FEDERAL POLICIES ARE WORSENING

MISSOURI’S BUDGET PROBLEMS

By

Nicholas Johnson,

Summary

|

PDF of

analysis Press Release: HTM | PDF |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Federal policies were a major cause of

the severe fiscal crisis

The federal policies that have

contributed to the fiscal crisis in Missouri and other states include tax

cuts that reduce state revenue because of the linkages between federal and

state tax systems, the federal ban on state taxation of purchases made over

the Internet and other preemptions of state taxing authority, “unfunded

mandates” such as the No Child Left Behind education initiative, and the

shifting of prescription drug costs from the federal government to the

states. In 2003 the federal government enacted a temporary program of aid

to states, which provided $376 million to

To cope with the fiscal

crisis of the past four years,

The impact on

-

Some 37,000 Missouri parents with low-paying jobs have lost eligibility for state-subsidized health insurance. Few of these jobs are likely to provide employer-subsidized care, so most of those parents will have to purchase insurance on their own, probably at a cost of thousands of dollars per year. Many of the parents will simply choose to forego insurance, exposing themselves to the risk of large medical bills and perhaps bankruptcy should they become ill.

-

Some 88,000

- Working parents with incomes slightly above the poverty line are no longer eligible for child care subsidies. For a family with income between $21,000 and $24,000, those lost subsidies were worth more than $3,000 per year.

- Cuts in state payments to grandparents providing foster care and to legal immigrants are costing several thousand families $1,500 to $3,500 per year.

- Property owners and renters in roughly one-fifth of the state are paying more in school property taxes, as school districts seek to offset substantial losses of state aid. Although tax rate increases vary, many homeowners are facing tax hikes of $100 or more. Since the state is unlikely to reverse its cuts in education funding soon, these property tax increases may spread even wider.

- Local governments are increasing fees to keep their budgets in balance in the face of lost state aid.

- The draining of budget reserves and the increased use of debt by state and local governments will place added burdens on future taxpayers.

|

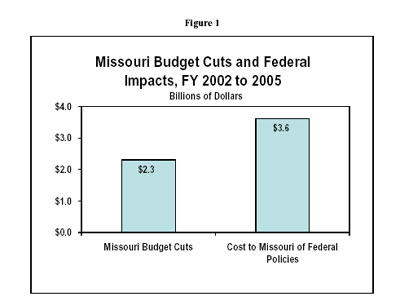

Table 1

The Cost to

|

|

|

FY 2002 |

$710 million |

|

FY 2003 |

$774 million |

|

FY 2004 |

$1.0 billion |

|

FY 2005 (proj.) |

$1.1 billion |

|

Total |

$3.6 billion |

The federal tax cuts enacted in 2001

through 2003 are a major reason the federal government has pursued the

policies that have worsened fiscal problems in

For a small number of very-high-income

For a large number of lower- and middle-income Missourians, however, the benefit of the tax cuts is likely to be outweighed by the harm done by state and local budget cuts. For instance:

-

In 2004, the average

federal tax cut for a

- In 2004, the average

federal tax cut for

-

In 2004, about 28 percent of U.S. taxpayers are receiving a tax cut of $100 or less, according to the Urban-Brookings Tax Policy Center. That is less than the increase in property taxes paid by the owner of a $100,000 home in a typical school district that has raised taxes to compensate for state shortfalls in education funding.

In essence, low- and middle-income Missourians have been paying for very generous federal tax cuts for the highest-income Americans and will continue to do so unless federal policies are changed.

Federal Policies’ Adverse Impacts on the

Federal policies have made

Reducing State Revenue and Preempting State Taxing Authority

Because state tax systems are tied to

the federal tax code in a number of ways, certain provisions of the federal

tax cuts enacted in 2001, 2002, and 2003 have reduced state revenues as well

as federal revenues. For example,

Some 17 states and the

In another example,

Like most states,

Federal policies also prevent

|

Table 2

|

|

|

Ban on taxing Internet purchases |

$1.1 billion |

|

Phaseout of estate tax credit |

$219 million |

|

Bonus depreciation |

$209 million |

|

Ban on taxing Internet access fees |

$83 million |

In the past, an argument against

federal action to enable states to collect sales tax on catalog and Internet

sales has been that as a result of differences among state sales tax

systems, a requirement to collect and remit sales tax would impose too great

a burden on the out-of-state vendors. In the last few years, however,

states have made substantial progress under their “Streamlined Sales Tax

Project” in harmonizing state sales tax systems in ways that will

substantially reduce the burden of collecting these sales taxes.

Donald Bruce and William Fox of the

Beyond the Internet Tax Freedom Act and the E-commerce problem, there are many other examples of federal preemption of state taxing authority, though they tend to be harder to quantify.

[6]Underfunding Programs and Increasing State Costs

Over time, the federal government has placed an assortment of requirements on state and local governments without providing adequate funding. Many of these unfunded mandates, or underfunded obligations, are difficult to quantify, such as new responsibilities imposed on state and local governments in the area of homeland security. (See the box below.) For illustrative purposes, we focus on three areas: the education of disabled children, the Leave No Child Behind law, and new election reform requirements.

- The Individuals with

Disabilities Education Act (IDEA), enacted in 1975 and most recently amended

in 1997, guarantees each disabled child an assessment and an individualized

education plan. When the law was enacted, the federal government promised

it would fund 40 percent of the additional costs that the law requires

states to incur. In

-

The No Child Left Behind

Act requires schools to take a variety of specific steps with respect to the

educational testing of children, including requiring school districts to pay

for tutors and school transfers when schools are not meeting certain

standards. The federal government, however, has not provided the promised

level of support. During the four years of the state fiscal crisis,

|

Underfunding Homeland Security? Ever since the tragedy of September 11, 2001, states and localities have received a host of new federal mandates intended to improve preparedness, strengthen food and agriculture security, upgrade interagency communication, and safeguard the water supply. To help meet the additional costs, the federal government has increased some grants to states and localities and created new grant programs. To date, however, no comprehensive study has been undertaken of whether states and localities have received sufficient federal aid to meet these new homeland security initiatives. In addition, some estimates indicate that substantial new funding will be needed for upgrades in several areas, such as telecommunications, water systems, and airport security. Yet no consensus exists regarding the appropriate division of responsibility among federal, state, and local governments for funding the desired upgrades. In the absence of

data assessing Missouri’s specific homeland security needs, we have

excluded homeland security costs from this analysis. It is clear,

however, that these costs are significant. The city of St. Louis, for

instance, estimates that it spent $4 million in fiscal year 2003 alone

to upgrade security at the city’s airport. According to city officials,

federal funds covered only a portion of these costs; the rest were

financed from city tax dollars.a |

-

The Help America Vote

Act was intended to provide federal guidelines — and resources — for local

precincts to update their voting technologies. Although the federal

government has made a substantial commitment to fund new election equipment

in 2004, minimal funding is expected in 2005, despite the slim likelihood

that all problems will be resolved by then. In

Unfunded mandates are not new, but the

recent confluence of the state fiscal crisis and both new and old mandates

is making life increasingly difficult for

The Federal Role in

Much has been made of the rapid growth

in Medicaid costs, in

Dual eligibles have their hospital

stays paid for by Medicare and some outpatient services and pharmaceuticals

paid for by Medicaid. In recent years, changes in the provision of health

care have led toward shorter hospital stays and a greater reliance on

outpatient services and pharmaceuticals to manage health conditions. This

trend has pushed costs from Medicare to Medicaid, and hence from the federal

government to the states. (While Medicare is entirely federally funded,

Medicaid costs are shared by the federal government and the states;

The effects of this trend are quite

significant: in

The 2003 Medicare drug law will leave states responsible for the large majority of these drug costs even after the new Medicare prescription drug benefit takes effect. Under the drug law, dual eligibles will receive drug coverage through Medicare beginning in 2006. This could produce significant savings for state Medicaid programs. Yet the drug law requires states to return the bulk of these savings to the federal government in perpetuity.

|

Table 3

|

|

|

Educating disabled children |

$858 million |

|

Drug coverage for low-income elderly |

$784 million |

|

No Child Left Behind requirements |

$469 million |

|

Updating voting technologies |

$12 million |

Moreover, states face new,

unreimbursed costs over the next three years for implementing the new

Medicare law. The Congressional Budget Office estimates that these costs

will reach $1.2 billion;

The Fiscal Crisis and Missouri’s Response

The costly federal policies described

above have occurred at a time when

|

Table 4 |

||||||

|

Department |

FY 2002 |

FY 2003 |

FY 2004 |

FY 2005 |

Total |

Department Cuts as % of Total Core Cuts |

|

Elementary & Secondary Education |

$20.1 |

$62.1 |

$58.0 |

$22.6 |

$162.8 |

$11.7% |

|

Higher Education |

9.6 |

99.7 |

42.9 |

1.3 |

153.5 |

11.0% |

|

Social Services |

88.3 |

303.6 |

110.6 |

55.3 |

557.8 |

40.1% |

|

Mental Health |

11.2 |

36.5 |

27.6 |

12.5 |

87.8 |

6.3% |

|

Health |

3.4 |

12.1 |

13.6 |

2.4 |

31.6 |

2.3% |

|

Public Safety |

5.6 |

5.2 |

8.4 |

0.9 |

20.2 |

1.4% |

|

Corrections |

12.8 |

39.1 |

6.4 |

20.8 |

79.0 |

5.7% |

|

All Other State Departments |

56.7 |

129.0 |

75.8 |

35.8 |

297.2 |

21.4% |

|

Total |

$207.8 |

$687.3 |

$343.2 |

$151.6 |

$1,389 |

100.0% |

|

Source:

Note: Some of these cuts may have been restored in later years; the vast majority of the cuts have not been restored, but the exact proportion has not been calculated by the Office of Administration. |

||||||

The state has also shifted some costs to future years and accelerated some revenue collections, preventing even deeper spending cuts now but making it more difficult to balance the budget in later years. For example, the state identified $275 million in capital projects that in previous budgets it had planned to pay for in cash and instead sold bonds to pay for them, using the cash savings to help balance the current budget. These bonds will have to be repaid in the future. In addition, the state used much of the revenues it received from the national tobacco settlement, averaging $150 million per year, to plug general fund holes and fund ongoing health expenditures, leaving less money available to pay for such items as anti-smoking programs than had been expected.

As shown in Table 4, some 40 percent of the core reductions came in the Department of Social Services, which oversees most state programs designed to assist low- and moderate-income families. K-12 education and higher education accounted for another 23 percent of the budget cuts, while mental health and corrections accounted for about 6 percent each.

It is worth noting that even before

these cuts were enacted,

The funding reductions have had substantial impacts on state services such as health care, assistance to people with disabilities, and higher education.

Health Care

Reductions in the state’s Medicaid program, which provides health insurance to low- and moderate income children, families, seniors, and people with disabilities, have largely been implemented by reducing the program’s income ceiling. As many as 96,000 parents, seniors, and people with disabilities are estimated to have lost coverage as a result. Another 30,000 women have lost coverage through cuts in a separate health care program. Specifically:

- An estimated 37,320 working parents lost Medicaid coverage when the state eliminated Medicaid eligibility for working parents with incomes between 75 percent and 100 percent of the poverty line.[10] (For a family of three in 2004, this means that families with incomes between $14,137 and $18,850 lost coverage.) Since most jobs at this wage level do not provide affordable health coverage, it is likely that most of those parents are now uninsured.

- Some 18,322 Missourians lost state-funded health insurance when the state tightened eligibility for several other Medicaid programs for working parents, including a program that provided Medicaid to very low-income non-custodial parents who were current in their child support.

-

Tens of thousands of Missouri seniors and persons with

disabilities have lost access to Medicaid coverage since July 2002, when

the state scaled back a Medicaid “spend-down” program that allowed people

to receive Medicaid if their health care bills otherwise would reduce

their incomes below the poverty line. It is estimated that 40,700

seniors per year who might have received coverage have not be able to

because of those changes.

It is important to note that even as many of those seniors and people with disabilities lost access to Medicaid coverage, others were coming onto the rolls; the total number of seniors and persons with disabilities receiving Medicaid actually has risen from 201,000 in August 2002 to 224,000 in May 2004. This increase results in part from factors like the weakening economy, declining availability of private-market health insurance, and demographic changes. It also results in part from a previously enacted increase in the income eligibility limit that was phasing in over a three-year period. Separating out the effects of these various factors is hard to determine, but it is clear that Missouri’s budget problems caused tens of thousands of seniors and people with disabilities to lose access to coverage for which they otherwise would have qualified.

(Meanwhile, under a separate law that was enacted before the extent of the fiscal crisis was known, the state is expanding Medicaid eligibility for the elderly and disabled from 80 percent of the poverty line to 100 percent over three years. The net effect of these changes remains unclear.)

These Medicaid reductions not only cost tens of thousands of Missourians their eligibility for health coverage, but also reduced reimbursements to health care providers such as doctors and hospitals. For providers that care for large numbers of these newly uninsured, the revenue loss may be quite significant.

Mental Health

Thousands of Missourians with mental disabilities have lost services due to cuts in the state’s Department of Mental Health. Although some of the $87.8 billion in initial cuts were restored in later years, net reductions over the 2002-2005 period totaled about $58.2 million in state general revenue. Nearly 600 jobs have been cut from the department. Although some of the budget cuts were achieved with administrative efficiencies, consolidations and other changes, the cuts also resulted in reductions in the number of people with mental-health needs that could be served at state-operated facilities and at private community facilities that operate with state funding.

[11]Specific cuts have included:

- A $4.7 million reduction in support for alcohol and drug treatment and prevention programs. This has resulted in the loss of substance abuse treatment funding for approximately 4,000 individuals.

-

An $11 million reduction

in funding for provide services for people with mental retardation and

- The state's "family stipend" program — which helped some 800 families to care at home for their children with serious disabilities rather than institutionalizing them — was reduced in fiscal year 2003 and completely eliminated in fiscal year 2004. The average annual stipend under this program was $766 in 2002.

Cuts Affecting At-risk Children

Other state budget cuts have hurt

- Some 2,500 grandparents caring for grandchildren who would otherwise be in the state-supported foster care system had their monthly payments reduced from $188 to only $63. The new level is one-quarter of the reimbursement given to non-relatives who provide foster care.

- The state eliminated cash assistance for legal immigrants under the TANF program, costing some 394 families a monthly payment that averaged $292 per month for a family of three.

- The eligibility ceiling for the state’s Child Care Assistance program, which provides child care subsidies to low-income families so the parents can maintain employment, has not been adjusted for inflation since 2002. As a result, the maximum allowable income for a family of four has declined from 125 percent of the federal poverty line to 112 percent between 2002 and 2005, which means that families of four with incomes of roughly $21,000 to $24,000 are no longer eligible for a child care subsidy. Such subsidies can be worth up to $281 per month or $3,370 per year.

Higher Education

Between 2002 and 2005, the state has made $153 million in spending reductions for its colleges and universities. Various colleges and universities have responded differently; some have scaled back course offerings or cut faculty.

One particularly visible result of the

funding cuts has been dramatic increases in tuition: since 2002, tuition

increases have ranged from $150 to $630 at two-year colleges and from $888

to $1,743 at four-year colleges. The largest increases have occurred at the

state’s largest campuses, those of the

Many of the 88,000 Missourians who attend the state’s public colleges and universities come from middle- and lower-income families and are likely to have difficulty absorbing these tuition increases, especially because state funding for grants and scholarships also has been reduced slightly.

Other Areas

|

Table 5 Core Reductions and Tuition Increases by College and University |

||

|

Institution |

FY 02-05 Core Cut |

Tuition Increase |

|

Community Colleges |

|

|

|

|

$740,000 |

$150 |

|

|

$898,000 |

$390 |

|

|

$1,318,000 |

$180 |

|

|

$5,476,000 |

$450 |

|

|

$864,000 |

$540 |

|

|

$824,000 |

$320 |

|

|

$426,000 |

$330 |

|

|

$1,569,000 |

$630 |

|

|

$714,000 |

$270 |

|

|

$7,874,000 |

$540 |

|

|

$916,000 |

$510 |

|

Three

|

$573,000 |

$390 |

|

|

$1,077,000 |

$360 |

|

|

|

|

|

Four-Year Institutions |

|

|

|

|

$71,714,000 |

$1,743 |

|

|

$9,208,000 |

$1,470 |

|

|

$7,647,000 |

$1,050 |

|

|

$11,459,000 |

$888 |

|

|

$3,260,000 |

$924 |

|

|

$6,974,000 |

$924 |

|

|

$3,221,000 |

$1,245 |

|

|

$2,185,000 |

$1,110 |

|

|

$2,191,000 |

$1,240 |

|

|

$1,678,000 |

$1,210 |

|

Sources:

|

||

The cuts in human services and education have been among the most visible, but other areas of the state budget have been cut substantially as well. For instance, the Department of Public Safety and the Department of Corrections have been reduced by a combined $99.2 million in the last four fiscal years. As a result:

- Some 88 corrections department institutional staff have been eliminated. This has increased the burdens on the correctional officers that remain, forcing them to spend less time supervising inmates.

- Some 31 probation and parole staff have been eliminated. This has reduced community-based coverage of parolees.

- Funding for regional crime labs has been cut nearly in half. This has slowed the pace of police investigations.

The Impact of State Spending Cuts on Local

Services and

The state’s budget

difficulties have also led to reductions in state funding to local

governments.

|

Table 6

Sources of Revenue for

|

|

|

Source of Revenue |

Share of Revenue |

|

State government |

30.6% |

|

Local property tax |

25.4% |

|

Local sales taxes |

12.5% |

|

Other local taxes |

4.2% |

|

Current charges (fees, etc.) |

16.1% |

|

Other revenues |

11.2% |

|

Total |

100.0% |

|

Source:

|

|

The collective impacts of state budget decisions on local governments are difficult to measure because state aid is administered to localities through a number of different departments according to varying formulas. Nevertheless, certain specific cuts and their impacts can be identified.

For example, the state has cut the Juvenile Court Diversion program by $1.6 million. As a result, Circuit Juvenile Courts will receive less state funding, and many of them will no longer be able to provide early intervention services to youth who are not at “imminent risk” of being committed to the custody of the Division of Youth Services. Other reductions in state payments to county juvenile detention centers caused a cut in state reimbursement rates from $17 to $14 per day for children in court custody, resulting in increased funding demands at the local level.

In another example, funding to train volunteer firefighters has been reduced by 39 percent. Some communities diverted local resources to provide trainings, but many trainings were not conducted in fiscal years 2003 and 2004.

In addition, state school district grants for school resource officers (police officers based in schools) were eliminated. Under these grants, the state, the schools, and local law enforcement each paid one-third of the officers’ salaries. Some areas responded to the ending of the grants by eliminating the officers; others diverted local resources to cover the shortfall.

|

Table 7 Underfunding of Foundation Formula |

|||

|

|

Estimated Required Funding |

Actual Funding |

Amount of Underfunding |

|

FY 2001 |

$1.98 billion |

$1.96 billion |

$20 million |

|

FY 2002 |

$2.06 billion |

$2.04 billion |

$21 million |

|

FY 2003 |

$2.22 billion |

$2.09 billion |

$122 million |

|

FY 2004 |

$2.43 billion |

$2.07 billion |

$364 million |

|

FY 2005 |

$2.79 billion |

$2.18 billion |

$610 million |

|

Source: Missouri Department of Elementary and Secondary Education |

|||

Moreover, these cuts have come during

a period in which

In response to the drop in state funding, many school districts have cut spending. According to the Missouri Office of Administration, the state’s elementary and secondary schools have eliminated 2,000 teacher positions and over 500 staff positions in the last two years, resulting in larger class sizes in some areas.

[13] Many districts also have cut back on extracurricular activities, including sports programs and programs for gifted and at-risk students.

Less-wealthy school districts have had

particular difficulty adjusting to the funding cuts. As in many other

states,

Another effect of the cuts in state

aid is higher property taxes. Nearly one in five

These increases range from the very modest to the substantial. The median increase approved in the April election was $.54 per $100 of assessed valuation, which translates into an annual tax increase of $102.60 for the owner of a $100,000 home.

[14] Of course, people who own more expensive property or live in communities with bigger tax hikes would face larger increases in their tax bills. Renters, business owners, owners of vacation property, and others also would pay more than previously.The Impacts of Federal and State Budget Policies on Localities: Two Examples

The experiences of local governments

in two communities —

In the city of

These reductions have come at a particularly inopportune time for the city. City revenues have not fared well as a result of the recession, and the city also faces rising costs for health insurance and workers’ compensation insurance. Most notably, in an example of how new federal obligations can make it more difficult for local governments to cover their expenses, the city was obligated to spend $4 million in fiscal year 2003 on airport security to meet new federal homeland security requirements.

In response to the budget squeeze, the city has increased building permits and other fees by $2 million, delayed infrastructure improvements such as road, bridge, and building construction, and eliminated 731 personnel positions or 9 percent of its workforce, including 36 uniformed police officers.

|

Table 8

Local

|

||||||

|

County |

|

|

|

County |

|

|

|

Andrew |

N Andrew Co |

$.40 |

|

|

Miller

|

$.60 $.27 |

|

|

Tarkio

|

$.75 $.65 |

|

Linn |

Bucklin Marceline |

$.65 $.77 |

|

Bollinger |

Leopold |

$.30 |

|

|

Macon Co |

$.57 |

|

Boone |

Sturgeon |

$.68 |

|

|

|

$.25 |

|

Buchanan |

|

$.63 |

|

|

Middle Grove |

$1.85 |

|

Cass |

Belton |

$.60 |

|

Nodaway |

NE Nodaway |

$.42 $.60 |

|

|

|

$.76 |

|

Ozark |

Dora |

$.60 |

|

Christian |

Nixa |

$.41 |

|

Pettis |

Smithton |

$.60 |

|

Clay |

Excelsior |

$.52 $.15 |

|

Phelps |

St. James |

$.02 |

|

|

Lathrop

|

$.75 $.75 |

|

|

N Platte Co |

$.47 |

|

Cole |

Cole |

$.53 |

|

Polk |

Bolivar |

$.63 |

|

|

Meramec |

$.50 $.70 |

|

|

Moberly |

$.39 |

|

Greene |

Willard Republic |

$.55 $.39 |

|

Ray |

Stet Orrick |

$.55 $.53 |

|

Grundy |

Grundy Co

|

$.45 $1.40 |

|

|

Francis Howell Wentzville

|

$.80 $.89 $.29 $.52 |

|

|

Hickory Co |

$.15 |

|

|

Hazelwood |

$.98 |

|

Holt |

Craig |

$.75 |

|

Saline |

|

$.50 |

|

Howell |

W. Plains Glenwood Junction Hill

|

$.64 $.35 $.30 $.30 |

|

Stone |

Reeds Spg. Blue Eye |

$.20 $.25 |

|

Iron |

Iron Co |

$.37 |

|

Taney |

Bradleyville Forsyth |

$.30 $.57 |

|

|

Lee’s Sum.

|

$.75 $.59 $.45 |

|

|

Warren Co |

$.47 |

|

Jasper |

|

$.67 $.40 |

|

Wright |

Manes |

$.50 |

|

|

Northwest

|

$.60 $.54 $.75 $.50 |

|

|

|

|

|

Johnson |

Chilhowee |

$.25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Missouri Department of Elementary and Secondary Education.

Note:

|

||||||

The St. Louis City Public Schools District, the state’s largest, faces one of the grimmest financial situations of any district, in large part because of the loss of state funding. Between fiscal years 2001 and 2003, state funding for the district declined by $26 million, or nearly 7 percent of the district’s operating budget. During the same period, school expenditures increased by 8.8 percent, almost entirely because of increases in employee health insurance costs and a previously negotiated teacher salary increase. The combination of decreased funding and increased costs resulted in a deficit of $12.3 million at the end of fiscal year 2003; a $38.6 million deficit was expected at the end of June 2004.

[16] The fiscal year 2005 deficit is expected to reach $54.6 million. Although other factors have contributed to the district’s financial problems, the state auditor concluded: “The substantial decrease in state funding was the most significant factor in the district's financial decline.”[17]The impact of these problems has been substantial. Twenty-one of the city’s 113 schools have been closed and their students moved other schools. The city has also frozen hiring, eliminated an extended school year program, and cut other costs. Although some of the reductions in spending may have been appropriate in light of declining enrollment, continuing financial problems may well lead to additional, more painful cuts in the coming years.

City leaders in

In the

The city government did not raise

taxes, but it did levy a $700,000 increase in various fees to keep the

budget in balance. In addition,

What Does It

This analysis has described the fiscal

problems that have been shifted from the federal to the state level and from

the state to local governments and schools. Because state and local

governments also have been facing their own fiscal difficulties, the overall

effect has been a reduction in the level and quality of public services to

In many cases, it is difficult to

quantify the effects of the decline in services. The closing of 21 schools

in

In many other cases, though, the

pocketbook impact of the state and local cutbacks on

- Property owners and renters in roughly one-fifth of the state are paying more in school property taxes, as school districts seek to offset substantial losses of state aid. Although tax rate increases vary, many homeowners are facing tax hikes of $100 or more. Since the state is unlikely to reverse its cuts in education funding soon, these property tax increases may spread even wider.

- Local governments are increasing various fees to keep their budgets in balance in the face of lost state aid.

- Some 37,000 Missouri parents with low-paying jobs have lost eligibility for state-subsidized health insurance. Few of these jobs are likely to provide employer-subsidized care, so most of those parents will have to purchase insurance on their own, probably at a cost of thousands of dollars per year. Many of the parents will simply choose to forego insurance, exposing themselves to the risk of large medical bills and perhaps bankruptcy should they become ill.

- Some 4,000 Missourians lost access to state-funded substance abuse treatment.

-

Some 88,000

-

Some 4,000 Missourians

with mental retardation and

- Working parents with incomes slightly above the poverty line are no longer eligible for child care subsidies. For a family with income between $21,000 and $24,000, those lost subsidies were worth more than $3,000 per year.

- Cuts in state payments to grandparents providing foster care and to legal immigrants are costing several thousand families $1,500 to $3,500 per year.

- The draining of budget reserves and the increased use of debt by state and local governments will place added burdens on future taxpayers.

Contrast with Federal

One reason the federal government has pursued the policies that have worsened states’ fiscal problems is that it has been focused on tax cuts. In other words, in a time when the federal government could have been ameliorating states’ fiscal problems, it instead has been cutting taxes, with most of the tax cuts targeted to high-income households. The federal tax cuts enacted since 2001 have been more costly than any of the other budgetary actions by the federal government; in fact, the tax cuts have been costlier than the combined impact of new spending for homeland security, the war in Iraq, operations in Afghanistan, expanded anti-terrorism efforts, and all domestic spending increases over the last three years.

[18] It is therefore instructive to compare what Missourians have gained from these federal tax cuts to what they have lost from the cuts in state and local services.

For a small number of very-high-income

For a large number of lower- and middle-income Missourians, however, the benefit of the tax cuts is likely to be outweighed by the harm done by state and local budget cuts. For instance:

-

In 2004, the average

federal tax cut for a

-

In 2004, the average

federal tax cut for

-

In 2004, about 28 percent of U.S. tax filers are receiving a tax cut of $100 or less, according to the Urban-Brookings Tax Policy center. That is a smaller amount than the increase in property taxes paid by the owner of a $100,000 home in a typical school district that raised taxes in April 2004, as many districts did.

Moreover, the federal tax cuts are

having a negative long-term impact on

Conclusion

The recent fiscal crisis in

Many of those reductions in services

and increased taxes and fees have quantifiable costs to families, often

hundreds or thousands of dollars per family. Hundreds of thousands of

It is not too late for the federal

government to undo some of the damage. Legislation now pending in Congress

would help states pay new costs associated with implementing the Medicare

prescription drug bill. But new threats — of federal tax pre-emption, for

instance — are emerging as well. If the federal government takes better

account of how its actions affect states, it can avoid some of the costly

impacts on

End Notes:

Nicholas Johnson and Iris J. Lav are with the Center on Budget and Policy Priorities; Amy Blouin is with the Missouri Budget Project. Also contributing to this report were Jennifer Hill, Tom Kruckemeyer, Chris Deason and Denise Strehlow, all of whom are with the Missouri Budget Project. The authors wish to thank numerous staff of Missouri state agencies and local governments who provided data and responded to inquiries. The authors are solely responsible for any errors. State-specific data on the distribution of the federal tax cut come from the microsimulation model developed by the Institute on Taxation and Economic Policy from U.S. Treasury tax data. Estimates provided by the[3] The ban expired at the end of November 2003. As of this writing, Congress continues to debate the form in which it will be extended. Some form of extension is likely, and states and localities are acting as if the ban is still in place.

[4]

One change that would be required by the streamlined sales tax approach

in

[6] For example, federal law prohibits state and local governments from taxing airline and bus tickets purchased for interstate travel. Were states able to apply their sales taxes to such tickets, the revenue gain would be large. Federal law (P.L. 86-272) also prohibits states and localities from imposing a corporate profits tax on an out-of-state corporation if the corporation’s only activity within the state is soliciting orders for physical goods. This allows corporations to have an unlimited number of salespeople in a state at all times, yet remain exempt from tax so long as the salespeople work out of their homes. When P.L. 86-272 was enacted in 1959, it was intended to be temporary. However, it has never been repealed, and over the years it has shielded tremendous amounts of corporate profits from state taxation.

[7] These and other estimates of spending and shortfalls in funding mandates are derived from data compiled by Federal Funds Information to States (FFIS), a joint service of the National Governors Association and the National Conference of State Legislatures that tracks and reports on the fiscal impact of federal budget and policy decisions on state budgets and programs. For details on sources and methodology, see Iris J. Lav and Andrew Brecher, Passing Down the Deficit, Center on Budget and Policy Priorities, May 2004.

[8] National Conference of State Legislatures, The Mandate Monitor,