How Much of the Surplus Remains after

the Tax Cut?

by Richard Kogan, Robert Greenstein, and Joel Friedman

| PDF of full report HTML of fact sheet PDF of fact sheet If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

President Bush has signed into law a tax cut that costs $1.35 trillion between 2001 and 2011. The White House and some Congressional leaders are now suggesting that Congress consider further tax cuts as well as large defense spending increases. Other Members of Congress seek increases in domestic programs. The question we now confront is: how much of the budget surplus is left?

Congress has set aside funds in the budget plan it adopted in May for a Medicare prescription drug benefit and program expansions in health, agriculture, and several other areas. Congress also has repeatedly expressed its intention to "wall off" the surpluses in the Social Security and Medicare Hospital Insurance trust funds and use only the remainder, and has passed several measures to that effect. Taking into account the new tax-cut law and the other initiatives in the Congressional budget plan, the remaining surplus outside the Social Security and Medicare Hospital Insurance trust funds appears on paper to be about $500 billion between 2002 and 2011, with more than $300 billion of that amount occurring in the last two years. But such estimates are misleading. They rest upon several highly unrealistic assumptions, including the following.

- The $1.35 trillion package of tax cuts, as signed by the President, actually will expire on December 31, 2010, while several other provisions of the law — including a measure providing relief from the Alternative Minimum Tax — will expire between 2004 and 2006. These "sunsets" are not credible. It is unrealistic to assume the wholesale expiration of the tax cuts after 2010 or termination of AMT relief after 2004.

- There will be no extension of various expiring tax credits that are certain to be renewed, such as the very popular research and experimentation tax credit.

- Appropriations for non-defense programs over the next decade will be strictly limited to the level assumed in the budget plan that Congress adopted last month, a level $45 billion below what is needed for these programs simply to keep pace with inflation and much farther below what is needed for these programs to remain constant in real per-capita terms (i.e., for the appropriation levels for these programs to keep up with inflation and changes in the size of the U.S. population). Past experience strongly indicates that the level the new budget plan assumes for non-defense appropriations is unrealistic and unattainable. The bipartisan interest in boosting funding for education, health research, and other areas makes it even more likely that this level will not be met.

As this analysis shows, when the budget estimates are adjusted to reflect more realistic assumptions, the surplus that remains available over the next ten years essentially disappears. Nor can Congress count on being bailed out by new projections of much larger surpluses. Given recent data on productivity growth, it is questionable whether the surplus projections will continue to grow.

| When realistic budget assumptions are used, hardly any surplus remains after 2002 outside Social Security and Medicare. |

This suggests that Congress overreached in passing the tax-cut package so quickly, before the full extent of other budgetary needs had been taken into account, and in using an array of gimmicks to mask the size of the tax cut. This analysis indicates there is no room for further tax cuts — which would breach the tax-cut targets in the Congressional budget plan and thus require 60 votes in the Senate — unless they are accompanied by revenue offsets, most likely from scaling back the newly enacted tax cuts, closing unproductive tax breaks, or a combination of such steps. This analysis also indicates that Secretary Rumsfeld's forthcoming proposals to increase defense spending sharply, which are not reflected in the budget plan, will threaten to eat into the Social Security and Medicare Hospital Insurance surpluses unless the tax cuts are scaled back.

This analysis looks first at the effects of the new tax law on the projected surplus. It then considers other budget policies called for in the Congressional budget plan. (We refer in this analysis to the Congressional budget resolution as the "Congressional budget plan".)

Current Budget Projections and the Tax Cuts

In April, the Congressional Budget Office (CBO) released revised ten-year budget projections.(1) These projections show a unified budget surplus that grows from $304 billion in 2002 to $883 billion in 2011 and totals $5.6 trillion over the ten-year period from 2002 through 2011. Because Congress has voted repeatedly to wall off the surpluses in the Social Security and Medicare Hospital Insurance trust funds, however, the "available" surplus is less — $2.7 trillion over the decade, according to the CBO figures.

These CBO projections do not account for the newly enacted tax cuts. According to the official estimate of the Joint Committee on Taxation (JCT), which estimates the cost of revenue legislation for Congress, the tax cuts cost $1.275 trillion over the ten-year period from 2002 through 2011 (and the more familiar figure of $1.350 trillion when the costs in 2001 are included). CBO's projected surplus will be reduced by that amount.

The surplus also will be reduced to reflect the increased interest payments on the debt that will be paid as a result of the tax cuts. Enactment of the tax legislation means that surpluses will be smaller and the debt larger than CBO projected in April; therefore, over the next decade, interest on the debt will be higher than CBO projected in April. Using CBO's standard methodology for estimating interest costs, the increased interest payments on the debt will total $383 billion over the next ten years. The available, ten-year surplus is consequently reduced from $2.7 trillion to $1.1 trillion as a result of the tax cut, as shown in Table 1.

| Total budget surplus in CBO's April projection | 5,629 | |

| less: Social Security surplus | 2,487 | |

| less: Medicare HI surplus | 397 | |

| "Available" surplus (excluding Social Security and Medicare HI surpluses) | 2,745 | |

| Enacted tax cut: | ||

| Official Joint Tax Committee cost estimate | -1,275 | |

| Resulting increase in interest costs | -383 | |

| Cost of enacted tax cut, including interest | -1,658 | |

| "Available" surplus (excluding Social Security and Medicare HI surpluses) after enacted tax cuts | 1,087 |

|

| Note: May not add due to rounding. | ||

In January, CBO wrote that its projections for 2002-2011 were subject to considerable uncertainty. CBO simulated both a more favorable and a less favorable outcome and found its ten-year surplus could easily be higher than projected by as much as $3.2 trillion or lower than projected by as much as $3.6 trillion.(2) In this analysis, we use CBO's basic (or intermediate) projections. Given the high degree of uncertainty surrounding these projections, the budgetary situation could be considerably worse or better than the figures in this analysis indicate.

The Congressional Budget Plan

The Congressional budget plan calls for additional expenditures in various areas. The largest is $300 billion over ten years for a prescription drug benefit and "Medicare reform." Table 2 lists the major costs assumed in the Congressional budget plan, beyond the tax cut.

If Congress approves the expenditures called for in the budget plan, the $1.1 trillion available surplus shown in Table 1 will be reduced to approximately $500 billion over ten years, as Table 3 shows. Some $210 of this $500 billion occurs in 2011, however, and is in substantial part an artifact of the sunset of the new tax law at the end of 2010. For 2002-2010, the available surplus is only $287 billion.(3)

Taking Into Account More Realistic Assumptions

Unfortunately, the bottom-line figures in Table 3 can not be taken at face value. These figures overstate how much of the projected surplus remains, both because the tax bill and the Congressional budget plan omit the costs of various "must pass" items and other measures that are very likely or virtually certain to become law and because the official cost estimate of the tax bill substantially understates its cost as a result of the gimmicks written into the bill.

| Entitlement benefits, mandatory spending, and miscellaneous receipts: | ||

| Prescription drugs / Medicare "reform" | 300 | |

| Agriculture and natural resources | 74 | |

| Health insurance programs, net | 57 | |

| Other mandatory spending and revenues (including SEC fees)(5) | 48 | |

| Appropriated programs: | ||

| Defense | 35 | |

| Non-defense | -45 | |

| Net spending increases in the budget plan | 469 | |

| Resulting increase in interest costs | 121 | |

| Total additional costs | 590 | |

| Notes: May not add due to rounding. The health program changes shown above encompass the Family Care and Family Opportunity expansions of Medicaid/SCHIP, expenditure increases for health insurance coverage generally, increases for Medicare home health payments, and a tightening of the "upper payment limitation" regulations in Medicaid to prevent unwarranted payments to states. | ||

| 2002 | 9-year total through 2010 | 10-year total through 2011 | ||

| Available surpluses after the tax bill (from Table 1) | 53 | 779 | 1,087 | |

| Less: | Cost of remaining policies in Congressional budget plan (from Table 2) | -21 | -401 | -469 |

| Resulting increase in interest

costs (from Table 2) |

-1 | -91 | -121 | |

| Remaining available surplus (excluding Social Security and Medicare HI) | 31 | 287 | 497 | |

| Notes: May not add due to rounding. This table assumes that the $28 billion in "Family Care" funds in the budget plan are expended over more than the first three years of the budget period. | ||||

There are at least two areas in which costs not reflected in Table 3 are very likely or inevitable.

Expiring Tax Credits: The new tax-cut measure fails to extend a number of popular existing tax credits that are scheduled to expire every few years but always are extended on a bipartisan basis. One example is the research and experimentation tax credit, currently authorized through 2004. President Bush's budget proposed to make this credit permanent, a move that enjoys overwhelming bipartisan support. Congress left this proposal out of the tax bill, knowing that extension of the credit will be enacted as part of a subsequent piece of tax legislation. Congress intends to extend the other expiring tax credits as well. Extending these credits will cost $78 billion over ten years.

Non-defense appropriations. As Table 2 showed, the Congressional budget plan reduces non-defense appropriations by $45 billion over ten years below the levels needed to keep pace with inflation. If, within that constrained total, favored areas such as education and health research are to be increased, as seems very likely, the reductions in other areas must be deeper. Such reductions are quite unlikely to be made, however, especially since neither the President nor the Congressional leadership has made any public case for such budget cuts. To the contrary, the public rhetoric is that there is plenty to meet all needs.

The minimum level of non-defense funding that Congress is likely to approve is above CBO's projected "baseline" levels. CBO's baseline levels assume that appropriations will keep pace only with inflation. By itself, an inflation adjustment does not account for growth in the U.S. population. Stated differently, if appropriations grow only with inflation, the purchasing power of the resources available for non-defense appropriated programs will shrink on a per-person basis. If applied to funding for education, for example, this would mean that as the student population grows, each student or classroom would have less real resources. Another example is that, as the U.S. population grows, the need for highway repairs or mass transit operating costs rises more quickly than inflation.

History indicates that, at the least, Congress will keep funding for non-defense discretionary programs constant in real per-capita terms (i.e., even with inflation and population growth). Appropriations for non-defense discretionary programs have risen at a faster average rate than that over the past 15 years, including during years of budget deficits.

During the past 15 years, expenditures for non-defense discretionary programs have remained constant as a share of the U.S. economy, a rate of growth that is consistent with the Congressional Budget Office's long-term forecast of the trajectory of non-defense discretionary spending. Given that funding for non-defense discretionary programs remained constant as a share of GDP — which means it increased in real per-capita terms — in times of deficits, it is not realistic to assume (as the Congressional budget plan does) that such funding will be cut in real per-capita terms in times of budget surpluses. That such an assumption is unrealistic is underscored by the fact that the only case the President and Congressional leaders have taken to the public for changes in funding levels for specific non-defense discretionary programs is the case they have presented for increases in non-defense discretionary spending in areas such as education and health research.

If Congress ends up keeping overall funding for non-defense appropriated programs at today's level in real per-capita terms (i.e., after adjusting for inflation and changes in the size of the U.S. population), expenditures for these programs will be $208 billion higher over the next ten years than the level the Congressional budget plan assumes.(6)

The Remaining Surplus Using More Realistic Assumptions

As Table 3 indicated, $497 billion in projected surpluses outside the Social Security and Medicare Hospital Insurance trust funds remain when the official cost of the tax bill and the other items in the Congressional budget plan are taken into account. But when the realistic assumption is made that the research and experimentation credit and the other expiring tax credits will be extended and non-defense discretionary appropriations will keep pace with inflation and population growth, the lion's share of this remaining surplus disappears. Making these reasonable assumptions reduces the "available" surplus by a little more than $340 billion over ten years.

This appears to leave approximately $154 billion over ten years. As Table 4 shows, however, the bulk of that surplus occurs in 2011 and is the result of the provision of the tax bill that terminates the tax cuts after 2010. For the years from 2002-2010, only $14 billion remains to deal with all of the following:

- The defense spending increases the Pentagon is expected to seek, which could amount to several hundred billion dollars over the decade.

- Relief from natural disasters, such as hurricanes, floods, and earthquakes. These expenditures have been averaging $5.6 billion a year according to the Office of Management and Budget.

| 2002 | 9-year total 2002 - 2010 | 10-year total 2002 - 2011 | ||

| Available surpluses after the tax bill and Congressional budget plan (from Table 3) | 31 | 287 | 497 | |

| Less: | Cost of extending the R&E tax credit and other expiring credits | 0 | -64 | -78 |

| Cost of keeping non-defense funding level with inflation and population | -2 | -168 | -208 | |

| Resulting increase in interest costs | 0 | -41 | -57 | |

| Remaining available surplus (excluding Social Security and Medicare HI) | 29 | 14 | 154 | |

| Note: May not add due to rounding. | ||||

- The artificial sunsets in the new tax-cut law, including the expiration of AMT relief after 2004 and the sunset of the entire law after 2010. The Joint Tax Committee estimates that reversing these sunsets and providing AMT relief would cost $386 billion over the next ten years (with the bulk of that being the cost of AMT relief; see the box on page 7 for a further discussion of the AMT issues.) Other needs that policymakers and the public may wish to address, such as restoration of long-term solvency to Social Security and Medicare (see box above), further steps to reduce the number of Americans who lack health insurance, and efforts to reduce child poverty. These needs also may include providing funding beyond the level the budget plan assumes for a prescription drug benefit. Many analysts have questioned whether Congress ultimately will be able to provide a drug benefit that the public finds adequate for $300 billion over ten years, the level reflected in the Congressional budget plan. While initial prescription drug legislation may be designed to cost this amount, such legislation is likely to be expanded upon in subsequent years when the public sees the limited nature of the drug benefits that the initial legislation provides.

Social Security and Medicare Reform An omission from the Congressional budget resolution is any plan to deal with the long-term financing problems that beset the Social Security and Medicare Hospital Insurance trust funds. As is well known, these trust funds are accumulating assets now that will be drawn down when the baby-boom generation retires, and the trust funds eventually will become insolvent if nothing is done to prevent that from occurring. The payroll tax increases and Social Security and Medicare benefit cuts that will be needed to bring these trust funds into long-term balance if no additional resources are provided to these programs are unacceptably large from a political standpoint. They cannot pass. This is why nearly every plan in recent years to restore long-term Social Security solvency has relied in part on transferring some of the surpluses projected in the non-Social Security budget to the Social Security Trust Fund. (It also is why no member of either party has advanced a plan that would fully restore long-term Medicare solvency.) President Clinton proposed transfers of non-Social Security surpluses to Social Security. So did the Social Security plan put forward in the last Congress by then-Ways and Means Committee chairman Bill Archer and Social Security subcommittee chairman Clay Shaw. The plans proposed by Reps. Jim Kolbe and Charles Stenholm in the House and Senators Gregg, Breaux, Grassley, and others in the Senate also include such transfers. Restoration of long-term solvency to these trust funds is likely to prove politically impossible without additional resources from the rest of the budget; otherwise, the magnitude of the Social Security and Medicare benefit cuts or payroll tax increases needed to restore long-term solvency will almost surely doom any solvency plan. Prudent budgeting consequently entails making an allowance for these transfers. The Congressional budget plan makes no such allowance. (Past Center analyses suggest that a minimum of about $500 billion over ten years — an amount that would cover only a modest faction of the unfunded liabilities of these trust funds — is likely to be needed for this purpose.) |

How to Address this Dilemma

The clearest lesson that emerges from this analysis is that unless Congress wishes to dip into the Medicare Hospital Insurance or Social Security surpluses to address these budget pressures, hardly any of the available surplus remains. This strongly suggests that policymakers need to adopt and adhere to a policy of holding the cost of the new tax law to no more than its official cost of $1.35 trillion over 11 years. This means both that:

- Any repeal of the various sunsets in the new tax law — including the sunset of the provision granting AMT relief through 2004 and the sunset of the entire law after 2010 — should be offset by scaling back other provisions of the law (generally provisions that have not yet taken effect), by other revenue-raising measures such as the closing of unproductive tax loopholes, or by a combination of these approaches; and that

- Any new tax cuts should be fully offset in the same manner. (This does not apply to the extension of the research and experimentation tax credit or other expiring tax credits not included in the new tax law; in this analysis, the costs of these extensions are already included as part of the cost of using realistic rather than fanciful budget assumptions.)

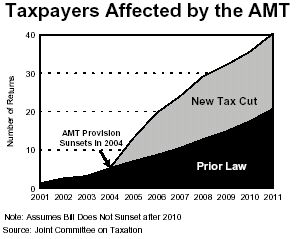

The Sunsets in the New Tax Law One of the principal devices used to hold down the new tax law's cost is a provision in the law that terminates all of its tax cuts at the end of 2010. Few observers expect that wholesale elimination of the tax cuts actually will occur after 2010. In addition, several tax cuts in the law are scheduled to expire earlier — in 2004, 2005, or 2006. For example, a provision to prevent the tax-cut law from causing millions of additional taxpayers to become subject to the Alternative Minimum Tax (AMT) expires in 2004. Extension of this provision or some other provision providing AMT relief on an ongoing basis is likely to be "must pass" legislation for a future Congress, which, of course, is what the framers of the tax law intended. These "sunsets" were designed to make the legislation comply on paper with the limit on tax cuts set forth in the Congressional budget plan. The issues relating to the Alternative Minimum Tax are of particular note. In the years after 2004, the tax law's reductions in income tax rates will reduce regular income taxes significantly, without modifying the AMT. The law consequently will greatly increase the number of taxpayers who become subject to the AMT, since many taxpayers' AMT liability now will exceed their regular income tax liability.

The Joint Committee on Taxation estimates that once the new law's AMT relief terminates after 2004, the number of taxpayers affected by the AMT will swell to 35.5 million by 2010. By comparison, the AMT will affect 1.4 million taxpayers in 2001 and 5.3 million taxpayers in 2004. Congress is likely to act to prevent 35 million taxpayers — including many middle-class taxpayers — from becoming subject to the AMT. Such action, however, will be costly. For instance, the Joint Tax Committee estimates that it would cost $247 billion through 2011 just to keep the number of taxpayers affected by the AMT at the levels projected prior to enactment of the tax-cut law — which would still mean that more than 20 million taxpayers would be subject to the AMT in 2011. |

The basic principle here essentially is that set forth in a recent New York Times editorial: further tax cuts that exceed the amount Congress allotted for tax cuts in the Congressional budget plan should be paid for by scaling back the new tax-cut law or providing offsetting revenues in other ways.

| If policymakers do not want to dip into the Medicare or Social Security surpluses or to abandon other priorities (such as a prescription drug benefit), they will need to forgo further tax cuts and to hold the new tax-cut law's total cost — including the cost of addressing the termination of AMT relief after 2004 — to the $1.35 trillion the budget plan allotted. |

Even with such a step, difficult choices remain. A more adequate prescription drug benefit, large defense increases, and other unmet domestic and international needs will compete with each other for the very limited resources that remain. To address this problem, Congress likely will have to use part of the Social Security and Medicare surpluses, raise further revenues (or scale back other elements of the tax cut before they take effect), or cut popular programs. Moreover, without additional resources, it seems unlikely that measures to restore long-term Social Security or Medicare solvency will be able to be enacted.

The history of the early 1980s may be instructive here. In 1981, Congress and a new President overreached in passing a tax cut too large for the budget realities of the time. Congress and the Administration subsequently found they needed to revisit that tax cut in two of the next three years and reduced its size about 30 percent.(7) The pattern could be repeated in the years ahead.

End notes

1. The new CBO projections are contained within An Analysis of the President's Budgetary Proposals for Fiscal Year 2002, CBO, May 2001. Available at http://www.cbo.gov/showdoc.cfm?index=2819&sequence=0&from=7.

2. See Surplus or Deficits? Projections of A Large Budget Surplus Are Surrounded by a High Degree of Uncertainty, Center on Budget and Policy Priorities, February 6, 2001. Also see chapter 5 of The Budget and Economic Outlook: Fiscal Years 2002-2011, CBO, January 2001, available at http://www.cbo.gov/showdoc.cfm?index=2727&sequence=0&from=7.

3. The available surplus of $31 billion in 2002 is the result of another gimmick in the tax bill. The tax legislation changed the date on which corporations pay their estimated taxes by a few days in order to shift $33 billion in revenues from 2001 to 2002. Had Congress not written this gimmick into the legislation, there would be no room left for any 2002 costs beyond those reflected in the Congressional budget plan. The conferees on the tax-cut bill went out of their way to create a timing gimmick to create $31 billion of room.

4. The Congressional budget plan is set forth in the Congressional budget resolution, adopted May 10, 2001. The budget resolution is not a law but a budget framework that provides budget allocations to the Congressional committees that write tax, entitlement, and appropriations laws. For non-defense appropriations, the Congressional budget plan adopted in May shows, in effect, only grand totals. These grand totals are not sufficient to cover the current (i.e., the FY 2001) level of non-defense funding plus inflation, but the budget plan is silent on how or where the reduction in real resources should be made. Does this mean Congress consciously decided to abandon increases in education, for example? No, it means only that Congress was not willing to commit to a specific level of education funding and, as a consequence, to show where the offsetting cuts should occur.

5. The numbers in this report reflect the costs and surpluses included in the Congressional budget plan as it was approved. In the Senate, there is a "hold harmless" procedure to adjust committee spending allocations and total revenue targets whenever a "reconciliation bill" (such as the tax cut just enacted) makes overall changes in outlays and revenues equal to the overall amount called for in the congressional budget plan, but in different proportions (between outlays and revenues) than the budget called for. When the Senate applied this procedure, however, it apparently double-counted an element of the tax bill involving refundable tax credits. The result is that the Senate Finance Committee has ended up with a $19 billion smaller remaining allocation for program increases than was reflected in the Congressional budget plan as agreed to on May 10 and than is available to the House of Representatives. The figures presented in this paper are consistent with the Congressional budget plan as agreed to on May 10 and as in effect in the House.

6. Adjusting for inflation and population is the same standard that President Bush used during his campaign and the Bush White House has used in recent months in describing changes in state spending in Texas during George W. Bush's tenure as governor. For example, the George W. Bush for President official web site states: "When adjusted for inflation and population, state spending will increase by only 3.6 percent between 1994-1995 and the end of the 2000-2001 biennium." Similarly, the Dallas Morning News reported: "Wednesday, [Governor Bush] said an 'honest comparison' of spending growth should take inflation and the state's increasing population into account" (October 28, 1999).

7. Since the income tax code was not indexed for inflation at the time the Reagan tax cut was enacted, a portion of that tax cut simply offset the effect that future inflation otherwise would have had in raising taxes. The tax increases enacted in 1982-1984 offset an even larger share (i.e., more than 30 percent) of the portion of the Reagan tax cut that reduced taxes as a share of people's incomes rather than simply offsetting the effects of inflation.