Lower-Cost Estate Tax Repeal Reflects Slow Phase-In

Cost in the Second Ten Years Could Reach $1.3

Trillion

by Joel Friedman

| View PDF of full report View HTML of short version View PDF of short version If you cannot access the file through the link, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

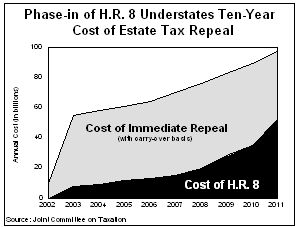

The House Ways and Means Committee bill (H.R. 8) to repeal the estate tax in 2011 has a much lower cost than other repeal proposals because of its extremely slow phase-in. The Joint Committee on Taxation estimates that the bill will cost $186 billion between 2002 and 2011. This is $81 billion less than the President estimated his proposal to cost; it is less than one-third of the Joint Tax Committee's $662 billion estimate of what immediate repeal would cost. The Joint Tax Committee's estimate of immediate repeal assumes capital gains on inherited assets are taxed in a manner similar to the way they would be taxed under the Ways and Means bill (known as "carry-over basis").

The bill also includes modest provisions to address the widespread income tax avoidance that the Joint Tax Committee expects to occur following repeal of estate and gift taxation (because, as discussed below, repeal would open up new tax avoidance strategies). But these provisions, as well as the proposed treatment of inherited capital gains, have virtually no impact on the bill's low ten-year cost, as they would not become effective until after the estate tax has been repealed in 2011.

- Because repeal of the estate tax is delayed until 2011, the full cost of the Ways and Means bill does not occur until the years after 2011. In the ten-year period between 2012 and 2021, the bill will likely cost about $1.3 trillion, even when the modest cost-saving provisions in the bill are taken into account. The cost in the second ten years is nearly seven times the cost in the first ten years.

- This $1.3 trillion cost between 2012 and 2021 could be reduced by

several hundred billion dollars, but that would require subsequent action to identify,

design, enact, and implement effective measures to prevent income tax avoidance. Testimony

before the Ways and Means Committee and recent articles have highlighted the vast

opportunities for income tax avoidance that repeal of the estate and gift tax could

create. The bill calls on the Treasury Department to study income tax avoidance

opportunities created by repeal of the estate and gift tax, acknowledging that further

steps will be

required to stem the

revenue losses that the bill eventually will cause, but there are serious questions as to

whether effective enforcement measures can be designed and implemented.

required to stem the

revenue losses that the bill eventually will cause, but there are serious questions as to

whether effective enforcement measures can be designed and implemented.

- The high cost in the second ten years is of particular concern, because that is when the costs associated with the retirement of the baby boom generation will increasingly be felt. Indeed, recent projections show that the long-term budget outlook has worsened rather than improved, because health care spending is now expected to grow faster over the long term than previously had been assumed.

Ways and Means Bill Relies on "Backloading"

The Ways and Means Committee bill to repeal the estate tax relies on "backloading" — pushing off repeal to 2011 (two years later than President Bush proposed), and lowering the estate tax rate much more slowly in the intervening years than under the Bush plan. As a result, the cost of the bill would jump from zero in 2002 and $13 billion in 2006 to $34 billion in 2010 and $49 billion in 2011, which is still well below the full cost. In other words, the cost would nearly triple between the fifth and ninth years, jump another 50 percent between the ninth and tenth years, and continue growing after the tenth year.

The Ways and Means Committee has relied on backloading to stay within the revenue targets set by the budget resolution the House of Representatives approved on March 28. The House budget resolution reflects the Bush Administration tax-cut target of $1.6 trillion over ten years, 2002 to 2011, excluding interest costs. To date, the House has passed two tax bills (H.R. 3 and H.R. 6) that together cost more than $1.3 trillion over this period. This leaves only $310 billion to accommodate the remaining pieces of the Bush tax plan, which the Administration estimates will cost $530 billion over ten years.(1) To make all the pieces fit, the Ways and Means Committee resorted to backloading estate tax repeal.

The backloading of estate tax repeal in the Ways and Means bill masks the bill's true cost over the first ten years. It has other consequences as well. Testimony received by the Ways and Means Committee pointed out that this long phase-in period for estate tax repeal also adds great complexity to estate planning.(2) People will have to maintain alternative wills and other estate planning documents, as their plans will be different depending on whether they die before or after the estate tax has been repealed. To the extent that there is uncertainty about whether repeal will be achieved — as well as whether the accompanying carry-over basis provision with its complex record-keeping requirements is implemented — estate planning becomes even more complicated. Supporters of estate tax repeal often point to the complexities of current estate planning as a rationale for repealing the tax, yet the backloaded approach taken by the Ways and Means Committee would add to this burden over the next decade rather than reduce it.

Full Cost of Repeal

The Joint Tax Committee has calculated the cost of immediately repealing the estate and gift tax, assuming a new tax treatment of some inherited assets — known as "carry-over basis," because the original basis or purchase price of the asset is carried over to the heirs — as proposed in H.R. 2488 (which Congress enacted and President Clinton vetoed in 1999). The carry-over basis provisions are similar to those in the current Ways and Means bill, H.R. 8; President Bush includes no carry-over basis in his repeal proposal.

- The Joint Tax Committee estimates that immediate repeal with carry-over basis would cost $662 billion over ten years, with the cost in 2011 reaching $97 billion.

- Under current law, the estate and gift tax will generate $410 billion in revenue over this period. The $252 billion of additional revenue losses in the Joint Tax Committee's estimate reflect the impact of income tax avoidance, opportunities for which would be created by repeal of the estate and gift tax.

- The Joint Tax Committee's estimates indicate that by 2011, for every dollar of estate and gift tax revenue lost, an additional 80 cents of income tax revenue would also be lost.

The Joint Tax Committee's estimate highlights the important interaction between the income tax code and the estate and gift tax. The Joint Tax Committee explains that it has recently adjusted its estimates to take into account the "significant revenue effects that result from a variety of income tax avoidance opportunities made possible by the repeal of the estate and gift tax."(3) That is, in the absence of estate and gift taxes, high-income families would have more flexibility to avoid income taxes.

With the attention generated by proposals to repeal the estate and gift tax, a number of commentators and practitioners have highlighted the potential for income tax avoidance in the absence of the estate and gift tax.(4) They have pointed out, for example, that without a gift tax assets can be transferred freely among taxpayers, making it possible for high-income persons to transfer income and assets to individuals who pay lower tax rates — such as a friend or relative in a lower tax bracket or living overseas — or to a trust. There are many ways these transfers can be done so that the high-income individual retains effective control of the asset.

Impact of Carry-Over Basis Appears to be Limited Some supporters of carry-over basis have argued it would replace a large portion of the revenues lost by the repeal of the estate tax. However, the Joint Tax Committee’s estimates, which assume a carry-over basis provision similar to the one included in the Ways and Means bill, show substantial revenue losses resulting from repeal of the estate and gift tax. Under current law, capital gains tax is levied on the difference between the original purchase price (or basis) of an asset and the value of the asset when it is sold. Heirs, however, inherit an asset at its value at the time of the decedent’s death. Thus, the original basis is "stepped up" to the market value at the time of the decedent’s death, and none of the appreciation in the value of the asset up to that point is subject to tax. The Ways and Means bill proposes to change this favorable treatment, requiring that for purposes of capital gains tax a portion of the assets in large estates would be valued at the original purchase price. In other words, the original "basis" would "carry over" to the new owner. If the heirs of such estates later sold the assets, capital gains taxes would be due on the difference between the price for which they sold the assets and the original price that the individual who died had paid for the asset. The Joint Tax Committee previously estimated that carry-over basis would yield $52.5 billion in additional revenues over ten years, or less than 13 percent of the total estate and gift tax revenue that would be collected over the period. The Ways and Means bill, however, exempts substantial amounts of inherited capital gains from carry-over basis. The bill would allow the basis of inherited assets to be increased by $1.3 million. Assets bequeathed to a surviving spouse would receive an additional $3 million increase in basis, bringing the total increase for assets transferred to a surviving spouse to $4.3 million. Thus a married couple could combine these exemptions from carry-over basis — $4.3 million when the first spouse dies, and another $1.3 million when the surviving spouse dies — to avoid capital gains taxation on up to $5.6 million of asset appreciation. Similar treatment of inherited assets, including the exemptions from carry-over basis, was included in estate tax repeal legislation the previous Congress enacted and President Clinton vetoed. It is not possible to determine from the Joint Tax Committee estimate of immediate repeal the precise impact of carry-over basis with exemptions. It is clear, however, that the bill’s carry-over basis requirement cannot offset more than a modest portion of either the loss of estate and gift revenues or the loss of income tax revenues that will accompany repeal of the estate and gift tax. The Joint Tax Committee has estimated that the total revenue loss from repeal combined with a carry-over basis with these exemptions would be $96.9 billion in 2011, of which $53.4 billion is lost estate and gift tax revenues and $43.5 billion is lost income tax revenues. The $43.5 billion in lost income tax revenues reflects the net impact of income tax avoidance offset by the additional revenues generated by the carry-over basis requirements. The bill’s carry-over basis provision thus is not the "silver bullet" to reduce costs that some had hoped it would be. Moreover, it is unclear whether carry-over basis will ever be implemented. Experience from the 1976 tax reform, when carry-over basis was enacted and then later repealed, would indicate that the complexities of implementing carry-over basis may prove to be insurmountable. |

The Actual Cost of the Phased-in Ways and Means Bill

The Ways and Means bill shows a revenue loss of $49 billion in 2011. This understates the true, on-going cost of repeal for two reasons. First, repeal would be in effect only for the final nine months of fiscal year 2011. Yet it takes at least one year to settle an estate. As a result, estate tax revenues from individuals who died in the preceding year or two would continue to be collected in 2011, reducing the overall revenue loss in that year. Second, the Joint Tax Committee's estimate of the revenue loss from immediate repeal shows that the income tax revenue losses grow throughout the ten-year period. Because under the Ways and Means bill the cost of repeal would not occur until the very end of the initial ten-year period, the $186 billion revenue loss resulting from the bill over the first ten years includes little of the revenue loss resulting from income tax avoidance that would ultimately occur.

It should be noted that the Joint Tax Committee stated in its estimate of immediate repeal that the income tax losses could be "reduced" if provisions were included to "prevent income tax avoidance and to enhance compliance." The Ways and Means bill, however, includes provisions that would have only a modest effect in addressing the anticipated income tax avoidance. The bill acknowledges that far more must be done to curb such avoidance, as it requires the Treasury Department to "conduct a study of opportunities for avoidance of the income tax" resulting from repeal of the estate and gift tax. The implication is that once Treasury conducts the study, future legislation can be considered that will include further anti-abuse provisions. There is no assurance, however, that Treasury will be able to design effective mechanisms to curb abuse or that such procedures could be enacted.

Budget rules require that in estimating the cost of legislation only the impact of language in a bill that alters existing law can be considered. The official estimators will estimate only the costs or savings associated with changes that a bill makes to the law and will not show costs or savings for provisions in a bill that reflect an intent to enact future legislation. While the provision in the Ways and Means Committee bill calling on the Treasury Department to study income tax avoidance strategies expected to emerge upon repeal of the estate and gift tax may express the Committee's interest in addressing these issues in the future, it has no impact on the estimated cost of the current legislation.

Applying these standard rules to estimating the cost in the second ten years, the period from 2012 to 2021, we find that the bill would result in revenue losses totaling approximately $1.3 trillion. This estimate takes into account the bill's carry-over basis and modest anti-abuse provisions. If Treasury identifies further anti-abuse measures and they are enacted in subsequent legislation and effectively implemented, it would be possible to reduce the income tax losses associated with repeal of the estate and gift, as the Joint Tax Committee indicated. We estimate that, even if such provisions were in place before repeal takes effect, the cost in the second ten years would still be between $1.3 trillion and $800 billion — with the lower end of the range requiring extremely effective measures, casting doubt on whether such a low estimate is feasible.

In calculating estimates for the second ten years, we typically assume that revenue losses associated with tax cuts grow in the years after 2011 at the same rate as the economy, such that they remain a constant share of gross domestic product or GDP. Estate and gift tax revenues lost as a result of repeal are assumed to grow somewhat faster, increasing relative to the economy, because the estate tax exemption in current law is not indexed to inflation. Although it rises from its current level of $675,000 to $1 million by 2006, the exemption remains at $1 million in the years after 2007. Income tax revenues lost as a result of repeal, however, are assumed to grow at the same rate as the economy after 2011.(5)

These estimates indicate that the cost of the Ways and Means bill in the second ten years would be approximately $1.3 trillion — or nearly seven times greater than the $186 billion cost in the first ten years. Even if the effects of inflation are removed, the cost of the bill in the second ten years would still be close to six times greater than the cost in the first ten years. (In 2001 dollars, the cost of the H.R. 8 in 2002 to 2011 would be about $160 billion, while the cost of the bill in 2012 to 2021 would be $940 billion, based on the language in the bill.)

Effective Implementation of Carry-Over Basis and Anti-Abuse Provisions Unclear

As noted, the Joint Tax Committee has taken income tax avoidance into account in estimating the cost of proposals to repeal the estate tax. The Joint Tax Committee has stated that costs could be "reduced" if measures were implemented to prevent these activities. It is unclear, however, whether measures to reduce the overall cost of estate tax repeal — either through carry-over basis or through anti-abuse measures to prevent income tax avoidance — can be effectively implemented.

The difficulties inherent in administering a carry-over basis provision are well known. A carry-over basis provision was enacted a little over 20 years ago, but it never took effect because of these complexities. The Tax Reform Act of 1976, which lowered the estate tax rate and increased the amount of an estate exempt from estate taxes, applied capital gains taxes to inherited assets when sold, based on the original purchase price of the asset. That provision was repealed in 1980, before it took effect. According to a Congressional Research Service report, the primary rationale for repeal was the concern that the carry-over basis would result in great administrative burdens for estates, heirs, and the Treasury Department.

A key problem is that, for assets that have been held for a long time, records on the original purchase price could be missing, and it could be difficult to establish the price for which the decedent purchased them. Moreover, the exemptions in the Ways and Means bill increase these complications. As noted in the box, a married couple could combine exemptions so that capital gains taxation on up to $5.6 million of asset appreciation could be avoided by the heirs. Once the assets were inherited, the record keeping and enforcement burden of distinguishing between assets that retained their original purchase price as a basis and assets that were revalued at death would be substantial. When the second generation passed on estates that include a mix of protected and unprotected assets, the complexities would multiply. Still more complexity would be added by opportunities for allocating the exemptions to best advantage. A wealthy person (or executor) would have the opportunity to minimize capital gains taxes by carefully choosing which assets would qualify for the exemption from carry-over basis and which assets would not, based on factors such as the likelihood of an asset being held or sold by the heirs. These complexities call into question whether carry-over basis will be implemented or, once again, be repealed before taking affect.

Beyond these administrative issues, there are concerns that making carry-over basis effective could require fundamental changes to tax law that may ultimately be unacceptable. For instance, in her testimony before Ways and Means, Lauren Detzel, an attorney based in Florida who specializes in estate tax planning, stated that because the proceeds of life insurance policies are not included in gross income for tax purposes, a family could shift assets into life insurance policies to avoid tax under a carry-over basis system. She said that changes in law to overcome this tax avoidance strategy and make carry-over basis effective would "represent the most severe change in the taxation of life insurance proceeds since the adoption of the Sixteenth Amendment to the Constitution." (The 16th amendment established the modern income tax in 1913.)

The opportunities for income tax avoidance would also be numerous, as individuals would have freedom to transfer assets in the absence of a gift tax. As noted, assets could be transferred to individuals for whom the income generated by the assets would be taxed at lower rates than would be the case if the original owner held the assets. The transfers could take place in various ways, including ways that do not necessarily cede control over the asset. While the IRS may be able to determine in advance some of the more straightforward tax avoidance schemes that would be employed, strategies to evade taxes are often complex, involving multiple steps and transactions in order to hide their true intent.

The problem goes beyond identifying these tax avoidance strategies and would require active enforcement by the Internal Revenue Service. For individual income tax returns filed in 1997, the IRS audited about one percent of all returns, and about two percent for taxpayers with incomes over $100,000. Recent evidence suggests that even these low rates have fallen by half over the last two years.(6) It is not clear, given these low audit rates, how the IRS could implement such rules effectively.

For instance, the bill includes a provision to address a loophole created by the repeal of the gift tax. The bill states that if a person were to give away an asset as a gift and were to receive, or was expected to receive, something of value in return, the IRS could treat the gift as never having been made and tax the person for any income the asset produced. In theory, this would suggest than an asset could not simply be given to someone in a lower tax bracket with the expectation that the after-tax income on the asset would be returned. But such a provision is likely to prove exceedingly difficult to enforce. Whether a person has received, or is expected to receive, something in value in return for a gift will likely be a matter of judgment, particularly when the gift-giving is between family members. It seems unlikely that the IRS could enforce such rules without extensive use of audits. Yet few policymakers are calling for expanding IRS' audit capabilities; this is not a cause that supporters of estate tax repeal are championing.

Conclusion

The House Ways and Means Committee's bill would repeal the estate and gift tax in 2011. The ten-year phase-in of estate tax repeal not only adds great complexity to estate planning, but masks the true cost of the bill over the next ten years. In the decade after 2011, when the full effect of the bill will be felt, the cost would be about $1.3 trillion — or nearly seven times the $186 billion cost in the first ten years. Reducing the cost in the second ten years would require subsequent action to shut down the proliferation of income tax avoidance schemes that the Joint Committee on Taxation believes will occur following repeal of the estate and gift tax. Whether tax laws can be changed to prevent these schemes is far from certain. Even if they can be successfully implemented, the cost in the second ten years still would be at least four times greater than in the first decade. Rising costs in the second ten years are of particular concern, because that is when the costs associated with the retirement of the baby boom generation begin to impact the budget.

End notes:

1. Joel Friedman, Richard Kogan, and James Sly, "House Ways and Means Committee Action To Date Adds $300 Billion to Cost of Administration's Tax Cuts," Center on Budget and Policy Priorities, March 23, 2001.

2. Lauren Y. Detzel, "Comments on Proposal to Repeal or Revise the Federal Estate and Gift Tax System," Testimony Before the House Ways and Means Committee, March 21, 2001

3. Lindy Paull, "Memorandum to John Buckley: Estate and Gift Tax Estimates," Joint Committee on Taxation, March 26, 2001.

4. Lauren Y. Detzel, "Comments on Proposal to Repeal or Revise the Federal Estate and Gift Tax System," Testimony Before the House Ways and Means Committee, March 21, 2001; Jonathan G. Blattmachr and Mitchell M. Gans, "Wealth Transfer Tax Repeal: Some Thoughts on Policy and Planning," Tax Notes, January 15, 2001; John Buckley, "Transfer Tax Repeal Proposals: Implications for the Income Tax," Tax Notes, January 22, 2001; and David Cay Johnston, "Questions Raised on New Bush Plan To End Estate Tax," New York Times, January 29, 2001.

5. For more details on methodology for the 2012 to 2021 projections, see Richard Kogan, Joel Friedman, and Robert Greenstein, "Cost of Tax Cut Would More Than Double to $5 Trillion in Next Decade," Center on Budget and Policy Priorities, April 2, 2001.

6. David Cay Johnston, "Rate of All I.R.S. Audits Falls; Poor Face Intense Scrutiny," The New York Times, February 16, 2001.