|

July 29, 2008

STATES CAN OPT OUT OF THE COSTLY AND INEFFECTIVE

“DOMESTIC PRODUCTION DEDUCTION” CORPORATE TAX BREAK

By Jason Levitis

Summary

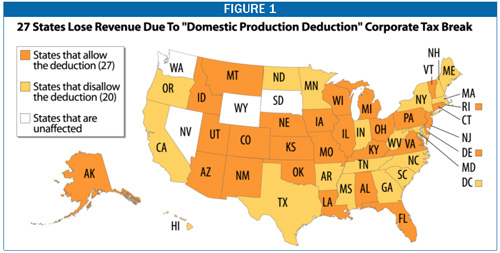

States are losing hundreds of millions of dollars to a relatively new and rapidly growing corporate tax break that in most states never even received a vote in the state legislature. The federal government created this tax break, known as the “domestic production deduction,” in 2004. Since most states base their own tax codes on the federal tax code, the tax break was carried over into many states without any consideration by state lawmakers. Now it is costing not only the federal government but also 27 states a large, and growing, amount of money. By 2011, its cost to these states will exceed $700 million per year.

States need not accept these losses. Some 20 states have already disallowed the deduction, including two in 2008, and it is straightforward for other states to do the same. With many states currently facing budget shortfalls, this may be an ideal time to consider decoupling.

The new deduction — enacted as Section 199 of the federal Internal Revenue Code — allows companies to claim a tax deduction based on profits from “qualified production activities,” a sweeping category that goes well beyond manufacturing to include such diverse activities as food production, filmmaking, and utilities — a substantial share of states’ corporate income tax base.

More than one-quarter of all deductions taken were claimed by the oil industry, which currently is enjoying record profits and has no need of an extra subsidy.

The revenue loss to states from the deduction is set to increase steeply over the next few years. Initially, the cost was relatively modest because the deduction was limited to 3 percent of qualifying income. As of January 1, 2007, however, the percentage rate rose to 6 percent, with another increase to 9 percent scheduled for 2010. As a result, it is likely that revenue losses to states have doubled over the past year and will triple by 2011. Federal estimates suggest that allowing this deduction is likely to cost states about 2.6 percent of their corporate tax revenue, plus a portion of their individual income tax receipts.

States are not required to allow this deduction. Indeed, some 20 states already have chosen to disallow it. But another 27 states continue to permit it. (Four states are unaffected.) If they continue to do so, a conservative estimate suggests the tax break will cost those states some $470 million in fiscal year 2009, rising to $730 million in 2011 and years thereafter. (These estimates are based on current levels of corporate profits and are likely to rise over time.[i])

There is no good reason why states should accept such revenue losses.

- The deduction is unlikely to protect or create jobs within the state, because multi-state corporations — which appear to represent the biggest beneficiaries — can claim the deduction for out-of-state “production activity” just as they can for in-state activity.

- The deduction provides little or no help to businesses that are struggling in the current downturn, since only profitable firms have taxable income for it to offset.

- The deduction is heavily slanted towards large corporations. In 2005, 94 percent of the deduction taken under the corporate income tax was claimed by the 0.4 percent of firms with over $100 million apiece in assets. Many of these large firms are multi-state corporations and may invest little or nothing in the state granting the tax break.

- Indeed, so far the largest beneficiaries of the deduction have been in highly profitable industries like oil production and pharmaceutical manufacture — industries that do not need a subsidy. With a growing number of states facing budget problems — 29 states have forecasted budget deficits totaling $48 billion for fiscal year 2009 and another three states are predicting deficits in fiscal year 2010 — such corporate tax breaks need to be carefully examined.

Decoupling from the domestic production deduction, as 20 states have already shown, is simple to enact and inexpensive to administer. It can be done by adding a single sentence to state tax law requiring corporations to add back the deducted amount to their taxable income.

Indeed, decoupling might even spare a state entanglement in the extensive administrative and legal action that may occur in coming years. The Internal Revenue Service has stated that the provision is complex and difficult for taxpayers to understand. It also has noted that it could be subject to abuse. States that conform to the federal provision risk becoming involved with these difficult and time-consuming enforcement issues.

Notes: Alabama: Deduction is allowed for corporate income tax only. See http://www.revenue.alabama.gov/incometax/fedsec199.pdf.

Michigan: Personal income taxpayers may choose whether their gross income is based on the IRC as of January 1, 1999, or the current tax year.

New Jersey: Deduction is allowed for gross receipts from qualifying production property which was manufactured or produced by the taxpayers, but not for gross receipts from other qualifying production property, including property that was grown or extracted by the taxpayer.

Pennsylvania: Deduction is allowed for corporate income tax only.

Source: Federation of Tax Administrators, based on survey responses from state tax agencies. Updated based on news reports and other sources. |

Click here to read the full-text PDF of this report (18pp.) Click here to read the full-text PDF of this report (18pp.)

End Notes:

[i] These estimates are based on forecasts by the Joint Tax Committee. The Office of Management and Budget forecasts much higher losses due to the domestic production deduction — about twice as high. For further discussion of estimating techniques, see Appendix 1. |