|

July 25, 2007

TESTIMONY OF ROBERT GREENSTEIN

Executive Director, Center on Budget and Policy Priorities

Before the House Budget Committee

July 25, 2007

Chairman Spratt, Congressman Ryan, and members of the Committee, I appreciate the opportunity to appear hear today to explain why I think the pay-as-you-go discipline is important and appropriate, and why establishing a statutory pay-as-you-go rule to reinforce Congressional rules is a sound idea.

My testimony will cover the following:

- Adherence to the pay-as-you-go principle is important because we face an extremely serious long-term budget problem and cannot afford to make that problem worse through entitlement increases or tax cuts that are deficit financed, rather than offset;

- The pay-as-you-go rule proved in the 1990s to be a highly effective tool to help restore fiscal responsibility;

- Pay-as-you-go does not prevent Congress and the President from enacting program expansions or tax cuts; it simply requires that the costs of those actions be paid for;

- Pay-as-you-go is not biased in favor of entitlement expansions and against tax cuts;

- There is not a valid argument for exempting tax cuts from pay-as-you-go on the grounds that requiring the cost of tax cuts to be paid for will hurt the economy;

- Establishing a statutory pay-as-you-go procedure backed up by sequestration will not produce a dramatic improvement compared with the current Congressional pay-as-you-go rules, but it will help to highlight and reinforce the importance of pay-as-you-go and, in particular, make it harder for a future Congress to quietly back away from pay-as-you-go.

Let me address each of these points in more detail.

Pay-as-you-go is Vital Because of the Long-term Fiscal Problem Facing the Nation

As the members of this Committee know all too well, there are many disagreements about the budget — disagreements about the appropriate level of taxes and spending, about priorities among federal programs, and about the kinds of tax and entitlement reform that would be appropriate. But virtually all budget analysts agree on one thing: the federal budget is unsustainable under a continuation of current policies. The looming retirement of large numbers of baby boomers and — more importantly — the continuing rapid growth in the cost of providing health care throughout the U.S. health care system will cause federal expenditures to rise more rapidly than revenues in coming decades. If changes in policies are not made to slow the growth of expenditures (which will primarily entail slowing the growth in health care costs), to increase revenues, or to do a combination of the two, federal deficits and debt will soar in coming decades to levels that will cause serious damage to the economy.

The Congressional Budget Office has reached this conclusion.[1] So has the Government Accountability Office.[2] So has the Bush Administration.[3]

The Center on Budget and Policy Priorities has developed its own set of long-term budget projections (drawing heavily on projections produced by CBO), which, like other projections, show that current policies are not sustainable.[4]

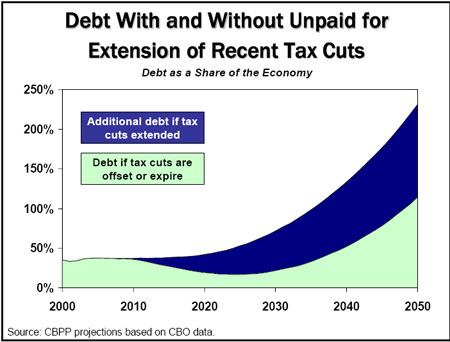

We find that expenditures for all items other than Medicare, Social Security, and Medicaid (excluding interest payments on the debt) are actually expected to shrink by 3.9 percent of GDP between now and 2050. But projected increases in costs for Medicare, Medicaid, and Social Security — driven by increases in health care costs system-wide and the aging of the population — will swamp the contraction in the rest of the budget, result in huge increases in interest payments, and produce deficits of approximately 12 percent of GDP by 2050 and debt in the vicinity of 115 percent of GDP, which would be the highest level of debt in the nation’s history. (Note: the key factor is the expected growth in health care costs per person throughout the U.S. health care system, in the private and public sectors alike, which drives up costs for Medicare and Medicaid. For the past 30 years, per-beneficiary costs have grown at virtually the same rate in Medicare and Medicaid as in private-sector health care, a development this is expected to continue.)

These projections assume that Congress and the President comply with the pay-as-you-go rule, and that discretionary spending grows at the rate of inflation and population, thereby declining somewhat relative to the size of the economy. That means these projections rest on an assumption that any increases in entitlement program expenditures, such as for expansion of the SCHIP program, will be paid for by reductions in other entitlements or increases in revenues. It also means that these projections assume that tax cuts relative to current law (including extensions of tax cuts enacted in 2001 and 2003), will be paid for by increases in other taxes or reductions in entitlement spending.[5]

If, however, one assumes instead that the tax cuts enacted in 2001 and 2003 are made permanent without offsets (while maintaining all of the other assumptions, including that no entitlement expansions are enacted without being paid for), the deficit in 2050 is projected to equal about 20 percent of GDP, and the debt would total approximately 230 percent of GDP, or twice what the size the debt will be if those tax cuts that are extended are paid for. A key reason the deficit and debt levels would be so much higher if the tax cuts were made permanent without their costs being offset is that the increase in deficits that the tax cuts cause would trigger increased interest costs that would compound over time and make the debt spiral markedly worse. This is the case even though our projections do not assume that interest rates would rise; if they do (as is likely), the situation would be even worse.

In other words, under current policies, even with strict adherence to the pay-as-you-go rule, deficits and debt are projected to rise to dangerous levels. Without pay-as-you-go policies, deficits and debt are likely to explode.

It is a cliché to say that when you find yourself in a hole, the first thing you should do is to stop digging, but it is a cliché that offers sound advice. We are in a hole. We eventually are going to have to start filling that hole in (by slowing the overall growth of programs — primarily by slowing the growth in the system-wide cost of providing health care — and by increasing revenues). But in the meantime, we should not dig the hole even deeper.

Looked at another way, eventually Congress simply will have to fill the budget hole, since it cannot allow a debt explosion to occur. Hence, the figures presented here show the projected amount of deficit reduction that Congress will need to enact in the future. Adherence to the pay-as-you-go rule is necessary to keep the eventual deficit reduction packages from being packages of enormous magnitude that consist of draconian cuts in basic programs and services or confiscatory tax increases. Every violation of pay-as-you-go will require an offsetting program cut or tax increase to be enacted later. A key reason to adhere to pay-as-you-go is to limit to some extent the amount of extraordinarily heavy lifting that future Congresses will have to do.

The laws of budgeting and economics mean that program increases or tax cuts eventually must be paid for. The pay-as-you-go rule essentially says that since this is so, it is only fair that a Congress that desires a program increase or a tax cut also should find the offset.

Pay-as-you-go Was a Highly Effective Tool in the 1990s

The pay-as-you-go approach proved very effective in the 1990s, when a statutory rule was in effect, along with a Senate procedural rule. Congress paid for all of its entitlement increases and tax cuts, including the extension of expiring measures such as the “tax extenders.” Along with a vibrant economy (which was likely helped by the federal government’s commitment to fiscal discipline), pay-as-you-go helped lead to the first federal budget surpluses in nearly 30 years. Pay-as-you-go discipline was adhered to without deviation until surpluses reemerged.

In a very real sense, we are in a deeper hole now than we were in 1990, when the original pay-as-you-go rule was enacted. Although the deficit is smaller now than it was then, we are much closer to the point where rising health care costs and demographics will cause deficits and debt to escalate sharply. Reestablishing and abiding by the pay-as-you-go rule is a very important first step in beginning to deal with that long-term problem.

It is important to note that the pay-as-you-go rule was established and maintained in the 1990s with bipartisan support. The original rule grew out of an agreement between a Republican President (the first President Bush) and a Democratic Congress. The rule was ratified and extended in 1997 by a Democratic President (Bill Clinton) and a Republican Congress. Concern over growing deficits motivated a significant number of members from both parties to support adoption or extension of the pay-as-you-go rule. As noted, the pay-as-you-go statute was adhered to without exception until 1999, when budget surpluses reappeared and seemed to be growing rapidly.[6]

Support for the rule did not reflect agreement on budget priorities — and did not need to. In both 1990 and 1997, many Republicans feared that Democrats would try to enact significant increases in entitlement programs, while many Democrats feared that Republicans would try to enact large tax cuts. The pay-as-you-go rule allowed each side to make sure that the other side could not move ahead with its priorities without paying for them.

Pay-as-you-go Does Not Prevent Program Expansions or Tax Cuts

Pay-as-you-go is not intended to — and does not — prevent entitlement expansions or tax cuts. Rather, it is intended to force proponents of entitlement expansions and tax cuts to find ways to offset the cost of their proposals. In the 1990s, it certainly prevented enactment of various spending increases and tax cuts that members of Congress concluded were not worth paying for, but it did not keep other, higher-priority entitlement expansions or tax cuts from being enacted. This was vividly illustrated in 1997, when entitlement cuts in the Balanced Budget Act of 1997 offset the cost of establishing the SCHIP program in that Act as well as the cost of tax cuts included in the Taxpayer Relief Act of 1997.

We also see in this new Congress that pay-as-you-go does not prevent action on priorities; it simply means that proponents have to find ways to pay for those priorities. We saw this at work in the higher education bill that the House recently passed. The pay-as-you-go rule did not prevent that bill from cutting the interest rate that students have to pay on subsidized loans, but did require that proponents of that policy change find ways to offset the cost. Similarly, the pay-as-you-go rule will not prevent Congress from extending alternative minimum tax relief this year, but will force the tax-writing committees to search for ways to offset the cost of that relief. Pay-as-you-go certainly makes it harder to take action to meet various priorities, but the payoff of not adding to the long-term deficit problem is worth making proponents of such actions work harder. If the proposed program expansion or tax cut is really worth enacting, it is worth paying for.

It is also important for proponents of program expansions to realize that adding to deficits now by enacting unpaid-for program expansions or tax cuts will increase the magnitude of the program cuts and tax increases that will be needed in coming years to bring exploding deficits under control. Thus, failing to abide by pay-as-you-go now will make it harder to sustain key programs and meet vital needs in the future.

Pay-as-you-go Is Not Biased In Favor of Spending and Against Tax Cuts

Despite the fact that the pay-as-you-go rule applies equally to entitlement expansions and tax cuts, the Administration and some others have argued that entitlement expansions are favored under the pay-as-you-go rules because entitlements and revenues are treated differently in the budget baseline used in determining the cost of legislation. For instance, Office of Management and Budget Director Rob Portman concluded last year that there is a bias in the baseline rules for spending and against tax relief “Because we assume that programs go out indefinitely on the spending side…. Whereas on the tax side, we assume the tax relief would not continue.”

Careful examination shows, however, that this argument is not valid. The general baseline rules treat temporary provisions of the tax code exactly the same as temporary provisions of entitlement programs. Moreover, a special rule dealing with the few cases where an entire entitlement program expires (such as SCHIP) does not give an advantage to those programs either.[7]

The general baseline rule for projecting the cost of entitlement programs (direct spending) and revenues (receipts) is set forth in section 257(a) of the Balanced Budget and Emergency Deficit Control Act of 1985, as amended.[8] The Act states that the projections of entitlement spending and revenues are to be based on the assumption that “Laws providing or creating direct spending and receipts are assumed to operate in the manner specified in those laws for each such year….”

When CBO or OMB analysts prepare a baseline projection of revenues for the next five or 10 years, they base their projection of revenues in each year on the provisions of the tax code that would be in effect in that year. That means they would take into account the fact that the 2001 tax legislation reduced most income tax rates through 2010, but provided for those rates to return to prior levels after 2010. Thus, legislation that changed current law to extend the lower rates beyond 2010 would be charged with the costs of lowering the rates in those years.

In general, the CBO analysts do the same thing when they project expenditures for entitlement programs; they take into account the provisions governing each program that would be in effect in each year under current law. For instance, since Congress has extended Medicaid’s Transitional Medical Assistance (TMA) provisions only through September 30, 2007, the baseline projections of Medicaid expenditures assume that the TMA provisions will expire on that date. Legislation to extend the TMA provisions beyond that date would be charged with the cost of the estimated increase in spending that results from extending those provisions. Neither the baseline nor the CBO scoring rules provide an advantage to the legislation to extend an expiring entitlement provision over legislation extend an expiring tax provision.

There is a special baseline rule that applies in the relatively few instances where Congress has decided that an entire mandatory program should be reexamined periodically and, to make sure the reexamination occurs, has provided that the entire program (as opposed to certain provisions of the program) will expire if legislation to extend the program is not enacted. For instance, the SCHIP program is scheduled to expire at the end of this year, which has led the current Congress to reevaluate the program. In cases where entire programs expire under current law, the baseline rules provide that projections of spending for those programs should assume that the laws governing those programs will be extended as in effect at the time of expiration.[9]

There is no similar rule in the case of taxes because the tax code does not comprise a collection of separate programs, and neither the entire tax code nor the entire personal income tax is slated to expire.[10] A temporary change in a provision within the tax code, such as a temporary provision lowering a particular tax rate, is analogous to the temporary extension of Medicaid’s TMA provision, which is assumed to expire in the baseline just as the temporary reductions in certain tax rates are. Under current law, income tax rates will change in 2011, but the income tax itself will not expire.

Most importantly, the expiring entitlement programs that are assumed to continue in the baseline receive no overall advantage relative to expiring tax-cut provisions. When estimating the costs of legislation that would establish or extend an entire entitlement program that is assumed to continue in the baseline, CBO scores the cost of that legislation for every year of the 10-year “budget window.” Congress can not make the cost of that legislation appear smaller by scheduling the new program to expire after a few years; CBO will score the costs in every year regardless. In contrast, legislation that schedules a tax-cut provision to expire is scored only for the cost of the tax cut in the years it is in effect. If both the program and the tax-cut provision are extended, the end result is the same. The full costs of both the program and the tax cut over the whole period are scored, although the full costs of the program are scored up front when it is established, while part of the cost of the tax cut is scored when it is first enacted and the rest is scored when the tax cut is extended.

To understand how this works, consider the following simple example. A new entitlement program and a tax provision are enacted at the same time. Each is scheduled to expire after two years, each is estimated to cost $5 billion over five years if extended ($2 billion in the first two years and $3 billion over the last three years), and each is then extended for three more years in later legislation.

- If the entitlement program is assumed to continue in the baseline, the original legislation establishing the program will be scored as costing $5 billion over five years, even though the program is slated to expire after two years. The subsequent legislation extending the program will be scored as having no cost.

- The original legislation containing the tax-cut provision will be scored as costing only $2 billion, while the subsequent legislation extending the provision will then be scored as costing $3 billion over the following three years.

- Thus, the new entitlement program and the tax-cut provision will each be scored as costing $5 billion over five years. The new entitlement program gained no advantage from the baseline assumption that it would be continued.

If proponents of the tax cuts believe that being charged with the cost of the tax cut in two installments is disadvantageous — even though the total cost is no greater than if the tax cuts had been treated as permanent in the baseline and the original legislation had been scored on that basis — they can avoid that outcome by making the tax-cut provisions permanent to start with. In recent years, tax-cut proponents often have purposely opted for the installment approach, because they concluded that doing so would be to their strategic advantage. Sunsetting a tax cut after a few years can make the cost appear lower when the tax cut is first considered, making it possible to pass larger tax cuts than would otherwise be possible.[11] Once the larger tax cut has been passed, its proponents then argue that it must be extended to avoid subjecting the public to a “tax increase."

Requiring the Cost of Tax Cuts To Be Offset Will Not Damage the Economy

The argument that not extending expiring tax cuts will damage the economy, or that enacting other new tax cuts will boost the economy, is used by some to argue that the pay-as-you-go rule should not apply to tax cuts. In its most extreme form, the argument is that applying the pay-as-you-go rule to tax cuts does not make sense because tax cuts pay for themselves — that is, that tax cuts boost the economy so much that revenues are higher than they would have been without the tax cuts.

In reality, tax cuts do not have such magical effects. There is agreement among mainstream economists that tax cuts generally have relatively modest long-term effects on the economy — other factors are much more important in determining the performance of the economy — and that, even under the best of circumstances, they do not boost the economy enough to come remotely close to paying for themselves.

Perhaps most importantly, mainstream economic analysis shows that the potential negative effects on the economy of higher tax rates (or the potential positive effects of lower tax rates) are smaller than the negative effects of allowing persistent, large deficits. This point was underscored in a recent response by the Congressional Budget Office to questions posed by Senate Budget Committee ranking Member Judd Gregg (R-NH) about the effects of raising taxes or cutting spending to achieve a sustainable long-term fiscal path. CBO explained:

“Differences in the economic effects of alternative policies to achieve a sustainable budget in the long run are generally modest in comparison to the costs of allowing deficits to grow to unsustainable levels. In particular, the difference between acting to address projected deficits (by either reducing spending or raising revenues) and failing to do so is generally much larger than the implications of taking one approach to reducing the deficit compared with another.”[12]

This is consistent with CBO’s earlier finding that, if deficit financed, a 10-percent across-the-board cut in income tax rates could potentially reduce economic output.[13] It is also consistent with the a letter CBO sent to Chairman Spratt last week on the cost of the 2001 and 2003 tax cuts, which concluded that “at this point in time (several years after enactment),…the overall impact of the tax legislation [on the economy] is likely to be modest….” and that, when that impact is taken into account, the actual cost of the tax cuts is likely to be about the same as the official cost estimates made at the time of the tax cuts’ enactment (which did not take economic feedback effects into account).[14] Similarly, in an analysis of the effects of reductions in individual and corporate tax rates that are deficit financed, the Joint Committee on Taxation found that: “Growth effects eventually become negative without offsetting fiscal policy [i.e. without offsets] for each of the proposals, because accumulating Federal government debt crowds out private investment.”[15] And, in an analysis of the argument that the tax cuts enacted in 2001 and 2003 cost less than was estimated at the time of enactment because they boost economic growth, the Congressional Research Service concluded in a September 2006 report that, “at the current time, as the stimulus effects have faded and the effects of added debt service has grown, the 2001-2004 tax cuts are probably costing more than expected.”[16]

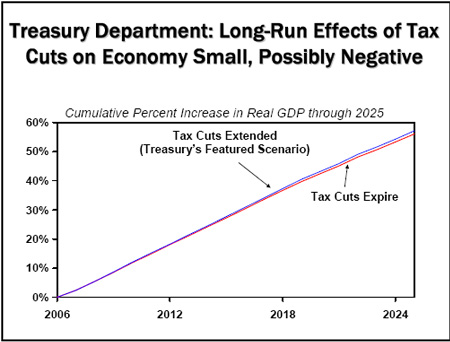

Even the Bush administration has concluded that the long-term economic effect of the tax cuts will be quite small if they are made permanent. A Treasury Department study found that making the 2001 and 2003 tax cuts permanent would increase the size of the economy over the long run (i.e., after many years) by only 0.7 percent — and that even this small growth increment would occur only if the tax cuts were paid for in full by unspecified cuts in government programs.[17]

As an indication of how modest a long-term increase in the economy of 0.7 percent would be, if it took 20 years for the increase to fully manifest itself (Treasury officials indicated it would take significantly more than 10 years but were not more specific than that), this would mean an increase in the average annual growth rate for 20 years of four-one hundredths of one percent — such as 3.04 percent instead of 3.0 percent. Such an effect is so small as to be barely perceptible. Moreover, after the 20 years (or whatever length of time it would take for the 0.7 percent increase to show up), annual growth rates would return to their normal level — that is, they would be no higher than if the tax cuts had been allowed to expire.

Congressional and executive branch economic experts are not the only ones to reach the conclusion that deficit-financed tax cuts are unlikely to substantially boost long run economic growth. University of California economist Alan Auerbach, a noted expert in fiscal policy, simulated the economic effects of the 2001 reductions in marginal tax rates, increase in the child tax credit, “marriage penalty relief,” and AMT relief under various financing assumptions. He found that the only scenario under which the tax cuts increased the size of the capital stock and thus increased long-run economic output was one in which they were fully paid for with spending cuts at the time they were enacted. Auerbach concluded that “whatever its benefits, the tax cut [enacted in 2001] does not offer the promise of enhancing savings and expanding output in the long run.”[18]

The clear conclusion is that whatever long-term economic benefits tax cuts might offer, those benefits will only be realized if the cost of the tax cuts is offset — that is, if enactment of the tax cuts is consistent with pay-as-you-go discipline. The potential for economic benefits from tax cuts if they are paid for offers support for the principle that tax cuts should be subject to pay-as-you-go, rather than for the argument that tax cuts should be exempt from such fiscal discipline.

Enacting a Statutory Pay-as-you-go Rule Would Help Promote Adherence to Pay-as-you-go

Finally, I would like to briefly discuss why enacting a statutory pay-as-you-go rule would be helpful. The House and the Senate have already taken the most important step toward establishing pay-as-you-go discipline by imposing rules that prohibit consideration of legislation that would increase entitlement spending or cut taxes if the costs of those actions are not offset. Establishing a statutory pay-as-you-go rule backed up by sequestration would not dramatically enhance the effectiveness of those rules. (Congress could include a waiver of the statutory pay-as-you-go requirement in future legislation, just as it can waive its own rules to consider legislation that violates pay-as-you-go.)

Nevertheless, enacting a statutory pay-as-you-go rule could add force to the Congressional rules by emphasizing the importance of adherence to pay-as-you-go and, in particular, by making it harder for future Congresses to quietly back away from adherence to pay-as-you-go. Once pay-as-you-go was written into law, it could be removed from the law (before its scheduled expiration date if there were one) or set aside on a case-by-case basis only by enactment of a statute that would require the assent of the President and, most likely, support from a supermajority in the Senate to become law. A statutory pay-as-you-go requirement also could have the virtue of improving the budgeting culture in Executive Branch agencies by reinforcing the idea that, when entitlement expansions or tax cuts are discussed, a key question should be “how will the costs be paid for?”

Conclusion

Enactment of a statutory pay-as-you-go rule would be highly desirable. But whether a statutory rule is established or not, what is of most importance is that Congress maintain a commitment to adhere to pay-as-you-go discipline even when living by that rule is not easy. Given the bleak long-term fiscal outlook for the nation, we cannot afford for Congress to do otherwise.

End Notes:

[1] “The Long-Term Budget Outlook,” Congressional Budget Office, December 2005.

[2] “The Nation’s Long-Term Fiscal Outlook: April 2007 Update,” Government Accountability Office, April 2007.

[3] “Mid-Session Review of the Budget of the United States: Fiscal Year 2008,” Office of Management and Budget, July 11, 2007, p. 6.

[4] Richard Kogan, Matt Fiedler, Aviva Aron-Dine, and James Horney, “The Long-Term Fiscal Outlook is Bleak: Restoring Fiscal Sustainability Will Require Major Changes to Programs, Revenues, and the Nation’s Health Care System,” Center on Budget and Policy Priorities, January 29, 2007.

[5] The projections do assume that current relief from the Alternative Minimum Tax will be extended without offsets, because the AMT would practically replace the regular income tax by 2050 if the relief were not extended.

[6] During the 1990s, every entitlement increase and tax cut was paid for. The only exception occurred in 1993, at a time when unemployment remained high, when the final six-month continuation of “extended unemployment benefits” was declared an emergency by both Congress and the President and for that reason was not subject to the PAYGO statute.

[7] For a more detailed discussion of this issue, see James Horney and Richard Kogan, “Key Argument Against Applying Pay-As-You-Go to Tax Cuts Does Not Withstand Scrutiny,” Center on Budget and Policy Priorities, March 22, 2007.

[8] The current rules were essentially established in the Budget Enforcement Act of 1990, which amended the Balanced Budget Act, and are often called the “BEA” baseline rules.

[9] The special rule only applies to programs that cost more than $50 million a year, and applies to a program established after 1997 only if he House and Senate Budget Committees have determined at the time of enactment that the programs should be assumed to continue.

[10] There is a special rule that says that expiring excise taxes that are dedicated to a trust fund should be assumed to continue. This could be viewed as one case where a set of taxes constitute a program. More importantly, these taxes fund highway and transit programs that expire under current law but are assumed to continue in the baseline.

[11] Sunsetting 2001 tax cuts that were intended to be permanent was one of a number of gimmicks used in a process that former Ways and Means Committee Chairman Bill Thomas described as an effort “to get a pound and a half of sugar in a one-pound bag.” From “News Conference with Representative Bill Thomas, Chairman of the House Ways and Means Committee,” Federal News Service Transcript, March 15, 2001.

[12] Congressional Budget Office, “Financing Projected Spending in the Long Run,” attachment to letter to Senator Judd Gregg, July 9, 2007, p. 1.

[13] Congressional Budget Office, “Analyzing the Economic and Budgetary Effects of a 10 Percent Cut in Income Tax Rates,” December 1, 2005.

[14] CBO estimated that the cost of the 2001 and 2003 tax cuts, incorporating economic feedback effects, is roughly $195 billion to $215 billion (including debt-service costs), compared with the official estimate (without feedback effects) of $211 billion. Letter of July 20, 2007, from Peter R. Orszag, Director of the Congressional Budget Office, to House Budget Committee Chairman John M. Spratt, Jr.

[15] Joint Committee on Taxation, “Macroeconomic Analysis of Various Proposals to Provide $500 Billion in Tax Relief,” JCX-4-05, March 1, 2005.

[16] Jane G. Gravelle, “Revenue Feedback from the 2001-2003 Tax Cuts,” Congressional Research Service, September 27, 2006.

[17] Department of Treasury, “A Dynamic Analysis of Permanent Extension of the President’s Tax Relief,” July 25, 2006. For a more detailed discussion of the Treasury study, see Jason Furman, “Treasury Dynamic Analysis Refutes Claims by Supporters of the Tax Cuts,” Center on Budget and Policy Priorities, revised August 24, 2006.

[18] Alan J. Auerbach, “The Bush Tax Cuts and National Saving,” National Tax Journal, September 2002. |