White House Distortions Mask Social Security Benefit Reductions

The President recently endorsed “sliding-scale” benefit reductions in Social Security, as proposed by investment executive Robert Pozen.[1] The Pozen proposal entails reducing benefits for most workers below the benefit levels that would be paid under the current benefit structure. (The benefits under the current benefit structure, sometimes referred to as “scheduled benefits,” are the benefit baseline that President Bush uses when he says there is an $11 trillion deficit in Social Security over an infinite horizon.) Reducing benefits relative to the scheduled benefit levels is how the President proposes to restore Social Security solvency.

On May 4, however, the White House released a document claiming its plan would increase Social Security benefits.[2] This claim is based on several distortions and a shifting and inconsistent standard against which to measure benefit levels. In its May 4 release, the White House also criticized the standard, widely used method for estimating benefit changes under Social Security reform proposals. These criticisms are generally unfounded.

The Center on Budget and Policy Priorities and other organizations that have been analyzing Social Security’s proposals have consistently relied on the standards and methods of the Social Security Administration’s Office of the Chief Actuary, as well as on specific numbers taken directly from the actuaries’ reports. These methods, which the White House criticized, are the same as those that form the basis of the benefit tables in the annual Social Security Trustees’ report, as well as the final report of President Bush’s own Social Security Commission.

The following are some of the principal distortions in the White House document issued May 4.

Distortion #1: The White House analysis compares benefits under its plan, which would close 59 percent of Social Security’s 75-year solvency gap, to the benefits that would be paid under an approach that closes 100 percent of the gap.

The White House claims its plan would increase benefits as compared to “payable benefits” — that is, as compared to the benefit levels that would be paid if no action were taken and Congress allowed the Trust Fund to be exhausted in 2041 and benefits to be reduced thereafter to the levels that Social Security tax receipts would support. This standard is inappropriate, however, for evaluating an Administration plan that is only a partial plan and falls well short of restoring solvency. Any plan that does not fully restore solvency can show benefits that are higher than the “payable benefits” level.

Robert Pozen has stated that his “progressive price indexing” proposal would “close the long-term deficit of Social Security by over 70%.”[3] This is consistent with the analyses of the Social Security actuaries, who analyzed the Pozen plan and found it would close 72 percent of the long-term (i.e., 75-year) deficit. The Pozen plan includes substantial reductions in Social Security disability benefits, however, and President Bush has indicated he will protect such benefits (although the benefits of disabled beneficiaries might still be cut after these beneficiaries reach retirement age[4]). The President’s plan also includes a new minimum benefit, a feature missing from the Pozen proposal.

These alterations in the Pozen proposal result in the President’s proposal eliminating 59 percent of the 75-year Social Security deficit, rather than 70 percent.[*] The White House has claimed its plan would close 70 percent of the gap and that the Pozen plan would close 81 percent of the gap. It turns out that the White House is referring to the percentage of the solvency gap that would be closed in a single year — the 75th year (i.e., 2079). However, the standard way of measuring the degree to which a proposal restores solvency is to measure its effect on the total shortfall over the next 75 years, and the White House plan closes only 59 percent of the 75-year shortfall. In addition, as discussed below, the new White House analysis focuses on benefits in 2050. The impact of its plan on solvency in 2079 is not relevant to that question.

Any plan that solves only part of the problem will have benefits higher than a plan that solves all of the problem. The White House has indicated that it will make additional changes to restore solvency, potentially including more benefit reductions. But such benefit reductions are not factored into the May 4 White House analysis of its plan.'

White House Shifts Standard of Comparison to Suit Its Purpose

In describing Social Security’s “crisis,” the Administration routinely bases its numbers on the scheduled benefits that Social Security promises to pay. The President’s estimate of an $11 trillion deficit in Social Security assumes scheduled benefits. Under payable benefits, there is no Social Security deficit.

Similarly, in a speech on May 3, the President declared that if Congress does nothing, “you’re either going to have to raise your payroll tax...or cut benefits dramatically by 30 percent.” In addition, the May 4 White House analysis includes a table showing what the White House describes as “benefit cuts” under the “if we do nothing” scenario. These benefit cuts are 26 percent in 2041 growing to 32 percent in 2079. All of these benefit cuts are expressed relative to the scheduled benefit baseline.

But when it comes to presenting the President’s plan, the White House shifts and describes it relative to a “payable” benefits baseline (or, on other occasions, to today’s benefits adjusted for inflation).

Distortion #2: The White House ignores the fact that, under its proposal, the Trust Fund would be exhausted in 2047, and benefits would consequently have to be cut about 15 percent at that time; this reduction would be in addition to the benefit reductions the Administration has explicitly proposed.

Under a Pozen-style plan that protects disability benefits and provides a minimum benefit, as the White House says it would do, the Trust Fund will be exhausted in 2047, or only six years later than under current law.[5] If nothing else is done, benefits would have to be cut by about an additional 15 percent at that time, above and beyond the benefit reductions the President has endorsed.

The “payable benefits” standard, to which the White House seeks to compare the benefit levels under its plan, assumes that if no action is taken benefits would otherwise be reduced after the Trust Fund is exhausted in 2041. Consistency requires that the same method be applied after 2047 to the White House proposal.

The White House may respond that under its plan, additional steps would be taken to restore solvency. But that is the whole point — those additional steps are not incorporated into the analysis that the White House put out on May 4, resulting in an apple-to-oranges comparison.

Distortion #3: The so-called “stylized workers” that we and others have used to assess benefit reductions under the President’s plan are a standard tool of analysis developed for such purposes by the Social Security Administration’s actuaries and featured in the actuaries’ own analyses.

The White House criticized the use of what it called “stylized workers” for analyzing of the impact of its proposal on Social Security benefits for workers at different earnings levels. But these workers (termed “scaled low earners,” “scaled medium earners,” “scaled high earners,” etc.) are taken directly from the reports and memoranda of the Social Security Administration’s Office of the Chief Actuary. They are precisely the same “stylized workers” that are used in the annual Social Security Trustees’ report and in the final report of the President’s own Commission to Strengthen Social Security. These “stylized” or typical workers are reasonably reflective of the experience of Americans at different levels of earnings.

The White House makes inaccurate charges about these workers in its May 4 document. It claims, for example, that “the $59,000 worker is assumed to earn that much every year, with annual raises at the rate of wage growth.” This is incorrect; the estimates of the benefit reductions for earners who earn an average of 60 percent more than the average wage (a group called “scaled high earners” by the Social Security actuaries) are based on earners with a realistic career earnings pattern that starts low, rises as the worker ages, and then falls again in the years before retirement. The scaling factors used are those that the SSA actuaries have developed and regularly employ.[6]

These “stylized” workers are used for all of the individual benefit numbers in the annual Social Security Trustees’ report. The Trustees’ report describes this approach as follows: “Four different pre-retirement earnings patterns are represented in table VI.F10… The three scaled-earnings cases have earnings patterns that reflect differences by age in the probability of work and in average earnings levels experienced by insured workers.”[7]

The “scaled medium earner” is a good proxy for the typical worker. For example, according to the Congressional Budget Office’s microsimulation model, the median worker in the middle quintile born in the 1970s will get an initial retirement benefit of $18,500.[8] This is extremely close to the Social Security Trustees projection of $18,491 for a “medium scaled earner.”

Distortion #4: The White House cherry picks the year to make its point.

The White House analysis is based on the year 2050. Not coincidentally, this is the single most favorable year for the methodology the White House elected to use. For any year from 2012 through 2040, benefits under the White House plan are lower than “payable benefits.” (This is because the payable benefits baseline assumes full promised benefits until the Trust Fund is exhausted, while the President’s plan initiates benefit reductions starting with retirees and survivors who become eligible for benefits in 2012.)

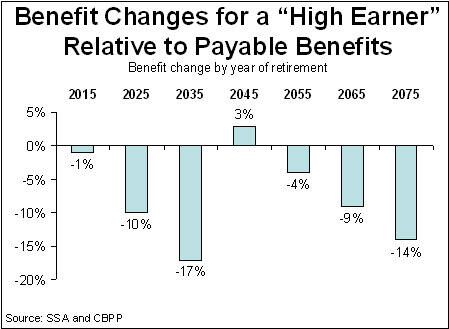

Furthermore, the benefit reductions under the President’s plan grow larger over time. That means that a “high-earner” (one with wages 60 percent above the average wage, or about $59,000 today) who retires in or after the early 2050s will have benefits lower than payable benefits (see bar chart). The White House analysis omits this information, focusing only on benefits in 2050.

Distortion #5: The White House methodology minimizes the benefit reductions in its plan.

Under the “progressive price indexing” proposal that the White House has embraced, benefits would be reduced by increasingly large amounts over time, relative to the benefits under the current benefit structure. Thus, workers who retire in 2050 would be subject to substantially larger reductions than those who retire in 2040.

The White House numbers for 2050, however, include everyone age 62 to 76 in 2050. Many of the people in this group would have become eligible for benefits as early as 2036 and consequently would have gotten much smaller benefit reductions than people who retired in 2050. The White House chart may be misinterpreted by some readers as reflecting the benefit changes for people who retire in 2050.

Distortion #6: The White House assumes unrealistically high stock-market returns for its private accounts and does not to adjust for the increased risk that stock-market investment carries.

The May 4 White House “analysis” is not transparent on the assumptions that it makes about the returns that private accounts would earn; it provides no information on these assumptions. If, as is likely to be the case, these assumptions are based on past Social Security actuaries’ assumptions about future financial market returns, they are likely to be too high for several reasons.

First, the Social Security actuaries assume that the return on stocks will average 6.5 percent above inflation in the future. However, a wide range of leading financial economists surveyed by the Wall Street Journal in February projected that average stock returns would be substantially lower than that.[9] In addition, a recent paper by economists Dean Baker, Brad DeLong, and Paul Krugman demonstrates that if economic growth slows as much as the Social Security Trustees project, then stock returns, as well, are likely to be lower than in the past.[10] The assumed average 6.5 percent real rate of return on stocks assumes that stock-market returns will be as high as in past decades even though economic growth is projected to be markedly lower than in the past.

Another issue is that the President’s proposal calls for “life-cycle accounts,” in which accounts are gradually shifted away from stocks and more heavily to bonds as the worker ages. Life-cycle accounts may reduce the degree of risk, but they also result in lower average returns. Noted financial economist Robert Shiller, author of Irrational Exuberance, has demonstrated that even with historical average rates of return, the median rate of return on “lifecycle accounts” modeled on the President’s proposal would be expected to be 3.4 percent above inflation annually.[11] This is significantly lower than the estimates used by the Social Security actuaries for private accounts that are not life-cycle accounts. (The actuaries have not issued projected rates of return on life-cycle accounts.)

Moreover, Professor Shiller believes the 3.4 percent rate of return (based on historical averages) is itself likely to prove too high, and that a more realistic estimate (that takes into account lower projected future economic growth and other factors) is that the accounts the President has proposed would yield a median rate of return 2.6 percent above inflation. The White House’s May 4 document appears to assume a much higher rate of return.

More fundamentally, the White House results are distorted because they do not take into account the higher risk associated with investing private accounts in the stock market. Most economists agree that the higher average returns in the stock market are compensation for the higher risks that are borne, and that this factor should be incorporated in comparing alternative investment options. For example, Nobel Prize laureate Gary Becker, a conservative economist who favors private accounts, wrote in a recent op-ed: “Contrary to the Bush position, however, I do not believe that the main advantage of a private-account system is that individuals can get a higher return on their old-age savings by investing in stocks. There are no freebies from such investments since the higher return on stocks is related to their greater risk and other trade-offs between stocks and different assets.”[12]

To address this reality, the Congressional Budget Office uses what is known as “risk adjustment” in estimating the returns on private accounts established under Social Security plans. This means that CBO adjusts stock returns to reflect the higher risk that stock investments carry. Under CBO’s analyses, private accounts “are expected to earn an annual return of 3.0 percent [above inflation],” after adjustment for risk.[13] The Office of Management and Budget uses an identical risk-adjustment methodology when estimating the returns that the Railroad Retirement Fund will earn on its stock investments.[14]

End Notes

[1] White House, “Fact Sheet: Strengthening Social Security for Those In Need,” April 28, 2005.

[2] White House, “Interpreting Benefit Estimates for the Pozen Provision,” May 4, 2005.

[3] Robert Pozen, “Testimony on Progressive Indexing before the Senate Finance Committee,” April 26, 2005.

[4] Social Security disability benefits are automatically converted to retirement benefits at that time. The White House has not specified what will happen to people receiving disability benefits when they reach retirement age.

[*]The Center previously released an estimate that the President’s plan closed 57 percent of the solvency gap. That was based on the 2004 Trustees Report, the report used to score the Pozen plan. This estimate is updated to reflect the assumptions in the 2005 Trustees Report.

[5] When combined with the President’s private accounts, the Trust Fund would be exhausted around 2030.

[6] Scaled earners also incorporate the standard employment patterns, specifically the fact that people are less likely to work in their 20s and their 60s. The actuaries’ model does this by scaling down earnings to reflect the probability of working in any given year. See Office of the Chief Actuary, Social Security Administration, “Scaled Factors for Hypothetical Earnings Examples under the 2004 Trustees Report Assumptions,” Actuarial Note No. 2004.3, December 2004.

[7] Social Security Trustees, 2005 Trustees Report, page 185. Note the low, medium and high cases are “scaled.” The actuaries’ “maximum earner” is assumed to have steady earnings at $90,000 per year.

[8] CBO, “Updated Long-term Projections for Social Security,” March 2005.

[9] Mark Whitehouse, “Social Security Reform Plan Leans on Bullish Market,” Wall Street Journal, February 28, 2005.

[10] Dean Baker, Brad DeLong and Paul Krugman, “Asset Returns and Economic Growth,” March 2005.

[11] Robert Shiller, “The Life-Cycle Personal Accounts Proposal for Social Security: An Evaluation,” March 2005.

[12] Gary Becker, “A Political Case for Social Security Reform,” Wall Street Journal, February 15, 2005.

[13] Congressional Budget Office, “Long-term Analysis of Plan 2 of the President’s Commission to Strengthen Social Security,” July 21, 2004.. CBO assumes a risk-adjusted rate of return on investment of 3.3 percent, which is CBO’s projected return on Treasury bonds, minus 0.3 percent for administrative and management fees.

[14]. Office of Management and Budget, Analytical Perspectives, Fiscal Year 2006 Budget, February 2005, p. 421.

More from the Authors