Conference Agreement Tax Cut Would

Cost

$2.6 Trillion in Second 10 Years

by Iris J.

Lav and Robert Greenstein

The conference agreement tax bill has an official cost of $792 billion over the 10-year period from 2000 through 2009. But its actual cost would likely exceed $792 billion in the first 10 years and would reach approximately $2.6 trillion in the second 10 years, from 2010 through 2019.

The bill's official cost is held to $792 billion in the first 10 years through use of a gimmick. The bill sunsets many of its principal provisions after 2008 — including the reductions in tax rates, the marriage penalty relief, the capital gains rate cut and capital gains indexing, the increase in IRA contribution limits, and repeal of the alternative minimum tax. The official cost estimate assumes that these provisions will not be in effect in 2009.

In fact, as explained below, canceling some of these provisions would be virtually impossible as a practical matter, while sunsetting others — while technically possible — would be extremely difficult politically. If these provisions really ceased to be effective after 2008, the result would be a $54 billion income tax increase in 2009 — larger than the tax increase that occurred in 1991 following the 1990 deficit reduction deal President George Bush negotiated with Congress. (These comparisons adjust costs from different years for inflation.)

If these provisions are enacted, they almost certainly would remain in effect. Furthermore, the only reason the conference agreement sunsets these provisions after 2008 is so that the conferees could stuff a large number of tax cuts from both the Senate and House bills into the conference package and still make it appear on paper as though the bill did not exceed its $792 billion cost limit. Using realistic estimates that do not assume these provisions terminate after 2008, the bill is found to miss its $792 billion target by more than $50 billion.

The conference agreement also sunsets the entire bill after 2009 to avoid triggering a Senate rule under which the conference agreement would need 60 votes to pass the Senate. This sunset, too, should not be taken very seriously. Full sunset of the bill would result in an unprecedented — and unthinkable — single-year tax increase of $180 billion. That would be nearly three times larger than the tax increase that took effect in 1994 following enactment of the 1993 deficit reduction legislation.

How Large is the Cost?

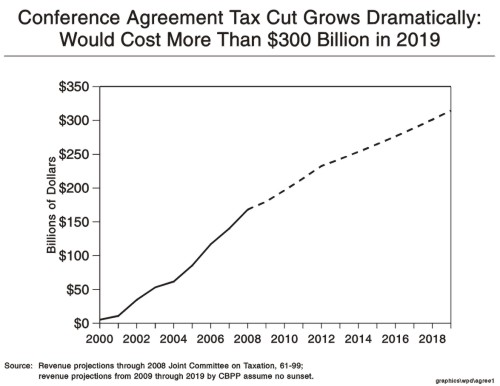

Without the gimmicky sunset provisions, the bill's cost — which mushrooms from $62 billion in 2004 to $117 billion by 2006 to $168 billion by 2008 — would rise to $180 billion in 2009. By contrast, the official estimate shows the cost plummeting from $168 billion in 2008 to $126 billion in 2009.

After the initial 10-year period, the cost of the tax-cut package would explode. Using conservative estimates that are likely to understate the bill's long-term cost, we find:

- The tax cut package would cost approximately $2.6 trillion in the second 10 years, from 2010 through 2019.(1)

- This is more than triple the $792 billion cost officially shown for the first 10 years.

These massive costs in the second 10 years would occur during the same period in which the baby boom generation begins to retire, Social Security and Medicare costs mount, and surpluses both in the Social Security budget and the non-Social Security budget are expected to stop growing each year and begin shrinking.

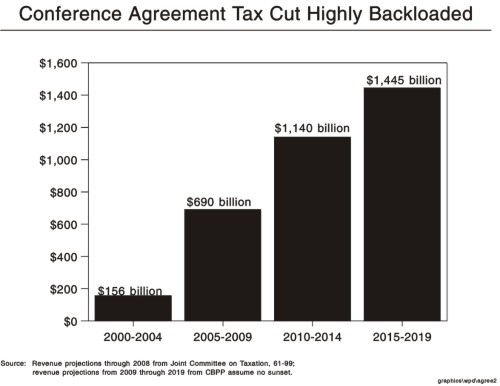

Even under the official estimates, the bill's costs grow explosively through 2008. The Joint Committee on Taxation estimates the bill would cost $156 billion in the first five years from 2000 through 2004, and $636 billion — more than three times as much — in the second five years from 2005 through 2009. The costs are far lower in the first five years than in the second five both because most of the bill's major provisions phase in gradually(2) and because several devices — such as a capital gains "mark to market" mechanism — are used to accelerate into the first five years some billions of dollars in tax payments that otherwise would be made in later years, making the bill's costs look smaller in the first few years.

Moreover, the $636 billion official cost for the second five years understates the likely cost in that period because it assumes the termination of various provisions after 2008, as discussed above. Without the bill's sunset gimmick, the cost is approximately $690 billion in the second five years.

Sunset Provisions

Some may attempt to argue that the large costs in the second ten years will not occur because of the sunsets. The sunset provisions do not mean, however, that the massive costs of the legislation in the second 10 years can be ignored.

Much of the bill's $2.6 trillion cost in the second decade would be unavoidable for practical or political reasons. Should the point of sunset ever be reached, Congress would be all but certain to extend all or most of these costly tax cuts.

- Consider first the sunset after 2008 of a number of the bill's specific tax-cut provisions. Terminating them after 2008 would cause a tax increase of at least $54 billion in 1999. Moreover, full termination of the entire bill would result in tax increase of $180 billion in a single year. A tax increase of that magnitude would be politically very costly for policymakers and also economically unsound.

- Furthermore, as a practical matter, various key tax cuts simply could not be reversed. Capital gains indexing is a good example. Under the capital gains indexing provision in the conference agreement, investors could use a "buy in" mechanism to qualify assets they already hold for the favorable tax treatment that indexing would provide. To qualify, taxpayers would pay taxes on the gain in the value of their assets between the date they purchased the assets and January 1, 2000, the date on which indexing would become effective. (This is sometimes called "mark-to-market," because capital gains tax would be paid based on the market price of the assets on the date that indexing begins. The Joint Committee on Taxation estimates a revenue gain of $15.5 billion in 2001 when these mark-to-market taxes would be paid.) If a taxpayer chose not to "buy in" to indexing, he or she would owe no capital gains taxes on his or her assets until the taxpayer actually sold the assets at some future point. Each taxpayer who chose to use the buy-in — and thus to pay some capital gains taxes now — would be making a financial judgement that the ability to use indexing in the future would be worth more to him or her than continued deferral of taxes on the assets until they are sold. Once taxpayers have made this judgement and accepted the government's offer under which they pay capital gains tax now in return for use of indexing later, the government cannot renege on its part of the bargain. Indexing must remain in place, and the future revenue losses must be absorbed.

- Many of the bill's IRA and pension changes would similarly be locked in and could not be reversed. For example, under the conference agreement, married taxpayers with incomes between $100,000 and $200,000 would be allowed to convert conventional IRAs to Roth IRAs. To make the conversion, they would pay income tax now on the amounts shifted from their conventional IRA accounts to Roth IRAs, rather than paying such taxes when they would withdraw the funds from the IRA accounts in their retirement years. Once this conversion is made, all of the money in these accounts — including all income earned on the funds in the account — would be forever free of tax. Taxpayers who chose to convert conventional IRAs to Roth IRAs essentially would "pay for" a new entitlement to tax-free earnings on these Roth IRA accounts by paying income tax now they otherwise would owe later. Once that bargain is made and these individuals have actually paid the taxes on the funds they have shifted into Roth IRAs, the earnings on the Roth IRAs cannot be taxed. Here, too, the provision can not be reversed. The ongoing revenue losses would be impossible to recoup.

- The repeal of the estate tax also could be exceedingly difficult to reverse, both because some revenue losses would be ongoing beyond the tenth year (estates take a number of years to be settled, and tax payments often are not made until two to four years after a death occurs) and because taxpayers would have relied on the repeal of the estate tax in making financial decisions as they grew older.

The same type of practical problem — that once a particular tax change is made it would be a serious breach of faith for the government to reverse it — does not apply to raising tax rates back up (including raising the 14 percent rate back to 15 percent), reducing the standard deduction for married filers, and otherwise reinstating current marriage penalties. Such changes would, however, likely be seen as middle-class tax increases for which policymakers would be loathe to accept responsibility.

End Notes:

1. Costs for years after 2009 were projected as follows: the 2009 cost is derived by adding back the continuing cost of the provisions that would supposedly end after 2008. For years after 2009, the estimate assumes that the cost of the bill will increase at the same rate that CBO projects GDP will be growing at the end of the 10-year period, a nominal rate of 4.4 percent per year. Additional adjustments are made to reflect full phase-in of the repeal of the estate tax.

2. The phased-in provisions, most of which would not fully effective under the bill until some point between 2006 and 2009, include: elements of the rate cut, the standard deduction increase, marriage penalty relief, the repeal of the individual Alternative Minimum Tax, and the repeal of the estate tax. Indeed, much of the effect of the costly elimination of the estate tax, which would become effective for people who die in 2009, would be felt only after the end of the 10-year period, because there is a time lag between the death of an individual and the settlement of the individual's estate and thus the payment of tax on the estate.