ALTERNATIVE MINIMUM

TAX BILL IN THE HOUSE OFFERS

ANOTHER LARGE DOSE OF BUDGET GIMMICKRY

by

Joel Friedman and

David Kamin

|

PDF of report |

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

On May 5, the House of Representatives is

expected to consider legislation that would extend Alternative Minimum

- The House legislation is reported to cost $17 billion, which may make it sound modest. But the House approach of extending AMT relief for just one year does not reduce the long-term cost of such relief. The long-term cost of AMT relief remains the same, whether done all at once or in ten one-year increments. So while the $17 billion price tag may create the illusion of a low cost, Congressional Budget Office estimates show that AMT relief similar to the proposal in the House bill would cost $376 billion over ten years.[1] That is 22 times the cost of the one-year measure coming to the House floor.

- Moreover, even this $376 billion estimate substantially understates the long-term cost of AMT relief, because it assumes that all of the tax cuts enacted since 2001 will expire on schedule. If one assumes instead that the President’s proposals to extend the tax cuts enacted since 2001 are adopted, the cost of this AMT relief jumps to $549 billion over the next ten years, according to CBO. The CBO estimates also show that when the higher interest payments on the debt associated with this AMT relief are taken into account, the total impact on the deficit climbs to $658 billion over the decade.

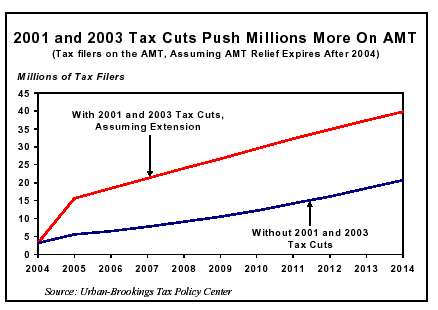

- In the absence of an extension of AMT relief, about 29

million taxpayers would be subject to the AMT in 2010, according to the

Yet, no one believes this will really occur. Virtually all policymakers — including the Administration — expect AMT relief to be extended in some form, and the Administration has stated on a number of occasions that it plans to propose ongoing AMT relief legislation in the future. Nevertheless, the official cost estimates assume that AMT relief will not be provided in the future — and thus that the AMT will cancel out a significant portion of the 2001 and 2003 tax cuts and their extension, leading the official cost estimates of those measures to understate substantially their true cost. In brief, that is how the AMT operates as a budget gimmick.

- Despite acknowledging the need for ongoing AMT relief, neither the Administration nor Congressional leaders are willing to propose permanent AMT relief just yet. Doing so would cause other tax-cut legislation they support — particularly proposals to make the 2001 and 2003 tax cuts permanent — to carry much higher price tags. Just last week, the House passed a measure to make permanent the tax reductions for married couples enacted in 2001 and 2003. The official cost of the measure is $105 billion through 2014, according to the Joint Committee on Taxation. Yet that is only about half of the true cost of the measure; other Joint Committee on Taxation estimates show that if the AMT does not cancel some or all of these tax-cut benefits for millions of couples, the cost of the measure rises to $204 billion. The official cost estimate was cut nearly in half through the use of the highly doubtful assumption that no AMT relief would be available and that tens of millions of families would be swept on to the AMT.

The Growing Reach of the AMT

The Alternative Minimum

Unlike the regular income tax code, however, the key parameters of the AMT are not indexed for inflation. As a household’s income rises over time with inflation, its regular income-tax liability does not increase (in inflation-adjusted terms) while its AMT liability does. Over time, therefore, more and more households will see their AMT liability exceed their regular income-tax liability and become subject to the AMT, unless AMT relief is provided.

This problem was made far more severe by the

2001 and 2003 tax-cut legislation, which reduced tax liabilities under the

regular income tax code without making corresponding adjustments in the

AMT. Today, about 3 million households face the AMT. According to

AMT Kept in Check by Temporary Provisions

Since 2001, the AMT has been kept in check largely by temporary provisions that have increased the amount of income exempt from the AMT. The 2001 tax-cut package provided for higher AMT exemption levels through 2004. These levels were then increased (to $58,000 for a married couple), but not extended, by the 2003 tax cuts.

The higher exemption levels are slated to

expire at the end of 2004. If allowed to expire, about 8 million more

households would be subject to the AMT in 2005, according to the

Like the AMT relief enacted in 2001 and 2003, the pending House AMT-relief bill (H.R. 4227) provides only a temporary fix. It extends the 2004 exemption levels, indexed for inflation, through 2005, and then allows this AMT relief to expire after just one year. This keeps down the official cost both of the AMT relief bill and of other tax-cut extensions Congress is now considering.

Piecemeal Approach to AMT Relief Designed to Hide Costs

This piecemeal strategy to AMT relief obscures the relief’s true cost. That cost will be the same in the years ahead regardless of whether ongoing AMT relief is enacted or relief is continually extended just for one or two years at a time. By breaking AMT relief into pieces that only last for a one or two years, the Administration and the House Republican leadership apparently hope to gain two advantages. First, they do not have to acknowledge the overall cost of AMT relief, making the overall budget situation seem less grim than it is. The one year of AMT relief in the pending House bill will reportedly reduce revenues by $17 billion through 2006. By contrast, permanently adjusting the AMT for inflation would reduce revenues by $549 billion over the next ten years, according to CBO, assuming that the expiring 2001 and 2003 tax cuts are extended as the Administration has proposed.[2] And the added interest costs on the debt would amount to another $109 billion, bringing the overall impact of AMT relief on the deficit to $658 billion over the coming decade.

Second, under the piecemeal strategy, the Administration and its Congressional allies are able to continue using the AMT as a major budget gimmick to reduce artificially the cost of their other tax-cut proposals. As noted, the 2001 and 2003 bills were designed to take full advantage of the AMT; with AMT relief provided only through 2004, the official cost estimates for the 2001 and 2003 bills are based on the assumption that those bills would push millions more taxpayers onto the AMT after 2004 and that the AMT would claw-back some of the tax cuts these millions of taxpayers were being promised. This substantially reduced the official cost estimates of the tax cuts, even though the designers of the tax cuts never intended to allow these millions of Americans actually to become subject to the AMT.

Keeping AMT relief temporary, along with the other gimmicks employed in the 2001 and 2003 tax-cut measures such as slow phase-ins and artificial sunsets, caused the official cost estimates of the 2001 and 2003 tax cuts to vastly underestimate the true budgetary impact of those measures. House Ways and Means Committee Chairman Bill Thomas, the chief Republican tax-writer in the House, acknowledged in 2001 that these gimmicks allowed more tax cuts to be crammed into the 2001 bill, likening it to “putting a pound and a half of sugar into a one pound bag.”[3] After passage of the 2003 tax bill — which was officially estimated to cost $350 billion — House Speaker Dennis Hastert frankly admitted that the cost estimate had been gamed. He said, “The $350 [billion] number takes us through the next two years, basically. But also it could end up being a trillion-dollar bill, because this stuff is extendable.”[4]

|

Revenue-Neutral AMT Relief AMT relief has the potential to be very expensive. The Treasury Department estimates that by 2013, repealing the AMT system would actually be more costly than doing away with the entire income tax system (assuming the 2001 and 2003 income tax cuts have been extended). As noted elsewhere in this analysis, simply extending the current form of AMT relief would increase deficits by more than $650 billion over the next ten years, counting the added interest costs (and assuming the 2001 and 2003 tax cuts are extended). Given the nation’s grim fiscal outlook, with large deficits extending “as far as the eye can see,” the federal government cannot easily afford such costly AMT legislation. Fortunately, it is possible to prevent most middle-class filers from falling under the AMT without incurring such significant costs. The Tax Policy Center has designed an option to restructure the AMT in a cost-neutral manner. This option would free most middle-class taxpayers from the AMT and offset that cost by making the AMT tougher on high-income taxpayers who employ multiple tax breaks, especially taxpayers at very high income levels, who currently are barely touched by the AMT.* Such a proposal, however, would be likely to encounter strong opposition from the Administration and on Capitol Hill. ________________ |

Long-term AMT relief would make the true costs of Administration and Congressional tax cuts more apparent, showing them to be much higher than advertised. Indeed, while an AMT problem existed before enactment of the 2001 and 2003 tax cuts, those tax cuts exacerbated the problem to such a degree that about 60 percent of the cost of indexing the AMT from 2005 to 2014 can be attributed to those tax cuts. Stated another way, the cost with interest of extending the Bush tax cuts is not $1.3 trillion between 2005 and 2014, as reflected by the official estimates, but $1.7 trillion when the anticipated extension of AMT relief is taken into account.[5]

The impact of the AMT on the cost of extending the Bush tax cuts was vividly illustrated just last week, when the House considered a measure to extend and make permanent the tax cuts for married couples enacted in 2001. The official cost of that bill is $105 billion through 2014, according to the Joint Committee on Taxation. But the Joint Committee on Taxation’s estimate assumes that the tax cuts in the bill would cause more married couples — more than 8 million a year after 2010 — to be subject to the AMT, and that the AMT would partially or entirely eliminate the bill’s tax reductions for millions of couples. Joint Committee on Taxation data show that if the AMT does not cancel out the tax cuts for married couples — a more plausible assumption — last week’s measure will cost $204 billion, or nearly twice as much.

Conclusion

The House is scheduled to consider this week a bill to extend AMT relief through 2005. This bill fits into a continuing strategy of using the AMT as a tool for budget gimmickry. Extending AMT relief for only one year obscures the long-term cost of such relief. In addition, by keeping AMT relief temporary for now, the Administration and members of Congress are able to understate substantially the cost both of the tax cuts enacted to date and various pending tax-cut proposals, including proposals to make the 2001 and 2003 tax cuts permanent.

End Notes:

[1] The House bill calls for continuing the higher exemption amount for the AMT, which was set in 2003 and is scheduled to expire at the end of this year, and indexing it for inflation after 2004. The CBO option assumes that, in addition to the exemption amounts, the AMT tax brackets are also indexed for inflation. See Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2005-2014, January 2004, Table 1.3.

[2] In addition to indexing the AMT parameters, it is likely that, at a minimum, AMT relief would also include allowing certain tax credits to count for AMT purposes. This provision expired at the end of 2003, and the House bill does not provide for its extension. But it is one of a group of temporary tax provisions (known as “extenders”) that, in the past, have been routinely renewed. Even though the provision was allowed to lapse this year, it is widely expected that it will be renewed, along with other extenders that have lapsed, retroactive to the beginning of 2004. If it is made permanent (or continually extended) along with indexing, the cost of AMT relief rises to $591 billion between 2005 and 2014. When the associated interest costs are included, the ten-year total would be $708 billion.

[3]

Representative William Thomas, “News Conference with Representative

Bill Thomas, Chairman of the

[4]

Mark Wegner and Richard E. Cohen, “Hastert Salutes ‘Trillion-Dollar’

[5] See Isaac Shapiro and Joel Friedman, “Tax Returns: A Comprehensive Assessment of the Bush Administration Tax Cuts,” Center on Budget and Policy Priorities, April 2004.