TOP TEN FACTS ON SOCIAL SECURITY'S 70TH ANNIVERSARY

by Jason Furman

PDF of this report If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader.

President Franklin Delano Roosevelt signed the Social Security Act on August 14, 1935, which established a basic compact between generations: younger workers would contribute payroll taxes, and retired workers would have a more secure retirement. Presidents from Dwight Eisenhower to Ronald Reagan have signed landmark Social Security reforms to expand Social Security to provide disability insurance (1954), index Social Security benefits so people would not become poorer as they grew older (1972), and reform Social Security to add decades to its life (1983).

As Social Security approaches its 70th anniversary on August 14, 2005, it remains one of the most successful and effective, as well as one of the most popular, of government programs. It provides a universal benefit that is progressive and lifts millions of people out of poverty. It also provides extremely valuable social insurance, providing payments to those who need them most — including workers who become disabled, families whose breadwinner dies, dependent spouses, and retirees who live to a very old age and outlive their assets.

A balanced set of reforms needs to be enacted to ensure that Americans can continue to count on this vital program. Social Security’s trust fund is expected to be exhausted in 2041 according to the Social Security actuaries, or in 2052 according to the Congressional Budget Office — and to be able to pay about 75 percent of currently scheduled benefits after that.[1] This matter needs to be addressed. Modest modifications in Social Security also could make the program even more effective than it already is at reducing poverty in old age.

But it is crucial not to undermine the essential features of Social Security in the name of saving it. Private accounts that divert revenue from Social Security and replace part or all of Social Security would jeopardize, directly or indirectly, many of Social Security’s most important accomplishments.

As policymakers contemplate changes in Social Security, they should keep in mind 10 important facts about the program:

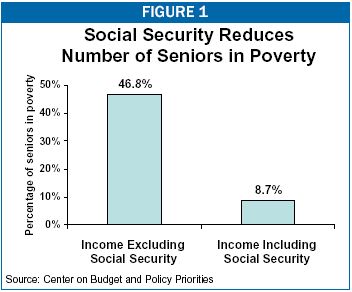

Fact #1: About half of the elderly have incomes that, without Social Security, leave them below the poverty line. Social Security lifts 13 million elderly Americans above the poverty line.

Fact #1: About half of the elderly have incomes that, without Social Security, leave them below the poverty line. Social Security lifts 13 million elderly Americans above the poverty line.

Without Social Security benefits, 46.8 percent of Americans aged 65 and older would have incomes below the poverty line, all else being equal. With Social Security benefits, only 8.7 percent of the elderly do. Some 13 million elderly Americans are lifted out of poverty by Social Security benefits.[2]

Fact #2: Social Security does more to reduce poverty among children than any other government program.

In 2002, one million children under age 18 were lifted above the poverty line by Social Security benefits. No other government program except the Earned Income Tax Credit (EITC) lifts more children out of poverty. In addition, if a broader poverty alleviation measure is used that includes reductions in the severity of poverty (for those who remain poor), then Social Security does more to alleviate poverty among children than any other government program, including the EITC.[3]

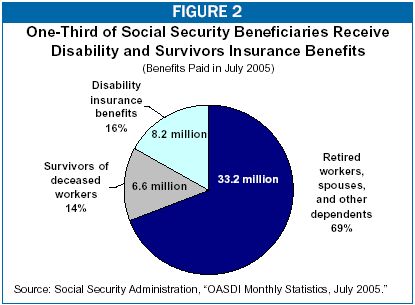

Fact #3: Social Security is more than just a retirement program: one-third of Social Security beneficiaries receive survivors benefits or disability insurance benefits. 10 million beneficiaries are adults below the age of 65, and 4 million are children.

Fact #3: Social Security is more than just a retirement program: one-third of Social Security beneficiaries receive survivors benefits or disability insurance benefits. 10 million beneficiaries are adults below the age of 65, and 4 million are children.

Social Security is more than just a retirement program. Of the 48 million beneficiaries in July 2005, 6.6 million received survivors benefits and 8.2 million received disability benefits. In total, 10.3 million adults below the age of 65 and 3.9 million children received Social Security benefits.[4] The Social Security Administration’s Office of the Chief Actuary has estimated that an illustrative family whose breadwinner dies at a young age can receive a total of $403,000 in survivors benefits, while an illustrative family whose breadwinner becomes permanently disabled can receive a lifetime benefit of $353,000 from Social Security disability insurance.[5] The Social Security Administration estimates that almost one of every three young workers will become disabled before reaching retirement age.

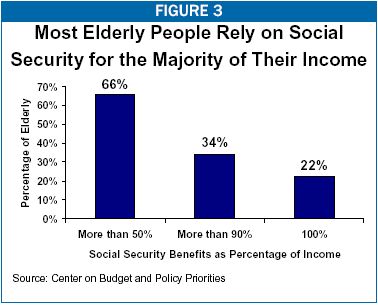

Fact #4: For two-thirds of the elderly, Social Security provides the majority of their income. For one-third of the elderly, it provides nearly all of their income.

Fact #4: For two-thirds of the elderly, Social Security provides the majority of their income. For one-third of the elderly, it provides nearly all of their income.

In 2002, Social Security provided 50 percent or more of the income of 66 percent of elderly people (those age 65 or older). Social Security provided 90 percent or more of the income of 34 percent of elderly people. For 22 percent of seniors, Social Security is the sole source of retirement income.[6]

Fact #5: Social Security provides benefits to 48 million Americans, with the average beneficiary receiving $10,500 per year.

In July 2005, Social Security provided benefits to 48.1 million Americans, with benefits averaging $876.70 a month, or $10,500 annually.[7]

Fact #6: Social Security is especially beneficial for women.

Some 57 percent of adult beneficiaries are women.[8] Women pay 39 percent of Social Security payroll taxes and receive 50 percent of Social Security benefits. [9] (This includes survivor and disability benefits as well as retirement benefits.) Women benefit disproportionately from a number of the program’s features, including its inflation-protected benefits (because women live longer), its progressive formula for calculating benefits (because women tend to have lower incomes), and its benefits for non-working spouses and survivors. Certain reforms could make Social Security even more effective for women, particularly widows.

Fact #7: Social Security is particularly important for African Americans.

African Americans benefit from Social Security’s progressive benefit formula and from its disability and survivor benefits. A wide range of studies, both by respected government agencies and by leading private scholars, have found that these benefits more than make up for the fact that African Americans have a lower average life expectancy.[10] African Americans make up 13 percent of the population but represent 17 percent of those receiving Social Security disability benefits and 21 percent of the children who receive Social Security benefits.[11]

Fact #8: Social Security provides an especially good deal for Hispanics.

Hispanics benefit substantially from the design of Social Security because, on average, they have lower incomes, a higher incidence of disability, more children per family, and longer life expectancies.[12] One study by Harvard economists Jeffrey Liebman and Martin Feldstein found that Hispanics get a Social Security rate of return that is 35 to 60 percent higher than the rate of return for the general population.[13] In addition, Hispanics are less likely to have access to employer-sponsored pension plans and consequently are much more reliant on Social Security for income in retirement. This should be an important motivation for improving Social Security for Hispanics, especially in terms of coverage issues.

Fact #9: Social Security provides a progressive benefit that keeps up with increases in the cost of living.

Social Security retirement benefits are calculated based on a progressive benefit formula. For the first dollar of average lifetime income, you get a Social Security benefit of $0.90. At higher incomes, a $1 increase in average lifetime income adds only $0.15 to annual benefits. Once benefits are computed, they are automatically adjusted for inflation annually, helping to ensure that people do not fall into poverty as they age. In contrast, most annuities sold by private insurance companies are very expensive and do not increase with inflation.

Fact #10: Social Security is an extremely efficient program, with administrative costs equaling only 0.6 percent of retirement and survivors benefits.

Administrative costs account for only 0.6 percent of total Social Security retirement and survivors benefit payments.[14] According to the most optimistic estimates, even private accounts plans with very limited choices and services would have administrative costs more than ten times as high. The Office of the Chief Actuary of the Social Security Administration generally assumes that with private accounts that offer limited choices and services, administrative costs would ultimately consume about 0.3 percent of account assets each year. At that rate, administrative expenses would ultimately eat up about 7 percent of a worker’s retirement benefit, more than ten times as much as the administrative costs under the current Social Security system.[15]

End Notes:

[1] See Jason Furman and Robert Greenstein, March 24, 2005, “What the New Trustees’ Report Shows About Social Security.”

[2] Arloc Sherman and Isaac Shapiro, February 24, 2005, “Social Security Lifts 13 Million Seniors Above the Poverty Line.” Note these figures are a three-year average from 2000 through 2002. This and other poverty figures cited here count certain non-cash benefits. According to the featured Census Bureau estimates, 10.2 percent of the elderly were living in poverty in 2003.

[3] Arloc Sherman, May 2, 2005, “Social Security Lifts One Million Children Above the Poverty Line.” Specifically, Social Security reduces the “poverty gap” (that is, the total amount by which poor families fall short of the poverty line) by 21 percent, compared to the EITC’s 20 percent reduction.

[4] Social Security Administration, “OASDI Monthly Statistics, July 2005.”

[5] Office of the Chief Actuary, July 23, 2001, “Present Values of Expected Survivor and Disability Benefits for an Illustrative Case.”

[6] Social Security Administration, Fast Facts & Figures About Social Security, 2004.

[7] Social Security Administration, “OASDI Monthly Statistics, July 2005.”

[8] Social Security Administration, Fast Facts & Figures About Social Security, 2004.

[9] Social Security Administration, 2005, Annual Statistical Supplement, 2004.

[10] See Dean Leimer, February 2004, “Historical Redistribution Under the Social Security Old-Age and Survivors Insurance and Disability Insurance Programs,” Social Security Administration Office of Research, Evaluation and Statistics Working Paper No. 104; Jeffrey Liebman, “Redistribution in the Current U.S. Social Security System,” in The Distributional Effects of Social Security and Social Security Reform, Martin Feldstein and Jeffrey Liebman, eds., Chicago: University of Chicago Press, 2002; and Government Accountability Office (GAO), “Social Security and Minorities: Earnings, Disability Incidence, and Mortality are Key Factors that Influence Taxes Paid and Benefits Received,” April 2003.

[11] Social Security Administration, 2005, Annual Statistical Supplement, 2004.

[12] See Fernando Torres-Gil, Robert Greenstein, and David Kamin, June 28, 2005, “The Importance of Social Security to the Hispanic Community” for an extensive discussion of these issues.

[13] Jeffrey B. Liebman, “Redistribution in the Current U.S. Social Security System,” in The Distributional Effects of Social Security and Social Security Reform, Martin Feldstein and Jeffrey B. Liebman, eds., Chicago: University of Chicago Press, 2002. Also, Martin Felstein and Jeffrey B. Liebman, “The Distributional Effects of an Investment-Based Social Security System,” in The Distributional Effects of Social Security and Social Security Reform, Martin Feldstein and Jeffrey B. Liebman, eds., Chicago: University of Chicago Press, 2002.

[14] In 2004, administrative expenses for OASI were $2.4 billion and total benefits were $415 billion. See Board of Trustees, Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds, The 2005 Annual Report of the Board of Trustees of the Federal Old-age and Survivors Insurance and Disability Insurance Trust Funds.

[15] The total cost of administrative expenses substantially exceeds the annual expenses because it reflects the accumulation over a number of years. For example, suppose a person puts $1,000 in an account for 40 years at a 0.30 percent annual cost. The person would pay $3 annually to manage the contribution – or $120 (or 12 percent) over 40 years. In contrast, if the contribution were just made for one year it would only cost $3 (or 0.3 percent). The total cost of 7 percent is close to the average of these two extreme cases.