ADMINISTRATION TAX-CUT RHETORIC AND SMALL BUSINESSES

by Joel Friedman

| PDF of this analysis |

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

The Bush Administration has consistently asserted that its tax cuts, and especially the reduction in the top income tax rate and repeal of the estate tax, are of great value to small businesses. These assertions have been at the heart of both the Administration’s claims regarding the virtues of its tax cuts and its calls to make the tax cuts permanent.

An examination of the relevant data demonstrates, however, that the Administration’s statements seriously exaggerate the benefits of its tax cuts — and especially of the top-rate reduction and estate tax repeal — to the vast majority of small businesses. Claims that the top-rate reduction and estate tax repeal are of substantial benefit to small-business enterprises hold true primarily for a small, rather elite group of businesses — those whose owners have very high incomes and have accumulated significant wealth. For the overwhelming majority of households with small-business income — about 99 percent of them — the reduction in the top income tax rate and the repeal of the estate tax offer no benefits at all.

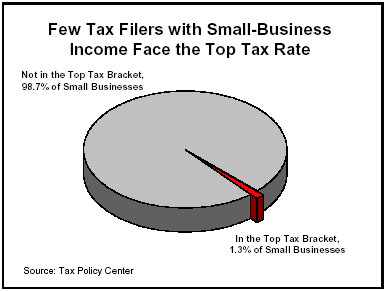

Top Rate Reduction Affects Very Small Number of Small Businesses

The top income tax rate was reduced to 35 percent in 2003, and will return to 39.6 percent after 2010, if the tax-cut legislation is allowed to expire. The Administration argues that making the top-rate reduction permanent is vital for small business. It says that a large share of those who face the top rate are people with small-business income, a group the Administration often refers to as “small-business owners.”

Analysis by the highly respected

-

The small number of tax filers with small-business

income who do face the top rate are an elite group.

The

-

Moreover, these

Treasury’s broad definition captures millions of tax filers, many with very high incomes, whose business income has little to do with the popular image of a small business. Under this definition, wealthy doctors and lawyers who organize their practices as partnerships are considered small-business owners, as are CEOs receiving fees for sitting on corporate boards. The definition also includes substantial numbers of wealthy investors who simply have “passive” investments in a business and have little or nothing to do with its day-to-day operations.

Miniscule Number of Small Businesses Affected

By Estate

The story is similar with regard to the estate tax. Repeal of that tax is slated to be in place for one year — 2010 — and then to expire. The Administration argues that making estate-tax repeal permanent is essential for small businesses and farms, because estates with small businesses or farms otherwise will face the prospect of having to liquidate the enterprise to pay the estate tax.

The

-

Only 340 estates nationwide in which small

business or farm assets represent a majority of the estate will

owe any estate tax in 2004, the

- Moreover, the Tax Policy Center found that by 2009, when estates worth up to $3.5 million for an individual and $7 million for a couple will be exempt from the tax, only 40 estates in the nation in which small business or farm assets represent a majority of the estate will face any estate tax. In 2009, an average of only one such small business or farm per state will be subject to the tax. All other estates with small business or farm assets will be exempt.

- Even when estates with larger businesses or farms are included — that is, businesses or farms valued at over $5 million — the number of estates subject to the estate tax in which the majority of the estate consists of business or farm assets remains very small. In 2009, only 170 such estates nationally will owe any estate tax.

Only this extraordinarily small number of small businesses and farms face any prospect of being liquidated to pay the estate tax. Accordingly, despite the high cost of estate tax repeal to the Treasury, only a tiny number of small businesses and farms will gain protection from the risk of liquidation when the large estate-tax exemptions that will be in place in 2009 give way to repeal of the estate tax in 2010.

The Tax Cuts for “Small Businesses” Are Flowing Primarily to Those With High Incomes

If the reduction in the top rate and repeal of the estate tax do not affect the overwhelming majority of small businesses, the question arises as to whether the overall package of tax cuts enacted since 2001 offers something special to a wide range of small businesses. Artfully presented statements by the Administration and other tax-cut proponents leave that impression.[1]

In fact, the tax cuts essentially affect small

businesses in the same way that they affect the population as a

whole. As studies by the Congressional

Who Is a “Small-Business Owner”?The potency of the term “small business” lies in the images it evokes in the public imagination. Typically, it brings to mind risk-taking entrepreneurs who are involved in the hands-on management of their small firms. To some people, it calls to mind the corner grocery store or the local auto mechanic. To others, it reflects a start-up firm, such as a new business developing a new type of software. Yet the Treasury Department’s definition of small-business owner — a person or couple who files an individual income tax return that includes any income (or loss) from a sole proprietorship, farm proprietorship, partnership, S corporation, or rental income — includes large numbers of tax filers who are not hands-on entrepreneurs. In general, the expansive Treasury definition suffers from two basic problems: it includes businesses that are not small; and it includes wealthy individuals who are passive investors and have nothing to do with operating the business in question (and may have never set foot in it). What does “small” mean? As the Joint Committee on Taxation has noted, “while many small businesses are arranged as a sole proprietorship, a partnership, or an S corporation, not all of the businesses organized in those forms are small…”* Using IRS data from 2000, the Joint Tax Committee showed that the Treasury definition of “small business” included 650,000 businesses with gross receipts of over $1 million and 75,000 companies with gross receipts of over $10 million. Businesses with gross receipts of more than $10 million accounted for two-thirds of the gross receipts of all partnerships and S corporations. What makes someone a “small-business owner”? The Treasury definition includes many individuals who clearly do not meet the popular image of a small-business owner. For instance, the Treasury definition includes people who passively invest in a business and have nothing to do with its day-to-day operations. According to the Tax Policy Center, passive income from partnerships and S corporations represents some or all of the small-business income of 2.9 million tax filers termed “small-business owners” under the Treasury definition. For 850,000 of these filers, all of their “business income” comes in this passive form. This is of particular note because the prevalence of passive business income increases at higher income levels. Passive investment income constitutes all or part of the business income of about 35 percent of the “small-business owners” with income above $200,000 and 58 percent of the “small-business owners” with incomes over $1 million. The Treasury definition also counts as small-business income the fees that CEOs are paid for sitting on corporate boards, as well as honoraria that journalists receive for giving speeches. This turns a number of corporate CEOs and journalists employed by large media corporations into “small-business owners.” Doctors and lawyers who organize their practices as sole proprietorships, partnerships, or S corporations are considered small-business owners as well, under this definition. Indeed, the President and Vice President are considered “small-business owners” under this definition. Counting as “small-business owners” large numbers of people whose business income comes from firms that cannot be categorized as small, who are merely passive investors, or who are corporate executives receiving fees for sitting on corporate boards has a distorting effect. It inflates the tax-cut benefits that are said to go to small businesses. These anomalies are especially prevalent with regard to S corporations and partnerships, since the income from those entities is highly concentrated among high-income individuals. IRS data show that in 2001, about 40 percent of all S corporations and partnership income was earned by “small-business owners” with incomes of more than $1 million. These anomalies in the data should make one highly skeptical of claims advanced by policymakers or lobbyists who seek to promote various tax cuts on the basis of the tax cuts’ purported value to “small businesses” or “small-business owners.” * Joint Committee on Taxation, “Background and Proposals Relating to S Corporations,” JCX-62-03, June 19, 2003. |

Most households with small-business income, however,

do not have high incomes. The

A related

- Tax filers with

small-business income whose total income exceeds $1 million

will receive an average tax cut of over $130,000 in 2004, the

- In addition, households with small-business income whose total income exceeds $200,000 — a group that represents eight percent of all households with small-business income — will receive 51 percent of the tax cuts going to people with small-business income.

- By contrast, households with small-business income whose total income is less than $75,000 — a group that represents 62 percent of all households with small-business income — will receive only 16 percent of the tax cuts going to households with small-business income.

- Similarly, households with small-business income whose total incomes fall below $100,000 constitute three-quarters of the households with small-business income but receive one-quarter of the tax-cut benefits going to such households.

This analysis

by the

|

Cash Income |

Returns of “small-business owners” |

Tax cuts going to “small-business owners” |

Percent change in after-tax income |

||

|

Number |

Percent of total |

Percent of total |

Dollar amount |

||

|

Less than $30,000 |

9,404,000 |

28.6% |

2.8% |

-$301 |

2.2% |

|

$30,000 - $50,000 |

5,277,000 |

16.1% |

5.1% |

-978 |

2.9% |

|

$50,000 - $75,000 |

5,702,000 |

17.4% |

8.3% |

-1,465 |

2.9% |

|

$75,000 - $100,000 |

3,833,000 |

11.7% |

9.1% |

-2,376 |

3.5% |

|

$100,000 - $200,000 |

5,588,000 |

17.0% |

23.0% |

-4,133 |

4.0% |

|

$200,000 - $1 million |

2,309,000 |

7.0% |

24.5% |

-10,670 |

4.1% |

|

Over $1 million |

208,000 |

0.6% |

26.9% |

-130,111 |

6.6% |

|

All |

32,845,000 |

100.0% |

100.0% |

-3,058 |

4.2% |

|

Addendum |

|

|

|

|

|

|

“small-business owners” who pay at the top rate |

436,000 |

1.3% |

28.4% |

-65,427 |

6.8% |

|

*Using Treasury Department

definition of “small-business owner” (see box page 4). Source: Urban-Brookings Tax Policy Center; returns with negative income are not included in the lowest income category but are included in the totals. |

|||||

Once the cost of paying for the tax cuts is taken into account,

only small-business owners with high incomes are likely to end up

better off as a result of the tax cuts. The disproportionately

large tax cuts that high-income households are receiving are

likely to more than offset whatever costs they ultimately bear to

help defray the costs of the tax cuts. But for small-business

owners who do not have high incomes, the opposite is likely to be

the case. Another

The Tax Cuts and the Economy

The Administration emphasizes the benefits of its tax cuts for small businesses in making the case that the tax cuts will boost long-term economic and job growth. The tax cuts are said to be a great boon for small businesses generally, and small businesses are said to be the engine of job growth. This linkage is used to advance the claim that making the tax cuts permanent is essential for job creation.

Claims about the positive

long-term effects of the tax cuts on the economy are sharply at

odds, however, with a growing array of studies from such

respected institutions and analysts as the Joint Committee on

In particular, studies by CBO and the Joint Committee on

Furthermore, if the tax

cuts are made permanent, they may do harm over the long term.

The federal government is on an unsustainable fiscal course, with

hefty deficits extending as far as the eye can see. Making the

tax cuts permanent would further enlarge these deficits. In a

comprehensive new study of the effects of budget deficits on the

economy, Brookings Institution economists

Conclusion

Small business typically evokes positive images in the public mind, and the Administration has frequently sought to associate its tax cuts with the small-business sector. Yet the benefits that the Administration claims will flow to small businesses as a result of its tax cuts generally, and of the reduction in the top income-tax rate and repeal of the estate tax in particular, are greatly exaggerated. Few small businesses will see any benefit from the reduction in the top rate or estate-tax repeal. Only business owners with high incomes or large accumulations of wealth will benefit from these costly tax changes.

Studies by CBO, the

Finally,

although the Administration often associates its tax cuts with

small businesses and uses that association to support its

assertion that the tax cuts will spur major economic and job

growth, studies by Joint Committee on

End Notes:

[1]

Typically, the Administration and its allies note that a high

percentage of people who face the top rate have

small-business income, creating the impression that many or

most small-business people face the top rate. As noted

above, using the Treasury Department definition of small

business, the

[2]

Congressional

[3]

The

[4] See William Gale, “Small Businesses and Marginal Income Tax Rates,” Tax Notes: Tax Facts Column, April 26, 2004.

[5] CBO, The Economic Outlook, August 2003. In a newer study, CBO examined the potential effects of the President’s 2005 budget proposals, which include making most of the 2001 and 2003 tax cuts permanent, and concluded that they would have an ambiguous effect in the short run and probably lead to slight economic gains from 2010-2014. Claims of large economic gains, however, are not borne out by the study.

[6] William G. Gale and Peter R. Orszag, “Budget Deficits, National Saving, and Interest Rates,” prepared for the Brookings Panel on Economic Activity, September 2004.