The Lukewarm 2004 Labor Market: Despite Some Signs of Improvement, Wages Fell, Job Growth Lagged, and Unemployment Spells Remained Long

Introduction

The labor market showed some signs of improvement in 2004; most notable in this regard was the job growth that occurred in every month of the year. This was the first year of consistent job growth since 2000, signaling the end of the jobless recovery. The unemployment rate also showed improvement, falling from an average of 6.0 percent in 2003 to an average of 5.5 percent for last year. On the other hand, several other indicators and comparisons depict a labor market that remains distinctly weak.

- Among nearly all groups of workers, wages fell, relative to inflation. Inflation-adjusted wages grew throughout the recession of 2001 and the jobless recovery that followed. However, by 2003, the persistently weak job market began to take its toll on wage growth, and last year the hourly wages of most workers either remained flat or dropped relative to inflation. (Throughout this analysis, all wage changes are expressed after making an adjustment for inflation.)

This period also represented a return to growing wage inequality, as wages grew faster among workers at the top of the wage spectrum than among other workers. For example, among men, the hourly earnings of the worker right in the middle of the wage spectrum was essentially the same in 2004 as in 2000 (down 0.2 percent), while hourly earnings rose 7.7 percent for the worker at the 95th percentile (five percent of workers have wages higher than this worker, 95 percent have wages lower than this worker).

Further, from 2003 to 2004, the only education group that experienced wage gains was the group where workers had been to graduate school. All other groups — workers with less than a high school education, with a high school education, with some college, or with a college degree — experienced either flat or falling wages. - Over the course of 2004, job growth fell 1.4 million short of the amount that would be typical for a recovery. Since the end of World War II, at this stage of the recovery job growth has typically occurred at a pace that would generate about 300,000 jobs a month. This is the same benchmark that was used when, in early 2004, the Bush Administration forecast that 3.6 million jobs would be created from December 2003 to December 2004.

The 2.2 million jobs created in 2004 thus fell 1.4 million — or nearly 40 percent — short of the level typically experienced at this stage of a recovery.

This shortfall indicates that the drop in the unemployment rate thus did not reflect robust job growth. Instead, it reflected an unusually slow pace of labor force growth. In 2004, the labor force grew more slowly than it had in 13 years. - Due to the relatively modest amount of job creation, long-term unemployment levels remained exceptionally high, with the number of unemployed individuals exhausting their regular state, unemployment benefits and not receiving additional aid hitting a record level of 3.5 million. Though long-term unemployment began to trend down somewhat in 2004 its level continued to be high. There were more than twice as many long-term unemployed — unemployed individuals who have been seeking a job for at least a half a year — in December 2004 as in March 2001, when the downturn began. The long-term unemployed have been more than one in five of the unemployed for 27 straight months, an unprecedented development in the post-WWII period.

Also, in 2004, some 3.5 million individuals used up all their regular unemployment benefits before they found a new job, and did not qualify for additional federal aid. For some period of time, they thus went without either a paycheck or an unemployment check. This level of unmet need was larger than during any other year on record, with data going back to 1973. It suggests that the temporary federal unemployment benefits program — which provided aid to workers who have exhausted their regular, state benefits — was ended too soon (the program quit providing aid to new exhaustees as of the end of December 2003).

All these developments are discussed in detail below.

Wage Trends: Weak Job Market, Higher Inflation, Lead to Real Wage Losses

While the momentum of a labor market that reached full employment in 2000 kept wages rising through the recession and jobless recovery, the persistence of weak labor market conditions since 2001 dampened wage growth by mid-2003. In addition, higher energy prices have recently led to faster price growth. The net result has been that among most workers wages are now failing to keep pace with inflation.

Table 1 presents inflation-adjusted changes in a variety of frequently cited wage series over two periods: from 2000 through 2003 (with the changes expressed on an annual basis), and from 2003 to 2004. The wages levels in the series follow a similar pattern: after rising from 2000 to 2003, they either grew more slowly or fell last year. In some cases, the gains that occurred from 2000-03 were relatively slight (for example, among the typical or median male worker), in part because wage growth slowed considerably by 2003 before turning negative in 2004. [2]

In some cases, wages went from growing relatively quickly from 2000-03 to stagnating in 2004; this was the pattern, for instance, of the wages of the median female worker. In other cases — such as among blue collar, non-managerial workers; the median male worker; and workers with a four-year college education — wages actually fell in 2004. The wage and salary component of the Employment Cost Index (ECI), a broad measure of the costs to employers of compensating workers, rose 1 percent per year in real terms, 2000-03, but fell slightly last year.

The only series that showed compensation growth from 2003 to 2004 was the ECI measure that, in addition to wage and salary costs, also included the costs of fringe benefits such as health premiums and pensions. This measure was up 1.1 percent in real terms, driven by an increase in the cost of fringe benefits. While such an increase signifies greater expenditures by employers on health insurance and pensions for those workers who receive those benefits, it does nothing to raise the take-home pay of the workforce. [3]

The second-to-last line of the table reveals an important countervailing trend in 2004: the sharp climb in productivity since 2000. For many economic analysts, a basic assumption is that the earnings and living standards of working families generally rise with productivity. But in none of these series did wage gains keep pace with productivity growth over this period. What’s more, as productivity growth remained strong in 2004, wage trends turned negative. Of course, the relationship between productivity and living standards is one that evolves over the long-term — we might expect to see gaps like this arise in unusual periods. Still, the extent of the gap is notable, and there’s little economic rationale to justify the 2004 pattern of strongly rising productivity and falling real wages.

Wage Trends Broken out by Gender and Other Characteristics

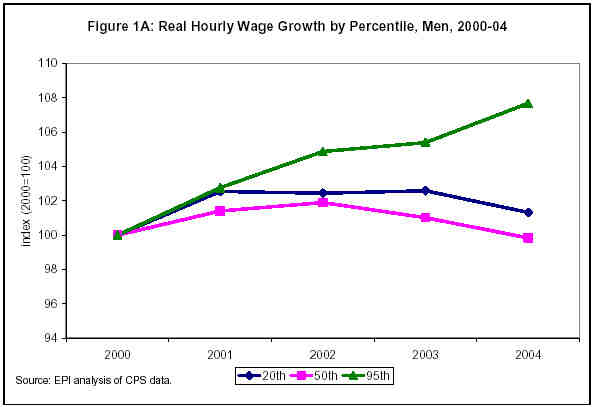

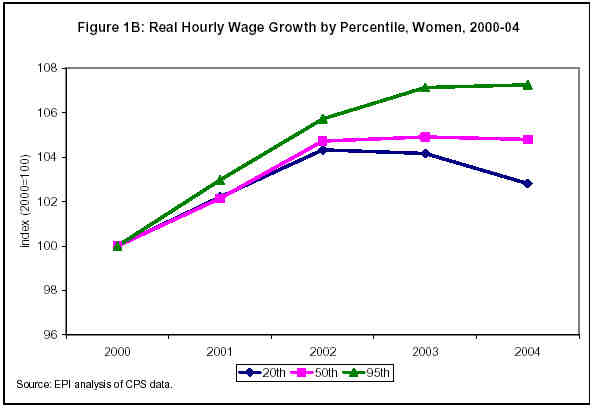

Table 2 takes a closer look at hourly wage trends throughout the wage scale, ranking workers by the level of their wage from lowest to highest. Thus, the 10th percentile represents the wage at which 10 percent earn less and 90 percent earn more. The median is the middle of the wage scale, or the 50th percentile. The table shows the percent changes in real hourly wages by wage deciles (and for the 95th percentile worker) for two time periods: 2000-03 (annualized) and 2003-04. Panels are presented for all workers, for male workers, and for female workers, and the accompanying Figures 1A and 1B focus on selected percentiles that plot the annual data by gender (data are for wage and salary workers, age 18-64). [4]

By wage level. The wages of low- and high-wage men grew by about 1 percent per year from 2000 through 2003, while the wages of the median male worker increased by 0.3 percent per year. (Table 1 shows little wage growth in other male wage deciles below the median). Wage growth for women was more positive, at around 1.5 percent per year for each decile shown in the figure.

In contrast, the data for 2004 reveal losses for middle- and lower-wage workers, and continued (women) or accelerated gains (men) for those at the top of the wage scale. As Table 2 shows, hourly wages fell for the bottom 80 percent of men and the bottom 70 percent of women from 2003 to 2004.

By education level. Table 3 provides a similar analysis by education level, using average hourly wages. For all workers (top panel) wages grew by between 0.7 percent and 1.2 percent per year over the period from 2000 to 2003. The gender panels suggest these gains were driven mostly by trends among women workers, as their wage gains outpaced men in each education category. Among male high school grads and those with some college, wage growth was relatively flat, growing 0.5 percent per year and 0.2 percent per year respectively.

In 2004, these education wage trends turned almost uniformly negative, as the only group with a significant gain was men with advanced degrees. The reversal was particularly sharp for high-school educated women. After growing 1.8 percent per year from 2000 through 2003, their wages fell 1.1 percent last year. The figure also reveals that for some workers, wages were slowing well before 2004. In 2004, however, wage losses became much more common across the wage scale.

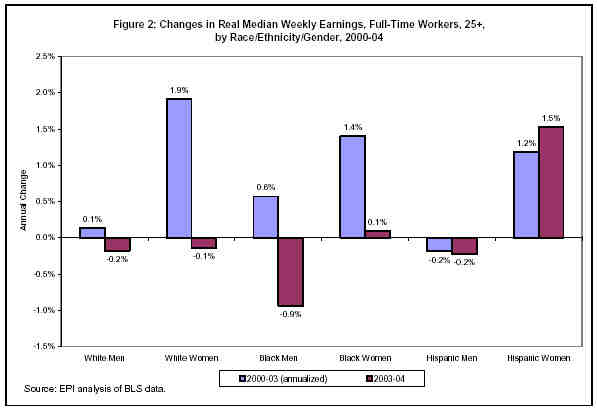

By race and ethnicity. Figure 2 examines BLS data on the median weekly earnings of full-time workers, 25 years and older, by race, ethnicity, and gender. White and Hispanic male workers experienced little earnings growth over the whole period, but for both white and African-American women, earnings went from solidly positive, 2000-03, to flat in 2004. A similar swing in earnings occurred among African-American men. Hispanic women are the only group whose weekly earnings grew more quickly in the latter period, as their median weekly earnings grew 1.2 percent per year from 2000 to 2003, and by 1.5 percent from 2003 to 2004.

Job Growth

Jobs were created in every month in 2004. Last year thus marked an end to the “jobless recovery” and the first year of substantial job growth since 2000. Altogether, 2.2 million jobs — or about 181,000 jobs a month — were created from December 2003 to December 2004. [5]

It is instructive, however, to put this growth into context by comparing it the amount of growth that has occurred during other recoveries. Since the end of World War II, the average annual growth in job creation has equaled 2.9 percent at this stage of the recovery. [6] If such a rate of job creation had been achieved in 2004, about 300,000 jobs per month would have been created from December 2003 through December 2004, or a total of 3.6 million jobs. Indeed, this was the level of job creation projected in the Economic Report of the President released in February 2004. That is, this report projected that non-farm payroll employment would grow by an average of 300,000 jobs per month in 2004. The chairman of the President’s Council of Economic Advisers said that this forecast reflected a rate of job growth “That is about average for a recovery.” [7]

Relative to this benchmark, however, job growth in 2004 continued to lag considerably.

The 2.2 million jobs created last year fell 1.4 million short of the amount of job creation that would have been average for this stage of the recovery.

The average job growth figure of 181,000 was nearly 40 percent below the 300,000 monthly figure typically associated with a recovery.

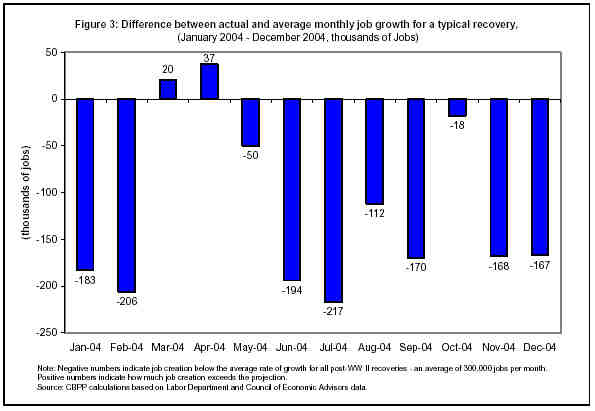

There were only three months during the year — March, April, and October — in which job growth exceeded the average yardstick. In the past two months, job growth occurred at about half the average pace. (See Figure 3)

Job growth over the next year may continue to fall below the level normally associated with a recovery period. This is the conclusion, for example, that was recently reached by the Administration itself. In December, the Administration issued its job growth projections for 2005. These estimates predict job growth in 2005 will average 175,000 a month. While this projection is in line with the pace of job growth in 2004, it also suggests that the Administration itself believes that job creation will continue to occur at a pace well below that typically experienced during a recovery.

Drop in Unemployment Rate Reflects Exceptionally Slow Labor Force Growth Instead of Robust Job Growth

As noted at the beginning of this analysis, the average unemployment rate of 5.5 percent in 2004 represents a drop from its 2003 average of 6.0 percent.

The drop in the unemployment rate, however, did not reflect especially robust job growth; as just discussed, job growth was significantly below the average for a recovery period. Instead, it reflected exceptionally slow labor force growth. The average size of the labor force in 2004 was only 0.6 percent larger than it averaged in 2003. This represents the slowest rate of labor force growth since 1991.

In other words, part of the decline in unemployment is itself a function of the weak job market. When, as is apparently the case now, workers are hesitant to enter or are quick to leave the labor force, this leads to both lower labor force participation rates and lower measured unemployment. In fact, the share of the population in the labor force fell each year since 2000, from 67.1% to 66% in 2004, the lowest annual level since 1988. In this climate, the lower unemployment rate in 2004 relative to 2003 does not reflect a tighter job market.

Long-term Unemployment Trends Signal Difficult Labor Market for Many Unemployed Workers

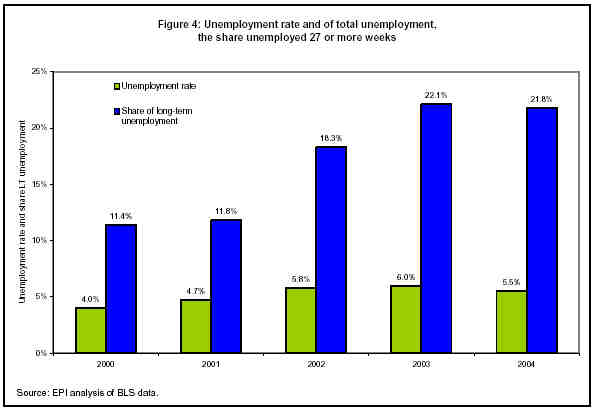

One symptom of the inadequate pace of job growth is the persistence of long-term unemployment, commonly defined as an unemployment spell lasting at least half-a-year (27 or more weeks). A hallmark of the jobless recovery and ensuing period of slow job growth has been levels of long-term unemployment well above those normally associated with unemployment in the five percent to six percent range.

As shown in Figure 4, both unemployment rates and the share of unemployed who were long-termers increased substantially from 2000 to 2003. Both measures fell from 2003 to 2004 but the long-term share remained above 20 percent. In fact, more than a fifth of the unemployed have been long-termers for 27 months in a row, from October 2002 to December 2004, an unprecedented development over recent decades.

Thus, while decreasing unemployment is good news, that it is accompanied by high shares of long-term unemployment is an indication that the level of job growth is too slow for many jobseekers.

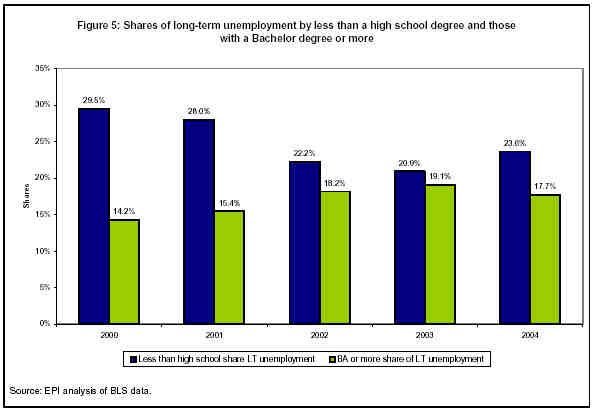

As is usually the case, the less-educated bear the brunt of economic downturns. The 2001 recession and subsequent weak recovery, however, saw an expansion of hardship across educational lines. In fact, the educational composition of the long-term unemployed has shifted since 2000 towards the more highly educated, as shown in Figure 5.

In 2000, 64.7 percent of the long-term unemployed had a high school degree or less, while those with more than a high school degree were 35.3 percent of the long-term unemployed (Figure 5). By 2004, the share with at least some college grew by 7.6 percentage points and the high-school or less share shrunk accordingly. While the difference in long-term unemployment shares by education was almost 30 percentage-points in 2000, a much narrower 14.2 percentage-point differential existed in 2004.

This shift suggests that even by 2004, highly educated workers continued to have difficulty finding jobs. The on-going weak demand for college educated workers is likely one reason why their real wages fell in 2004.

Unemployment Insurance Exhaustions

Consistent with the problem of enduring long-term unemployment, the lack of adequate job creation has also created another problem: in 2004, a record number of persons exhausted their regular unemployment benefits before they found a job. Typically, these people have been unemployed for 39 weeks, or three-quarters of the year, when they exhaust their benefits. In 2004, an exceptionally large number of jobless workers exhausted their regular benefits, went for a time without federal aid, and received neither a paycheck nor an unemployment check.

Labor Department data show that 3,530,000 unemployed individuals exhausted their regular unemployment benefits in 2004. About 20,000 of them qualified for additional unemployment aid through the permanent federal/state extended benefits program. (This program, whose eligibility criteria are quite stringent, was only in effect in four states in January 2004 and has not been in effect in any state since May.) The remaining 3.5 million individuals did not qualify for any federal unemployment benefits beyond their regular benefits.

The 3.5 million jobless workers that exhausted their regular benefits and went without federal aid during 2004 was higher than the number of such exhaustees in any other period of comparable length on record. (Data are available since 1973) The comparison adjusts for the growth in the labor force over time; that is, the record figure is not a reflection of the growth in the labor force but of the current severity of long-term unemployment.

The record number of exhaustees suggests the federal temporary benefits program was ended prematurely. The Temporary Extended Unemployment Compensation (TEUC) program was created in March 2002 to provide additional weeks of federally funded unemployment benefits to jobless workers who have run out of regular, state-funded unemployment benefits but have not found a job. TEUC provided up to 13 weeks of benefits to most workers who participated in it. The program phased out when Congress declined to extend the program beyond the close of December 2003. President Bush did not ask Congress for an extension. Individuals who have exhausted their regular unemployment benefits since December 20, 2003 have not been eligible for TEUC aid.

Stated differently, over the past three-plus decades, during any other year when 3.5 million or more people were using up their regular unemployment insurance benefits, a temporary federal benefits program was in place to assist them.

Conclusion: The Loss of Full Employment and the Unbalanced Recovery

These problems of falling wages, inadequate job creation, long-term unemployment, and a safety net that’s failing to protect job losers have contributed to a recovery that is considerably unbalanced. The economic growth that has occurred has flowed to corporate profits to a degree unseen in the post-World War II period, leaving relatively little for compensation. [8] These economic conditions stand in stark contrast to those that prevailed at the end of the last business cycle, where full employment ensured that the benefits of the growing economy lifted the living standards of working families the income scale.

The job market data presented above show that even though unemployment was at a relatively low level in 2004 — 5.5 percent — substantial slack remains in the job market. As long as this slack remains, the negative 2004 wage trends documented above are unlikely to reverse course.

In fact, using an econometric model of wage growth, and plugging in Blue Chip 2005 consensus values for unemployment (5.3 percent), inflation (2.5 percent), and productivity (2.6 percent, from Jorgenson et al, 2004)[9], we forecasted some of the series discussed above. [10] The forecast has wages among the typical male or female worker continuing to fall by about 1 percent in 2005. In addition, the aforementioned forecast of the Administration suggests that job growth will continue to occur at a level well below that experienced in other recoveries.

Whether these pessimistic forecasts actually occur will depend largely on whether and how quickly we return to a more normal, and far more robust, labor market recovery. Absent this reversal, much of our economy’s growth will continue to accrue to the top to wage and income scale, reinforcing the unbalanced nature of a recovery that has thus far eluded too many working families.

We thank Yulia Fungard for research assistance, Danielle Gao for programming, and Jeff Chapman for bootstrapping percentile standard errors.

| Table 1: | ||

| 2000-03 | 2003-04 | |

| Average Hourly Earnings, non-supervisors | 0.9% | -0.5% |

| Average Weekly Earnings, non-supervisors | 0.3% | -0.4% |

| Median Hourly Wages, All Workers | ||

| Men | 0.3% | -1.2% |

| Women | 1.6% | -0.1% |

| Median Weekly Earnings, Full-Time Workers, 25+ | ||

| Men | 0.2% | -0.2% |

| Women | 1.9% | -0.1% |

| High School Hourly Wage | 1.1% | -0.5% |

| College Hourly Wage | 0.7% | -1.0% |

| Employment Cost Index, W&S | 1.0% | -0.2% |

| Employment Cost Index, Compensation | 1.6% | 1.1% |

| Productivity | 3.8% | 4.0% |

| Inflation (CPI-U) | 2.2% | 2.7% |

| Notes: Average hourly and weekly earnings are for production, non-supervisory workers. Percentile hourly wages and wages by education are for all wage and salary workers, 18-64 years old. Median weekly earnings are for full-time workers, age 16 and up. The employment cost index is an index of hourly employer costs for all civilian workers. Productivity is from the nonfarm business sector; 2003-04 uses the average from the first three quarters of each year, as productivity data for 2004q4 are not yet available. Each series comes from the Bureau of Labor Statistics except for percentile hourly wages and wages by education, which come from EPI's analysis of CPS earnings files. We deflate these latter series by the CPI-RS; all other wage and compensation data are deflated using the CPI-U. The growth rates of these deflators are almost identical over this period, the only difference being that the RS grows by 2.223% per year, 2000-03 while the U grows 2.224%. | ||

| Table 2: | ||||||||||

| Percentile | ||||||||||

| All | 10th | 20th | 30th | 40th | Median | 60th | 70th | 80th | 90th | 95th |

| 2000-03 | 1.3% | 0.7% | 1.0% | 1.6% | 1.4% | 0.9% | 1.1% | 1.3% | 1.8% | 1.3% |

| 2003-04 | -1.3% | -0.5% | -1.7% | -1.0% | 0.0% | -0.4% | -1.2% | 0.4% | -0.8% | 1.0% |

| Men | ||||||||||

| 2000-03 | 0.6% | 0.9% | 0.5% | 0.3% | 0.3% | 0.9% | 1.0% | 1.0% | 1.1% | 1.8% |

| 2003-04 | -0.8% | -1.2% | -1.1% | -0.4% | -1.2% | -1.1% | -1.1% | -0.5% | 1.9% | 2.2% |

| Women | ||||||||||

| 2000-03 | 1.4% | 1.4% | 1.6% | 1.3% | 1.6% | 2.1% | 2.0% | 1.5% | 1.6% | 2.3% |

| 2003-04 | -0.8% | -1.3% | -0.4% | 0.0% | -0.1% | -0.2% | -0.6% | 1.2% | 1.4% | 0.1% |

| Source: EPI analysis of Current Population Service data. | ||||||||||

| Table 3: | |||||

| All | Less than High School | High School | Some College | College | Advanced Degree |

| 2000-03 | 1.2% | 1.1% | 0.7% | 0.7% | 0.7% |

| 2003-04 | -0.8% | -0.5% | -0.3% | -1.0% | 1.1% |

| Men | |||||

| 2000-03 | 1.0% | 0.5% | 0.2% | 0.8% | 0.8% |

| 2003-04 | -0.7% | -0.3% | 0.0% | -1.1% | 2.0% |

| Women | |||||

| 2000-03 | 1.4% | 1.8% | 1.3% | 0.9% | 0.9% |

| 2003-04 | -1.4% | -1.1% | -0.9% | -1.1% | 0.1% |

| Source: EPI analysis of CPS data. Note: All 2000-03 changes are statistically significant at the 0.05 level, except male, some college. For 2003-04, these changes are significant: College, all; HS, Some College, and College, female, (the latter two at the 0.1 level), and male, advanced. | |||||

End Notes

[1] Sylvia Allegretto and Jared Bernstein are economists at the Economic Policy Institute; Isaac Shapiro is an associate director at the Center on Budget and Policy Priorities.

[2] We identified these trends in The State of Working American, 2004/2005 by Mishel et al, 2004 (Introduction). For example, male median wages fell in real terms in 2003 by 0.9 percent; the real average hourly earnings of production, non-supervisory workers increased by about 1 percent per year in both 2001 and 2002, slowing to 0.4 percent in 2003.

[3] As opposed to increases in wages and salaries, the degree to which the increases in payments for insurance and pensions have enhanced living standards is unclear. Rising employer payments for health insurance premiums partly reflect the acceleration in health care cost growth, which may not appreciably benefit covered workers. In addition, many employers with pension plans that promise a defined benefit to workers have had to increase their pension contributions to make up for the drop in the stock market, which reduced the value of pension plans’ portfolios. The increased contributions were necessary to assure payment of the promised pension benefits. In this respect, the current increase in pension contributions makes workers no better off than they were before, since many workers would still expect to receive the same pension benefit that was promised previously.

[4] Bootstrapped standard errors reveal that, 2003-04, changes less than 1 percent are statistically insignificant at the 0.05 level and visa versa.

[5] These employment data come from the BLS Establishment survey. This survey, also known as the “payroll employment survey,” is the standard measure of employment featured by the government and relied upon by economists. In 2004, the director of the Bureau of Labor Statistics, the Congressional Budget Office, and Federal Reserve Chairman Alan Greenspan, all reiterated how this measure is more accurate for measuring than the “household employment survey” some have been citing. For a detailed discussion of the advantages of the Establishment over the Household survey for this purpose, see Elise Gould “Measuring Employment Since the Recovery,” Economic Policy Institute briefing paper # 148, December 2003.

[6] This is the average growth rate of payroll employment from the 25th to 37th month in a recovery, averaging over all past recoveries for which such an average can be taken (in two cases, the recovery had ended by this point and, thus, were not included in the average).

[7] Reuters News Service, “White House advisor says sees big job gains in 2004,” February 10, 2004. The Administration later backed off this CEA projection somewhat. For a detailed analysis of CEA’s 2004 projection, see two reports co-authored by Jared Bernstein, Lee Price, and Isaac Shapiro, “White House Backs Off CEA Prediction of ‘Average’ Job Growth,” Center on Budget and Policy Priorities and Economic Policy Institute, February 18, 2004; and “Missing the Moving Target,” February 12, 2004, Appendix Table B.

[8] David Kamin and Isaac Shapiro, “An Uneven Recovery: New Government Data Show Corporate Profits Enjoying Unusually Large Gains, While Workers’ Incomes Lag Behind,” Center on Budget and Policy Priorities, September 3, 2004.

[9] Jorgenson, Ho, and Stiroh “Will the U.S. Productivity Resurgence Continue?” Federal Reserve Bank of NY, Current Issues Vol. 10, No. 13, December 2004.

[10] Bernstein and Baker “The Benefits of Full Employment,” Economic Policy Institute 2003, Chapter 4, for a description of the wage forecasting model.

More from the Authors