Changes to Excise Tax on High-Cost Health Plans Address Criticisms, Retain Long-Term Benefits

Under one scenario for Congress to enact health reform legislation, the House would pass the Senate health bill, and the House and Senate would both pass a budget reconciliation bill that includes changes to the health bill that House and Senate leaders have negotiated. One apparent obstacle to this course of action is continued objection by some House members to the Senate bill’s excise tax on high-cost health plans. In the last few months, the Senate excise tax provision has faced a heavy barrage of criticism. Some who expressed opposition to the Senate excise tax provision seem to assume that the criticisms also apply to the more recent agreement on the tax that the Administration and labor leaders have produced. Other policymakers and commentators worry that that agreement would create new problems by unduly favoring labor unions.

Many analysts, including Nobel-prize winning economist Paul Krugman, have found the basic concept of the excise tax to be sound but have noted that certain aspects of the Senate-passed measure — those that, in the popular parlance, would have taxed some “Chevy” plans as well as “Cadillacs” — were problematic and needed to be changed. “The details of the excise tax should be fixed,” Krugman wrote, “but it’s on balance a good idea.” (See Box 1 below.) Sharing that basic view is a broad cross-section of health economists, including many of the nation’s leading progressive economists.

The recent agreement that the Administration and labor leaders negotiated — which, like the basic concept of the excise tax itself, has been misunderstood — fixes the key flaws that Krugman and others identified. At the same time, it maintains the measure’s expected effectiveness in helping to slow health care cost growth over time:

- The agreement solves the principal problem with the Senate provision — that it could tax some plans that are not overly generous but that have a high cost because the plans’ enrollees are disproportionately older and sicker. Age is by far the largest factor that can cause substantial variations in costs of comparable health plans for different groups of enrollees. The agreement fully adjusts the tax, on a permanent basis, for all variation in plan costs caused by the age and gender of enrollees. It thereby addresses the principal reason that the Senate version of the tax could have affected some “Chevys” (that is, plans with typical benefits) as well as “Cadillacs” (that is, very generous plans).

- The agreement also removes the cost of dental and vision coverage in determining whether, and by how much, a plan exceeds the excise tax threshold. Since dental and vision benefits do not contribute significantly to the rapid rise in health care costs, this change eases the bite of the tax without impairing its ability to help slow health care cost growth over time.

- At the same time, the agreement retains the excise tax’s strongest attribute: its promise of helping to slow the rate of growth of health costs, without which health care reform will likely not be sustainable over the long term. Although the agreement will likely reduce the savings that the Senate excise tax provision would have produced by a third to a half over the first ten years, the reduction in savings would be considerably smaller in subsequent decades.

Nevertheless, the agreement between the Administration and labor leaders has faced a new round of attacks (generally from a different set of players). Here, too, examination of the agreement shows the criticisms to be overblown.

- The Congressional Budget Office (CBO), Joint Committee on Taxation (JCT), and most economists have concluded that by restraining the growth of health insurance premiums, the excise tax would allow larger wage increases. Although some opponents of the excise tax deride the notion that employers will pass through the reductions in premiums to workers in the form of higher wages, the trade-off between wages and health insurance premiums is strongly supported both by basic economic analysis and by extensive academic evidence, and has been confirmed by statements by labor unions in the past (see Box 2 below).

- The Senate excise tax provision, however, was problematic in this area in one respect. While workers generally would see their wages rise if their employers made health plans somewhat less generous to avoid the tax, workers whose compensation is set by multi-year collective bargaining contracts — and thus can’t immediately be changed — could have been in jeopardy. In many cases, these workers gave up wage gains for broader health benefits when they negotiated their contracts. The recent agreement addresses this problem by giving workers whose health plans are determined in collective bargaining contracts a transition period through 2017.

- The agreement does not give the union workers a permanent exemption from the excise tax. Starting in 2018 they would face the tax on the same basis as everyone else. The transitional period, however, would give those workers and their unions time to adjust. And those adjustments almost certainly would start well before 2018. Unions with generous health plans that are negotiating before 2018 multi-year contracts that will extend into 2018 almost certainly would seek to shift some compensation from health benefits to wages when they negotiated those contracts.

- Transition rules, or “grandfather” clauses — under which large changes in tax or benefits policies are deferred or phased in over a number of years for various affected groups — are very common in major pieces of legislation. Indeed, as major legislation goes, this five-year transition period (from 2013 through 2017) is not remarkable. Consider, for example, the landmark Tax Reform Act of 1986, widely considered to be one of the outstanding pieces of reform legislation of recent decades. That legislation tightened depreciation rules but exempted property that would be built, remodeled, or acquired under a contract that was in existence by a specified date in 1986. It also included hundreds of other transition rules that were much more narrowly tailored to specific groups, individuals, or businesses.

This analysis examines the strengths and weaknesses of the original Senate excise tax provision, criticisms of that provision that had merit and those that did not, and how the recent agreement seeks to address them.

The Senate Provision and the New Agreement

The Senate-passed bill would have imposed an excise tax of 40 percent on the portion of the value of health plans that exceeds $8,500 for individuals and $23,000 for families, starting in 2013.[1] The new agreement increases those thresholds to $8,900 and $24,000. The thresholds would be increased each year by the rate of increase in the Consumer Price Index plus one percentage point. The tax would be levied on a non-deductible basis on insurance companies or insurance administrators; it would apply to plans sold in the group insurance market and to self-insured plans but not to plans purchased in the individual market.

Under the agreement, the tax thresholds will be adjusted to fully reflect the age and gender of a firm’s workforce. With this change, health plans that have high costs because they cover large numbers of older workers or women will be completely protected from any disproportionate impact of the tax. As in the Senate bill, plans that cover retired people over the age of 55 and people in high-risk occupations also would have higher thresholds. High-risk occupations include law enforcement, firefighting, rescue and ambulance squads, construction, mining, agriculture, forestry, fishing, and longshore work.

The agreement adds a transitional provision that exempts collectively bargained health plans and plans covering state and local government workers from the tax through 2017. The transition period will give labor leaders time to negotiate new contracts and to modify health benefits to fit within the tax thresholds and obtain corresponding increases in workers’ wages. The agreement also retains the Senate bill’s transitional adjustments for plans in high-cost areas. In the 17 states with the nation’s highest health insurance premiums, the thresholds would be 20 percent, 10 percent, and 5 percent higher than these national thresholds for the first three years, respectively.

The agreement removes the cost of dental and vision coverage in determining whether and by how much a plan exceeds the excise tax threshold, thereby effectively raising the threshold further. Since dental and vision benefits are not significant factors in driving the health care cost explosion, their exclusion from the excise tax should not impair the tax’s ability to help control cost growth over time.

With the increase in the tax thresholds, the transitional provisions, and the other changes, the excise tax will take longer to have a significant effect on health care costs than would have been the case under the Senate bill. But it eventually should achieve largely the same results in containing the growth of health care costs.

Box 1: Paul Krugman on the Excise Tax

“Should there be a limit to the tax deductibility of employer-provided health insurance, which is what the excise tax in the Senate bill is supposed to fix?

“My answer is yes, but the final bill should address the criticisms.

“The argument for limiting the tax exclusion is that the tax break on health insurance encourages over-spending, so limiting it could help in the process of ‘bending the curve.’ More generally, since we think the United States spends too much on health for not-so-good results, it makes sense where possible to pay for expanding coverage from the health sector itself. Both arguments are reasonable.

“The counter-arguments seem to run along three lines.

“First, there’s the argument that many ‘Cadillac’ plans aren’t really luxurious — they reflect genuinely high costs. That’s surely true. A flat dollar limit to tax deductibility has real problems. At the very least, the limit should reflect the same factors insurers will be allowed to take into account in setting premiums: age and region.

“Second, there’s the argument that any reductions in premiums won’t be passed through into wages. I just don’t buy that. It’s true that the importance of changing premiums in past wage changes has been exaggerated by many people. But I’m enough of a card-carrying economist to believe that there’s a real tradeoff between benefits and wages.

“Maybe it will help the plausibility of this case to notice that we’re not actually asking whether a fall in premiums would be passed on to workers. Even with the excise tax, premiums are likely to rise over time — just more slowly than they would have otherwise. So what we’re really asking is whether slowing the growth of premiums would reduce the squeeze rising health costs would otherwise have placed on wages. Surely the answer is yes.

“The last argument is that this hurts unions which have traded off lower wages for better benefits. This would be a bigger issue than I think it is if the excise tax were going to kick in instantly. But it won’t, giving time to renegotiate those bargains. And bear in mind that this kind of renegotiation is exactly what the tax is supposed to accomplish.

“A last general point: we really don’t know what it will take to rein in health costs, but that’s a reason to try every plausible idea that experts have proposed. Limiting tax deductibility is definitely one of those ideas.

“Bottom line: the details of the excise tax should be fixed, but it’s on balance a good idea.”

Paul Krugman, “The Conscience of a Liberal: The health insurance excise tax,” The New York Times, January 9, 2010. Available at http://krugman.blogs.nytimes.com/2010/01/09/the-health-insurance-excise-tax/

Strengths of the Excise Tax

The excise tax has many positive features, which is why it enjoys broad support among health economists, including many of the nation’s leading progressive economists.

Slows the Growth in Health Care Costs. The excise tax would help to slow the rate of health care cost growth, without which health reform will not be sustainable in the long run. It would discourage insurers from offering, and firms from purchasing, extremely generous health insurance coverage that promotes excess health care utilization. The Congressional Budget Office (CBO) cites the excise tax as one of the provisions in the Senate bill “that would encourage the development and dissemination of less costly ways to deliver appropriate medical services.”[2]

Henry Aaron, Alan Blinder, David Cutler, Uwe Reinhardt, and 20 other prominent economists — many of them progressives politically — have identified the excise tax as one of the key cost-control measures in health reform. “The excise tax will help curtail the growth of private health insurance premiums,” they wrote to President Obama in November, “by creating incentives to limit the costs of plans to a tax-free amount. . . . This provision offers the most promising approach to reducing private-sector health care costs while also giving a much needed raise to the tens of millions of Americans who receive insurance through their employers.”[3]

Redirects Tax Subsidies to Those Most in Need. The proposed excise tax begins to reform the current upside-down structure of tax subsidies for health insurance. The federal government currently provides Americans with more than $250 billion each year in tax subsidies by excluding the full value of employer-sponsored health insurance from individuals’ taxable income. These subsidies are the largest for high-income individuals who are enrolled in the most expensive health plans. The proposed excise modestly scales back the large subsidies provided to those who have the most expensive coverage in order to finance the expansion of affordable, but considerably more limited, coverage to people without insurance. Tax expenditures for employer-sponsored insurance will total almost $3 trillion over the 2013-2019 period; the excise tax will recoup less than 5 percent of that subsidy.

Does Not Affect Most People and Plans. The large majority of health insurance plans would be unaffected by the excise tax, since the dollar thresholds far exceed the value of the typical plan. In 2013, more than 91 percent of family plans will have premiums below $24,000, the threshold for the excise tax.[4] A plan costing $24,000 in 2013 (the equivalent of about $20,800 in 2010) would be about 40 percent more generous than the plan that most Members of Congress have.[5] In later years, as health insurance costs rise, more plans would be faced with exceeding the tax thresholds, but only to a small degree. Since the tax would apply only to costs above the thresholds, its effect on people with plans just over the thresholds would be minimal.Even by 2019, well below 8 percent of total premiums for employer-sponsored insurance would be affected by the excise tax. [6]

Increases Wages, Not Premiums . By slowing the growth in health care spending, the excise tax would result in higher pay for workers. Most of the affected plans and households would not actually pay the excise tax. The Congressional Budget Office, Joint Committee on Taxation (JCT), and most economists and health analysts who have examined the proposal conclude that health insurance plans and employers generally would respond by modifying their health plans to stay below the thresholds and avoid the excise tax; employers would convert the savings produced by modifying the health plans into higher wages or other compensation for employees. Indeed, JCT estimates that more than four-fifths of the revenue that the government would collect as a result of the excise tax would come from income and payroll tax revenue on the hundreds of billions of dollars in higher wages and salaries that employees would be paid.

Responding to the Criticisms

Opponents of the excise tax have raised four major criticisms of the proposal. We examine each of them in turn.

Sources of High Health Insurance Costs

The high-cost insurance plans that the tax would affect generally offer unusually generous benefits that are not available to most Americans. These plans typically have small or no deductibles, low copayments, few restrictions on choice or provider, and other features that push up costs. [7]

Critics correctly noted that under the Senate excise tax provision, plans could be considered high-cost and made subject to the tax not because they provide very generous benefits, but because they cover an older workforce (or for other reasons). Besides the generosity of its benefits and its network of providers, the major determinant of the cost of a health insurance plan is likely to be the age of the workforce covered by the plan. The health costs of a person aged 55 to 64, for example, average several times those of a young worker. Although the Senate excise tax made an adjustment for the age of a firm’s workforce, that adjustment was not adequate, in part because it applied only to retirees.

The new agreement completely solves the problem by adjusting the tax thresholds to account fully for differences in the cost of health plans that stem from the difference in the age and gender of those covered by the plan, whether they are active workers or retirees. It requires a computation of the amount by which a plan costs more because the composition of its enrollees by age and gender differs from that of a standard beneficiary population. The tax threshold for a plan will be raised by this full amount.

Effects on Cost Sharing

Some critics have argued that to come in at (or below) the excise tax threshold, health plans that otherwise would exceed the threshold would raise deductibles or other cost-sharing charges. This assessment is correct. But the criticisms that such actions would represent a terrible development that would seriously harm workers are greatly overblown. Cost sharing for affected plans generally would remain comparatively modest, and affected plans generally would still be quite generous. The deductibles and co-payments for people who buy coverage in the new health insurance exchanges generally would be several times higher than the deductibles and co-pays that people with the most generous employer plans would face even after their plans were pared back somewhat because of the excise tax.

CBO reports that employer plans overall have an average actuarial value of 88 percent. This means that, on average, the plans pay 88 percent of beneficiaries’ covered health care costs, with beneficiaries paying the other 12 percent of costs out of pocket. The plans that would be subject to the excise tax would, in general, be significantly more generous than the average employer plan and have actuarial values above 90 percent. The excise tax could lead to affected plans trimming a few percentage points off the actuarial value, with employers generally passing through the savings in the form of higher wages, which would be taxable. The resulting increase in federal tax collections would be used to help make coverage more adequate and affordable for people who lack employer coverage and would have far less generous plans. Under the Senate health bill, for example, people buying coverage through the health insurance exchanges who have incomes above 200 percent of the poverty line (above $21,660 for an individual and $36,620 for a family of three) would generally receive coverage with an actuarial value of 70 percent.

Relationship Between Health Costs and Wages

Labor leaders have long argued — persuasively and accurately — that workers have sacrificed higher cash wages to obtain more generous health benefits. By this same logic, there is every reason to conclude that, by restraining the growth of health insurance premiums, the excise tax would allow larger wage increases. Although some critics of the excise tax deride the notion that reductions in premiums will be passed through into higher wages, the trade-off between wages and premiums is strongly supported both by basic economic analysis and by extensive academic evidence (as well as by past statements by unions themselves). CBO, JCT, and most economists — including Krugman and many other highly regarded progressives — have concluded that, by restraining the growth of health insurance premiums, the excise tax would lead to larger wage increases.

Blogger Matt Yglesias has provided a simple illustration of how the process works: “Your boss wants to spend as little money as possible getting you to work for him. Subsidizing your health insurance costs money. Paying you money costs money. You extract as much total money out of him as your market bargaining power lets you do. If he’s willing to part with $65,000 in exchange for your services, he doesn’t care if that’s $55,000 in salary and $10,000 in insurance benefits or $65,000 in cash or whatever. You can bargain what you can bargain for.” [8]

Unions themselves have pointed out in the past that slower growth in health care costs would allow for larger wage increases. For example, a national public employee union has noted that a reduction in health care costs “provides more money for wages,” and a local teachers union has explained to its members that reducing benefits from health insurance would provide a means to increase wages. (See Box 2.)

Box 2: Slower Growth in Health Care Costs Would Leave More Room for Wages, Unions Say

“Reform reduces health care costs and provides more money for wages.”

- AFSCME, “Health Care Reform: What’s in it for Union Members and Families.” Available at http://www.afscme.org/publications/27295.cfm. Accessed January 10, 2010.

“The health care cost spiral is forcing no-win choices upon the bargaining table: do we negotiate a modest wage increase, but take on employee co-pays that reduce or eliminate the wage increase, or accept flat wages in return for keeping health care cost increases at bay?”

- California Federation of Teachers, “Collective bargaining-based health care hits skids.” Available at http://www.cft.org/index.php/current-issues/256-collective-bargaining-based-health-care-hits-skids.html . Accessed January 9, 2010.

“With the tremendous increases in healthcare costs in recent years, little has been left to increase teacher wages.”

“More money would be available for wages if [Madison Teachers Inc.] switched to [health maintenance organization] provided coverage.”

“The question is whether, as a means to increase wages which are subject to income tax, MTI members are willing to reduce the benefits from health insurance and risk paying for healthcare with after tax dollars.”

- Madison [Wisconsin] Teachers Inc., At Issue: Health Insurance, October 2005. Available at http://www.madisonteachers.org/Focused%20Service/Health%20Insurance%20At%20Issue%201.pdf . Accessed January 9, 2010.

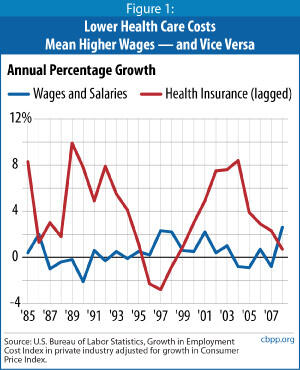

The trade-off between wages and benefits is also visible in economy-wide data on the components of employee compensation. Figure 1 displays the relationship between the annual growth of wages and salaries in private industry and the rate of growth of health insurance costs for the previous year (both adjusted for inflation). From 1985 through 2008, periods of rapid growth in health insurance costs were generally marked by slow growth in wages and salaries, and vice versa. The correlation between the two data series is -0.46, a strong statistical correlation which demonstrates that cash wages and health insurance costs move in opposite directions.

One recent paper on the relationship between health costs and wages successfully attacks the notion “that health care costs are large enough (and the tradeoff with wages is large enough) to drive major changes in overall wages.”[11] Proponents of the excise tax do not argue, however, that the cost of health insurance is either the sole or the principal determinant of wages. Clearly, productivity and other factors matter greatly. And wages do not adjust instantaneously to changes in health insurance costs. But the evidence is powerful that movements in health insurance and wages are closely related, and that at the margin more spending on health insurance leads to lower wages — and vice versa.

In some cases, multi-year labor contracts may make it impossible for unions to renegotiate their members’ compensation package before the excise tax goes into effect. The agreement’s transition provision for plans that are collectively bargained or cover state and local government workers will provide time for these unions and their workers to negotiate new contracts with higher wages.

Distribution of the Tax Burden

Critics of the excise tax also argue that it would be less progressive than some other possible sources of revenue, such as the high-income surcharge included in the House-passed bill.[12] This observation is correct, but it has been overstated.

MIT’s Gruber estimates that the excise tax will raise workers’ wages substantially over the next decade, and the bulk of these additional wages will accrue to middle-income households.[13] Under the Senate-passed version, for example, workers earning less than $100,000 would receive two-thirds of the wage increases, but they would pay only 49 percent of the tax. In contrast, workers earning more than $200,000 would receive 10 percent of the wage gains and pay 16 percent of the tax.[14]

More important, by limiting the existing tax bias in favor of employer-sponsored health insurance, the excise tax would curtail an inequity in the existing tax system. At present, a worker with a health insurance plan that costs $26,000 — for whatever reason — gets twice the tax break that goes to an otherwise similar worker whose insurance costs only $13,000. A worker without employer-sponsored insurance receives no tax benefit at all. The excise tax would reduce, but not eliminate, this disparity.

The excise tax also needs to be viewed in the context of the entire health reform legislation. The House and Senate bills are full of provisions that would create a fairer distribution of health insurance costs, not the least of which is the limit on age-based variation in premiums. Any final legislation that is comprehensive would likely include other tax provisions that fall primarily on very-high income people, such as the Senate’s increase in the Medicare payroll tax on high-wage earners. Any such legislation likely would also provide new health insurance subsidies that would make coverage more adequate and affordable for low- and moderate-income people who purchase insurance through the new health insurance exchanges. Thus, health reform as a whole would improve the progressivity of the federal tax and transfer system.

End Notes

[1] Sections 9001 and 10901 of H.R. 3590, as agreed to by the Senate on December 24, 2009. For purposes of comparison with the thresholds, the value of coverage would include the cost of basic health insurance and reimbursements under a health flexible spending account (FSA), employer contributions to a health savings account or health reimbursement arrangement, and supplementary health insurance coverage.

[2] Congressional Budget Office, An Analysis of Health Insurance Premiums Under the Patient Protection and Affordable Care Act, November 30, 2009, p. 26.

[3] “Economists’ Letter to Obama on Health Care Reform,” New York Times, November 17, 2009. Available at http://economix.blogs.nytimes.com/2009/11/17/economists-letter-to-obama-on-health-care-reform/ .

[4] Thomas A. Barthold, Letter to the Honorable Joe Courtney, December 8, 2009. The figures cited refer to the Senate-passed version of the excise tax. Under the new agreement, fewer plans would be affected, and those that remained subject to the tax would be affected to a smaller extent, but estimates are not yet available.

[5] Blue Cross Blue Shield standard option, the health insurance plan most commonly chosen by federal employees — including Members of Congress — costs $6,459 for individual coverage and $14,589 for a family in 2010.

[6] See footnote 5.

[7] Paul N. Van de Water, Excise Tax on Very High-Cost Health Plans Is a Sound Element of Health Reform,” Center on Budget and Policy Priorities, October 22, 2009.

[8] Matt Yglesias, “Health Care and Wages,” ThinkProgress.org, January 8, 2010. Available at http://yglesias.thinkprogress.org/archives/2010/01/health-care-and-wages.php .

[9] Austin Frakt, “Do Premiums Affect Wages?,” The Incidental Economist, January 7, 2010. Available at http://theincidentaleconomist.com/premiums-wages/.

[10] Jonathan Gruber, “Health Insurance and the Labor Market,” National Bureau of Economic Research Working Paper No. 6762, October 1998. Available at http://econ-www.mit.edu/files/69.

[11] Lawrence Mishel, Employer Health Costs Do Not Drive Wages, Economic Policy Institute, Issue Brief No. 269, January 6, 2010. Available at http://epi.3cdn.net/f121df10fab53d2b16_3nm6bhd7e.pdf.

[12] Chuck Marr, House Health Bill’s High-Income Surcharge Is Sound and Well Targeted, Center on Budget and Policy Priorities, November 6, 2009.

[13] Jonathan Gruber, “‘Cadillac’ tax isn’t a tax—it’s a plan to finance real health reform,” New York Times, December 28, 2009; Gruber, “Impacts of the Senate High Cost Insurance Excise Tax on Wages: Updated,” November 20, 2009. Available at http://econ-www.mit.edu/files/4895.

[14] Barthold, Letter to the Honorable Joe Courtney.

More from the Authors