July 18, 2003

SANITIZING THE GRIM NEWS:

The Administration's Efforts to Make Harmful Deficits Appear Benign

By

Richard Kogan and

Robert Greenstein

| PDF of this report |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

The Administration has attempted to downplay the

mushrooming

Do Deficits Shrink Over Time?

In the Administration’s just-released Mid-Session Review, deficits are projected to shrink from $455 billion in 2003 to $226 billion in 2008, or from 4.2 percent of Gross Domestic Product this year to 1.7 percent in 2008.[1] The 4.2 percent of GDP deficit in 2003 — and the deficits in general — are described as manageable, while cutting the deficit in half by 2008 is portrayed as a victory. This treatment is misleading in several respects.

In short, the Administration’s new budget forecast significantly understates the expected deficits in future years. There surely will be some reduction in deficits in the years immediately after 2004; all budgets recover to some extent when the economy rebounds, and deficits should recede as the economy pulls out of its current slump. The question here is how much the deficits will recede and for how long. Realistic projections suggest the deficit will not fall below $300 billion in any year.

| start | end | change | |

| 2003 to 2008, CBPP est. | 4.2% | 2.6% | -1.6% |

| 2003 to 2008, OMB est. | 4.2 | 1.7 | -2.5 |

| 1992 to 1997 | 4.7 | 0.3 | -4.4 |

Most important, as discussed in the next section of this analysis, without major changes in policy, the reduction in deficits after 2004 will be only a temporary phenomenon. As the baby-boom generation begins retiring after 2008 and additional tax cuts such as estate-tax repeal take effect, deficits will start growing again and eventually surpass the 2003 and 2004 levels.

Are the Current High Deficits a Temporary Phenomenon?

OMB’s figures imply that the high deficits in 2003 and 2004 are temporary. Unfortunately, it is the dip in the deficit in years after 2004 that is a temporary phenomenon. Had OMB projected its budget policies over a period longer than five years, the temporary nature of the improvement would be clear.

Indeed, OMB’s own figures show a small increase in the deficit from 2007 to 2008. Our estimates of the cost of current budget policies (assuming the continuation of current tax cuts, AMT relief, and funding of the Administration’s multi-year defense plan, as discussed above) show deficits rising from more than 2 percent of GDP in 2007 to 3 percent of GDP in 2013. And after 2013, deficits will go on rising.

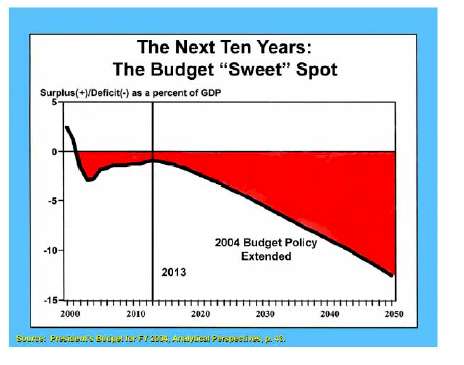

The leading edge of the baby-boom generation

becomes eligible to start drawing Social Security benefits in 2008 and

Medicare benefits in 2011. As the years pass and the baby boomers’

retirement accelerates, the

The budgetary effects of these rising costs are easy enough to understand — they portend rising deficits. In the Administration’s own budget issued in February, OMB included a graph showing spiraling deficits as the baby boomers retire. (See the graph. The graph is taken from the President’s budget, although the title at the top of the graph is not.) With OMB now projecting much higher deficits than it did in February, the deficits will be larger in all years than is shown in the graph, and the deficit will start growing again in 2008, rather than in 2013.

In short, claims that current deficits are “manageable” miss the point. The deficits are not harming the nation now, while the economy is weak. But focusing on that point diverts attention from the central issue. The question is not whether the credit markets are willing to finance a high level of deficits temporarily during an economic slump. The question is whether the nation is able to finance the persistently high level of deficits we now face over the long term and for as far as the eye can see. The answer is no. The current fiscal policy path is neither manageable nor sustainable.

Tax Cuts or Spending Increases?

Some people engage in sophistry, implying that since a deficit means expenditures exceed revenues, by definition this means that “excess spending” must be the cause of deficits. This makes little sense. If spending is cut but taxes are cut even more, deficits will increase. By the reasoning that some policymakers are now employing, the resulting deficits would still be spending-driven because spending would exceed revenues.

An honest assessment of the relative role that

tax cuts and program increases have played in contributing to the

deterioration of the budget over the past 2½ years requires estimating the

cost of legislation enacted since the start of 2001. OMB presents such an

analysis in the Mid-Session Review. OMB seeks to draw attention to what

that analysis shows for fiscal year 2003, a year when the costs of program

increases — such as the fighting in

It is more useful, however, to examine the relative role of tax cuts and program increases for the period from 2002 through 2008. After all, it is not deficits in 2003 that should concern us; deficits while the economy is weak are not a problem. It is the persistence of large deficits after the economy recovers that represents the budgetary threat.

OMB’s own figures in the Mid-Session Review show that tax cuts account for 54 percent of the cost over the 2002-2008 period of all legislation that has been enacted since the Administration took office or that the Administration is now proposing. In other words, under Administration policies, tax cuts will account for the majority of the deterioration in the budget caused by actions taken by policymakers.

|

|

2002-2008 |

Share, attributable to legislation |

|

Baseline surpluses projected by OMB in February 2001 |

3,195 |

|

|

Economic and technical re-estimates |

-2,484 |

|

|

Enacted tax cuts |

-1,291 |

46% |

|

Proposed tax cuts |

-217 |

8% |

|

Enacted programs increases (primarily defense, homeland) |

-979 |

35% |

|

Proposed program increases (primarily defense, Rx drugs) |

-289 |

10% |

|

Subtotal, enacted and proposed legislation |

-2,780 |

100% |

|

Resulting deficits in the President’s Budget |

-2,069 |

|

| Columns may not add due to rounding. Estimates for all budget changes include the associated increase in interest payments. | ||

Moreover, as noted above, OMB’s figures stop in 2008. All independent analyses show deficits growing after 2008. Such analyses also show that several tax cuts enacted in 2001 which are slated to expand after 2008 are one of the reasons that deficits will widen in those years. Under the 2001 tax-cut law, three provisions of the tax code that affect high-income individuals — the estate tax, the phase-out of the personal exemption for taxpayers at high income levels, and the limit placed on itemized deductions for high-income taxpayers —are all repealed in years after 2008. This adds substantially to the revenue losses projected in these years. The cost of AMT relief also will mount in these years.

By contrast, some of the spending increases that

show up in the 2003 and 2004 budget figures — and that are among the reasons

that tax cuts and expenditure increases contribute about equally to the

budget deterioration in 2003 — are temporary. These include the extension

of unemployment benefits (which always occurs during an economic downturn

and ends when the economy recovers), temporary fiscal relief to states that

are now facing their worst fiscal crises in 50 years, and the costs of

fighting a war in

In other words, under Administration policies, nearly all of the tax cuts enacted in 2001 and 2003 will be maintained and some will grow larger. Meanwhile, some of the spending increases that are in place in 2003 are temporary in nature, and their costs will recede in the years ahead. To be sure, the costs of a prescription drug benefit will grow in future years, as will defense expenditures if the Administration’s future-year defense plan is fully funded. But the cost of tax cuts is expected to grow faster than the cost of spending increases. As a result, in future years, tax cuts will be responsible for a significantly larger share of the deterioration in the budget than spending increases. We estimate that by 2011, tax cuts will account for 57 percent of the budget deterioration caused by legislation, relative to the budget projections made in 2001.[5]

Revenues and Spending in Historical Perspective

|

in 2002-2004 |

20.1% |

|

in 1991-1992 |

22.3% |

|

in 1982-1983 |

23.3% |

|

in 1975-1976 |

21.4% |

|

* The budgetary effect of a recession usually lasts a year or so after the official end of the recession. |

|

If the deficits truly are spending-driven with tax cuts playing little role, one would expect federal spending now to be high in historical terms. This is not the case. Measured as a share of the economy, federal expenditures today are low for a high-unemployment period. The Mid-Session Review shows that federal expenditures will equal 20.6 percent of the GDP in 2003 and 20.2 percent of GDP in 2004. In each of the last three economic downturns, federal expenditures were considerably higher. Expenditures averaged about 22.3 percent of GDP in 1991-1992, about 23.3 percent of GDP in 1982-1983, and about 21.4 percent of GDP in 1975-1976. Indeed, federal expenditures will be lower in 2003 and 2004, as a share of the economy, than they were in any year from 1980 through 1995.[6]

What stands out in examining the new OMB figures is not that expenditures are unusually high but that revenues are unusually low. The new OMB estimates show that federal revenues this year will be at their lowest level as a share of GDP since 1959. In fiscal year 2004, according to the OMB figures, federal revenues will be at their lowest level as a share of GDP since 1950.

|

2003 |

average, 1962-2001 |

|

| Expenditures |

20.6% |

20.6% |

| Revenues |

16.3% |

18.7% |

| Deficits |

4.2% |

1.9% |

|

Columns may not add due to rounding |

||

Moreover, revenues will remain at these historically low levels even after the economy recovers. We project that over the next ten years (2004-2013), revenues will be at a lower level than the average levels for the 1960s, 1970s, 1980s, and 1990s. The role of the tax cuts in shrinking the nation’s revenue base can clearly be seen in these figures.

By contrast, the OMB figures show that when expenditures peak at 20.6 percent of GDP in 2003, they will simply be at their average level for the period from 1962 through 2001.

A final point is that many of the recent spending increases that have been instituted are not truly elective. The nation had little choice but to rebuild after 9/11 or to strengthen homeland security. Large, permanent tax cuts do not qualify as necessities for the nation in the way that some of the spending increases do.

End Notes:

[1]

Office of Management and Budget, Mid-Session Review, Budget of the

[2]

N. Gregory Mankiw, Deficits and Economic Priorities, op-ed in the

Washington Post,

[3]

See Steven M. Kosiak, Cost Growth in Defense Plans, Wars and

Occupation of

[4]

These figures are from backup tables supporting CBO, A 125-Year

Picture of the Federal Government’s Share of the Economy, 1950 to 2075,

[5] In addition to legislation assumed in the President’s budget, our figure for 2011 assumes AMT relief, extension of “50 percent bonus depreciation” for businesses, full funding of the Administration’s “future-year defense plan,” domestic appropriations at current levels (adjusted for inflation and a growing population), and spending for natural disasters at the historical average level.

[6]

Expenditures have grown from their 2000-2001 levels, but those levels —

about 18.5 percent of GDP — were the lowest levels of expenditure since

1966, when Medicare and Medicaid were in their infancy.