The Disappearing 2001 Surplus:

Tax Cuts, Budget Increases, and the Economy

by Richard Kogan and Robert Greenstein

| PDF of this report If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

When the Bush Administration issued its budget on April 9, 2001, it predicted a budget surplus outside Social Security of $125 billion for fiscal year 2001, which at that time was six months complete.(1) Now, four months later, the predicted $125 billion surplus has practically disappeared. How did this happen? The quick answer is that the recently enacted tax-cut reduced revenues by $74 billion in 2001 and the economy slowed significantly, so that revenue collections fell below predicted levels. (See Table 1.)

Some members of the Administration have attempted to blame the previous Congress and administration for the reduction in the 2001 surplus, pointing out that last fall, Congress increased funding for appropriated (or "discretionary") programs.(2) While true, this is not relevant; the Bush Administration's April prediction of a $125 billion surplus already accounted for all the funding and tax decisions made last fall by the previous Congress. Clearly, the level of spending enacted last fall does not explain why predictions made this April were off base.

Nevertheless, to put the issue of program increases and tax cuts into context, this analysis also examines how the surplus projection for 2001 made by the Congressional Budget Office in July 2000 has changed over the course of the last 13 months. In so doing, the analysis compares the budgetary effects of last fall's appropriations bills with the effects of this spring's tax cuts.

- Thirteen months ago, CBO projected a surplus of $125 billion outside Social Security. (It is coincidental that last July's baseline projection of the 2001 surplus by CBO and this April's estimate of the 2001 surplus by OMB, under the Bush Administration's budget proposals, were both $125 billion.)

- CBO's new budget projections, released on August 28, show that the projected 2001 surplus outside Social Security has turned into a deficit of $9 billion. Some $95 billion of the $134 billion deterioration in the size of the projected surplus is due to legislation enacted last fall or this spring.

- Only 15 percent of that $95 billion was enacted by the previous Congress and previous administration. Some 85 percent was enacted by this Congress and this Administration.

This analysis also examines the historical record of federal spending to ascertain whether program spending surged in 2001 as a consequence of decisions made last fall.(3) The data do not show such a surge.

- In 2001, federal spending dropped to its lowest level as a share of the economy since 1966.

- In 2001, federal spending grew by 0.5 percent after adjusting for inflation, well below the historical average of 2.8 percent (over the 1962-2001 period) and even further below the 3.9 percent growth rate in spending that the Bush Administration has proposed for 2002.

- Looking only at appropriated programs, expenditures grew by 2.8 percent in 2001 after adjusting for inflation. The Bush Administration has proposed a 5.8 percent increase for 2002; the size of the increase the Administration has proposed is primarily driven by the large increases the Administration is seeking in defense spending.

Changes in the 2001 Surplus from April to August

As Table 1 shows, OMB's April projection of a $125 billion surplus for 2001 (excluding Social Security) has disappeared, largely because of the tax cut but also because of the economic slowdown.

What does the economic slowdown signify for the budget in the future? Where will we be after the economic slowdown is over and the economy once again is operating at full capacity? Will the economy resume the torrid pace of the second half of the 1990s, or will the promise of a "new economy" prove to have been too optimistic? The answers to these questions, which are not known at this time, will affect the nation's long-term fiscal condition. (They will not materially affect the immediate budget situation.)

| 2001 surplus predicted by the Administration on April 9, 2001, based on enactment of its proposed budget policies | 125 | |

| Enacted tax rebates and immediate rate cuts (beyond those proposed by the Administration) | -41 | |

| Enacted shift of two weeks of corporate income tax receipts from 2001 to 2002 (included in the tax cut bill) | -33 | |

| Enacted new spending vs. proposed new spending, since April | -4 | |

| Economic and technical reestimates since April (largely caused by the economic slowdown) | -50 | |

| Changes in accounting procedures | +4 | |

| Current OMB estimate of the 2001 surplus | 1 | |

| Source: Joint Committee on Taxation and Congressional Budget Office estimates of the cost of enacted legislation (these estimates differ slightly from OMB's); OMB April and August estimates of surplus. | ||

In previous analyses, we have suggested that the long-term revenue losses the tax cut will generate are too large — that over the long term, the tax cut will not leave enough resources to prepare the nation and the Social Security and Medicare trust funds for the retirement of the baby boomers, while also meeting other needs.(4) If the current economic slowdown proves to be a harbinger of generally slower growth during the coming decade, the budgetary problems over the course of the decade may be hundreds of billions (or even trillions) of dollars larger than previously thought.

Changes in the Projected Surplus from July 2000 to August 2001

Some advocates of the recent tax cut speak of the budget increases enacted by the previous Congress as though they far outweigh the tax cut this Congress approved. An examination of the data shows the opposite is the case.

Costs in 2001

This examination starts with the surplus of $125 billion that CBO projected for 2001 in July 2000, thirteen months ago. It then compares the legislation enacted last fall with the legislation enacted this year, to see which contributed more to the deterioration of the 2001 surplus. It can be seen that the revenue losses from this year's tax cut far exceed the cost of increases in appropriations or entitlement programs enacted last year.

| 2001 surplus projected by CBO, July 2000, assuming there would be no tax changes and that appropriations for 2001 would grow only with inflation | 125 | |

| Legislation enacted last fall: | ||

| 2001 appropriations | -8 | |

| entitlement changes | -4 | |

| tax cuts | -2 | |

| Legislation enacted so far this year: | ||

| tax rebates and immediate rate cuts | -41 | |

| shift of two weeks of corporate income tax receipts from 2001 to 2002 | -33 | |

| 2001 supplemental appropriations | -1 | |

| increase in farm price supports | -6 | |

| Economic and technical reestimates since July 2000 | -39 | |

| 2001 deficit projected by CBO, August 200 | -9 | |

| Source: CBO * The $1 billion surplus shown by OMB (Table 1) includes the net cost of the Postal Service (about $1 billion in 2001). The $9 billion deficit shown by CBO (above) does not include the Postal Service since it is designated by law as an off-budget federal agency. CBO's deficit figure would be $10 billion if calculated using the same accounting treatment as OMB. |

||

| Enacted last fall | $14 | 15% |

| Enacted this session | $81 | 85% |

| TOTAL | $95 | 100% |

| A more complete analysis of the figures in Table 2 is shown in Table 3. | ||

Some $95 billion of the deterioration in the 2001 surplus from last July to this August is due to legislation enacted last fall or so far this year. Of that $95 billion, the vast bulk — 85 percent — is the result of laws passed by this Congress and signed by President Bush. (See Tables 2 and 3.) These data suggest that, even using last year rather than this year as the reference point, it is difficult to blame the deterioration of the 2001 surplus primarily on the prior Congress or the prior administration.

Long-term Costs

We also compare the ten-year cost of the legislation enacted last fall with the ten-year cost of the tax cut. As Table 4 (on the next page) indicates, the cost of the tax cuts enacted this year far exceeds the cost of last year's budget increases. Over a ten-year period, the tax cut is nearly four times as costly as the budget increases. The tax cut will be more than five times as costly when it is fully in effect.(5)

Administration Finds Some of Last Year's Spending Increases Inadequate

It also should be noted that although the Bush Administration apparently finds it useful to castigate the program increases enacted last fall, it is far from clear that the Administration really objects to those increases. The Administration had the opportunity this spring to request the rescission of some amounts enacted last fall. It chose not to do so. Furthermore, of the $434 billion in ten-year expenditure increases enacted last fall, about 60 percent occurred in three areas of the budget: health research and training, defense, and education. In this year's budget, the Administration requested further funding increases for 2002 in all three of these areas — an 8 percent funding increase for health research and training, a 7 percent funding increase for defense, and a 4 percent increase for education, compared with the levels needed to cover inflation. In these areas, the Bush Administration appears to believe the previous Congress did not raise spending sufficiently and further increases are needed.

| Ten-year cost in billions | Tenth-year cost as a share of GDP | |

| Discretionary and mandatory program increases enacted last fall | $434 | 0.33% |

| Tax cuts enacted last fall | $37 | 0.03% |

| Tax cuts enacted this June (assuming all provisions are made permanent) | $1,660 | 1.75% |

| Source: CBO/JCT. The ten-year cost of legislation enacted last session covers the period 2001-2010. The ten-year cost of the recently enacted tax cut covers the period 2002-2011, and therefore excludes the $74 billion cost of that tax cut in 2001. Costs would be higher if they also included the resulting increase in federal interest payments. | ||

What Spending Explosion? Putting 2001 Spending Increases in Context

Some policymakers have termed the program increases enacted last fall a "spending explosion."(6) In fact:

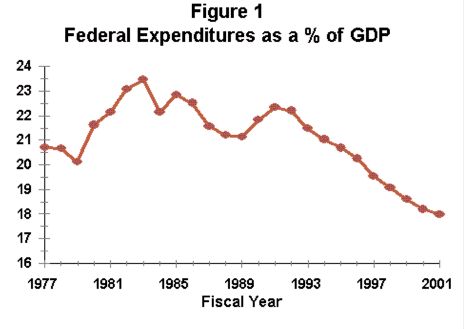

- Even with last year's program increases, federal spending continued to fall in 2001 as a share of the economy. OMB's newest figures suggest that federal expenditures will equal about 18 percent of the gross domestic product (GDP) in 2001, which is the lowest level since 1966.

- The rate of growth in federal expenditures between 2000 and 2001 was below the historical average.

- The rate of growth in federal expenditures called for in the Bush budget for 2002 is higher than the rate that occurred in 2001.

In short, the rhetoric about "last year's spending explosion" is not justified by the data.

Expenditures as a Share of the Economy

As a share of the economy, federal spending has fallen for the last ten years. At about 18 percent of GDP in 2001, it is at its lowest level since 1966. (See Figure 1.) Federal expenditures rise as a share of the economy when the economy is a recession (because even a flat level of expenditures will constitute a larger share of a smaller economy). Although the current year is characterized by a weak economy, federal expenditures will constitute a smaller share of GDP this year than in all years of recent decades, including years in which the economy was robust.

Rates of Growth in Federal Spending

OMB now projects that federal expenditures will grow by 3.1 percent in 2001. This is significantly lower than the historical average (for the period 1962-2001), which is 7.5 percent. OMB also projects that under the Bush Administration budget, federal spending will increase at a faster rate — 6.4 percent — in 2002. These figures are shown in Table 5.

| Nominal increase | Real increase (i.e., adjusted for inflation) |

|

| Historical average, 1962 — 2001 | 7.5% | 2.8% |

| In 2001 | 3.1% | 0.5% |

| In 2002 | 6.4% | 3.9% |

| Source: figures for 1962-2000, Historical Tables, OMB, April 2001; figures for 2001 and 2002, Midsession Review, OMB, August 22, 2001. The 2001 costs of the spring supplemental appropriations bill and the recent farm bill are omitted since they were not enacted by the previous Congress. Had they been included, the figures would be only slightly different. The adjustments for inflation used the OMB deflators published in April 2001. | ||

These figures just cited do not adjust for inflation; they simply show the year-over-year growth of federal expenditures. Because inflation was noticeably higher in some years in the 1970s and 1980s, the previously mentioned historical average rate of expenditure growth appears larger than it really is. A better comparison, also provided in Table 5, shows the real rate of growth, in which the effects of inflation are removed. In real terms, federal spending grew by 0.5 percent in 2001, well below the historical average of 2.8 percent per year and also well below the 3.9 percent that the Bush Administration has proposed for 2002.

| Nominal increase | Real increase (i.e., adjusted for inflation) |

|

| Historical average, 1962 — 2001 | 5.7% | 0.9% |

| In 2001 | 5.2% | 2.8% |

| Proposed for 2002 | 8.2% | 5.8% |

| Source: figures for 1962-2000, Historical Tables, OMB, April 2001; figures for 2001 and 2002, Midsession Review, OMB, August 22, 2001 | ||

Some have sought to focus the debate about rates of growth on appropriated (or "discretionary") programs, which represent about one-third of the federal budget. A more complete analysis that covers all federal spending is preferable to an analysis only of discretionary programs. However, even if the analysis is limited to appropriated programs, it is hard to make the case that the Bush Administration is trying to reverse a "spending explosion." Table 6, above, makes the same comparisons as Table 5, but only for the one-third of the budget that is annually appropriated. As the table shows, the increases in discretionary spending that occurred in 2001 are smaller — not larger — than those the Administration has proposed for 2002.

Adjusting for Population Growth Some argue that calculations of rates of growth in government

expenditures should adjust not only for inflation, but also for increases in the

population. When he was Governor of Texas, for example, President Bush said that "an

'honest comparison' of spending growth should take inflation and the state's increasing

population into account."* Many analysts agree that such an adjustment makes sense;

with such an adjustment, analysts can measure the change in the real, per-person level of

goods, services, and benefits that a government provides. If such an adjustment is made,

the average rate of growth in total federal spending from 1962 through 2001 is 1.8 percent

per year, federal spending shrank by 0.4 percent in 2001, and the increase the

Administration's budget proposes for the coming year (2002) is 2.9 percent. |

The magnitude of the discretionary spending increases the Bush Administration has proposed for 2002 primarily reflects the large defense increases the Administration is seeking. Under the Bush budget, expenditures for defense in 2002 would rise at almost twice the rate, after adjusting for inflation, as expenditures for domestic appropriated programs.

Funding versus Spending This analysis has focused exclusively on program expenditures for the budget as a whole and for the one-third of the budget covering appropriated programs. It has focused on expenditures because of the attention being paid to the surplus; the difference between revenues and expenditures determines whether the budget is in surplus or deficit. The Administration, in discussing a "spending explosion," has instead focused on funding levels, not expenditures, and sometimes limits its analysis to domestic appropriations, which represent just one-sixth of the budget. Such an approach ignores the $32 billion increase in defense funding the Administration has proposed for 2002. Counting defense, and using data published by OMB in April and August, it can be seen that total funding for appropriated programs was increased in nominal terms by 8.6 percent in 2001 by the previous Congress and Administration, and that this Administration is proposing a further nominal increase of 7.1 percent. In nominal dollar terms, last year's funding increase for appropriated programs was $50 billion and this year's proposed increase is $45 billion. From this perspective, the primary difference between funding increases for 2002 and 2001 is not so much their total size as the fact that last year's increase occurred mostly in domestic programs such as education and health research while this year's increase occurs mostly in defense. (A better analysis of funding increases would make a variety of adjustments to these data to correct for anomalies and distortions. See How Realistic Are the Discretionary Funding Levels in the President's Budget and the Congressional Budget Resolution? Center on Budget and Policy Priorities, August 3, 2001.) |

Conclusion

Appropriation bills enacted last fall contributed to the growth of federal spending in 2001, but they are not the reason the 2001 surplus that OMB projected this April has disappeared. The tax cut and the economic slowdown are the reasons. More generally, the 2001 expenditure increases enacted last year are only one-fifth the size of the tax cut over the long run. And as a share of the economy, total federal spending in 2001 is at its lowest level since 1966.

In addition, the rate of spending growth that occurred in 2001 appears low by historical standards. Indeed, the level of expenditure growth the Bush budget proposes for 2002 exceeds the level that occurred in 2001.

End Notes:

1. The Budget of the United States Government, Fiscal Year 2002, Office of Management and Budget, Summary Table 3, p 225, April 9, 2001. OMB predicted a total surplus of $281 billion, of which $156 billion was "off budget" (the off-budget surplus is accounted for almost entirely by the Social Security Trust Fund), leaving a predicted $125 billion on-budget surplus. For simplicity, this analysis will refer to the on-budget surplus, which excludes Social Security, as "the surplus." If the $29 billion surplus in the Medicare Hospital Insurance Trust Fund predicted by OMB also were excluded, as Congress evidently believes it should be, the predicted surplus for 2001 would have been $96 billion. (The OMB estimate of a $29 billion surplus in the Medicare HI trust fund appears in Table 15-4 of the OMB's Analytical Perspectives, also issued April 9.)

2. Lawrence Lindsey, the President's economic advisor, speaking on CNN's Inside Politics of August 6, 2001, said "[T]he previous Congress last year, to get out of town, spent $30 billion more than what they had agreed they were going to spend."

3. Because this aspect of the analysis examines spending in 2001 resulting from legislation enacted last fall, it does not include the 2001 expenditures that will result from this spring's defense supplemental appropriations bill and this summer's increase in farm price supports. Inclusion of those two pieces of legislation would make little difference in the figures.

4. See How Much of the Surplus Remains After the Tax Cut? Center on Budget and Policy Priorities, revised June 27, 2001.

5. For a discussion of the costs of the recently enacted tax cut, see "New Tax-cut Law Ultimately Costs as Much as Bush Plan: Gimmicks Used to Camouflage $4.1 Trillion Cost in Second Decade," Center on Budget and Policy Priorities, revised June 27, 2001. The data are from JCT estimates of the enacted tax bill and JCT estimates provided to Rep. Charles Rangel of the cost of making the provisions of the tax cut permanent, including adjusting the Alternative Minimum Tax thresholds so that the number of people subject to the AMT does not rise any faster than it would have under prior tax law.

6. Because this aspect of the analysis examines spending in 2001 resulting from legislation enacted last fall, it does not include the 2001 expenditures that will result from this spring's defense supplemental appropriations bill and this summer's increase in farm price supports. Inclusion of those two pieces of legislation would make little difference to the figures.