|

September 18, 2008

NORTH DAKOTA'S MEASURE 2 IS IMBALANCED

AND WOULD HARM EFFORTS TO SECURE STATE'S ECONOMIC FUTURE

By Nicholas Johnson and Elizabeth Hudgins

North Dakota’s proposed Measure 2, a major change to the state’s income tax that will appear on the November ballot, would be detrimental to the state for three principal reasons:

Measure 2 is risky and short-sighted. Measure 2 would cost the state a very large amount of revenue — some $400 million per biennium, growing indefinitely into the future — that normally goes to K-12 schools, colleges, universities, public safety, health care, and other services. This amount matches or exceeds the entire increase in General Fund revenues that the state is now experiencing as a result of the energy- and commodity-price-induced economic boom. When the current economic boom ends, the loss of such a magnitude of revenue is likely to undermine funding for schools, infrastructure, and public services.

Measure 2 is imbalanced and would prevent broad-based tax changes that could benefit all North Dakota families. The change would affect only income taxes, which are already very low in North Dakota compared to other states. The great majority of the dollars lost to the state would benefit a small number of well-off households; many families would get nothing at all. Measure 2 would do nothing to address other parts of the tax code which are more significant in North Dakota, such as property taxes, sales taxes, and other taxes paid by lower- and middle-income families.

Measure 2 would foreclose efforts to address the state’s real needs. To compete and succeed in the long term, North Dakota — like any other state — needs high-quality schools, strong universities, up-to-date infrastructure, and a good overall quality of life. The increased revenues that the state is realizing due to its current economic boom — estimated at $363 million in the current biennium — could be devoted, in part, to addressing goals like improving teacher training, making college more affordable, supporting small businesses, improving supports for the state’s working families and senior citizens, paying off the state’s unfunded liabilities, reforming the state’s tax code, or some of those items in combination. The surplus is probably not big enough to do all of those things, of course. But by spending almost the entire surplus on a big tax cut, Measure 2 would prevent the state from making any of those investments.

Measure 2 Is Risky and Short-sighted

Measure 2 would enact permanent tax cuts of 50 percent in the personal income tax and 15 percent in the corporate income tax as of January 1, 2009.[1] Although the official cost estimate of Measure 2 has yet to be published, it is reasonable to expect that it will cost the state $420 million in lost revenue in the two-year budget period that begins July 1, 2009 (the 2009-2011 biennium).[2]

This loss of revenue represents 15 percent of the revenue forecast for the upcoming budget period. It equals about half of current state appropriations for K-12 education ($710 million) or nearly all of state appropriations for higher education ($469 million). Over the next few budget periods, the cumulative revenue loss due to Measure 2 will rise to a cost of several billion dollars.

Measure 2 may be perceived as “affordable” on the grounds that, for the moment, North Dakota’s revenues are coming in at a higher rate than expected due to the rare confluence of positive economic conditions in the state — high oil prices, development of new oil fields, high crop prices, and other factors.

But this should be of little comfort. The current elevated level of revenue is unlikely to last forever. Other states have experienced economic booms before, and they typically end in dramatic busts. Consider the post-oil-shock downturns in places like Colorado, Oklahoma, and Texas in the 1980s, for example; or the current housing crisis in once-prosperous states like Arizona and Florida, which has forced those states to enact widespread cutbacks in public services.

Measure 2 would be one of the sharpest changes in taxes enacted by any state in the last several decades. Even considering states that have gradually phased in major tax cuts, as a number of states did during the economic expansion of the 1990s, very few states enacted tax changes as dramatic as would be required by Measure 2.[3]

The danger of such large, sudden tax cuts is illustrated by the experiences of the three states that enacted comparable or larger tax cuts as a share of revenue during the 1990s: Massachusetts, New Jersey, and New York. New York cut taxes by 24 percent during the 1990s, but when its boom ended, it faced some of the nation’s largest budget deficits, saw its bond ratings downgraded, and was forced to raise taxes substantially. New Jersey cut taxes 17 percent in the 1990s, but this led to a major budget crisis that has persisted throughout this decade and required substantial tax increases. Massachusetts’ 17 percent tax cuts in the 1990s boom presaged an economic and fiscal crisis in the 2002-04 period, resulting in significant reductions in public services as well as tax increases.[4] In these three states, some or all of the tax cuts had to be reversed by subsequent tax increases and public services suffered declines.

It is worth noting that Measure 2 would require the tax cuts to remain in place for at least seven years, so North Dakota would not have the ability to reverse course if it finds, as these other states did, that it had overshot the mark on the amount of tax cut that was affordable without devastating public services.[5]

Oil and Gas Revenues Cannot Be Relied Upon to Make Up the Difference

In addition to growing general revenues, North Dakota is realizing higher-than-expected revenues accruing to the state’s oil and gas trust fund. Original estimates were that $146 million would be deposited into this trust fund in the current biennium (2007-2009). This was revised upward in June 2008 to reflect record-high worldwide energy prices, but analysts are still not sure whether the actual level will be $380 million, $614 million, or somewhere in between.

But North Dakota cannot count on being able to transfer that money into the General Fund on an ongoing basis into the future. For one thing, oil and gas revenue is inherently uncertain and cannot justify a permanent tax cut of the magnitude proposed in the ballot measure. If oil prices and/or production were to tumble, the legislature would not be able to undo, or even modify, the income tax under this measure for at least seven years. And even after those seven years were up, it would be politically very difficult for the legislature and governor to undo a measure that the voters had approved.

There is another key reason why oil and gas revenues cannot be assumed to pay for the loss of revenue. Appearing on the November ballot, alongside Measure 2, is Measure 1, which amends the state constitution so that only a small portion of oil trust fund money can be transferred to the General Fund — and even that very small transfer requires a three-fourths vote of the legislature. Even under the most optimistic scenarios of high oil prices and high production volume, this small transfer would be nowhere near enough to pay for the loss of revenue from the income tax cut.[6]

Measure 2 Is Imbalanced In Its Approach to Changing the Tax Code

Measure 2 makes dramatic changes to North Dakota’s personal and corporate income taxes, and does not change any of its other taxes at all. This is a strange approach to tax reform, for at least two reasons: first, income taxes in North Dakota are already very low compared to those in other states; and second, Measure 2 delivers by far the biggest benefits to higher-income individuals.

Measure 2 Addresses the Wrong Tax

Measure 2 targets North Dakota’s income tax, particularly its personal income tax — a tax that is already among the nation’s lowest. Among the 41 states with personal income taxes, North Dakota’s is the very lowest, equaling just 1.3 percent of total income — roughly half the national average. Similarly, for corporate and personal income taxes combined, North Dakota ranks 42nd-highest among the 50 states. [7]

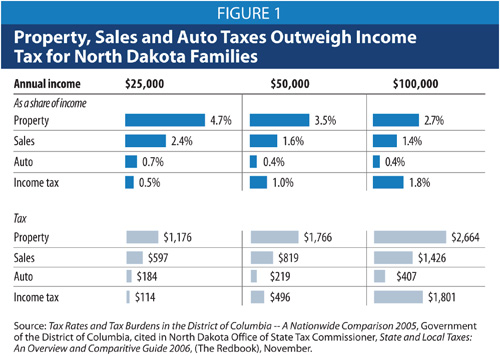

Measured another way — in terms of taxes paid by representative families — North Dakota also ranks low for income tax. Analysis reported by the North Dakota Tax Commissioner — based on a study originally done for the District of Columbia — shows that families with gross family income of $100,000 in North Dakota already rank 41st in income taxes compared to their peers in other states. Compared to nearby states, the income tax owed ($1,801) is less than half that of similar households in Montana ($3,966), Minnesota ($4,227) or Nebraska ($3,808).[8] (South Dakota lacks an income tax, but a family in Sioux Falls pays higher sales and property taxes than a comparable family in Fargo; similarly, a family in Cheyenne, Wyoming, faces higher sales taxes and automobile taxes than the family in Fargo.)

In fact, many North Dakota taxpayers already pay no income taxes at all. These include low-income working families with children whose income tax obligation is eliminated by exemptions and deductions; senior citizens whose income is entirely or mostly derived from Social Security; and farm owners and small-business owners who report net business losses, among others. The Institute on Taxation and Economic Policy estimates that 30 percent of the state’s taxpayers pay no income taxes.[9]

By contrast, virtually all North Dakotans pay sales taxes and property taxes. For most taxpayers it is these taxes — not income taxes — that have the biggest pocketbook impact. The North Dakota Tax Commissioner reports that for sample families with incomes of $25,000 and $50,000, sales tax liability and property tax liability each are larger than income tax liability. For a family with an income of $100,000, property tax liability substantially exceeds income tax liability, and sales tax liability is only slightly lower. (See graph.) One might imagine, therefore, that sales and property taxes — not income taxes — would be the highest priority for tax relief, as has been the case in other states.

Measure 2 Mostly Would Benefit a Few North Dakota Families With High Incomes

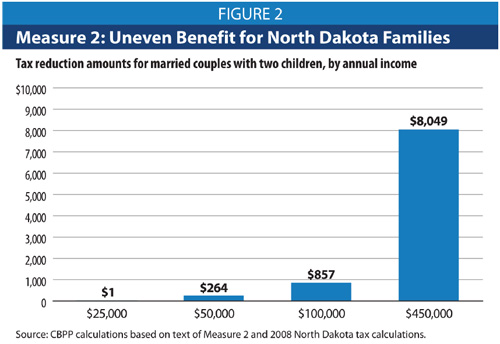

Not only would Measure 2 target for reduction a tax that is not particularly onerous, but it is designed in such a way that a few high-income taxpayers would reap most of the benefits. Under Measure 2, families with modest incomes would experience only very small tax cuts; families with low incomes would receive no benefit at all.

Under Measure 2, the higher a family’s income, the greater the payoff from Measure 2. For example:

- Families without taxable income — for instance, working families with incomes below the federal poverty line, families whose income is offset by farm or business losses, and seniors living on Social Security — get no tax cut at all. As noted above, this represents some 30 percent of North Dakota households.

- A single person with no dependents and annual income of $20,000 could expect a tax cut of no more than $116, or about $2 per week.

- A married couple with two children with total income of $50,000 per year could expect a tax cut of no more than $264 per year (about $5 per week), and less if they have itemized deductions such as a mortgage or property tax payments.[10]

- A similar family with adjusted gross income of $450,000 could expect a tax cut of $8,049 — a benefit 30 times the size of the tax reduction for the family earning $50,000.[11]

The Institute on Taxation and Economic Policy, a Washington, DC-based research organization that has a detailed tax model for each of the 50 states, estimates that more than one-quarter of the benefit from Measure 2 (28 percent) would go to the state’s top 1 percent of taxpaying families — families with an average income of about $807,000. The average tax cut for them would be over $11,000 per year. By contrast, the 60 percent of North Dakota taxpayers with incomes below $52,000 would receive just one-ninth of the benefit (11 percent), averaging about $83. (See Appendix for more details on the ITEP data.)

|

Americans for Prosperity’s Misleading Analysis of

Measure 2’s Impact on Households

In its analysis of Measure 2 dated August 25, Americans for Prosperity purports to describe the impact of Measure 2 on four families with income levels of $25,000, $50,000, $75,000 and $100,000. AFP says these families would receive anywhere from several hundred to several thousand dollars as a result. These figures are somewhat misleading for at least three reasons:

-

AFP implies that an “average family household” earns “$50,000 in taxable income,” and uses this figure to exaggerate what a typical North Dakota family might receive. In fact, the U.S. Census Bureau reports that a typical (or median) North Dakota household earns about $44,708 in total income.

-

The distinction between “taxable” and actual income is important, but is not explained in the AFP analysis. Under federal and North Dakota tax law, “taxable income” refers to total income after exemptions and deductions. Thus taxable income for many taxpayers is a fraction of total income. A casual reader might read the AFP analysis to think that a family with “income” of $25,000 could expect a tax cut of several hundred dollars. In fact, most such families would get less. A married-couple family of four with income of $25,000 in 2008, for instance, is typically eligible for exemptions and deductions of at least $24,900, meaning the family would have taxable income of just $100 — and receive a tax cut under Measure 2 of exactly $1, rather than the $263 shown in the AFP press release.

-

AFP fails to show the tax impact on high-income tax filers. This is important, because as described elsewhere in this analysis, these households receive a large share of the benefit under Measure 2. By excluding high-income families from its analysis, as well as by focusing on taxable income rather than total income, the AFP analysis makes Measure 2 appear more equitable than it actually is.

|

Measure 2 Would Cause North Dakota to Miss Historic Opportunities for New Investments or Tax Reform

Because Measure 2 is such an expensive and poorly targeted measure, it would deprive North Dakota of the opportunity to spend its surplus more wisely. The state’s current surplus is an opportunity to make investments in K-12 education, roads, bridges, health care, and services for families and seniors. These investments could not only improve the quality of life for North Dakotans today but also lay the groundwork for a more economically significant future.

The additional General Fund revenues North Dakota is receiving from the current economic boom are not infinite, but they are substantial. The state should have the opportunity to consider how to allocate its budget surplus among a range of options — including those listed below — that would benefit a broad range of North Dakota families and ensure a strong economic future for the state for decades to come. But Measure 2 would prevent that discussion from even occurring.

Measure 2 would prevent needed improvements to bridges and roads: As North Dakota has experienced an oil boom and increased construction of wind turbines, use of state roads by heavy vehicles has increased, accelerating the need to repair, improve, and build new roads. The North Dakota Department of Transportation says it needs some $256 million per year just to maintain North Dakota roadways in light of these new burdens on roads and rising road construction costs. Major repairs are also needed to the nearly 1,000 bridges in North Dakota that are considered structurally deficient or functionally obsolete, at a potential additional cost of several hundred million dollars.[12] By investing in these improvements now instead of spreading repairs and maintenance over decades, North Dakota could be better poised to deal with the increase in demand on the roads that the oil boom and strong agricultural growth are spurring. Measure 2 would take such investments off the table.

Measure 2 would undermine efforts to create a highly qualified workforce: North Dakota is experiencing an increase in demand for an educated workforce, but the cost of a college education is rising. Instead of cutting income taxes, North Dakota could reduce tuition and fees at state colleges and universities and offer more scholarships. A program of scholarships to all graduating seniors to attend state universities at low cost or even tuition-free for four years could save North Dakota families tens or even hundreds of millions of dollars per year and substantially increase educational attainment. Additional funds could go to colleges and universities to repair and replace buildings. Such opportunities would be forgone under Measure 2.

Measure 2 would sidetrack K-12 education investments: Proven strategies for improving student performance such as expanding early childhood education, increasing teacher training, and expanding student assessments all cost money. But per pupil spending on K-12 schools in North Dakota is 6 percent below the national average. When Wyoming experienced its boom over the last several years, it chose to invest additional state dollars in K-12 education and spends 23 percent more on each student than North Dakota. [13] To match the national average in K-12 education would cost North Dakota roughly an additional $50 million per year; matching Wyoming would cost more. Such new expenditures would be precluded by Measure 2.

Measure 2 would undermine investments in the state’s future: North Dakota faces a number of other fiscal and economic challenges that the current fiscal surplus could be used to address. The state employee pension and retiree health funds are underfunded by about $620 million, meaning that there is not enough money in them to pay for pensions and retiree health benefits that have been promised to state workers; the state could use all or part of the surplus to reduce that debt rather than passing it along to future generations. Also, as recent legislative hearings have highlighted, the state could invest additional resources to address the nursing shortage in rural areas, raise reimbursement rates so that more people have access to dentists, promote wireless coverage across the state, expand health care coverage, or take other steps to improve the quality of life and economic competitiveness of the state and make North Dakota an even more desirable state in which to live. Measure 2 would undercut the ability of the state to make such investments.

Measure 2 would prevent tax changes that could benefit more working families, senior citizens, and small businesses. As noted above, every North Dakota family and business pays sales taxes and property taxes in some form. One could imagine the state using the budget surplus to pay for various types of tax measures: a reduced sales tax rate, increased aid to localities to finance for property tax relief, a tax credit targeted to working families with children, targeted tax cuts for small businesses, or others. By focusing solely on the income tax, Measure 2 would render such possible changes unaffordable.

Conclusion

No state can count on an economic boom or a budget surplus to last forever. The wise fiscal course for North Dakota would be to consider carefully how to invest its current surplus in education, infrastructure, and/or other areas, as well as tax changes that benefit a wide range of families. Measure 2 would short-circuit such consideration and instead pour a very large amount of money into a poorly targeted tax plan. The result would be a lost opportunity for the long-term prosperity, attractiveness, and competitiveness of the state. |