Tax Foundation Figures Lead to Inaccurate

Impression of Middle-Income Tax Burdens

by Iris J. Lav, Joel Friedman, and James Sly

| View PDF version of this full report View HTML of factsheet View PDF of factsheet If you cannot access the file through the link, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Each year since 1993, the Tax Foundation has claimed that the average tax burden of Americans has reached a new record high, and that "Tax Freedom Day" — the day the Tax Foundation estimates Americans must work to pay their taxes — occurs later in the year. The Tax Foundation released its latest tax burden report today, stating that Americans must work until May 3 to pay their taxes for the year.

The Tax Foundation's report — when it concludes that "the average American taxpayer is shouldering a heavier tax burden than he ever has before" — presents a misleading picture of the tax burden middle-income families face. The Tax Foundation's conclusion is at odds with the findings of the Congressional Budget Office and the Joint Committee on Taxation, the two leading sources of tax information for Congress. CBO and the Joint Tax Committee find that:

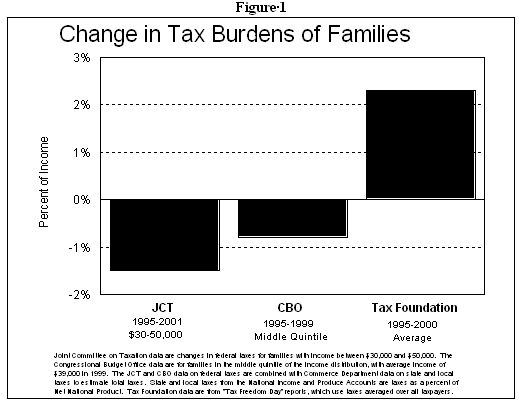

- Taxes on families in the middle of the income spectrum are substantially lower than the taxes the Tax Foundation claims Americans pay on average. (In this report, the term "family" is used in its broadest meaning to include individuals, married couples, and parents with children.)

- Taxes on middle-income families have been declining in recent years, not rising as Tax Foundation reports would lead the public to believe.

Tax Foundation Methodology Paints Misleading Picture

Why is there this contradiction between the Tax Foundation and these two much more authoritative sources of tax data? It is because the picture the Tax Foundation presents — that the tax burden is high and has been rising — is inaccurate when applied to typical or average middle-income families. The Tax Foundation computes what it describes as the percentage of income that Americans, on average, pay in taxes and converts this to the portion of the year that Americans have to work to pay their tax bills. This methodology draws a misleading picture; it substantially exaggerates the amount of taxes that middle-income families pay.

Under the method the Tax Foundation uses, increased tax payments solely by high-income taxpayers increase the taxes that "Americans" pay and thereby advances "Tax Freedom Day" to later in the year. This methodology can produce particularly sharp distortions when large increases in capital gains income or in executive salaries cause high-income people to have strong income growth and therefore to pay more in taxes.

The impact of rising capital gains income and executive salaries and bonuses on the growth in revenues in recent years is widely understood. For example, White House economic adviser Lawrence Lindsey acknowledged this point in testimony before Congress in January 1999. He stated: "A disproportionate share of this extra revenue is coming from upper income taxpayers through higher income tax payments. The likely reason for these payments is the booming stock market. The extra revenue is in part due to higher capital gains realizations due to higher stock prices, but is probably even more dependent upon higher bonuses being paid to upper bracket individuals."(1) The Congressional Budget Office has reached a similar conclusion, finding that the increase in capital gains taxes alone accounted for roughly 30 percent of the increase in tax collections relative to gross domestic product between 1994 and 1998. Despite the recent downturn in the market, CBO is projecting an increase in capital gains receipts in 2001.

The Tax Foundation's methodology also errs in important ways. Of particular concern, the Tax Foundation fails to count some of the income on which the taxes that it counts are levied. It counts capital gains tax payments as taxes but fails to count as income the capital gains income on which these taxes are levied. In addition, the Tax Foundation counts as taxes various items that clearly are not taxes, such as the optional premiums that elderly and disabled people elect to pay for physicians' coverage under Medicare. The methodological errors that the Tax Foundation commits all distort its figures in the same direction — they all make taxes look higher than they actually are.

Tax Foundation Exaggerates Federal Tax Burden on Middle-Income Families

The federal tax burden the Tax Foundation says families pay on average is about 25 percent larger than the federal tax burden that CBO estimates families in the middle of the income spectrum bear and about 40 percent larger than the federal tax burden the Joint Tax Committee estimates these families bear.

| Federal | 1995 | 1999 | 2001 |

| CBO | 19.7% | 18.9% | — |

| JCT | 18.3% | — | 16.8% |

| State and Local | |||

| Average Taxes | 10.3% | 10.3% | 10.3% |

| Total Taxes | |||

| CBO | 30.0% | 29.2% | — |

| JCT | 28.6% | — |

27.1% |

| Source: Congressional Budget Office, May 1998; Joint Committee on Taxation, November 16, 1995 and February 21, 2001 for incomes between $30,000 and $50,000; U.S. Department of Commerce, Bureau of Economic Analysis, March 2000, for average state and local taxes. | |||

In its 2001 Tax Freedom Day report, the Tax Foundation estimated that families on average pay about 23.6 percent of their income in federal taxes, including income tax, payroll tax, and other taxes. By contrast, the Congressional Budget Office estimates that families in the middle of the income scale paid 18.9 percent of income in federal taxes in 1999 (the latest year for which CBO data are available), while the Joint Committee on Taxation's estimate is 16.8 percent for families making between $30,000 and $50,000 in 2001.(2) The Tax Foundation's estimates are about one-fourth to two-fifths higher than the estimates of these official institutions.

Misleading Word-Play? Both the Center on Budget and Policy Priorities and a number of prominent economists such as William G. Gale of the Brookings Institution have criticized the Tax Foundation's methods as providing a misleading picture of the taxes that middle-income families pay. As noted elsewhere in this report, the average tax burden figure the Tax Foundation derives — and on which Tax Freedom Day is based — is substantially higher than the tax burden that families in the middle of the income scale pay. This is in part because the Tax Foundation's method effectively ascribes to middle-income families certain types of taxes and tax rates that apply primarily or solely to upper-income taxpayers. Nevertheless, the Tax Foundation persists in describing its measure as the tax burden the average American pays. The front page of its 2001 report states: "Tax Freedom Day illustrates that the average American taxpayer is shouldering a heavier tax burden than he ever has before." In other places, the Tax Foundation describes its measure as the tax burden on "Americans" or "the nation's taxpayers." Nevertheless, many pundits and politicians misinterpret the Tax Foundation's reports to reflect how tax burdens have changed for a large portion of American families. The Tax Foundation material essentially invites this misinterpretation. When it says that Americans must work until May 3 or some such date to pay their taxes, the implication that most people would draw is that large numbers of Americans must work until that day to pay their tax bills, not just the well-off. Yet Joint Tax Committee data show that the average tax burden of Americans, as the Tax Foundation computes it, exceeds the tax burden not only of middle-income families (those with incomes between $30,000 and $50,000) but also of families with higher incomes (in the $75,000 to $100,000 range). The Tax Foundation releases do not help readers understand that under our progressive tax system, that the "average" tax bill is much higher than what a middle-income family pays. |

The federal tax burden posited by the Tax Foundation is not only higher than what CBO and the Joint Tax Committee estimate middle-income families pay but is also slightly higher than what the Joint Tax Committee estimates that families with incomes between $75,000 and $100,000 pay. The Joint Tax Committee estimates that families in this income range will pay 21.8 percent of income in federal taxes in 2001. In its 2001 report, the Tax Foundation claimed that Americans on average pay about 23.6 percent.

Using Averages Exaggerates Middle-Income Tax Burden

The Tax Foundation's use of averages substantially exaggerates middle-income tax bills. In contending Americans must, on average, work until May to pay taxes, the Foundation computes average tax burdens. It takes what it says is the total amount paid in federal, state, and local taxes and simply divides this amount by the Foundation's estimate of the total amount of income in the nation. The result is the percentage of income the Tax Foundation pictures Americans as paying, on average, in taxes. The Foundation then converts this into the percentage of the year Americans must work to satisfy their tax obligations. There are fundamental problems with this approach.

The federal personal income tax is a progressive tax. The typical middle-income family is in the 15 percent federal income tax bracket. High-income families are in brackets with marginal rates more than twice that high and pay substantially higher percentages of income in federal income tax than middle-income families do. The tax burden figure the Tax Foundation computes by dividing total taxes by total income is misleading as an indication of the taxes that middle-income Americans pay.

The problem of using the Tax Foundation's approach is easily seen. Suppose four families with $25,000 incomes each pay $1,250 in income tax — or five percent of their income — while one wealthy family with $500,000 in income pays $125,000 in income tax, or 25 percent of its income. Under the Tax Foundation approach, these five families pay 22 percent, on average, of their income in federal income taxes. (Total tax payments of $130,000 divided by total income of $600,000 equals 22 percent.)

But the 22 percent figure is misleading. The four moderate-income families pay five percent of their income in income tax, not 22 percent. Using averages in the manner the Tax Foundation does when talking about tax burdens produces skewed results; it essentially ascribes tax rates to the average person that only taxpayers at considerably higher income levels pay.

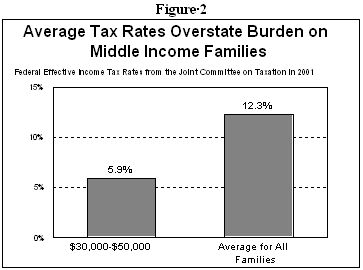

Figure 2

shows the extent to which the average income tax rate is higher than the income tax rate

paid by middle-income families. The Joint Tax Committee estimates that middle-income

families (those in the $30,000 to $50,000 range) pay 5.9 percent of their incomes in

federal income taxes. The average income tax rate for all income ranges is higher, at 12.3

percent, reflecting how the taxes paid by higher-income families push up the average.

Figure 2

shows the extent to which the average income tax rate is higher than the income tax rate

paid by middle-income families. The Joint Tax Committee estimates that middle-income

families (those in the $30,000 to $50,000 range) pay 5.9 percent of their incomes in

federal income taxes. The average income tax rate for all income ranges is higher, at 12.3

percent, reflecting how the taxes paid by higher-income families push up the average.

The Tax Foundation's averaging approach is flawed in the same regard with respect to various taxes in addition to income taxes. For example, the Tax Foundation method assumes that middle-class families pay the same percentage of income in estate taxes as a family with a multi-million dollar income. But estate taxes are paid on only the largest one to two percent of estates; all smaller estates are exempt. The Treasury Department estimates that 99 percent of estate taxes are paid on the estates of people who were in the highest 20 percent of the income distribution around the time of their death.

This holds true for corporate income taxes, as well, which most economists (including those at CBO) believe are primarily passed through to the owners of capital assets. The Tax Foundation's averaging method effectively assumes that typical middle-class families pay the same percentage of income in corporate income as wealthy investors and stockholders. That clearly is not correct.

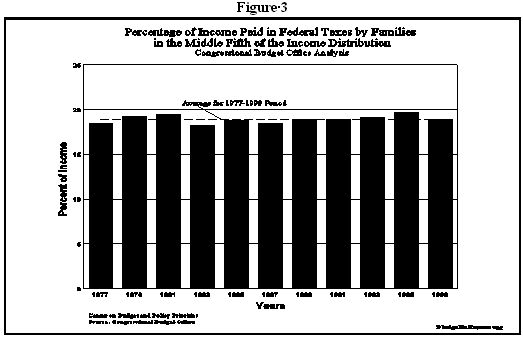

Middle-Income Tax Burden Declining in Recent Years

Federal taxes have been declining for families in the middle of the income spectrum. The Treasury Department has calculated for each year going back several decades the federal income and payroll taxes paid by a married couple with two children that earns the median income. In 1999, this family paid a smaller percentage of its income in federal income taxes than in any year since 1965. Even when payroll taxes are added in, the family is found to have paid a smaller percentage of its income in federal income and payroll taxes in 1999 than in any year since 1978.(3)

The Tax Foundation itself acknowledged this point in a February 1998 release that received little coverage, where it acknowledged that "...federal taxes as a percent of income will be lower on the median single- and dual-income families in 1998 than two decades ago,...even without the 1997 Tax Relief Act."(4) In a more recent report released last year, the Tax Foundation stated that the tax burden on the median income two-earner family peaked in 1996 and has dropped since then.(5)

Nor have taxes been rising at the state and local level. Commerce Department data show that state and local taxes amounted to 10.3 percent of Net National Product in 2000. This Commerce Department measure of state and local taxes has been remarkably stable over time; it was at about the same level in 2000 and throughout the 1990s as it was in 1977.(6)

Federal Revenues Rising as Share of Economy Do Not Reflect Increased Burden for Middle-Income Families

The Tax Foundation's methodology misleadingly portrays the increase in federal revenue as a share of the economy in recent years as representing a rise in the average family's tax burden. The increase in revenue as a share of the economy largely reflects the increased taxes collected from high-income individuals as a result of substantial increases in their capital gains income and salaries and bonuses. It does not reflect an increase in ordinary families' tax burdens.

In 1998, former CBO director June O'Neill testified that tax receipts have risen in recent years as a share of the Gross Domestic Product "mainly because realizations of capital gains were unusually high and because a larger share of income was earned by people at the top of the income ladder, who are taxed at higher rates."(7)

Federal Reserve Board Chair Alan Greenspan has made the same point. He testified in January 1999 that "...we have had a very significant rise in individual tax receipts which unquestionably are reflective of the very large capital gains; and secondarily, the impact of rising stock prices on other types of income."(8)

Tax Levels versus Expenditures on Food, Shelter and Housing Tax Foundation reports often state that families must pay more in taxes than they pay for food, clothing, and shelter combined. This Tax Foundation claim further illustrates the problems with using figures on total tax payments in the nation, total payments for food, and the like. If the statement that total tax payments exceed total expenditures for food, clothing and housing were accurate, that would tell us little about the relationship between taxes and spending for families in the middle of the income scale. It is no doubt true that upper-income families pay more in taxes than they do for basic necessities. At the same time, it also is true that low- and moderate-income families pay less in taxes than they spend for basic necessities; necessities consume most of their income. The precise family income level at which taxes typically exceed expenditures for food, clothing and housing is unclear. The Foundation's report does not help to answer that question. Furthermore, while Americans spend a smaller proportion of their incomes on food, clothing, and housing than they used to, this is not because they are paying more in taxes. Rather, it is because the share of after-tax expenditures devoted to food, shelter, and clothing has shrunk significantly, while the share devoted to costs for items such as health care has risen. In 1970, some 44 percent of after-tax expenditures went for food, clothing and shelter. That figure has declined to about 33 percent in 2000. A drop in the share of expenditures going for food accounts for most of the decline. |

A more formal analysis of the increase in taxes as a percentage of GDP was published by the Congressional Budget Office in January 2001. It found that between 1994 and 1998, capital gains realizations nearly tripled. The increase in capital gains taxes alone accounted for roughly 30 percent of the increase in tax collections relative to GDP. CBO also reported that a significant share of the remaining increase could be attributed to income growth at the top of the income distribution. (9)

A Congressional Research Service study, based on Joint Committee on Taxation data for 1999, finds that three-quarters of all capital gains taxes are paid by the 1.8 percent taxpayers with incomes exceeding $200,000. The bottom third of taxpayers pay almost no capital gains taxes. The middle third of taxpayers pay about one percent of these taxes.(10)

Recent IRS data also show that the rapid increase in incomes among the top one percent of taxpayers — at a pace much faster than among the rest of the population — is the primary reason that the top one percent of the population pays a larger share of the income taxes over the past decade. Approximately two-thirds of the increase in the share of income taxes paid by the top one percent of tax filers that occurred between 1989 and 1998 reflected the increased concentration of income at the top of the income scale rather than higher tax rates.(11)

These developments have little if any effect on families in the middle of the income scale. Nevertheless, the mistaken notion that the tax burdens of middle-income families have risen is the conclusion that most policymakers and pundits who cite the Tax Foundation's work draw from the Tax Foundation reports. The Tax Foundation's "Tax Freedom Day" methodology invites this misinterpretation by treating some of the increased taxes that high-income taxpayers pay as though those taxes were paid by the average taxpayer. This makes it appear as though middle-class families have to work longer to pay their taxes than they actually do.

Other Flaws in Tax Foundation Methodology

The Tax Foundation's methodology contains other shortcomings that make taxes look larger as a percentage of income than they are. In its report, the Tax Foundation counts as taxes items that are not taxes. These include: optional Medicare premiums that older Americans pay if they wish to receive coverage for physician's services under Medicare; intra-governmental transfers that are solely bookkeeping devices and not taxes; and rental payments that individuals or businesses pay to state or local governments to rent property those governments own.

Furthermore, the Tax Foundation methodology fails to count all income. The methodology counts capital gains taxes as part of the taxes people pay, but it fails to count as part of people's income the capital gains income on which these taxes are levied. Counting taxes while failing to count the income on which the taxes are paid makes taxes appear larger as a percentage of income than they actually are. In addition, in a period such as the present when capital gains income — and hence taxes on such income — have risen rapidly, the Tax Foundation procedure makes even average tax burdens appear to have grown faster than is the case.

Tax Foundation State-by-State Data Also Are Flawed The Tax Foundation's report in recent years has also included a list of the dates it says represent "Tax Freedom Day" for each state. These dates reflect the Foundation's estimate of the average tax rate in each state. The serious flaws that mar the Tax Foundation's estimates of tax burdens nationally also plague its state-by-state estimates.

|

Burden of Federal Individual Income Taxes Small for Middle-Income Families

Federal individual income taxes represent a small portion of the total tax burden. The Tax Foundation numbers frequently are used by those who argue either that the federal income tax code should be replaced with a flat tax or consumption tax or that large income tax cuts should be the nation's top budget priority. The argument is that federal income tax burdens on middle-class families have exploded and reached crushing levels. The Tax Foundation's release of its study around April 15, the income tax filing date, may lead people to think federal income taxes are the main cause of the high tax burdens that the Tax Foundation pictures the average family as facing.

In fact, the Joint Committee on Taxation estimates that families in the middle of the income spectrum will pay just 5.9 percent of income in federal individual income tax in 2001. In the Tax Foundation's terms, that means it took only until January 21 for middle-income families to pay their federal income taxes. The Joint Tax Committee estimates show that three of every four families are paying less than 10 percent of their incomes in federal individual income taxes.

End Notes:

1. Lawrence B. Lindsey, Federal Tax Policy, testimony before the Senate Budget Committee, January 20, 1999.

2. The Congressional Budget Office divides families into five equal groups (i.e., quintiles). The middle quintile, therefore, reflects families from the 40th percentile to the 60th percentile of income. This group had an average income of $39,000 in 1999. The Joint Tax Committee divides families based on income ranges. The $30,000 to $50,000 range used in this analysis reflects the 43rd percentile to the 64th percentile. Although reflecting slightly higher incomes than the middle quintile, it is the best approximation of the "middle" in the Joint Tax Committee figures. The federal taxes that the CBO analysis includes are individual income taxes, employer and employee shares of payroll taxes, excise taxes, and corporate income taxes. The federal taxes the JCT analysis includes are individual income taxes (including the outlay portion of the EITC) employer and employee shares of payroll taxes, and excise taxes.

3. Department of the Treasury, Office of Tax Analysis, Average and Marginal Federal Income, Social Security and Medicare, and Combined Tax Rates for Four-Person Families at the Same Relative Positions in the Income Distribution, 1955-1999, January 15, 1998.

4. Tax Foundation, Family Tax Burdens 20 Years Later, Revisited, February 5, 1998.

5. Claire M. Hintz, Tax Burdens on the Median American Family, Tax Foundation Special Report No. 96. March 2000.

6. This measure represents an average state and local tax rate for taxpayers of all income levels. Data are not available on the state and local tax burdens of typical middle-income families.

7. June E. O'Neill, The Economic and Budget Outlook: Fiscal Years 1999-2008, Testimony before the Senate Budget Committee, January 28, 1998.

8. Testimony before the Senate Budget Committee, January 28, 1999.

9. Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2002-2011, January 2001, pp. 54-61. CBO notes that most of the increase occurred before the cut in capital gains tax rates in 1997.

10. Jane G. Gravelle, Capital Gains Taxes: Distributional Effects, Congressional Research Service, September 24, 1999.

11. IRS data show that, from 1989 to 1998, the share of income taxes paid by the top one percent of tax filers rose from 25.2 percent to 34.8 percent. If the top one percent had paid the same percentage of its income in income taxes in 1998 as in 1989, it would have paid 31.4 percent of all income taxes in 1998. In other words, if the average income tax burden of the top one percent of tax filers had remained the same, this group's share of all income taxes would have risen from 25.2 percent in 1989 to 31.4 percent in 1998, simply because of the increased share of the national income it received. The increasing concentration of income thus accounted for about two-thirds of the increase that occurred in the share of income taxes paid by the top one percent.