Women’s Retirement Income, The Case

for Improving Supplemental Security Income

by Kilolo

Kijakazi

Prepared for the 2001 Institute for

Women's Policy Research Annual Conference

June 8, 2001

Introduction

| PDF version If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Social Security has been accurately credited with being highly effective in reducing poverty among the elderly. The program is responsible for removing more people from poverty than all other government programs combined. Yet the labor experiences of some individuals place them at risk of being poor when they grow old, even after receiving Social Security. Women are among those at risk.

In 1998, the poverty rate for individuals age 65 and older declined from approximately 46 percent before Social Security to 12 percent after the receipt of Social Security (and other social insurance benefits).(1) About 3.8 million seniors were poor after receiving Social Security.(2) Some of the individuals at greatest risk of experiencing poverty during their old age include unmarried women. One fifth of elderly unmarried women and one third of elderly women of color were in poverty in 1998. The poverty level for elderly unmarried women equals the poverty rate for children in this country and the level for elderly women of color exceeds the rate for children.

Improvements can be made within Social Security to reduce poverty further among elderly individuals in these and other communities. Social Security alone, however, cannot compensate completely for the labor-market factors that result in lower retirement income for women. In addition to improvements in Social Security, changes also are needed in the Supplemental Security Income program — a means-tested program that serves the elderly, blind, and disabled.

Retirement Income and the Economic Status of Women

Women are more likely than men to be poor as they grow older. Without Social Security, 51.4 percent of women age 65 and older would have been poor in 1998, compared to 39.7 percent of elderly men.(3) As a result of receiving Social Security benefits, the proportion of the elderly living in poverty was reduced to 14 percent for women and approximately 8.4 percent for men. Social Security greatly reduced poverty for both genders, but the percentage of women remaining in poverty was nearly twice the percentage of elderly men.

Not only does financial well-being vary by gender, but the financial well-being of women also differs markedly by marital status, race, and ethnicity.

Married and Unmarried Elderly Women

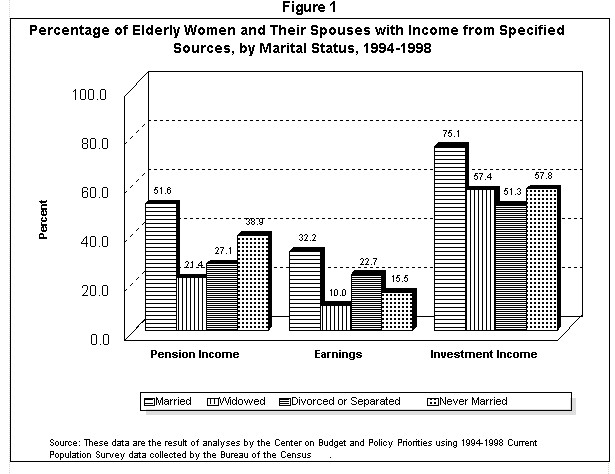

Among elderly women, unmarried women are at greater risk financially largely because they are less likely to receive income from pensions, earnings, or investments than married women. Married women have access to their husbands' income from pensions, earnings, and investments in addition to their own income from these sources.(4) Figure 1 shows the percentage of elderly women who received retirement income from each of these sources during the period from 1994 to 1998. Some 51.6 percent of married women and their spouses had pension income while only 21.4 percent of widows, 27.1 percent of divorced or separated women, and 38.9 percent of never-married women had pension income.

The receipt of earnings and investment income by elderly women also varies by marital status. Figure 1 shows that elderly married women were more likely to have income from earnings than elderly women who were widowed, divorced or separated, or never married. Elderly married women were much more likely to have investment income than any other group. Women of every marital status were more likely to have investment income than earnings or pensions.

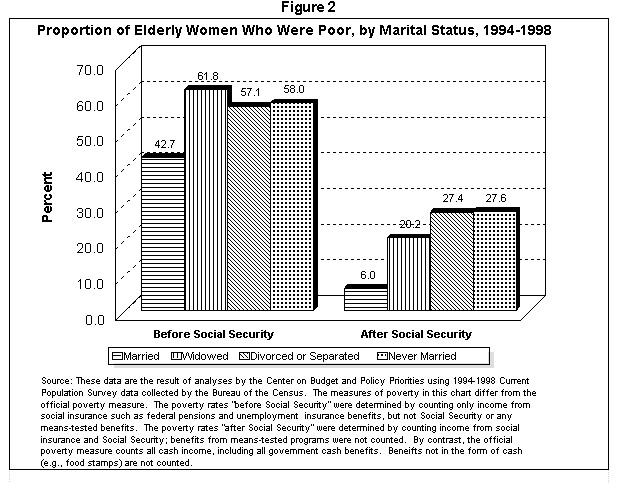

Given the lower rate of receipt of income from pensions, earnings, and investments by unmarried women compared to married women, one might expect unmarried women to have a higher incidence of poverty than married women. Figure 2 illustrates that this is the case. Before counting Social Security, 61.8 percent of elderly widows were poor during the period from 1994 to 1998, as were 57.1 percent of divorced and separated women and 58 percent of women who never married. By comparison, 42.7 percent of married women were poor before receiving Social Security.

Social Security reduced poverty substantially for women of every marital status. Figure 2 shows that the program lowered poverty rates for married women to just six percent, and cut the percentage of women in poverty by more than half for each unmarried category. (Using the official poverty measure, poverty rates were 18.6 percent for elderly widows, 23.9 percent for divorced or separated women, 24.7 percent for never-married women, and 5.1 percent for married women.)

Several components of the Social Security system help to remove women from poverty. The progressive benefit formula favors women because they have lower lifetime earnings than men, on average, due to a combination of labor-market factors. Women are disproportionately represented among low-wage workers. While women accounted for about 48 percent of all workers in 1996, they made up 58 percent of minimum-wage workers.(5) Women also were more likely to be part-time workers. In 1999, some 62 percent of all part-time workers were women.(6) Women also spent 12 fewer years in the labor market than men, on average. This absence from the labor market often reflects time spent caring for family members.(7) The progressive benefit formula helps to counteract the effect of these employment experiences by replacing a larger share of pre-retirement earnings for women than men, on average. In December 1997, women received 53 percent of all Social Security retirement and survivors benefits, but paid only 38 percent of payroll taxes.(8)

Women also are assisted more than men by the annual cost-of-living adjustment (COLA). Social Security benefits are increased each year to keep pace with inflation. The COLA is particularly important for women because they have a longer average life span than men. A 65-year-old woman is expected to live to 84, while a 65-year-old man's anticipated life span is 80.(9) Unlike most other sources of income for women, which dwindle as they grow older, Social Security benefits rise each year to maintain their purchasing power.

Auxiliary Social Security benefits, including spouse and survivors benefits, provide another fundamental source of protection for many married and widowed individuals, typically women. An elderly married woman can receive either a benefit based on her own earnings history or a spouse benefit equal to 50 percent of her husband's benefit, whichever is larger. (If the husband were the lower-wage earner, he would qualify for the spouse benefit instead of the wife.) An elderly woman who outlives her husband can receive a survivors benefit based on her own earnings history or an amount equal to 100 percent of her deceased husband's benefit, whichever is greater.

Social Security is favorable to women across marital categories, but it is most advantageous to married women. The Social Security income a married couple receives is at least 150 percent of the benefit for the higher earner.

Elderly Women of Color

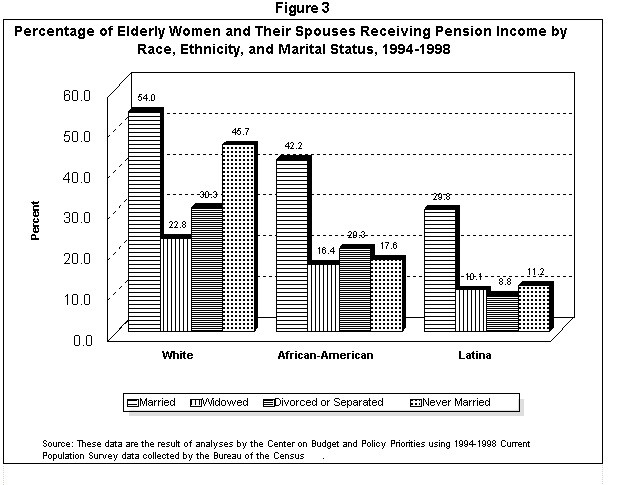

Women of color are some of the elderly individuals at greatest risk of having insufficient retirement income. The proportion of women with pension income varies by race, by ethnicity, and by marital status within each racial or ethnic group (see Figure 3). Elderly white women were the most likely to receive pension income in 1994-1998, followed by African-American women and Latinas. Married women had the highest rate of pension receipt regardless of race or ethnicity. (If a married woman does not have pension income, but her husband does, his pension income counts as income for her.) Among elderly white women, widows lagged behind women in all other marital categories in receipt of pension income. For African-Americans and Latinas, the percentages of widows, divorced or separated women, and never-married women who received pension income were about the same.

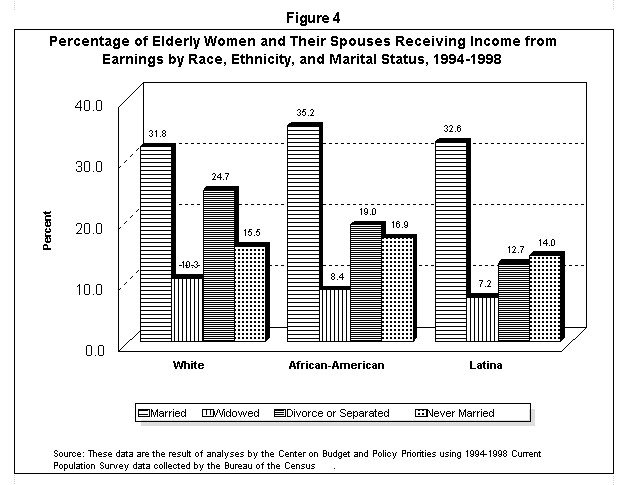

Income from earnings was received by a comparable proportion of white, African-American and Latina women within most marital categories (see Figure 4). For example, the percentage of married women with income from earnings was similar for whites, African-Americans and Latinas. (Income from earnings for married women includes their husbands' earnings. Women who do not work will have earnings income counted if their husbands have earnings.) The same was true for widows and never-married women. There was greater variation among divorced or separated women. The percentage of such women with income from earnings was only about half as high among elderly Latinas as among elderly white women.

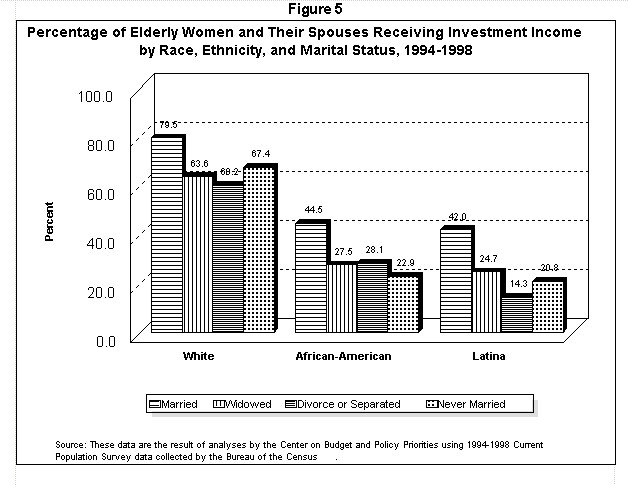

Receipt of income from investments — interest, dividends, and rent — varied markedly by race and ethnicity as well as marital status (see Figure 5). Elderly white women were much more likely to have investment income than African-Americans or Latinas. In addition, the proportion of elderly married women who had investment income was notably higher than the proportion of unmarried or separated women. (If a married woman does not have investment income of her own, but her husband has investment income, her husband's income is counted as her investment income.) The likelihood of having investment income ranged from nearly 80 percent for elderly married white women to less than 20 percent for divorced or separated Latinas.

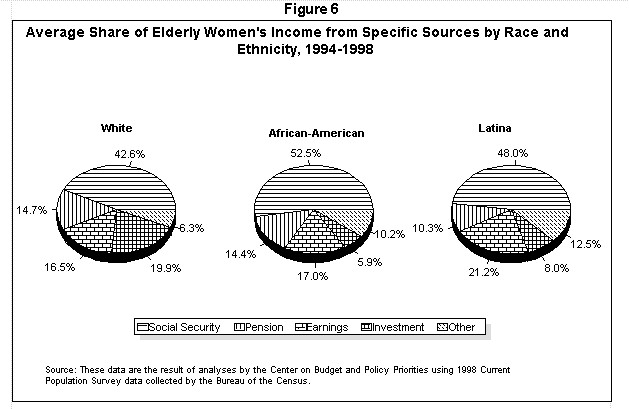

Social Security is by far the most prevalent source of income for elderly women. Figure 6 shows that from 1994 to 1998, Social Security accounted for an average of 42.6 percent of the income of elderly white women and their spouses, 52.5 percent of the income of African-American women and their spouses, and 48 percent of the income of Latinas and their spouses. For each of these groups, the share of income received from Social Security was almost twice as great as the share of income from any other source.

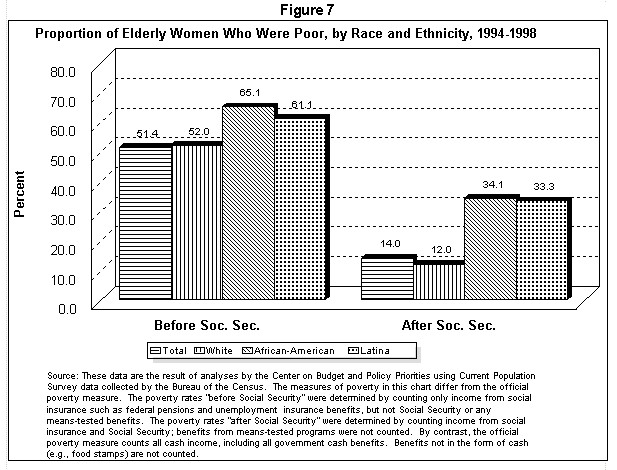

The relatively lower rates of income received from pensions, earnings, and investments by elderly women of color coincide with higher rates of poverty compared to elderly white women. Before receiving Social Security, 52 percent of elderly white women were poor during the period from 1994 to 1998, compared to 65.1 percent of African-American women and 61.1 percent of elderly Latinas (see Figure 7).(10) Social Security benefits reduce poverty by nearly 50 percent for African-American women and Latinas and by substantially more than that for white women. However, the proportion of elderly women remaining in poverty was nearly three times greater for African-Americans (34.1 percent) and Latinas (33.3 percent) than for whites (12.1 percent). (Using the official poverty measure, poverty rates were 30.3 percent, 27.2 percent, and 11.1 percent for elderly African-American women, Latinas, and white women, respectively.)

Improvements Needed in the Supplemental Security Income Program

The varied paths that may lead a woman to poverty in the later years of her life suggest that several improvements are needed to enhance the economic status of poor elderly women. The remainder of this paper will examine several proposals to reduce elderly poverty by improving SSI.

A number of proposals have been advanced for improving the Social Security program to enhance the financial well-being of elderly individuals who are susceptible to poverty. In addition to enhancing Social Security benefits, there are other steps that can be taken that will not cause Social Security costs to rise. Rather than relying solely on Social Security to improve the financial well-being of elderly people who remain in poverty, adjustments can be made in the SSI program. Established through legislation proposed by President Nixon and enacted in 1972, SSI is a means-tested, federally administered program that provides cash benefits for low-income aged, blind, and disabled individuals. Certain changes in SSI could improve the income of elderly individuals with very low incomes without exacerbating the long-term financial imbalance in Social Security, since SSI is financed with funds from the non-Social Security budget.

There is a second reason to modify the SSI program. Two proposals that are frequently offered for improving Social Security benefits — increasing surviving spouse benefits and implementing an effective minimum benefit — would cause some widows who would have been eligible for SSI under the current Social Security rules to be ineligible as a result of their increased Social Security income. Each additional dollar of Social Security income received by a SSI participant results in a dollar reduction in his or her SSI benefits. For some SSI participants, the increased Social Security benefit would push their income over the SSI income eligibility limit. This is of particular importance because Medicaid eligibility for the elderly is tied to receipt of SSI in most states. (In some states, Medicaid eligibility criteria are more restrictive than SSI eligibility rules. States also have the option of setting eligibility criteria that are more liberal than SSI eligibility rules.) Thus, a widow whose Social Security benefit rises as a result of an increase in the surviving spouse benefit might lose SSI eligibility and, as a result, also lose her Medicaid coverage. Adjustments should be made in the SSI program to address unintended interactions resulting from improvements in Social Security.

Finally, changes in SSI are needed in the rules governing the type and amount of assets that an individual may own and still be eligible for the program. There is a need to both modernize these rules and adjust the asset limits for inflation.

Fortunately, the Social Security Administration released a report in 2000 that does an excellent job of describing the components of SSI that are used to determine program eligibility and benefit levels.(11) The report demonstrates that several components of the SSI eligibility and benefit structure have eroded because they have not adequately kept pace with inflation. It also presents options for modernizing the program in these areas, along with cost estimates. This section of the paper incorporates some of the information in the SSA report.

Improve SSI's General Income Exclusion

While some elderly women become poor as the result of an event such as the death of their husband, a study by Sharmila Choudhury and Michael Leonesio of the Social Security Administration showed that the most important determinant of poverty among elderly women is their poverty status prior to reaching old age.(12) Women who experience spells of poverty at younger ages are more likely to be poor when they get older. Women who did not experience poverty are not likely to become poor when they are elderly, even after a catastrophic event. This research suggests that women who have been in the labor market but earned low wages and were poor prior to retirement are more likely to be in poverty when they are elderly. Similarly, women who were married to men with low wages may be at greater risk of poverty when they grow old.

The SSI program assists elderly and disabled men, women, and children who are susceptible to poverty. To be eligible for the program, an individual must be at least 65 years old, blind, or disabled. Nearly one-third of SSI beneficiaries were 65 or older in 1998.(13) Program eligibility is also based on income and asset limits. SSI is intended to be a "program of last resort," and nearly all other income that an applicant receives is considered before SSI eligibility is determined.(14) Under the rules governing the federal SSI program, individuals and couples are eligible for federal SSI benefits if their countable incomes fall below the maximum monthly federal SSI benefit, which is $530 for individuals and $798 for couples in 2001.

Not all income is counted in determining SSI eligibility. Twenty dollars per month of unearned income is excluded.(15) This is called the general income exclusion (GIE) and was originally intended to reward past work by ensuring that beneficiaries receiving Social Security income would have a higher total income than beneficiaries without income from Social Security.(16) An additional $65 of earned income plus 50 percent of any remaining earnings also are excluded. This is called the earned income exclusion and is intended to encourage current work by providing a higher total income to low-income beneficiaries with earnings.

By way of example, an elderly individual whose only source of income is a Social Security benefit of $450 a month would be eligible for an SSI benefit of $100. (The Social Security benefit of $450 minus the $20 GIE equals $430. When the $430 is subtracted from the SSI maximum benefit of $530, the remaining $100 is the SSI benefit amount.) In 1998, some 61 percent of elderly SSI beneficiaries received Social Security retirement benefits and, consequently, received the $20-a-month general income exclusion.(17)

The SSI program is an important source of income for the elderly, but the program can be made more effective in reducing poverty by increasing this GIE. The $20 GIE was established when the original SSI law was enacted in 1972. It has not been adjusted since then to keep pace with inflation. The Social Security Administration's recent report states:

The $20 GIE amount as enacted in 1972, is now worth $5 [in 2000 dollars]. Therefore its significance as recognition of past work is substantially reduced. As a result, the value of SSI benefits has declined for many beneficiaries. In 1974, the $20 exclusion represented over 14 percent of the $140 Federal benefit rate (FBR) for an individual. The Federal benefit rate is the maximum SSI benefit level. By contrast the $20 exclusion is less than 4 percent of the current $512 FBR for an individual.(18)

Effect of the Low SSI GIE on Total Income Ms. Harris, a minimum wage worker, retired at 62 and began to receive Social Security benefits. At age 65, she became eligible for SSI.

If Ms. Harris had not worked at all, she would have received a benefit of $530 from SSI. |

The consequence of maintaining such a low GIE is that a retiree who worked steadily but earned low wages could have a combined Social Security and SSI benefit that is only slightly larger than the SSI benefit the retiree would have received if he or she had not worked at all. For example, Ms. Harris worked hard all of her adult life but earned the minimum wage throughout her work life (see box). The jobs she held were physically arduous, and she retired at age 62 in 1998. Ms. Harris' only source of income was Social Security until she turned 65 and became eligible for SSI benefits. Her Social Security benefit is $539 in 2001.(19) Therefore, she receives a SSI benefit of $11 per month, making her total income $550. Had Ms. Harris not worked at all and had no Social Security income, she would have received an SSI benefit of $530. Her hard work reaped only $20 more per month than not working, and her income level fell well below the poverty threshold. This is inconsistent with the bipartisan goals of encouraging and rewarding work.

Two principles that have enjoyed bipartisan support are that individuals who work should not be poor and those who work should be significantly better off than those who do not. Toward that end, Presidents Reagan, Bush, and Clinton and members of Congress have developed and improved programs such as the Earned Income Tax Credit (EITC) to increase the income of the working poor. In that same vein, individuals who have worked hard but received low wages for the better part of their working lives — and individuals (typically women) who have taken time out of the labor market or worked part time to raise children or care for an infirm elderly relative — should not be consigned to a life of poverty in their later years.

One means of raising the level of income for individuals with a history of low wages is to increase the GIE.(20) Raising the GIE would reduce the amount of Social Security income counted in determining SSI eligibility and benefits. Consequently, SSI benefits for poor Social Security beneficiaries would rise. If the GIE were adjusted to account for inflation since 1972, the updated amount would be approximately $80.(21) A GIE of this level would substantially improve the financial well-being of low-income elderly individuals. According to the Social Security Administration report:

Example of Social Security's Impact on SSI and Medicaid Eligibility Mrs. Carver is the widow of a minimum wage worker who retired at age 62. When the Carvers turned 65, they became eligible for SSI and had the following income:

When Mr. Carver died, the following adjustments were made to Mrs. Carver's income.

If Mrs. Carver received a Social Security survivors benefit equal to 75 percent of what the couple would have received, she would receive a $593 Social Security benefit, but she would become ineligible for SSI and consequently could lose Medicaid coverage. By contrast, if the SSI general income exclusion were raised to $80, Mrs. Carver would maintain her eligibility for SSI and Medicaid and she would have a larger total income that would bring her closer to the poverty line (although she still would be below it).

|

Such an increase would enable those SSI beneficiaries who are also receiving Social Security benefits and other unearned income to retain more of their SSI benefit, and would restore the exclusion to its original congressional intent by more tangibly rewarding past work.(22)

The $80 general income exclusion also would preserve SSI eligibility and, therefore, Medicaid coverage for some elderly women if the Social Security survivors benefit is increased (see box on page 17).

Beyond raising the GIE from $20 to $80 per month, Congress should automatically index it to the Consumer Price Index (CPI) to prevent future erosion of the exclusion by inflation. Adjusting the GIE for inflation each year would make the treatment of the exclusion consistent with the treatment of the SSI maximum benefit.

The Social Security Administration report estimates that the cost of increasing the $20 GIE to $80 to compensate for erosion of the exclusion since 1972 would be $1.9 billion in 2001, and $20.7 billion over a 10-year period (see Table 1). The cost of both increasing the exclusion to $80 and indexing it for inflation would be $24 billion over the next 10 years.

Options |

2001 | 2001-2005 | 2001-2010 |

| Increase the GIE to $80 | $1.9 | $10.4 | $20.7 |

| Increase the GIE to $80 and Index to CPI | $1.9 | $11.2 | $24.0 |

| Source: Social Security Administration, Report on Supplemental Security Income: Income and Resource Exclusions and Disability Insurance Earnings-Related Provisions Washington, DC, March 2000, p. 60. | |||

In addition to this cost, Medicaid costs will rise as the number of newly eligible SSI participants rises, since SSI participants are categorically eligible for Medicaid in most states. No official cost estimates are currently available, but for the purpose of this analysis, estimates have been generated using Medicaid costs for aged, blind, and disabled enrollees.(23) The federal share of the Medicaid cost for acute care would be approximately $1.75 billion per year if the SSI improvement were made by itself without an accompanying improvement in Social Security benefits.(24) (The Medicaid cost estimate provided here is intended only to give a sense of the magnitude of the costs and should not be interpreted as an exact cost level.) The Medicaid cost would be lower if improvements in the Social Security survivors benefit also were made.

The enhanced GIE also would generate some additional income for Medicaid that would partially offset the costs to the program. Under current law, Medicaid enrollees in long-term care facilities receive $30 per month of their Medicaid benefit and any additional benefit is passed through to the institution in which they reside. If the GIE is raised to $80 per month and the amount paid to the enrollee remains at $30, the $60 increase in the GIE would be passed through to the institution. This pass-through would result in about $106 million in additional Medicaid income annually that would partially offset Medicaid cost increases.

Food stamp program costs also would be reduced as a result of the enhanced GIE. The increase in SSI income would make some individuals ineligible for food stamps or eligible for lower benefits. The savings would be at least $100 million per year.

The cost of raising the GIE would need to be weighed against other demands on the budget surplus. (As noted, the cost of improvements to the SSI program will not affect the solvency of Social Security. SSI is funded through general revenue.) If cost proves to be a barrier, the GIE could be raised from its current level of $20 to a level of less than $80.

Raise the Asset Limit for SSI

In general, eligibility for the SSI program is limited to individuals with no more than $2,000 in assets and couples with no more than $3,000. Some assets — such as the beneficiary's home, reasonably valued household goods and personal items, a car used for employment or to obtain medical care or transport a disabled individual, and life insurance with a face value of less than $1,500 — are not counted.

The limits for countable resources for SSI have eroded since the program's inception because they have not kept pace with inflation. The limits were set at $1,500 for individuals and $2,250 for couples in 1972, when legislation establishing the program was passed. These limits took effect in 1974 when the program was implemented. In 1984, Congress enacted legislation that raised the thresholds, based on the schedule in Table 2.

| Effective Date | Individual | Couple |

| January 1, 1987 | $1,800 | $2,700 |

| January 1, 1988 | $1,900 | $2,850 |

| January 1, 1989 & Thereafter | $2,000 | $3,000 |

Source: Social Security Administration, 1997 Social Security Handbook, Washington, DC: U. S. Government Printing Office, 1997, § 2167. |

||

There has not been an increase in the SSI resource limits in more than a decade, although the cost of living climbed approximately 38 percent between 1989 and 2000. An adjustment could be made in one of two ways. The resource limit could be increased by a flat amount, as was done in the past. Alternatively, the asset limit could be increased each year based on the change in the CPI. This would be consistent with the treatment of SSI benefits, which are updated using the CPI. If these thresholds were adjusted to reflect inflation since 1989, the resource limit for individuals would rise to $2,845 in 2001 and the limit for couples would be $4,268. Adjusting for inflation since 1989 would not entirely correct for inflation that occurred since 1972 when the asset limits were first established. If the thresholds were adjusted for inflation since 1972, the asset limit for individuals would be $5,959 in 2001 and the limit for couples would be $8,939.(25)

The Social Security Administration's report on income and resource exclusions shows that increasing the resource limits to $3,000 for individuals and $4,500 for couples would cost $65 million over the next five years and $152 million over the next ten years (see Table 3). Increasing the resource limit to $6,000 for individuals and $9,000 for couples would cost $89 million in 2001, $814 million over the next five years, and $1.8 billion over the next ten years. (This does not include increased costs in Medicaid.)

| Limit Options | 2001 | 2001-2005 | 2001-2010 |

| $3,000 / $4,500 | $7 | $65 | $152 |

| $6,000 / $9,000 | $89 | $814 | $1,800 |

| Source: Social Security Administration, Report on Supplemental Security Income: Income and Resource Exclusions and Disability Insurance Earnings-Related Provisions, Washington, DC, March 2000, p. 60. | |||

Exclude Defined-contribution Plan Balances from the SSI Asset Test

Defined-contribution plans, or retirement plans that are based on contributions of workers and employers to individual accounts, represent a rapidly growing share of employer-sponsored pension plans. These accounts also may be part of forthcoming Social Security and pension reform legislation. Such legislation could take the form of Retirement Savings Accounts (RSAs) outside the Social Security system, as proposed by the Clinton Administration, or individual accounts that replace a portion of Social Security, as proposed by several members of Congress and President Bush. If such accounts are created, Congress and the President should exempt balances in individual accounts from counting as assets in SSI and other means-tested programs.(26) Otherwise, such accounts can have the perverse effect of making low-income workers and retirees ineligible for SSI, Medicaid, and food stamps.

This is not simply a problem that would arise if the federal government established new forms of individual retirement accounts and failed to exempt them from asset tests. The problem already exists with regard to employer-provided defined-contribution pension plans such as 401(k) plans. Assets in these plans are counted as assets in SSI, food stamps, and, in most states, in Medicaid. Low-income individuals with such accounts generally are ineligible for means-tested benefits unless they deplete their accounts prematurely.

This problem has its origins in the 1970s, when the primary assets limits in the major means-tested benefit programs were developed. At that time, employer-sponsored defined-contribution plans were rare, especially for low-wage workers. (Most workers with pension coverage participated in defined-benefit plans.) The asset tests in most means-tested benefit programs were designed to exclude "inaccessible" resources and count "accessible" resources. Pension benefits that workers have accrued in defined-benefit plans are considered "inaccessible" but amounts in defined-contribution plans — which feature individual accounts — are generally considered accessible even if there is a penalty for early withdrawal.

In recent years, an increasing number of employers have either replaced defined-benefit plans with defined-contribution plans or established defined-contribution plans where they previously had no plan. Women have been expanding their participation in the labor market at the same time that employers have been instituting defined-contribution plans. As the number of low-income workers with defined-contribution plans grows, an increasing number of workers may lose eligibility for means-tested benefits if account balances are counted as assets.

Because defined-benefit pension funds are not accessible while withdrawals generally can be made from defined-benefit contribution plans, current law discriminates against low-income workers and retirees whose employers participated in a defined-contribution retirement plan as compared to workers whose employers provide a defined-benefit plan. Low-income workers with defined-contribution accounts generally must withdraw most or all of their accounts and spend those assets down, regardless of any early withdrawal penalty or tax consequences, before they can qualify for means-tested programs such as SSI, Medicaid, and food stamps.

Failure to exclude amounts in such accounts from asset tests in means-tested programs would create a perverse incentive for poor elderly individuals to withdraw funds from their retirement accounts prematurely and spend them; only then would they be eligible for SSI, Medicaid, and food stamps. Moreover, non-elderly workers who experienced temporary periods of need, such as during a recession, would be forced to liquidate and spend the retirement savings they had managed to accumulate — and often to pay substantial early withdrawal and often tax penalties — to be eligible for food stamps or Medicaid during the economic downturn. Some workers who were hard-pressed during a downturn — and withdrew most of the funds in their retirement accounts because they could not receive means-tested assistance until the accounts were spent down and consequently could not meet current needs without drawing on their retirement funds — could reach retirement with little left in their accounts.

Forcing low-income workers and retirees to deplete their savings before they can access means-tested benefits runs counter to efforts to encourage low-income workers to save for retirement and does not represent sound policy. Federal policy ought to encourage low-income workers to build retirement savings. It should encourage low-income retirees to withdraw funds from their retirement accounts gradually over their remaining years (rather than in a lump sum) so that sufficient funds remain to avert severe poverty when they become very old. This is particularly important for reducing high rates of poverty among elderly women, since women have longer life expectancies than men.

There still is a small enough number of low-wage workers with defined-contribution plans that these aspects of the asset rules of means-tested programs are not invoked much. Not many people lose means-tested benefits for this reason. As a result, making this change should have little cost in the next five or 10 years.

Congress and the Administration could address these problems through changes in asset rules in means-tested programs to treat defined-contribution accounts in the same manner as defined-benefit plans. If an individual (whether a retiree or a younger household) withdraws funds from a tax-deferred retirement account, the amounts withdrawn should be counted as income. But amounts not withdrawn should not be considered an asset for means-tested program eligibility purposes. Such an approach is important if new forms of individual accounts (whether in the form of Retirement Savings Accounts outside the Social Security system as proposed by President Clinton or individual accounts within Social Security as favored by President Bush) and employer-sponsored defined-contribution plans are to help low-income workers save for retirement and to enable low-income retirees to have adequate income that lasts into very old age.

Conclusion

The Social Security program has been a constant upon which women have been able to depend for income when they become elderly. The program has been one of the nation's most effective defenses against poverty. There are, however, limits to what Social Security can and should be expected to do to reduce poverty. There is a role for programs such as SSI.

Improvements in the SSI program would target elderly individuals and couples with the lowest incomes. Adjusting the GIE and asset limits for inflation and excluding defined-contribution plan balances from the asset test would modernize the SSI program and increase the number of poor elderly who benefit from the program.

To prevent unintended consequences as a result of raising Social Security benefits for elderly individuals at risk of poverty, improvements in SSI should be coupled with improvements in Social Security benefits. It is unlikely that SSI improvements will be enacted if they are not combined with a Social Security reform plan.

End notes

1. It is important to note that the measure of poverty used throughout this report, unless otherwise specified, differs from the official poverty measure. In this report, the phrase "before (or without) Social Security" means the poverty rate was determined by counting only income from social insurance such as federal pensions and unemployment insurance benefits, not Social Security or any means-tested benefits. The phrase "after Social Security" means income from social insurance and Social Security was counted; benefits from means-tested programs were not. By contrast, the official poverty measure counts all cash income, including all government cash benefits. Benefits not in the form of cash (e.g., food stamps) are not counted.

2. Using the official poverty measure, about 3.4 million elderly individuals were poor in 1998. Eighteen percent of elderly, unmarried women, 26 percent of elderly African Americans, and 21 percent of elderly Latinos were poor compared to eight percent of white elderly.

3. These data are the result of analyses by the Center on Budget and Policy Priorities using 1999 Current Population Survey data collected by the Bureau of the Census.

4. For the purposes of this paper, the income of individuals age 65 and older and the income of their spouses (where relevant) are included, whether or not the spouse also is 65 or older. Counting the income of non-elderly spouses better captures the total cash income available to the elderly. See also, Barbara A. Butrica, Howard Iams, and Steven H. Sandell, "Using Data for Couples to Project the Distributional Effects of Changes in Social Security Policy," Social Security Bulletin, Vol. 62, No. 3, p. 21.

5. Lawrence Mishell, Jared Bernstein, and John Schmitt, The State of Working America 2000-01, Washington, DC: Economic Policy Institute, 2000, Table 2.41, p. 189.

6. U.S. Department of Labor, Employment and Earnings, Washington, DC: U.S. Government Printing Office, January 2000, Table 22, p. 198.

7. National Economic Council Interagency Working Group on Social Security, Women and Retirement Income, October 1998.

8. Kathryn H. Porter, Kathy Larin, Wendell Primus, Social Security and Poverty Among the Elderly: A National and State Perspective, Washington, DC: Center on Budget and Policy Priorities, April 1999, p. 25.

9. Centers for Disease Control, Vital Statistics of the United States, 1993: Life Tables, Washington, DC: U.S. Government Printing Office, 1997, Table 6-1, p. 7.

10. These data are the result of analyses by the Center on Budget and Policy Priorities using 1994-1998 CPS data collected by the Bureau of the Census.

11. Social Security Administration, Report on Supplemental Security Income: Income and Resource Exclusions and Disability Insurance Earnings-Related Provisions, Washington, DC: Social Security Administration, March 2000, p. 9.

12. Sharmila Choudhury and Michael V. Leonesio. "Life-Cycle Aspects of Poverty Among Older Women," Social Security Bulletin, Vol. 60, No. 2, 1997.

13. Social Security Administration, Annual Statistical Supplement, 1999, op. cit., Table 7.E4, p. 303.

14. Committee on Ways and Means, U.S. House of Representatives, The Green Book. Washington, DC: U.S. Government Printing Office, May 1998.

15. Income from other federally funded means-tested programs is not excluded. See Social Security Administration, Income and Resource Exclusions, op. cit., p. 8.

16. Social Security Administration, Income and Resource Exclusions, op. cit., p. 9.

17. Ibid., p. 8.

18. Ibid., p. 8.

19. In 1998 Ms. Harris would have received a Social Security benefit of $498. Her benefit would increase annually as a result of the cost of living adjustment and would be approximately $539 in 2001. See Social Security Administration, Statistical Supplement, 1999, op. cit., Washington, DC: U.S. Government Printing Office, 2000, Table 2.A.26, p. 71.

20. Social Security benefits make up 91 percent of the unearned income received by SSI participants to which the general income exclusion is applied. Other sources of unearned income include veterans benefits, railroad retirement, black lung benefits, employment pensions, worker's compensation, and support from absent parents. See Committee on Ways and Means, U. S. House of Representatives, 1998 Green Book, Washington, DC: U.S. Government Printing Office, 1998, p. 300.

21. Congress passed legislation in 1972 that established the SSI program and designated 1974 as the initial year of benefit payments. Congress also established a cost-of-living adjustment for SSI benefits, so that maximum benefit levels rise each year in tandem with the Consumer Price Index. No similar adjustments were made for the general income exclusion. Comparable treatment of benefit levels and the general income exclusion would require an adjustment in the GIE to reflect inflation since 1972. See Social Security Administration, Annual Statistical Supplement, op. cit., Table 2. B1, p. 90. See also Social Security Administration, Income and Resource Exclusions, op. cit., pp. 4 and 8-9.

22. Social Security Administration, Income and Resource Exclusions, op. cit., p. 9.

23. Analyses by the Center on Budget and Policy Priorities using 1998 Current Population Survey data collected by the Bureau of the Census were used to determine the number of new aged enrollees, and SSA data were used to determine the number of new disabled enrollees. Medicaid costs are based on data from the Urban Institute on the cost for aged, blind, and disabled enrollees who were receiving cash assistance.

24. Acute care includes costs for inpatient and outpatient care, physicians, lab work, x-rays, prescriptions, and payments to managed care providers. Medicaid also covers long-term care, but these costs are not included in this estimate.

25. These estimates are based on the CPI-U-X1 (Consumer Price Index experimental series created by the Bureau of Labor Statistics, U. S. Department of Labor) rather than the CPI. The CPI-U-X1 more accurately captures changes in living costs and mortgage rates prior to 1983. See U.S. Census Bureau, Money and Income in the United States: Current Population Reports, Consumer Income, 1998, Washington, DC: U. S. Government Printing Office, September 1999, Appendix D.

26. Robert Greenstein, Building Retirement Savings Can Cause Low- and Moderate-income Working Families to Lose Means-Tested Assistane in Times of Need," Washington, DC: Center on Budget and Policy Priorities, September 20, 2000. See also, Kathy Larin and Wendell Primus, Individual Accounts, Defined-contribution Plans, and Assets Tests in Means-Tested Programs, Washington, DC: Center on Budget and Policy Priorities, March 29, 1999.