Medicaid Expansion in Health Reform Not Likely to “Crowd Out” Private Insurance

Contrary to claims by some critics, the Medicaid expansion in the new health reform law will overwhelmingly provide coverage to people who otherwise would be uninsured, rather than shift people who already have private coverage to Medicaid.

Under the new law, beginning in 2014 Medicaid will cover non-elderly individuals with incomes up to 133 percent of the federal poverty line — about $29,000 for a family of four.[1] The Congressional Budget Office (CBO) estimates that by 2019, 16 million more adults and children will enroll in Medicaid and gain access to affordable coverage as a result.

Some critics claim that a large share of the insured individuals who become eligible for Medicaid will drop their existing employer or individual market coverage and instead enroll in Medicaid. This claim does not withstand scrutiny: there has been only modest substitution of public for private coverage, or “crowd-out,” in similar state-level expansions of public programs in the past.[2]

- In states that have raised Medicaid income eligibility limits to levels similar to those under health reform, the shares of low-income residents who have private coverage are virtually identical to the shares in states that have not expanded Medicaid coverage.

- An extensive body of research finds that among low-income children enrolled in Medicaid, the proportion that previously was privately insured is between 10 percent and 20 percent, nowhere near the 48 percent rate assumed, for example, in a dubious analysis commissioned by the state of Indiana that some health reform critics have cited (see below).

- The vast majority of low-income individuals who will become eligible for Medicaid under health reform do not have access to affordable private health insurance coverage.

enroll in Medicaid; as a result, the analysis estimates that nearly half of new Medicaid enrollees will have had private insurance. [4]

Cost estimates for Indiana would be 28 percent to 38 percent lower if the analysis assumed a crowd-out rate that reflected consensus research findings. [5]

Expanding Medicaid Has Not Undermined Private Insurance

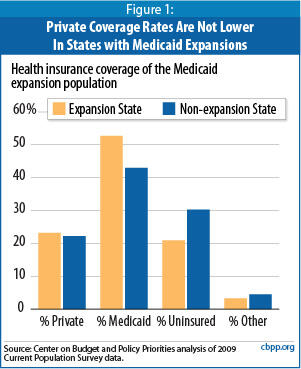

If critics’ claims regarding the extent of crowd-out that will occur under health reform are correct, states that have expanded Medicaid coverage for low-income adults should have significantly lower rates of private coverage among that population than other states. An analysis of Census data finds that this is not the case.

In the 12 states that have expanded Medicaid to cover adults with incomes at or above the poverty line, an average of 23 percent of individuals with incomes eligible for Medicaid have private coverage. In the states that haven’t expanded Medicaid, a nearly identical share — 22 percent — of the same population has private coverage (see Figure 1).[6] Moreover, relative to non-expansion states, the 12 expansion states have a much higher proportion of low-income residents enrolled in Medicaid (53 percent versus 40 percent) and a much lower proportion of low-income residents who are uninsured (21 percent compared to 30 percent).

Nor do these results simply reflect underlying conditions in these groups of states that existed before the Medicaid expansions went into effect.

Consider the examples of Arizona and New York, which expanded Medicaid coverage to poor adults in 2000 and 2001, respectively. In these two states, the decline in private coverage has been no steeper since the expansions were implemented than in non-expansion states. What has occurred in these two states since the expansions took effect is that Medicaid coverage growth has been more robust, and the increase in uninsurance among poor adults has been smaller, than in non-expansion states.[7]

These data strongly indicate that the Medicaid expansions have contributed to a notable decline in uninsured populations rather than to substantial crowding out of existing private coverage.[8]

Extensive Research Finds Minimal Crowd-Out in Past Medicaid and CHIP Expansions

Several other research studies have examined whether Medicaid crowds out private health insurance coverage, focusing primarily on state expansions in the 1990s of children’s Medicaid eligibility to income levels similar to those that will apply to adults under health reform. [9] The most common estimates suggest that if a Medicaid coverage expansion increases enrollment by 100 children, some 80 to 90 of them will have been uninsured, while the rest will have shifted from employer-based insurance. (The estimated size of the crowd-out effect varies from study to study because of methodological differences; some studies find no statistically significant evidence of crowd-out, while others find some crowd-out.)

In addition, the marked reduction in the number of uninsured low-income children after CHIP was created in 1997 and states began easing barriers that were impeding the entry of eligible low-income children into Medicaid provides clear evidence that Medicaid and CHIP expansions primarily benefited uninsured children. Data from three federal agencies demonstrate that the growth of Medicaid and CHIP coverage for children far outweighed the modest losses in private coverage, and led to sharp reductions in the number of uninsured children:

- Centers for Disease Control and Prevention data show that the percentage of children with incomes below 200 percent of the poverty line who are uninsured fell by more than one-third between 1997 and 2005, from 22.6 percent to 13.9 percent.

- Census Bureau data show that the percentage of low-income children who are uninsured declined from 24.6 percent in 1997 to 18.7 percent in 2005. [10] (CDC and the Census Bureau differ in how they define and measure insurance coverage and conduct their surveys, so they produce somewhat different results.)

- The Agency for Healthcare Research and Quality also found a marked reduction in uninsurance among children over the past decade. [11]

Moreover, the modest crowd-out that did occur was overwhelmingly due to an individual or family involuntarily losing its private coverage or finding private coverage to be unaffordable. For example, 93 percent of those who previously had private coverage and enrolled in CHIP did so either due to the loss of private coverage (such as an employer no longer offering health coverage) or because the private coverage had become unaffordable, according to a rigorous ten-state analysis conducted as part of the congressionally mandated CHIP evaluation. [12]

Finally, much of the research on crowd-out in children’s coverage finds that it is a significant factor only when states expand coverage further up the income scale, since children in moderate-income families are more likely to have access to affordable employer-based coverage than their lower-income counterparts. Using a broad definition of crowd-out, CBO concludes that between 25 percent and 50 percent of children enrolled in CHIP — which covers children with incomes too high to qualify for Medicaid — previously had private health insurance.[13] However, two studies that examined the impact of CHIP program expansions found no significant evidence of crowd-out among poorer children eligible for Medicaid. (Expansions higher up the income scale can increase participation among those with lower incomes.) These studies suggest that crowd out is unlikely to be a significant issue among the poor and near-poor people who will be made newly eligible for Medicaid under health reform.

New Study Finds Medicaid Expansion a Good Deal for States

Some state legislators and administrators have expressed concern that the health reform law’s Medicaid expansion will place too great a weight on states’ budgets. A new study by the Urban Institute and the Kaiser Commission on Medicaid and the Uninsured estimates, however, that states’ additional costs under health reform — including costs associated with the predicted levels of crowd-out — will be modest, considering the law’s broad coverage expansion.

In the average state, Medicaid enrollment will increase by 27.4 percent while state costs will increase by just 1.4 percent, the study finds. The primary reason is that the federal government will bear more than 95 percent of the total Medicaid expansion cost, as compared to roughly 57 percent of current Medicaid costs.a

The net cost of the Medicaid expansion may be even less, the authors argue, since the expansion of coverage will likely reduce state costs associated with providing uncompensated care to the uninsured. Referring to criticisms of the expansion as extremely costly to states, the study’s co-author John Holahan commented, “It’s absurd. They come out ahead. It’s just crazy.”

Contrary to some states’ assumption that 100 percent of the people made eligible for Medicaid will participate, the Urban-Kaiser study assumes that between 57 percent and 75 percent of uninsured people who become eligible for Medicaid will enroll and that a much lower share of people with private coverage will exchange it for Medicaid coverage.b

The study’s assumed crowd-out rates fall into the general range — albeit at the higher end — of the existing research. Between 23 percent and 30 percent of those newly enrolled in Medicaid will come from the ranks of the currently insured — including some who would be shifting from other public programs including CHIP) — the study concludes.c

a John Holahan and Irene Headen, Medicaid Coverage and Spending in Health Reform: National and State-by-State Results for Adults at or Below 133% FPL, The Urban Institute and the Kaiser Commission on Medicaid and the Uninsured, May 2010.

b The authors evaluate two scenarios — one under “standard” participation rates and another under “enhanced” participation rates. The standard participation rates attempt to approximate the rates used by CBO in its health reform model. The enhanced participation rates assume more aggressive outreach and enrollment efforts.

c Under the “standard” scenario, 15.9 million people who are newly eligible for Medicaid will enroll in the program, 11.2 million of whom are uninsured. Under the “enhanced” scenario, 22.8 million people will enroll in Medicaid, 17.5 million of whom are uninsured. These figures translate into crowd-out rates of 30 percent and 23 percent, respectively. However, some of the insured individuals who enroll in Medicaid will have been enrolled in CHIP or state-financed health insurance programs, so the incidence of Medicaid substituting for private coverage will be less than these estimates imply.

Large Share of Medicaid-Eligible Population Lacks Access to Employer-Based Coverage

Another reason why crowd-out is unlikely to be a significant factor in the Medicaid expansion is that most low- and moderate-income individuals and families lack access to employer-based coverage. Many low-income workers are employed in small firms and service industries where health insurance is typically not offered as a benefit. In 2005, only 34 percent of non-elderly workers with incomes below the poverty line were offered coverage through their job, compared to 90 percent of workers with incomes at least four times the poverty line. [14] In addition, many low-income workers who are offered employer-based insurance do not take up the coverage because they cannot afford the premiums. [15]

When a low-income family that does have access to private insurance enrolls in Medicaid, the decision is usually beneficial for the family. The private insurance available to the family may contain significant gaps in coverage or may require payment of substantial premiums and large deductibles and cost-sharing charges. Research has shown that when low-income families face large cost-sharing charges, they often go without — or delay obtaining — health care services that they or their children need.[16]

Conclusion

The existing body of research and the results of new analysis show that claims that the new law’s Medicaid expansions will lead to extensive crowd-out are highly exaggerated. Crowd-out rates among the low-income population are best estimated at between 10 percent and 20 percent, significantly less than the analyses touted by critics assume. The incidence of the substitution of public coverage for private coverage is very low at this income range, in large part because of the scarcity of affordable private coverage options. At the same time, health reform’s Medicaid expansion can be expected to lead to a substantial reduction in the number of low-income Americans who are uninsured and to a large increase in access to care among many of the nation’s more vulnerable citizens.

End Notes

[1] In addition, the law requires that states disregard 5 percent of an applicant’s individual or family income when evaluating eligibility for Medicaid. Thus, the effective income-eligibility threshold is 138 percent of the federal poverty line.

[2] Crowd-out can be defined in several different ways, and estimates of the magnitude of crowd-out in public program expansions vary. Generally, crowd-out refers to the substitution of publicly funded coverage for existing private coverage. Individuals may choose to forgo coverage available from their employer or in the individual market because publicly funded coverage is more affordable or more comprehensive. Alternatively, employers may choose to drop coverage for their workers once public coverage becomes available.

[3] For an analysis examining how the federal government will bear the vast majority of the costs of the Medicaid expansion, see January Angeles, “Health Reform Is a Good Deal for States,” Center on Budget and Policy Priorities, April 26, 2010.

[4] Milliman, “Health Care Reform – Comparison of Results,” May 7, 2010.

[5] This estimate is based on a Center on Budget and Policy Priorities (CBPP) analysis assuming crowd-out rates of between 10 percent and 20 percent. The Indiana analysis that assumes a 48 percent crowd-out reaches that level only by assuming that 100 percent of those with private insurance who become newly eligible for Medicaid will drop such coverage and shift to Medicaid. The Indiana analysis also assumes that all uninsured people who become eligible for Medicaid will participate, ignoring the fact that there is no means-tested program that achieves 100 percent participation, or close to it, among those who are eligible.

[6] The 12 expansion states are Arizona, Delaware, the District of Columbia, Hawaii, Maine, Massachusetts, Minnesota, New York, Pennsylvania, Vermont, Washington, and Wisconsin. Several of these states cover adults well above the poverty line, such as Minnesota at 275 percent of poverty for parents and 250 percent of poverty for childless adults. While four of the 12 expansion states have capped enrollment in their expansion programs, private insurance rates are comparable among expansion states with capped enrollment, expansion states without capped enrollment, and non-expansion states.

[7] Based on a CBPP analysis of the ASEC supplement to the 2001, 2002, 2008, and 2009 CPS. The survey data report health insurance coverage in the previous year. For the analysis, we compare aggregated 2001/2002 data with aggregated 2008/2009 data (two years of data are grouped to achieve adequate sample size). We calculate coverage rates among non-elderly adults below 138 percent of the federal poverty line and evaluate change over time. In non-expansion states, private coverage fell six percentage points, Medicaid coverage rose one percentage point, and the uninsurance rate rose five percentage points. Comparable figures for Arizona were a six percentage point decline in private insurance, a six percentage point increase in Medicaid, and only a two percentage point increase in uninsurance. In New York, there was no loss of private coverage, a four percentage point growth in Medicaid, and a three percentage point reduction in the uninsurance rate. We analyze data from Arizona and New York because they are the only states that expanded coverage to poor adults after 2000, the first year for which CPS data are comparable from year to year. For these states, we can evaluate over time the full impact of the Medicaid coverage expansion.

[8] Based on a CBPP analysis of the Annual Social and Economic Characteristics (ASEC) supplement to the 2009 Current Population Survey (CPS). The CBPP analysis includes all non-elderly individuals below 138 percent of the federal poverty line.

[9] See, for example, Gestur Davidson, Lynn Blewett, and Kathleen Call, “Public Program Crowd-out of Private Coverage: What Are the Issues,” The Synthesis Project, Robert Wood Johnson Foundation, June 2004; Lisa Dubay, “Expansions in Public Insurance and Crowd Out: What the Evidence Says,” Kaiser Family Foundation, October 1999; and Anna Sommers, Steve Zuckerman, Lisa Dubay, and Genevieve Kenney, “Substitution of SCHIP for Private Coverage: Results from a 2002 Evaluation in Ten States,” Health Affairs 26:529-537, March/April 2007.

[10] The data in these first two bullets are based on CBPP analyses of the CDC’s National Health Interview Survey and the Census Bureau’s Current Population Survey.

[11] Jessica Vistnes and Jeffrey Rhoads, “Changes in Children’s Health Insurance Status, 1996-2005: Estimates for the U.S. Civilian Noninstitutionalized Population Under Age 18,” Medical Expenditure Panel Survey Statistical Brief #141, Agency for Healthcare Research and Quality, September 2006. This report examined changes in insurance for children at all income levels, not just low-income children.

[12] Anna Sommers, Steve Zuckerman, Lisa Dubay, and Genevieve Kenney, “Substitution of SCHIP for Private Coverage: Results from a 2002 Evaluation in Ten States,” Health Affairs 26:529-537 (March/April 2007).

[13] Congressional Budget Office, “The State Children’s Health Insurance Program,” May 2007.

[14] Bianca DiJulio and Paul D. Jacobs, “Change in Percentage of Families Offered Coverage at Work, 1998-2005,” Kaiser Family Foundation, 2007.

[15] Gregory Acs and Austin Nichols, “Low-income Workers and Their Employers: Characteristics and Challenges,” The Urban Institute, May 2007.

[16] Leighton Ku and Victoria Wachino, “The Effect of Increased Cost-Sharing in Medicaid,” Center on Budget and Policy Priorities, July 7, 2005.

More from the Authors

Areas of Expertise