HISPANICS AND SOCIAL SECURITY:

THE IMPLICATIONS OF REFORM PROPOSALS

By Fernando Torres-Gil, Robert Greenstein, and David Kamin[1]

Executive Summary

|

PDF of

this report

Related Reports: The Importance Of Social Security To The

Hispanic Community |

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. | |

|

KEY FINDINGS |

|

|

|

Plans that rely largely on benefit cuts to restore solvency to Social Security are adverse for Hispanics, compared to plans that employ a balanced mix of benefit reductions and progressive revenue changes. |

|

|

Hispanics are likely to do worse under reform plans that make young workers and future generations bear the brunt of the sacrifices needed to preserve Social Security. |

|

|

The President’s Social Security plan fails on both of these counts. It relies entirely on backloaded benefit cuts that would hit young workers and future generations hard. |

|

|

Replacing Social Security with private accounts would be especially harmful to Hispanics. Hispanics benefit disproportionately from Social Security’s social insurance aspects and redistributive nature, which would be eliminated in a pure private account system. |

|

|

Hispanics should be encouraged to save more for retirement by revamping and improving the current system of tax preferred saving accounts. |

The Hispanic community has a great deal at stake in the debate over Social Security. In a separate report, we have analyzed the particular importance of the Social Security system to the Hispanic community.[2] Hispanics receive a higher rate of return on the taxes they pay into the system than the rest of the population, and elderly Hispanics rely on Social Security for a larger share of their income than other elderly Americans do. For Hispanics, Social Security reform plans must be evaluated in light of the significant benefits they receive from the current system.

In this analysis, we outline the potential effects of Social Security reform on Hispanic Americans. We consider how the Administration’s proposals to change Social Security benefits would affect the Hispanic community. We also discuss alternative types of reforms.

In summary:

- Plans to restore Social Security solvency that rely largely on reductions in Social Security benefits would tend to be more harmful to Hispanics than plans that employ a balanced mix of benefit reductions and progressive revenue changes, since Hispanics disproportionately gain from Social Security benefits. Simply stated, Hispanics would tend to be harmed disproportionately if large cuts are made in a system from which they disproportionately benefit.

- The Hispanic population today is overwhelmingly young, but it is

expected to age rapidly over the coming decades. Reforms that

shield current retirees and spare baby boomers much pain, while making later generations of retirees bear the heaviest load, would be especially detrimental to Hispanics.

To be sure, all generations — both old and young — benefit from Social Security, as it serves and is expected to continuing serving as a basic form of income security for the survivors of deceased workers, people with disabilities, and retirees. But, the system faces a fiscal shortfall that needs to be addressed. For Hispanics, it is particularly important that this shortfall not be closed by measures that largely spare the baby boomers and place the burden of reform almost entirely on younger generations.

- The President’s Social Security proposals fare poorly on both

of these counts. The plan that the President has proposed relies entirely

on benefit cuts to reduce the Social Security shortfall. Furthermore, the

President’s plan largely exempts the baby-boom generation from significant

benefit reductions and makes later generations bear much steeper cuts as a

result. Such backloaded cuts would fall especially heavily on Hispanics.

Closing the Social Security shortfall is particularly important to the Hispanic community. As a young population that is rapidly aging and receives more in return for its contributions to Social Security than others, Hispanics have much invested in the future solvency of the system. The President’s plan, however, would restore solvency in a way that is more detrimental to Hispanics than various other reforms would be.

- There has been a campaign to sell the Hispanic community on the notion that Hispanics would fare better if Social Security were replaced by private accounts. Careful analysis shows that the opposite is true. Hispanics benefit disproportionately from the various types of insurance that Social Security provides and from Social Security’s redistributive nature. Pure private account plans would eliminate this redistribution, as they would tie each worker’s benefits directly to that worker’s contributions to his or her private account. This would be harmful to the Hispanic community.

- Hispanics, in general, tend to be ill-prepared for retirement in terms how much they have accumulated in pensions and other retirement savings. The solution is not to begin to dismantle the Social Security system, which is the one form of retirement security that works particularly well for Hispanics. Instead, the current system of tax-preferred saving accounts, such as 401(k)s and IRAs, should be revamped and improved. In their current form, these accounts and the tax breaks that support them provide their greatest benefits to people with the highest incomes. To better secure Hispanics’ retirement, the current system of tax incentives for saving should be reformed to provide greater incentives and opportunities for saving by middle- and low-income American workers and their families. The National Council of La Raza has also recently suggested a number of relatively modest adjustments to the Social Security system that would benefit the Hispanic community and should be considered as part of reform.[3]

The Threat of Large Benefit Cuts and Imbalanced Reform

A number of plans under discussion would restore Social Security solvency primarily or exclusively through benefit reductions. Over time, some of these plans would sharply reduce the portion of a worker’s pre-retirement income that Social Security replaces and would reduce Social Security survivor benefits and possibly disability benefits, as well. This would have adverse effects on Hispanics.

|

||||||||||||||||||||||||||||||||||||||||||

As noted, Hispanics receive a higher rate of return on the taxes they pay into the system than the rest of the population, and elderly Hispanics rely on Social Security for a larger share of their income than do other elderly Americans. Thus, to the extent that a plan substantially reduces Social Security’s role in providing retirement security and redistributing resources, the Hispanic community would tend to be harmed. Hispanics would be harmed disproportionately if large cuts are made in a system from which they disproportionately benefit.

The President’s Social Security proposals, as they have been outlined so far, rely solely on benefit cuts to restore solvency to the Social Security system. The President has proposed “sliding scale benefit reductions” (also known as “progressive price indexing”) that would result in growing and, eventually, sharp benefit cuts for many Social Security beneficiaries.

-

All workers who earn more than about $20,000 today would be subject to benefit reductions. About seven of every ten workers would be affected.

-

The benefit reductions for middle-class workers would be large. The benefit cuts would escalate sharply in size as income rose above $20,000, until income reached $90,000. (The benefit reductions would be the same for people making $90,000 as for people making larger amounts.) A worker who earns about $37,000 today (the current average wage) would be subject to benefit reductions more than half as large, as a percentage of the worker’s scheduled Social Security benefits, as the benefit cuts imposed on people at very high income levels. And a worker who makes about $59,000 today would be subject to benefit reductions nearly as large, as a percentage of scheduled benefits, as the reductions imposed on someone making millions of dollars a year. The Social Security benefits of a $59,000-a-year worker who retires in 2045 would be reduced by 25 percent, or about $6,400 a year.

-

Since middle-income Americans rely on Social Security to replace a much larger share of their pre-retirement income than wealthy individuals do, the pain of these benefit cuts would be much sharper for the middle class than for high-income individuals. As Table 2 shows, the proposed benefit cuts would be much larger, as a share of average pre-retirement income, for middle-income Americans than for those at high income levels. For example, in 2045, someone making $1 million a year in today’s terms would face an annual Social Security benefit cut equal to 0.6 percent of his or her pre-retirement income. In contrast, a worker making about $59,000 in today’s terms would face a benefit cut equal to 7.4 percent of his or her pre-retirement income. The Administration’s proposed cuts would thus impose a greater burden on middle-income workers than on very high-income workers, relative to their incomes.

-

Table 2

Who Feels the Burden of Sliding Scale Benefit Cuts?

(Cuts in 2045)Earnings of:

Cut as a Percent of Pre-Retirement Income

$36,600*

-6.0%

$58,560*

-7.4%

$90,000*

-7.0%

$1,000,000*

-0.6%

* Note: The earnings levels in the table are given in today’s terms. Over time, workers’ earnings are assumed to grow at the same rate as average wages.

Source: Authors’ calculations.

To its credit, the President’s proposal would exempt many of the poorest workers from these benefit cuts, although contrary to White House claims, some poor beneficiaries would indeed be subject to cuts (see footnote).[4] The President’s proposal also includes an enhancement for low-income workers, which represents a positive step. Nonetheless, middle-income Hispanic workers would face sharp benefit reductions in retirement, and Hispanics as a whole would fare worse under the President’s proposal than under plans that combine much more modest benefit cuts with progressive revenue enhancements.

Moreover, the Administration may eventually endorse deeper benefit cuts. The benefit cuts that the Administration has proposed to date would close only about 59 percent of the 75-year Social Security shortfall, as measured by the Social Security Trustees. [5] Further adjustments on top of the President’s proposed benefit reductions would be needed to close the shortfall.

When asking his Social Security Commission to outline options for reform in 2001, the President directed the Commission to avoid any measures that would raise additional revenues. Since then, the President has softened his stance somewhat and has not ruled out legislation that would raise the maximum level of income that is subject to the Social Security payroll tax (currently set at $90,000). But so far, the Administration has proposed only benefit cuts, and it seems clear that the Administration will support only measures to restore Social Security solvency that rely largely or entirely on benefit reductions.

Hispanics generally would fare better under plans that impose smaller benefit cuts on middle-income workers than the President has proposed, by making those with very high incomes shoulder a larger share of the load. This could be done through progressive revenue changes, such as the following:

- Instead of repealing the estate tax (as Congress is currently

considering doing, and as the President has proposed), the estate tax could

be scaled back and reformed, with the revenues it continues to collect

dedicated to the Social Security Trust Fund. According to the Social

Security Administration’s Chief Actuary, a reformed estate tax that exempts

from that tax any estate that is worth less than $7 million per couple and

$3.5 million per individual would close about 30 percent of the 75-year

Social Security shortfall.[6]

The Brookings Institution-Urban Institute Tax Policy Center estimates that,

as of 2011, such an estate tax would apply to only the three wealthiest of every 1,000 people who die;

the other 997 of every 1,000 people who die would be exempt entirely from

the tax. The fraction of Hispanics who would be subject by the tax would be

even more miniscule, given Hispanics’ relatively lower-wealth levels.

-

In addition, many have suggested raising the maximum level of wages and salaries that is subject to the Social Security payroll tax, which, as noted, is now set at $90,000. Still another option, proposed by economists Peter Diamond and Peter Orszag, would be to impose a modest surcharge on earnings above the taxable maximum, with the resulting revenues devoted to the Social Security Trust Fund. Diamond and Orszag propose a three to four percent levy on earnings above the maximum amount that is subject to the full payroll tax.

Taxing income above the current $90,000 maximum would raise substantial revenues but affect only a small slice of workers and an even smaller fraction of Hispanics. Only a tiny share of the Hispanic population has earnings above the current $90,000 Social Security taxable maximum. About six percent of all workers with wage and salary income have earnings above the current $90,000 maximum. But only about two percent of Hispanic workers with wage and salary income have earnings above this level.[7]

The President’s proposals do not include any progressive revenue adjustments that would enable the Social Security benefit reductions imposed on middle-income workers to be more modest. The Administration’s proposals instead rely entirely on benefit cuts and place much of the burden of restoring Social Security solvency on middle-income people. Hispanics would not be well served by such an approach.

Future Generations Could Bear the Heaviest Load

The Hispanic population today is overwhelmingly young, but it is expected to age rapidly over the coming decades.

- Only five percent of the 42 million U.S. residents of Hispanic origin are aged 65 or older today. (This compares to 12 percent of the total U.S. population that is 65 or older.)

- The Census Bureau projects this proportion will triple by 2050, with the share of the Hispanic population that is aged 65 or older rising to 15 percent by that year.

- Similarly, Hispanics are expected to compose a far larger share of the elderly population in future years than they do today. Currently, six percent of the population aged 65 or older is Hispanic. The Census Bureau projects that by 2050, however, Hispanics will make up 18 percent of the elderly population.[8]

Due to these demographics, Social Security changes that shield current retirees and spare baby-boomers much pain while making later retirees bear the heaviest loads would be especially detrimental to Hispanics. To be sure, all generations — both old and young — benefit from Social Security, as it serves and is expected to continuing serving as a basic form of income security for the survivors of deceased workers, people with disabilities, and retirees. But, the system faces a fiscal shortfall that needs to be closed. For Hispanics, it is particularly important that the shortfall not be closed by measures that largely spare baby boomers and place the burden almost entirely on younger workers. Hispanics would fare better under approaches that more equitably spread the burden of reform across generations. The Administration’s Social Security plan fails to do this.

Under the Administration’s proposals, Social Security benefit reductions would be modest for those retiring in the next couple of decades, but would grow steadily deeper over time, with each new group of retirees facing sharper benefit cuts. As a result, today’s younger workers, including many Hispanics, would face dramatically larger benefit reductions than earlier retirees.

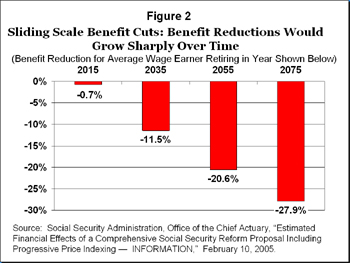

Specifically, the President’s plan exempts those aged 55 or older from any cuts in Social Security benefits. For those retiring in or after 2012, the first year in which new retirees would begin to be subject to benefit reductions, the proposed cuts would start small but mount over time. As Figure 2 illustrates, an average wage-earner would face a benefit cut each year of:

- Less than one percent if the worker retired in 2015;

- 11.5 percent if he or she retired in 2035;

- 21 percent if the worker retired in 2055; and

- 28 percent if the worker retired in 2075.

|

|

The generational imbalance in the President’s plan is further exacerbated by the financing of the private accounts that the President has proposed. To finance the “transition” to these accounts, the federal government would borrow trillions of dollars. That would greatly magnify the debt burden on younger generations.

Because of the borrowing undertaken to finance the private accounts, the President’s Social Security proposals would add $4.9 trillion (in current dollars) to the national debt over the plan’s first 20 years, with several trillion dollars in additional debt added in the decades after that. Under the President’s plan, this debt would eventually be paid off through additional reductions in the Social Security benefits of young workers. In the words of economist Lawrence Kotlikoff, who himself favors private accounts, “the dirty little secret underlying most Social Security privatization schemes is that they head precisely down this road” of “dumping the entire…bill in our kids’ laps.”[9] Doing that would not be in the interests of the Hispanic community.

The Danger of Private Accounts

As we have detailed in a separate analysis, the Social Security system disproportionately benefits people with:

-

lower-than-average lifetime earnings;

-

a higher-than-average incidence of disability;

-

more children per family;

-

and longer-than-average life expectancies.[10]

Hispanics have all of these characteristics.[11]

Hispanics thus would be harmed by plans, such as many private account plans, that would shrink the social insurance aspects of Social Security by linking each person’s benefits to a much greater degree to that individual’s payroll tax payments, without regard to whether the person was paid low wages throughout his or her career, how long the person remains alive (and thus for how many years he or she needs income in retirement), or the misfortunes that may befall a person, such as disability or premature death. In their most extreme form, private account plans would eliminate these redistributive aspects of Social Security, since the level of income that people could draw from the accounts would be determined solely by the size of a person’s contributions to his or her account and the rate of return on the account’s investments (rather than also being determined in part by circumstances such as whether the person had low earnings or whether his or her spouse or parent had died). Scaling back Social Security benefits to pay for private accounts consequently could affect Hispanics adversely, since they benefit disproportionately from the social insurance and redistributive features of the current Social Security system and receive a higher rate of return than the rest of the population on the contributions they make to the system.

Despite this, some reports have claimed that Hispanics would be better off if Social Security were entirely replaced by private accounts. For instance, a widely publicized 1998 Heritage Foundation report asserted that the “Social Security system’s rate of return for most Hispanic Americans will be vastly inferior to what they could expect from placing their payroll taxes in even the most conservative private investments.”[12] In a separate analysis, we have explained the severe shortcomings with the Heritage report (which has been sharply criticized by the Social Security actuaries and widely discredited) and other reports making such claims.

In summary, reports that claim the rate of return on private accounts would be significantly higher than the rate of return under Social Security suffer from two critical flaws.[13]

- They generally fail to account for the substantial “transition costs” of switching to a private account system. This stacks the deck in favor of private accounts by comparing rates of return under a Social Security system with one level of financing to rates of return under a private-account system with substantial additional financing, without taking the cost of the additional financing into account.

- They ignore the cost of the added risk associated with shifting funds from the traditional Social Security system — which invests solely in U.S. Treasury bonds, generally regarded as the world’s most secure investment — to the stock market, which is riskier and more volatile. The nonpartisan Congressional Budget Office and a wide range of economists agree that the cost of the added risk involved in investing in stocks (after all, some people lose money in the stock market) should be incorporated into any analysis that compares returns under Social Security to returns under private accounts.

The “bottom line” is that once transition costs and stock-market risk are taken into account, a system with private accounts would not produce a better rate of return for the population as a whole than the Social Security system. And for Hispanics, the Social Security system is distinctly preferable to private accounts since Hispanics benefit disproportionately from Social Security’s social insurance aspects and redistributive nature.

Strengthening Retirement Security for Hispanics

Hispanics in general tend to be ill-prepared for retirement in terms how much they have accumulated in pensions and other retirement savings. The solution to this problem is not to contract or dismantle the Social Security system, the one form of retirement security that works especially well for Hispanics. Rather, the solution is to revamp and improve the system of tax-preferred saving accounts, such as IRAs and 401(k)s. In their current form, those accounts provide the most powerful incentives and most generous tax benefits to people who have the highest incomes (and the least need for incentives and subsidies to help them save adequately for retirement). To better secure Hispanics’ retirement, the current system of tax incentives for retirement saving should be reformed to provide greater incentives and opportunities for middle- and low-income Americans to save.

- Hispanic workers have far lower participation rates in employer-sponsored retirement plans than either whites or blacks. A recent study by the Employee Benefits Research Institute found that of the 16.3 million Hispanic wage and salary workers aged 21-64 in 2003, only 29 percent participated in an employer-sponsored retirement plan. This compares to a participation rate of 53 percent among white wage and salary workers in the same age range and 45 percent among black wage and salary workers.[14]

- The Social Security Administration reports that, as of 2002, only 26 percent of elderly Hispanics aged 65 and over had income from assets. By contrast, 55 percent of the elderly population as a whole received income from assets. Similarly, only 13 percent of the Hispanic elderly population received income from private pensions or annuities while 29 percent of the elderly population as a whole did.[15]

-

Hispanics consequently tend to rely on Social Security for a larger share of their retirement income. In 2002, some 41 percent of elderly Hispanic Social Security beneficiaries relied on Social Security for all of their income, compared to 22 percent for Social Security beneficiaries as a whole. [16]

The current system of tax-preferred saving accounts is particularly ill-suited to helping Hispanic workers provide for their retirement. To encourage participation in retirement saving plans, the current system relies principally on tax deductions and exclusions which shield from taxation the money that people save in various types of retirement saving vehicles. The value of such deductions and exclusions depends on an individual’s tax bracket. The higher the tax bracket, the greater the value of the deduction or exclusion; the lower the tax bracket, the smaller the value of the deduction or exclusion and thus the smaller the size of the tax subsidy. In addition, the current system of saving incentives can be quite complicated. For a population like Hispanics with lower-than-average income and education levels, this incentive system tends to be rather ineffective.

Brookings Institution economist Peter Orszag has proposed a number of policy changes that would improve retirement security for low- and middle-income families by simplifying the current system and strengthening the incentives. Such reforms would be especially beneficial for Hispanics. These reforms include:[17]

-

Automating 401(k)-type retirement plan so employees are automatically enrolled in these plans. (To refrain from participating, employees would have to opt out, as opposed to the current system in which employees must specifically opt in.) When one large U.S. corporation instituted automatic enrollment in its retirement plan, participation rates increased dramatically among its new employees, especially Hispanic employees. The participation rate for new Hispanic employees quadrupled, jumping from 19 percent to 75 percent.[18] This follows the trend seen among the employees of other corporations that have instituted automatic enrollment, where participation rates have also risen dramatically.[19]

-

Revamping and expanding the current saver’s credit. This credit, enacted in 2001, provides a tax subsidy to encourage moderate-income families to make contributions to retirement accounts. The tax credit essentially provides a government matching contribution for the contributions that moderate-income workers make to IRAs, 401(k)s or similar accounts. To be more effective, this tax credit should be made refundable (as the Earned Income Tax Credit is) so that the credit also can benefit low-income workers who do not earn enough to owe federal income tax. In addition, the saver’s credit could be made more transparent so people can more readily see that the government will match the contributions they make.

-

Reducing the disincentives to save for retirement produced by the asset tests applied in means-tested programs such as Food Stamps, Medicaid, and the Supplemental Security Income program. Although the rules vary from program to program and from state to state, the rules often require that retirement accounts such as 401(k)s and IRAs be counted toward the asset limits in these programs. This means low-income families can lose eligibility for the programs if they began to build even modest retirement savings. Exempting retirement accounts from the asset tests used in these programs would remove a significant barrier to saving among low-income working families.

-

Allowing workers to deposit part of their tax refund directly into a retirement account while preserving the rest of the tax refund for other purposes. Currently, taxpayers may direct the IRS to deposit their entire refund amount into only one account. Taxpayers may not ask the IRS to split their tax refund, with part (but not all) of it going to a retirement account. Peter Orszag has noted that, “This all-or-nothing approach discourages many households from saving any of their refund. Some of the refund is often needed for immediate expenses....”[20] Allowing taxpayers to split their refunds would give them greater flexibility to direct a portion of the refunds into retirement accounts.

National Council of La Raza’s Proposals to Expand Coverage and Enhance Benefits for Hispanics

As this analysis explains, the Social Security system provides better returns to the Hispanic community than to the population as a whole and to non-Hispanic whites or blacks. Nonetheless, the system could be improved and strengthened.

In a new report, the National Council of La Raza suggests ways in which the Social Security system could be adjusted to widen its coverage and strengthen its support for elderly Hispanics.[21] NLCR notes that “most Latinos who are eligible for Social Security benefits receive an ample amount of income support over their retirement and benefit greatly from the system’s progressivity and indexed benefits.” But NCLR also finds that while those Hispanics who are eligible for Social Security benefits are helped more than other beneficiaries, on average, a smaller share of elderly Hispanics receive Social Security checks than of other retirees.

According to the Social Security Administration:

- 77 percent of Hispanics aged 65 or older were paid Social Security benefits in 2002.

- By contrast, 83 percent of blacks and 91 percent of whites received Social Security checks.

Social Security coverage is lower among elderly Hispanics for several reasons. Although undocumented workers frequently pay taxes into the Social Security system (under false or non-work status Social Security numbers), many of these workers, who are disproportionately Hispanic, will never collect Social Security benefits based on these contributions. The presence of undocumented workers lowers Hispanic participation rates.

The Social Security system, through its ten-year work requirement, also lowers coverage rates for Hispanic workers who are here legally. To qualify for Social Security retirement benefits, a worker must contribute to the Social Security system for at least ten years (40 quarters). This creates a cliff in the system that can adversely affect workers with short work histories. Despite the fact that they have contributed payroll taxes, those who work for less than ten years in covered employment receive no retirement benefits (unless there is a “totalization” agreement in effect with an immigrant’s native country; see footnote 22), while someone who works exactly ten years can receive substantial benefits.

New immigrants, of which there are many in the Hispanic community, tend to have relatively short work histories in the United States and thus would tend to be disproportionately harmed by the way the threshold is structured. [22] The Social Security earnings requirements also make it more difficult for domestic workers (many of whom are Hispanic) than for others to get work counted toward the ten-year threshold. Finally, a number of Hispanics work in sectors, such as agricultural labor, where some employers underreport earnings to the Social Security. This makes it more difficult for some Hispanics, such as itinerant farm workers, to accrue the ten years necessary to qualify for benefits.

To raise coverage rates among Hispanic workers, NCLR suggests a number of adjustments to the current system. The proposed changes include:

- Reducing the amount of earnings necessary in a year for domestic workers to get work counted toward the ten-year eligibility threshold.

- Increasing the reporting of earnings to Social Security by applying stronger enforcement measures to those industries (such as farm and construction work) in which underreporting is widespread.

- Approving a “totalization” agreement with Mexico. Last year, the United States signed a “totalization” agreement with Mexico that would allow workers to apply work in both countries toward the ten-year eligibility requirement for Social Security. (See footnote 22.) The agreement has yet to go into effect. For this to happen, the Social Security Administration has to complete implementation procedures for the agreement. With this done, the President must submit the agreement to Congress for a 60-day review, during which neither house of congress passes a resolution of disapproval.

NCLR also has added its voice to that of many independent groups and policymakers, including the President and a number of members of Congress, in expressing support for strengthening Social Security’s minimum benefit. The current system includes a minimum benefit, but the benefit is small and rapidly phasing out. A meaningful minimum benefit in Social Security would help lift low-income workers out of poverty in retirement.

|

Strengthening the

Social Security Administration’s Other Program: The Social Security Administration also administers the Supplemental Security Income program, which provides a basic safety net for poor seniors and people with disabilities who either receive small Social Security benefits or do not receive Social Security at all. The SSI program lifts poor individuals who are elderly or disabled to about 75 percent of the poverty line and poor couples to about 90 percent of the poverty line. In most states, receipt of SSI also qualifies an individual or couple for health insurance coverage through Medicaid. As the recent report from the National Council of La Raza notes, SSI is of particular importance to Hispanics. Some 13 percent of Hispanics aged 65 and over receive SSI. This percentage is much higher than those for elderly whites, three percent of whom receive SSI benefits, and also exceeds the percentage for elderly blacks, 10 percent of whom receive SSI.* The NCLR report explains that “SSI is particularly important as a safety net for Latinos who work intermittently for very low wages, who didn’t always work in Social Security-covered jobs, or who immigrated to the U.S. late in life.”** Such people tend to qualify for small Social Security benefits that leave them well below the poverty line or not to qualify for Social Security at all.

SSI Improvements Needed to Prevent

Well-intended There appears to be broad consensus across the political spectrum in support of reforms that would assist poor Social Security beneficiaries by strengthening Social Security’s “minimum benefit” (discussed elsewhere in this report) and improving what is sometimes referred to as Social Security’s “widow’s benefit” — i.e., the benefit for surviving spouses who are age 50 or older if disabled and age 60 or older otherwise. (Under the consensus proposal to strengthen the widow’s benefit, the Social Security benefits of a low- or moderate-income widow or widower would not fall below 75 percent of the combined Social Security benefit that the couple received when both spouses were alive.) Both of these reforms would be desirable. Yet they would have a severe side-effect on some poor elderly and disabled people who receive both Social Security and SSI — and would make these people significantly worse off — unless the reforms are accompanied by a key reform in SSI. For people who receive both Social Security and SSI, an increase in Social Security benefits triggers a dollar-for-dollar reduction in SSI benefits. If an increase in Social Security benefits lifts such people modestly above the SSI income limit, they lose eligibility for SSI — and consequently could lose Medicaid coverage in a majority of states. The resulting loss of health care coverage and the increase in out-of-pocket health care costs these people would have to bear would far outweigh the small increase they would get in their monthly checks from the Social Security Administration. With a larger share of elderly Hispanics receiving income from a combination of Social Security and SSI than of the rest of the elderly population, this is a matter of particular significance for the Hispanic community. This matter could be addressed by including in Social Security legislation a provision requiring that people who would be eligible for SSI in the absence of improvements in Social Security’s minimum benefit and widow’s benefit be “deemed” to be receiving SSI for purposes of determining their eligibility for Medicaid. This would enable the affected people still to qualify for Medicaid. On several occasions in the past when Congress made changes in Social Security that would cause some people to become ineligible for SSI, Congress has included such a provision to prevent the loss of Medicaid coverage. Other SSI Improvements The SSI asset limits, set at $2,000 for individuals and $3,000 for couples, have not been adjusted since 1989. They have been heavily eroded by inflation. These limits have effectively been reduced by 36 percent since 1989, because of the lack of any inflation adjustment. These limits are eroding further and becoming more restrictive with each passing year. An upward correction in them, and a provision to adjust these limits for inflation in the future, would be of significant help to Hispanics. In a similar vein, when the SSI program was created in 1972, Congress directed that the first $20 in Social Security benefits, veterans’ benefits, or other unearned income be disregarded in determining SSI eligibility and benefit levels. This level has not been adjusted for inflation in the 33 years since. Consideration should be given to increasing it, as well, and adjusting it for inflation in the future. Finally, the harsh limitations enacted in the mid-1990s that severely restrict SSI eligibility for legal immigrants should be eased. Legal immigrants who lawfully entered the United States on or after August 22, 1996 are categorically ineligible for SSI, unless they (or a spouse or parent) have amassed 40 quarters of work in this country. Even a legal immigrant who has been unable to amass 40 quarters of work because he or she has become severely disabled after entering the United States, as a result of a workplace or other accident or the onset of a serious disease, is barred from SSI despite his or her obvious need. The SSI rules regarding the eligibility of legal immigrants are more restrictive than the rules in food stamps, Medicaid, or the Temporary Assistance for Needy Families program and should be made less harsh. * Social Security Administration, Income of the Population 55 or Older, 2002, March 2005, Table 1.3. ** National Council of La Raza, “The Social Security Program and Reform: A Latino Perspective,” 2005, p. 12. |

It should be kept in mind, however, that not all minimum benefit proposals are alike. Some proposed minimum benefits, including the minimum benefit endorsed by the President’s commission on Social Security, would phase out over time. Such proposals would establish a minimum benefit floor, but the floor would rise more slowly than the Social Security benefits it is meant to augment. Over time, the minimum benefit would become largely meaningless. Other proposals would allow the minimum benefit to grow along with Social Security benefits as traditionally calculated. This would produce a minimum benefit that would not phase out over time and be of far greater value in retirement to low-wage workers who are young today.

These NCLR proposals deserve consideration as part of Social Security reform. It should be noted that resolving these issues does not require making fundamental changes to Social Security. They can be addressed through relatively modest adjustments within the current system. Private accounts would do little to solve these problems and would end up harming Hispanics by undermining the features of Social Security that benefit the Hispanic population substantially.

Conclusion

The current Social Security system provides the Hispanic community with valuable benefits. Hispanics receive better returns on the taxes they contribute to the Social Security system than other workers, and elderly Hispanics rely on Social Security benefits for a greater share of their income than the rest of the population.

Closing the Social Security shortfall is particularly important to the Hispanic community. As a young population that is rapidly aging and that receives more in return for its contributions to Social Security than others, Hispanics have much invested in the future solvency of the system.

However, as this analysis indicates, the Hispanic community should be wary of changes that seriously threaten the benefits that Hispanics receive from the current system, under the guise of restoring solvency. Plans such as the President’s that rely solely on benefit reductions to close Social Security’s shortfall, and that would place the greatest burden on younger workers, would be more detrimental to the Hispanic community than alternative reforms. Hispanics also would be harmed by private-account plans that shrink the social insurance aspects of Social Security by linking each person’s benefits more directly to that person’s tax contributions without regard to whether the worker has earned low wages or encountered some major misfortune.

Hispanics’ retirement security needs to be strengthened. But substantially scaling back Social Security would have the opposite effect, as it is the one form of retirement security that now works well for the Hispanic community. Hispanics should instead be given incentives to increase the amounts they save for retirement and thereby to bolster their retirement security. This can be done by reforming the current system of retirement tax incentives to provide greater incentives and opportunities for low- and middle-income Americans workers and their families to build assets for retirement.

End Notes:

[1] Fernando Torres-Gil is Director of the UCLA Center for Policy Research on Aging and Acting Dean of the UCLA School of Public Affairs. Robert Greenstein is Executive Director, and David Kamin is a Research Assistant, at the Center on Budget and Policy Priorities.

[2] See Fernando Torres-Gil, Robert Greenstein, and David Kamin, “The Importance of Social Security to the Hispanic Community,” Center on Budget and Policy Priorities, June 28, 2005.

[3] National Council of La Raza, “The Social Security Program and Reform: A Latino Perspective,” June 2005, available at http://www.nclr.org/content/publications/download/32018.

[4] Although the President’s Social Security proposals have been widely reported as protecting benefits for all of those the bottom 30 percent of income earners, this is clearly not the case. A substantial number of low-income beneficiaries would be subject to benefit reductions. Those affected include elderly widows and divorced spouses, as well as low-income children of deceased workers. Such beneficiaries would be subject to Social Security benefit cuts, regardless of their income level, if they receive a Social Security spousal or survivors benefit that is based on the earnings of another person (usually a deceased parent or a spouse or ex-spouse) who was not in the bottom 30 percent of wage earners. Many spouses and children whose families were not poor while the family’s breadwinner was alive fall into poverty or low-income status after the death of the breadwinner; such people would face benefit reductions under the President’s plan. For more details, see Jason Furman, “New White House Document Shows That Many Low-Income Beneficiaries Would Face Benefit Cuts,” Center on Budget and Policy Priorities, May 10, 2005, available at https://www.cbpp.org/5-10-05socsec2.htm.

[5] Including the cost of the private accounts that the President has proposed, the President’s proposals close an even smaller share of the 75-year gap. Taken together, the President’s proposals would close only about 30 percent of the 75-year shortfall.

[6] This assumes an estate tax along the lines of the tax that is slated to be in effect in 2009, when the exemption from the tax will be $3.5 million per individual ($7 million per couple) and the top estate tax rate will be 45 percent.

[7] Census Bureau, Current Population Survey, March 2004, data available at http://ferret.bls.census.gov/ macro/032004/perinc/new10_001.htm.

[8] Census, U.S. Interim Projections by Age, Race, and Hispanic Origin, March 2004, available at http://www.census.gov/ipc/www/usinterimproj/.

[9] Lawrence Kotlikoff, “What’s Wrong?: Don’t Make the Kids Pay for Our Mess,” The Washington Post, January 23, 2005, Outlook p. B02.

[10] According to official government projections, Hispanics have substantially longer life expectancy than the rest of the population. Based on Census Bureau data, the Social Security Administration reports that Hispanic men turning age 65 in 2004 can expect to live an additional 20 years, compared to 16 years for all men, and Hispanic women aged 65 in 2004 can expect to live an average of 23 years, compared to 20 years for all women. The Government Accountability Office has come to similar conclusions, also using Census Bureau data, as have the Social Security actuaries. Several researchers have raised questions as to whether Hispanics’ longer-than-average life expectancies are real or are a product of measurement error. Even if Hispanics did not have longer-than-average life expectancies, they would receive well-above-average rates of return on their contributions to the Social Security system because they exhibit all of the other characteristics described here.

[11] The Hispanic population also has certain characteristics that would tend to lower Hispanics’ rate of return on their contributions to Social Security. In particular, a slightly smaller share of the elderly Hispanic population aged 65 or older is or has been married than is true of the rest of the elderly population. Thus, the Hispanic population may not benefit quite as much as the rest of the population from spousal benefits. According to official government measures, Hispanics of working age also have lower mortality rates than others of the same age, which would tend to reduce the benefits Hispanics receive from Social Security survivors benefits. The effects of these two characteristics, however, are substantially outweighed by the impact of the characteristics described in this analysis that significantly increase the rate of return that Hispanics receive on their Social Security contributions. On net, Hispanics receive a substantially higher rate of return on Social Security than the rest of the population.

[12] William W. Beach and Gareth G. Davis, “Social Security’s Rate of Return for Hispanic Americans,” Heritage Foundation, March 27, 1998, available at http://www.heritage.org/Research/SocialSecurity/CDA98-02.cfm.

[13] For detailed analysis of the problems with comparing the rate of return on private accounts to the rate of return on Social Security, see Jason Furman, “Would Private Accounts Produce a Higher Rate of Return Than Social Security?” Center on Budget and Policy Priorities, June 2, 2005, available at https://www.cbpp.org/6-2-05socsec.pdf.

[14] Craig Copeland, “Employment-Based Retirement Plan Participation: Geographic Differences and Trends,” Employee Benefit Research Institute Issue Brief, October 2004, available at http://www.ebri.org/ibpdfs/1004ib.pdf.

[15] Social Security Administration, “Income of the Population Aged 55 or Older, 2002,” March 2005, Tables 1.1 and 1.4, available at http://www.ssa.gov/policy/docs/statcomps/income_pop55/.

[16] Ibid., Tables 6.B1 and 6.B4.

[17] For a more detailed description, see Peter R. Orszag, “Improving Retirement Security,” Testimony Before the Committee on Ways and Means, May 19, 2005, available at http://www.retirementsecurityproject.org/pubs/File /Ways%20and%20Means%20Testimony%2020050517.pdf?PHPSESSID=d48df6046644e8926f38b1cbf74c337a.

[18] Brigitte C. Madrian and Dennis F. Shea, “The Power of Suggestion: Inertia in 401(k) Participation and Savings Behavior,” Quarterly Journal of Economics, vol. 116, no. 4, November 2001, Table 4.

[19] James J. Choi, David Laibson, Brigitte C. Madrian, and Andrew Metrick, “Defined Contribution Pensions: Plan Rules, Participant Decisions, and the Path of Least Resistance,” in Tax Policy and the Economy, vol. 16, James Poterba, ed. (MIT Press, 2002), pp. 67-113.

[20] Orszag, “Improving Retirement Security,” p. 8.

[21] NCLR, “The Social Security Program and Reform: A Latino Perspective.”

[22] This is not the case for citizens from the 20 countries with which the United States has “totalization” agreements in effect. Under these agreements, the United States coordinates Social Security benefits with the public pension systems that exist in those countries. Work in both countries can be counted toward the ten-year eligibility requirement for Social Security benefits, although to be eligible for “totalization” a worker must be employed in the United States for, at least, a year and a half. Initial Social Security benefits are then pro-rated, reflecting the number years of employment in the United States. Currently, Chile is the only Latin American country with which the United States has a totalization agreement that is in effect. The United States has signed such an agreement with Mexico, but the President has yet to submit it for Congressional review.