Administration Medicaid and SCHIP Waiver

Policy

Encourages States to Scale Back Benefits Significantly and

Increase Cost-Sharing for Low-Income Beneficiaries

Policy Does Not Require States to

Reinvest the Savings in Expanded Health Coverage

by Edwin Park and Leighton Ku

| PDF version of this report If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

On August 4, 2001, the Administration unveiled its Health Insurance Flexibility and Accountability (HIFA) demonstration initiative, a new waiver policy for Medicaid and the State Children's Health Insurance Program (SCHIP) that is intended to reduce the ranks of the uninsured.(1) The Administration argues that its waiver policy, which builds on a proposal by the National Governors Association, provides states additional flexibility that will translate into savings that states can use to finance further coverage expansions through Medicaid and SCHIP.(2) The waiver policy was generally portrayed in the media as a positive step by the Administration to increase the number of Americans with health insurance.

Analysis shows, however, that the policy invites states to cut critical health benefits and increase cost-sharing for up to 12 million low-income elderly and disabled individuals, parents, pregnant women, and children without any requirement that states use the resulting savings to expand coverage. As a result, through these waivers, states that wish to do so apparently will be able to take actions that can reduce the access of current beneficiaries to health services (because certain services are no longer covered or because some beneficiaries cannot afford the higher copayments they are charged) in order to finance other non-health expenditures or tax cuts.

For the federal government to encourage states to expand coverage significantly without adversely affecting current beneficiaries, the federal government could instead provide states additional federal financial resources and incentives. For example, bipartisan legislation recently introduced in Congress, the FamilyCare Act of 2001, would provide additional federal funds to states, at the enhanced SCHIP matching rate, for extending Medicaid and SCHIP coverage to parents of children enrolled in these programs.(3) Such a proposal would not only substantially reduce the number of uninsured working parents in the United States but also would have the additional beneficial effect of facilitating the enrollment of low-income children who are eligible but not yet participating in Medicaid and SCHIP. Research shows that the participation rates of eligible children increase when a state expands coverage to the parents of these children. Congress has set aside $28 billion in this year's budget resolution to expand health coverage to the uninsured; the FamilyCare Act could serve as the basis of legislation using these new federal resources.

The Administration's Medicaid and SCHIP Waiver Policy

Under section 1115 of the Social Security Act, the federal government may permit states to establish comprehensive demonstration projects that waive federal Medicaid and SCHIP requirements related to benefit standards, beneficiary cost-sharing, and eligible populations.(4) The primary goal of the Administration's new policy is to use such waivers to increase the number of individuals with health insurance coverage. Specifically, the policy envisions waivers that use savings derived from additional Medicaid flexibility and a state's unspent SCHIP funds to expand coverage.

The greater state flexibility would be available with regard to "optional" Medicaid populations: individuals whom federal law allows but does not require states to cover and whom states have elected to cover.(5) States would be permitted to limit the range of Medicaid benefits for these optional groups to the benefits required under SCHIP and, in some cases, potentially to a lesser range of benefits than SCHIP generally provides. States also would be permitted to impose substantially greater cost-sharing on these beneficiaries; in many cases, there would be no limit on the level of cost-sharing a state could impose. Under current law, only nominal cost-sharing is permitted.

The resulting savings to states could be used, in combination with unspent SCHIP funds, to finance further coverage expansions under Medicaid and SCHIP, including the provision of health insurance to groups that may not otherwise be covered under those programs, such as adults without children. In addition, under the new policy, states could expand premium assistance programs, under which states pay the employee share for premiums of Medicaid and SCHIP beneficiaries who are enrolled in private employer-based coverage, instead of financing their care directly through Medicaid or SCHIP-funded programs.

This new waiver policy raises a number of concerns:

- There is no requirement that states reinvest the

savings from reduced benefits and greater beneficiary cost-sharing in expanded coverage.

While the purpose of the new waivers is to reduce the number of uninsured Americans, states are not required to demonstrate that the savings from additional Medicaid flexibility actually are used to expand coverage. The new policy asks only that states set coverage goals and evaluate annually whether uninsurance rates have declined. According to media reports, officials at the Department of Health and Human Services have confirmed the lack of such a requirement and would consider waiver applications from states that do not plan to reinvest the savings in coverage expansions.(6) Section 1115 waivers only need to be "budget neutral," which means that the cost to the federal government is no greater under the waiver than it would be without the waiver. Budget neutrality does not require that combined federal and state expenditures on health insurance equal what health insurance expenditures would be without the waiver.

Under the new policy, states could scale back Medicaid benefits and increase cost-sharing without any appreciable benefit to the uninsured. A state could use part or all of the savings to offset existing Medicaid and SCHIP obligations or to finance other budget items, such as constructing roads or providing tax cuts.

- Nearly 12 million Medicaid beneficiaries, many of whom

have incomes well below the poverty line, could be at risk for reduced benefits and

onerous cost-sharing.

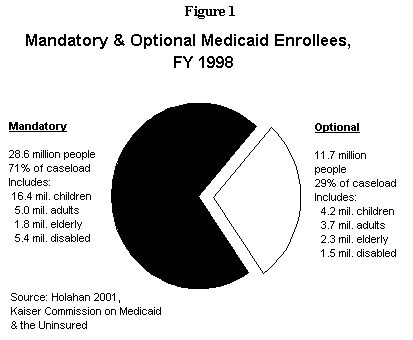

As seen in Figure 1, some 11.7 million Medicaid beneficiaries in 1998 — or 29 percent of all beneficiaries — were part of the optional groups that would be at risk for a reduced array of benefits and increased cost-sharing under the new waiver policy. These beneficiaries include 4.2 million children, 3.7 million pregnant women and parents, 2.3 million elderly individuals and 1.5 million disabled people. An estimated 500,000 individuals who now receive Medicaid through section 1115 waivers also would be vulnerable.

Supporters of the waiver policy may argue that imposing modest reductions in benefits or increases in cost-sharing on moderate-income individuals (as distinguished from low-income individuals) is justified when such policies help to finance further coverage expansions.

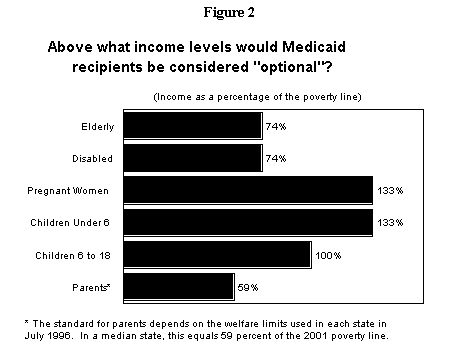

As seen in Figure 2, however, many individuals in these optional groups have family incomes at or below the poverty line ($8,590 for an individual, $14,630 for a family of three). The optional groups that would be subject to reduced benefits and increased cost-sharing include the following types of low-income individuals:

- An elderly widow with income of $7,800 a year. Her income is above the federal eligibility limit for the Supplemental Security Income (SSI) program. In many states, she qualifies for Medicaid because she collects a state-funded SSI supplement.

- A severely disabled man with income of $8,000 a year who qualifies for Medicaid because his state has expanded Medicaid eligibility for the disabled up to the poverty line.

- A mother of two who works in a full-time minimum wage job and earns $10,300 a year (or 70 percent of the poverty line). Her income is above welfare limits. She receives Medicaid because her state has expanded income eligibility for parents to the poverty line.

- A 12-year-old child living in a family of three that has income of $16,100 a year (110 percent of the poverty line) who receives Medicaid under an SCHIP-funded program.

- Optional beneficiaries, especially those with special

health care needs, may lose critical Medicaid benefits such as long-term care and EPSDT.

To ensure that beneficiaries have a comprehensive health services package, federal law requires states to provide certain benefits to all Medicaid beneficiaries. Such benefits include nursing home care and home health care for those with long-term care needs and Early and Periodic Screening Diagnosis and Treatment (EPSDT) services for children.(7) EPSDT is a comprehensive prevention and treatment benefit for children that ensures that children receive all of the medical items and services they are found to need. This means a disabled child would, for example, have access to medically necessary personal care services or a specific piece of durable medical equipment when such services or equipment are not otherwise covered by a state's Medicaid program.

Under the new waiver policy, states may roll back Medicaid benefits for optional beneficiaries (even if these are so-called "mandatory benefits"). States may reduce benefits to the levels that federal law requires under separate SCHIP plans. SCHIP benefits vary by state but must be equal to at least one of the following benchmark plans: the Blue Cross-Blue Shield option under the Federal Employees Health Plan, the state's plan for state employees, or coverage offered by the HMO with the largest enrollment in the state.

Furthermore, the new waiver policy appears to permit states to reduce Medicaid benefits below even SCHIP benchmark standards. A model application form for the waivers indicates that states may limit coverage to a level specially approved by the Secretary of Health and Human Services if the coverage provides certain services.(8) While SCHIP already permits specially approved coverage, the SCHIP regulations expect that such coverage be generally consistent with Medicaid or with the SCHIP benchmarks, a higher standard than the one set by the waiver policy.(9)

SCHIP benefits themselves are significantly less generous than the benefits Medicaid provides. SCHIP is required to cover fewer services, and states often establish more restrictive service caps, such as limiting mental health visits to 20 per year.(10) In addition, because the benchmark plans used to set standards for SCHIP coverage generally do not cover long-term care, separate state SCHIP plans typically do not include long-term care benefits. Separate SCHIP plans also do not include EPSDT for children.(11) Because SCHIP benefits are less comprehensive, they are less likely than Medicaid benefits to be appropriate for the medical needs of persons with special health care needs.(12) Under the new waiver policy, some "optional" individuals — including disabled individuals not receiving SSI — may find they have less access to essential needed benefits than they previously did.(13)

- Greater cost-sharing could discourage optional

Medicaid beneficiaries from accessing medically necessary services.

Under the new waiver policy, states may require cost-sharing for all benefits provided to optional Medicaid populations; this cost-sharing may exceed the current "nominal" limits, which are generally no more than $3.00 per service.(14) In the case of optional children who are currently exempt from any Medicaid cost-sharing, charges must not exceed a total of five percent of family income, as under SCHIP. For all other Medicaid groups, including the elderly, the disabled, pregnant women, and parents, the new policy allows states to impose unlimited cost-sharing.

Increased cost-sharing could adversely affect access to needed health care services for these optional groups. The research literature amply documents that cost-sharing reduces utilization of health care services. It also has a disproportionate effect on low-income populations. For example, the RAND Health Insurance Experiment compared health care utilization and health status between people facing various levels of cost-sharing and those facing no cost-sharing. As expected, health care utilization was lower for those with cost-sharing than for those receiving free care. Nevertheless, for the average person, this did not have a significant effect on health status. Among poor individuals, however, certain important aspects of health status such as blood pressure rates and vision improved significantly in the absence of cost-sharing. This was because cost-sharing had a larger impact in discouraging use of necessary health services among low-income populations.(15)

| Group | Current Cost-Sharing Limits | Waiver Cost-Sharing Limits |

| Medicaid Children* | No cost-sharing permitted | Total must not exceed 5% of family income |

| Elderly | Up to $3.00 per service | Unlimited |

| Disabled | Up to $3.00 per service | Unlimited |

| Adults (Pregnant Women/Parents) | No cost-sharing for

pregnancy-related services. Others up to $3.00 per service |

Unlimited |

| * SCHIP children in Medicaid expansions are subject to Medicaid cost-sharing protections. SCHIP children in separate state programs are subject to the 5% limit established under SCHIP. | ||

Some states may target Medicaid's prescription drug benefit for greater cost-sharing, considering states' particular concern about rising prescription drug costs.(16) One study demonstrated that even modest copayments placed on prescription drugs under Medicaid led to lower utilization and greater burdens among those with serious health problems.(17)

Greater cost-sharing may make prescription drugs unaffordable for some low-income populations and could deter some of those with the greatest medical needs (the chronically ill who use the most drugs) from obtaining necessary care. Moreover, states may be inclined to impose greater cost-sharing on other services disproportionately used by elderly and disabled Medicaid beneficiaries such as long-term care. This is because the elderly and disabled constitute only one-quarter of all Medicaid recipients but account for three quarters of Medicaid expenditures.(18)

- Expansion populations are not guaranteed meaningful health

insurance coverage.

Even if states use most or all of the savings achieved by scaling back coverage for optional Medicaid populations to finance further coverage expansions, the newly covered individuals may receive only limited benefits. Under the new waiver policy, states need provide only a basic primary care package of physician services for "expansion" populations that are not otherwise eligible under Medicaid and SCHIP.(19) While it is reasonable for states to have some additional flexibility on benefits for expansion groups, some in these populations, such as poor non-disabled adults without children, may have little income and a greater likelihood of having serious health conditions. Under the new policy, individuals in such groups could continue to lack access to medical specialists (oncologists for example) and inpatient hospitalization. States also would have complete flexibility to impose whatever cost-sharing they wish on "expansion" individuals, which could restrict access to necessary services even when the services are covered.

- In some cases, expanding "premium assistance" under

these waivers could cost the federal government more money while leaving beneficiaries

with lesser benefits and greater cost-sharing.

Current law already gives states flexibility to pay premiums and enroll Medicaid and SCHIP beneficiaries in employer-based coverage. States must ensure, however, that doing so is cost-effective for Medicaid and SCHIP and that beneficiaries have the same benefits and cost-sharing protections they would otherwise have. For example, if Medicaid or SCHIP covers physical therapy and private coverage does not include such benefits, states must furnish "wrap-around benefits" that cover the missing services. States also must pay for the additional cost-sharing that beneficiaries in private coverage may face.

As Figure 4 shows, the new waiver policy would appear to allow states to bypass these requirements. Premium assistance no longer has to be found cost effective. Under the new policy, the Administration would apparently approve waivers where premium assistance costs would be higher than costs under the regular Medicaid or SCHIP program, so long as the costs are not "significantly" higher. This could result in public funds substituting for private funds, as some employers with a labor force composed primarily of low-wage workers could reduce their contribution knowing that states could then increase the premium assistance they provided (even when such subsidies would exceed average expenditures for an eligible individual through Medicaid or SCHIP).

Finally, states would no longer have to assure that the benefits and cost-sharing of beneficiaries receiving premium assistance were equivalent to those receiving regular Medicaid or SCHIP coverage. Under a waiver, beneficiaries could find themselves placed in private coverage with lesser benefits and higher cost-sharing than under regular Medicaid or SCHIP, at a somewhat greater cost to the government.

| Requirements | Current Law | Waiver Policy |

| Cost Effectiveness | Costs of premium assistance must be no greater than under regular coverage. | Costs of premium assistance may exceed costs of regular coverage so long as costs are not "significantly" higher. |

| Benefits | State must wrap-around coverage to ensure same level of Medicaid/SCHIP benefits. | No requirement. |

| Cost-Sharing | State must ensure that cost-sharing is no greater under premium assistance than under regular coverage. | No requirement. |

| * SCHIP children in Medicaid expansions are subject to Medicaid cost-sharing protections. SCHIP children in separate state programs are already subject to the 5% limit. | ||

An Alternative Approach

The new waiver policy implies that states committing to reduce the ranks of the uninsured should do so largely or entirely within existing federal Medicaid and SCHIP resources. If states scale back benefits or increase cost-sharing only modestly and invest all of the savings in expanding Medicaid and SCHIP coverage, savings are not expected to be large and thus would not provide adequate financing for more than small expansions. An analysis of a National Governors Association proposal made earlier this year that is broadly similar to the new waiver policy found that modest reductions in the types of services that could be scaled back under the new waiver policy would not be likely to result in substantial savings.(20) As a result, states interested in financing significant expansions through Medicaid savings would have no choice but to cut major benefits more substantially (like long-term care) or to impose onerous cost-sharing requirements on benefits such as prescription drugs.

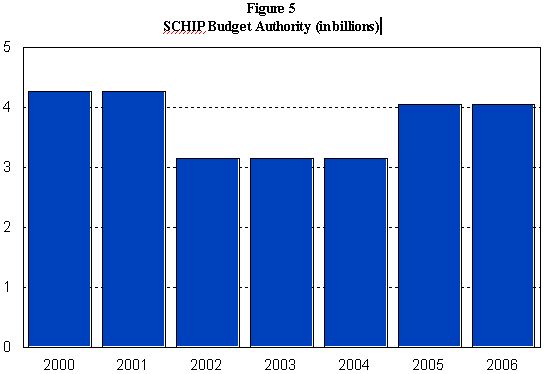

It also should be noted that the Office of Management and Budget estimates that funding for the SCHIP program will be insufficient to maintain even current levels of children's enrollment beginning in fiscal year 2005. Many states cannot look to unspent SCHIP funds to finance coverage expansions, as the new waiver policy seems to envision.

When Congress established the SCHIP program in 1997, it wrote into law a substantial reduction in the federal SCHIP funding level for fiscal year 2002 and the two following years. SCHIP funding was reduced in those years to help balance the budget in 2002 under the economic and budget assumptions in use in 1997. The dip in funding will take effect, however, at a time that states will need increases, not decreases, in SCHIP funds. Although states struggled with initial implementation challenges and the SCHIP program had a slow start in many states, SCHIP enrollment has been increasing substantially in the past few years, resulting in corresponding increases in federal SCHIP expenditures. These expenditures totaled $200 million in fiscal year 1998 (the first year of the program), $600 million in 1999 and $1.8 billion in 2000. Federal SCHIP expenditures are expected to reach $3.4 billion in fiscal year 2002 when the reduction in SCHIP funding is slated to go into effect.

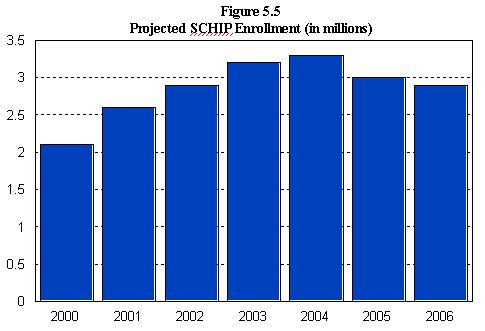

Considering the dip in funding and the increasing state need for SCHIP funds, as seen in Figure 5, OMB estimates that the increase in the number of children enrolled in SCHIP will slow markedly in 2003 and 2004 and the number actually will begin to fall in 2005. OMB projects that enrollment will decline from 3.3 million children in 2004 to 3 million in 2005 and 2.9 million in 2006, a decline of 400,000 children nationwide in two years. In other words, states will be unable to maintain their existing SCHIP enrollment, let alone use available SCHIP funds in combination with savings derived from additional Medicaid flexibility under the new waiver policy.

|

The new waiver policy thus essentially establishes a framework under which states are encouraged to choose between not cutting back on Medicaid and expanding coverage. To avoid such a Hobson's choice, the federal government could instead provide states additional financial resources and incentives. In its budget resolution, Congress has set aside $28 billion for legislation to expand coverage to the uninsured.(21) One viable approach, the bipartisan FamilyCare Act of 2001, could serve as the basis of legislation using these new federal funds. The FamilyCare proposal would provide states additional SCHIP funds, at the SCHIP enhanced matching rate, to extend Medicaid and SCHIP coverage to parents of children enrolled in these programs.(22) In the Senate, the bill was introduced by Senators Edward M. Kennedy (D-MA) and Olympia Snowe (R-ME) and co-sponsored by Senators Susan Collins (R-ME) and Lincoln Chafee (R-RI) as well as all of the Democratic members of the Senate Finance Committee.

The FamilyCare proposal would offer several benefits to states. First, states could significantly expand coverage to parents without rolling back existing Medicaid coverage. Second, it would allow states adversely affected by the dip in SCHIP funding to use the new federal funds to maintain their existing SCHIP caseload, in addition to expanding coverage for parents. Third, it would reward innovative states that have previously expanded parental coverage by making available enhanced matching funds for such expansions. Fourth, it would help facilitate the enrollment of eligible children in public programs. According to a growing number of studies based on state experiences, the participation rates of eligible children increase when a state institutes an expansion to the parents of these children.(23) One study also determined that children are more likely to receive preventive care, such as well-child visits, when both the child and the parent are insured and in public programs.(24) Finally, in addition to helping states expand coverage to parents, the FamilyCare proposal increases state flexibility under the Medicaid and SCHIP programs. For example, it permits states to cover legal immigrant pregnant women and children who entered the United States after August 22, 1996, the date the welfare law was signed, and gives states new simplification options in administering transitional medical assistance (TMA) for people leaving welfare for work.(25)

Conclusion

The Administration's Medicaid and SCHIP waiver policy establishes a flawed framework under which states may expand coverage only by using existing Medicaid and SCHIP resources. Considering the pending SCHIP funding shortfall, many states interested in expanding coverage would have no choice but to target the existing Medicaid program for reductions in benefits. The new waiver policy invites states to cut back important benefits and increase cost-sharing for millions of low-income Medicaid beneficiaries.

The new policy also fails to include a requirement that states be able to roll back Medicaid benefits only if they dedicate the resulting savings to expanded coverage. As a result, in some states, the new policy may result in significant harm to existing beneficiaries without materially reducing the ranks of the uninsured.

A superior alternative would be for Congress to provide states additional federal financial resources and incentives to expand coverage particularly to parents of children enrolled in Medicaid and SCHIP. This would provide funds to states for increasing health insurance coverage substantially without cutting back on coverage for needy, vulnerable populations.

End Notes:

1. Centers for Medicare and Medicaid Services, "Health Insurance Flexibility and Accountability (HIFA) Demonstration Initiative," August 4, 2001. Available at www.hcfa.gov/medicaid/hifademo.htm.

2. NGA Policy Position HR-32 "Health Care Reform", adopted 2001 Winter Meeting on February 27, 2001 and effective through 2003.

3. S.1244 (sponsored by Senators Kennedy and Snowe) and H.R. 2630 (sponsored by Representative Dingell).

4. For an overview of section 1115 waivers, see Jeanne Lambrew, Section 1115 Waivers in Medicaid and the State Children's Health Insurance Program: An Overview, Kaiser Commission on Medicaid and the Uninsured (July 2001).

5. "Mandatory" Medicaid populations include low-income families that would have met the eligibility criteria for cash assistance prior to welfare reform, children in foster care, elderly and disabled SSI beneficiaries, pregnant women and children up to age 6 with incomes up to 133 percent of the poverty line, and children ages 6-18 with incomes up to 100 percent of the poverty line. "Optional" populations include children with incomes above these mandatory levels, pregnant women with incomes up to 185 percent of the poverty line, elderly and disabled individuals who are poor but whose incomes are too high for them to qualify for SSI, disabled people in institutions who have incomes up to 300 percent of the SSI payment standard, low-income uninsured women with breast cancer, and people with disabilities who are returning to work.

6. Laura Meckler, "Bush Medicaid Plan Worries Liberals," Associated Press, August 7, 2001.

7. Other services that states have been required, until now, to provide to all beneficiaries include hospital services, physician services, clinic services, laboratory and x-ray services, family planning, and nurse practitioner and midwife care. States may also elect to offer other optional services, such as prescription drugs, durable medical equipment, physical therapy, and personal care services. States must offer the same array of Medicaid benefits to both mandatory and optional populations.

8. The minimum services are hospital services, physician and other medical services, laboratory and x-ray services and well-baby and well-child care including immunizations. Centers for Medicare and Medicaid Services, "Application Template for Health Insurance Flexibility and Accountability (HIFA) §1115 Demonstration Proposal," August 4, 2001. Available at www.hcfa.gov/medicaid/hifatemp.pdf.

9. The regulations define Secretary-approved coverage as including Medicaid benefits provided to children, comprehensive Medicaid benefits for children under a section 1115 waiver, coverage that includes EPSDT or has been extended under Medicaid to all populations, benchmark coverage or its actuarial equivalent, and premium assistance coverage if it is substantially equivalent or greater than benchmark coverage. While the regulations state that this is not an exclusive list and the federal government would consider additional coverage options, the representative benefit packages are likely to include more than the minimum benefits under the waiver policy. For example, when providing equivalent coverage, states are expected to also include prescription drugs, mental health services, and vision and hearing services if such services are included in the benchmark plan.

10. General Accounting Office, Medicaid and SCHIP: Comparisons of Outreach, Enrollment Practices and Benefits (April 2000).

11. Nor does SCHIP cover family planning, another mandatory Medicaid service.

12. John Holahan, Restructuring Medicaid Financing: Implications of the NGA Proposal, Kaiser Commission on Medicaid and the Uninsured (June 2001); General Accounting Office, Children with Disabilities: Medicaid Can Offer Important Benefits and Services (July 2000). See also Harriette Fox, Margaret McManus and Stephanie Limb, Access to Care for S-CHIP Children with Special Health Needs, Kaiser Commission on Medicaid and the Uninsured (December 2000).

13. It should be noted that permitting states to reduce Medicaid benefits to SCHIP levels (or possibly below) would undercut the value of the Family Opportunity Act (S. 321, H.R. 600). This is bipartisan legislation now before Congress that would permit states, at their option, to allow families that include children with disabilities to buy into the Medicaid program for their children on a sliding scale based on income. The purpose of the legislation is to give these families access to the comprehensive Medicaid services that their children require but that these children may not receive even when they are eligible for SCHIP or private insurance. Because the new waiver policy permits states to reduce Medicaid benefits to SCHIP levels for all optional populations and the new buy-in category would constitute an optional population, the disabled children the Family Opportunity Act is intended to help might not actually benefit.

14. Under Medicaid, states may impose one, but not more than one, of the following types of cost-sharing: deductibles, cost-sharing, and copayments. Deductibles may not exceed more than $2.00 per service. Cost-sharing may not exceed more than half of the reimbursement the state pays a provider for the first day of service. For example, if a state pays a hospital $200 per day on behalf of a Medicaid beneficiary, the state may require the beneficiary to pay no more than $100 for the hospitalization. Finally, copayments, the most common form of cost-sharing, may be not exceed $3.00 per item or service. States may not impose any cost-sharing for services for children, pregnancy-related services, family planning, hospice services, or inpatient services for medically needy beneficiaries who are eligible because they have already "spent down" to the state Medicaid income eligibility limit.

15. R. Brook, et al. "Does free care improve adults' health? Results from a randomized controlled trial." New England Journal of Medicine, 309(23):1426-34, Dec. 8, 1983. E. Keeler, et al. "How free care reduced hypertension in the health insurance experiment," Journal of the American Medical Association. 254(14):1926-31, Oct. 11, 1985. N. Lurie, et al. "How free care improved vision in the health insurance experiment. " American Journal of Public Health, 79(5):640-2, May 1989.

16. Prescription drug costs are expected to rise 70 percent faster than overall Medicaid spending over the next five years. Leighton Ku and Jocelyn Guyer, Medicaid Spending: Rising Again but not to Crisis Levels, Center on Budget and Policy Priorities (April 2001). A number of states have enacted legislation this year establishing drug formularies and requiring prior authorization in order to reduce prescription drug expenditures.

17. B. Stuart and C. Zacker, "Who bears the burden of Medicaid drug co-payment policies?" Health Affairs, 18(2): 201-12, March/April 1999. See also C.E. Reeder and Arthur Nelson, "The Differential Impact of Copayment on Drug Use in a Medicaid Population," Inquiry 22,4, Winter 1985.

18. Brian Bruen and John Holahan, Medicaid Spending Growth Remained Modest in 1998, but Likely Headed Upwards, Kaiser Commission on Medicaid and the Uninsured (February 2001).

19. The basic primary care package means "health care services customarily furnished by or through a general practitioner, family physician, internal medicine physician, obstetrician/gynecologist, or pediatrician."

20. John Holahan, Restructuring Medicaid Financing: Implications of the NGA Proposal, Kaiser Commission on Medicaid and the Uninsured (June 2001). In addition to providing states greater flexibility on benefits and cost-sharing as does the new waiver policy, the NGA proposal also provided states the enhanced SCHIP matching rate for all optional Medicaid populations and services if states agreed to provide at least the SCHIP level of benefits. The enhanced matching rate would lower the cost of expansions, while also reducing the incentives to cut back on benefits and cost-sharing (because the state savings would be reduced by 30 percent through the enhanced match). The availability of enhanced matching under the NGA proposal thus would be likely to spur state expansions, while additional state flexibility alone — as the Administration's new policy provides — would offer little savings for expansions unless benefits are scaled back or cost-sharing increased more than modestly.

21. See Jocelyn Guyer, Congress Has a $28 Billion Opportunity to Expand Coverage for Low-Income Working Families with Children, Center on Budget and Policy Priorities (July 2001).

22. The enhanced SCHIP matching rate reduces the state's share of expenditures by 30 percent, as compared to Medicaid.

23. See Leighton Ku and Matthew Broaddus, The Importance of Family-Based Expansions: New Research Findings about State Health Reforms, Center on Budget and Policy Priorities (September 2000); Lisa Dubay and Genevieve Kenney, The Effects of Family Coverage on Children's Health Insurance Status, Presentation to the Academy for Health Services Research and Health Policy Conference, Urban Institute (June 2001); and Jeanne M. Lambrew, Health Insurance: A Family Affair, The Commonwealth Fund (May 2001).

24. Elizabeth Gifford and Robert Weech-Maldonado, Encouraging Preventive Health Services for Young Children: The Effect of Expanding Coverage to Parents, Presentation to the Academy for Health Services Research and Health Policy Conference, Pennsylvania State University (June 2001).

25. Current law generally prohibits states from using federal Medicaid and SCHIP funds to cover legal immigrants who entered the country after August 22, 1996 during these immigrants' first five years in the United States. Current law also requires states to impose onerous income reporting requirements, which operate as a barrier to participation, on recipients of transitional Medicaid (people who become ineligible for Medicaid because of an increase in their earnings are entitled to up to 12 months of transitional coverage) even if states wish to ease these requirements.