job, businesses are helped rather than harmed: the benefits increase consumer demand for goods and services and thereby enable businesses to put unemployed workers back to work and put idle capacity back into production (or to refrain from cutting workforces and production even further).

The crowding out argument would have more force if the economy today looked more like the economy in the 1990s expansion — the longest in our country's history and the last time we had a balanced budget. But in today's economy, weak demand, not competition for funds, is the much more plausible explanation for inadequate investment and job creation.

The premise of the "Spend Less, Owe Less, Grow the Economy" view is that the United States is already in the midst of a debt crisis and immediate action is imperative. Yet investors believe otherwise, as demand for U.S. securities remains strong and interest rates remain at historic lows. Similarly, the Federal Reserve remains more concerned about slack resources and high unemployment than an outbreak of inflation, and Chairman Bernanke is cautioning against immediate sharp spending cuts.

Expansionary Austerity Literature No Help for Long-Term Deficit Reduction

Since the United States doesn't have sharply rising interest rates or other symptoms of an imminent debt crisis, we shouldn't be debating which immediate deficit-reduction steps would be least destructive to the economic recovery. Instead, we should be debating how to strengthen the recovery in the short run while putting in place a sound long-run deficit-reduction program. International evidence on short, sharp adjustments offers no help in that regard, and offers no insight on what the composition of deficit reduction between spending cuts and revenue increases should be. That should not be surprising to anyone who has noted the caveats in the austerity literature. The following two are notable:

- Alesina and Ardagna say in their widely cited study: "Thus, the study of these episodes gives a clue on what happens with sharp and brief changes in the fiscal stance." (emphasis added). How much can a "clue" about "sharp and brief" changes in fiscal stance tell us about the appropriate composition of a long-term deficit reduction strategy?

- In their study, revealingly titled "Limiting the Fall-Out from Fiscal Adjustment," Goldman-Sachs analysts Ben Broadbent and Kevin Daly say:

It is easy to misinterpret the result as a commentary on the — inherently political — question of what constitutes an appropriate level of taxes and government spending in the long run. In this regard, we emphasize at the outset that the results in the literature, and what we add to that here, are only about the transition to fiscal sustainability, not about the size of the government once you arrive at that position. The empirical evidence is much more equivocal with regards to the appropriate size of government in the long run and we do not attempt to comment on this. [13]

As CRS observes, "The mix of policies (tax increases, spending cuts, and the types of either) depend on many factors including preferences for public programs and distributional objectives, as well as growth."[14]

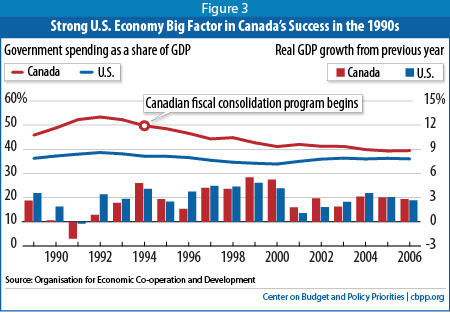

- The pattern of economic growth is very similar in both countries, with growth falling in the slumps of the early 1990s and 2000s and rising in the subsequent expansions. The Canadian economy expanded at an average annual growth rate of 3.4 percent from 1993 to 2006, nearly identical to the 3.3 percent U.S. growth rate.

- Yet the two countries' budget policies were quite different. Government expenditures were much larger as a share of GDP in Canada than in the United States in the early 1990s and remained larger even after Canada's budget cutting. And unlike Canada, the United States achieved impressive budget balancing without especially sharp reductions in government spending — in part by raising taxes on high-income taxpayers in both 1990 and 1993.

Canada started with a level of expenditures significantly higher than the United States and then reduced expenditures at a time when its major trading partner was experiencing a strong economic boom — after raising taxes. The more plausible narrative is that the Canadian economy performed well in this period primarily because the U.S. economy was growing so robustly rather because of Canadian budget cuts.

It is worth emphasizing that the United States experience in the 1990s is a good example of successful deficit reduction followed by a sustained economic expansion. Bipartisan negotiations produced a budget agreement in 1990 that included both tax increases and spending cuts as well as sensible budget enforcement procedures that provided a useful for framework for achieving meaningful deficit reduction. [15] The 1993 deficit reduction act was passed without bipartisan support and amidst dire warnings from opponents that the tax increases on the richest 2-3 percent of taxpayers would throw the economy back into recession. In fact, the United States enjoyed its longest economic expansion on record and the budget was balanced for the first time since 1969.

Finally, I would like to note that the budget contains many revenue measures that are in fact better thought of as spending measures — hence the name "tax expenditures." In 2010, the tax code included over $1trillion a year in tax expenditures. This far exceeded the cost of Medicare and Medicaid combined ($719 billion), or Social Security ($701 billion), or non-security discretionary programs, which stood at $589 billion or a little over half the cost of tax expenditures. Martin Feldstein, the Harvard economist who served as Chairman of President Ronald Reagan's Council of Economic Advisers, wrote last summer that tax expenditures are the single largest source of wasteful and low-priority spending in the federal budget and should be the first place that policymakers go to restrain spending.

Nothing in the literature on international episodes of short-sharp deficit reductions or in our own history of successful deficit reduction tells us that revenue measures cannot or should not be an important component. As a practical matter they must be part of achieving sustainable deficit-reduction that is large enough to do the job, and done right, there is no reason to think they will be an obstacle to achieving sustainable long-term growth with shared prosperity.

Conclusion

The United States faces a serious long-term deficit problem and an immediate short-term problem of slow growth and high unemployment. Current economic and budget conditions in the United States do not look at all like the conditions in countries that have experienced successful deficit reduction through short, sharp fiscal contractions. Non-partisan experts like Fed Chairman Bernanke and the Congressional Budget Office warn against cutting deficits too fast. And as the non-partisan Congressional Research Service concludes from its analysis of the international evidence, cutting budget deficits too rapidly under current U.S. economic conditions is most likely to hurt the economy and ultimately be unsuccessful. If we go down this path, I'm afraid the lesson will be "Spend Less, Grow Less, Slow the Economy."

End Notes

[1] Ben S. Bernanke, "Fiscal Sustainability: Remarks at the Annual Conference of the Committee for a Responsible Federal Budget," Board of Governors of the Federal Reserve System, June 14, 2011: http://www.federalreserve.gov/newsevents/speech/bernanke20110614a.pdf.

[2] Congressional Budget Office, "The Budget and Economic Outlook: Fiscal Years 2011 to 2021," CBO, January 2011: http://www.cbo.gov/ftpdocs/120xx/doc12039/01-26_FY2011Outlook.pdf

[3] Robert Greenstein, "A Framework for Deficit Reduction: Principles and Cautions," Center on Budget and Policy Priorities, March 24, 2011.

[4] Bernanke, 2011

[5] Alan S. Blinder and Mark Zandi, "How the Great Recession Was Brought to an End," July 27, 2010: http://www.economy.com/mark-zandi/documents/End-of-Great-Recession.pdf

[6] Kathy A. Ruffing and James R. Horney, "Economic Downturn and Bush Policies Continue to Drive Large Projected Deficits," Center on Budget and Policy Priorities, May 10, 2011.

[7] James R. Horney, Kathy A. Ruffing, and Paul N. Van de Water, "Fiscal Commission Should Not Focus on Gross Debt," Center on Budget and Policy Priorities, July 21, 2010.

[8] Congressional Budget Office, Federal Debt and Interest Costs, December 2010, Chapter 2: http://www.cbo.gov/ftpdocs/119xx/doc11999/12-14-FederalDebt.pdf

[9] Greenstein 2011. That paper suggests a combination of reasonable savings in discretionary programs, some tax loophole closures, and various entitlement reforms that can be enacted now (for example, in farm subsidies and some other programs, along with some relatively modest additional savings in Medicare that can be taken now) — in conjunction with letting the Bush tax cuts expire after 2012 (or paying for those tax cuts that are extended).

[10] Jane G. Gravelle and Thomas L. Hungerford, "Can Contractionary Fiscal Policy Be Expansionary?" Congressional Research Service Report R41849, June 6, 2011.

[11] Arjun Jayadev and Mike Konczal, "The Boom Not the Slump: The Right Time for Austerity," The Roosevelt Institute, August 23, 2010: http://www.rooseveltinstitute.org/sites/all/files/not_the_time_for_austerity.pdf and Dean Baker, The Myth of Expansionary Fiscal Austerity, Center for Economic and Policy Research, October 2010: http://www.cepr.net/documents/publications/austerity-myth-2010-10.pdf

[12] Gravelle and Hugerford, p.12.

[13] Ben Broadbent and Kevin Daly, "Limiting the Fall-Out from Fiscal Adjustment," Goldman-Sachs Global Economics Paper No: 195, April 14, 2010, p. 4: http://www2.goldmansachs.com/ideas/global-economic-outlook/limiting-the-fallout-doc.pdf

[14] CRS 2011

[15] See Greenstein 2011 for a discussion of the difference between the budget caps in that legislation and the kinds of caps currently being discussed.

More from the Authors