From Rags to Riches to Rags?

The D.C. Council Tax Plan

by Iris J. Lav

Table of Contents I. High Cost Likely to be Unaffordable II. Is $419 Million the Full Cost of the Plan? III. A "Supply-Side" Response? |

Summary

District of Columbia Councilmembers Jack Evans and David Catania, along with seven other members of the Council, have introduced a tax cut plan that would reduce D.C. revenue by at least $419 million a year when fully in effect. The major features of the plan include income tax reductions for individuals, corporations and nonincorporated businesses, and cuts in property taxes on commercial buildings and residential rental buildings.

While the tax cut was put forth in the name of improving economic development, mainstream economic research suggests it is unlikely that much increased business activity or employment would result from these changes. Moreover, this tax cut plan is far more expensive than it would appear the District can afford at this time. The plan carries a strong risk of returning the District to budget deficits or declining service levels.

A disproportionate share of these costly tax reductions would benefit the District's highest-income residents; some 65 percent of the benefits of the individual income tax cut, for example, would go to the highest income 20 percent of District households. At the same time, the plan leaves unaddressed problems in the tax system that result in unusually high tax burdens on working families with incomes modestly above the poverty line. Less than eight percent of the cost of the tax cut would benefit the lowest-income 40 percent of D.C. households.

Among the issues the Council plan raises are the following:

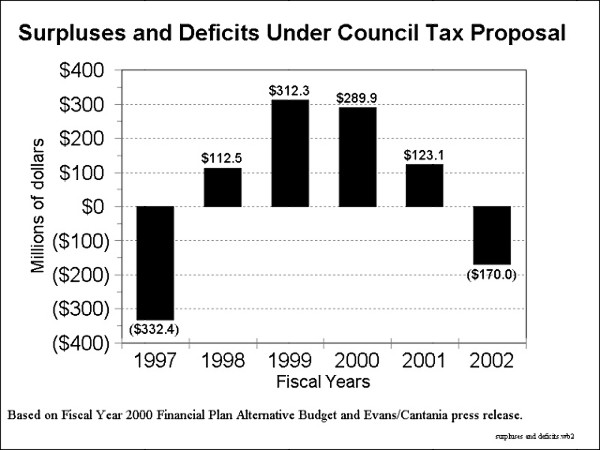

- The District's Financial Plan projects surpluses of revenues over expenditures over the next five years of between $100 million and $200 million annually. Surpluses of this magnitude cannot support a tax cut that reduces revenues by at least $419 million a year. Table 1 shows the cost of the tax cut relative to projected budget surpluses. This calculation is made utilizing using the same data and methodology as presented in the sponsors' press release; the only difference is that the sponsors stop their presentation in the year 2000, while Table 1 continues the analysis through 2002. The table shows that by fiscal year 2002, the cost of the tax cut would have expended accumulated surplus funds and the District budget would once again be in deficit.

- When fully in effect, the plan would eliminate about one dollar out of every eight the District receives in taxes and other own-source revenue. The magnitude of the cut — at least $419 million annually — is approximately the amount of all District annual expenditures for police and fire protection. All else being equal, significant service reductions would be required to compensate for the lost revenue. While it is possible that efficiency savings beyond those already assumed in the financial plan could compensate for a modest share of revenue reductions, few if any jurisdictions have achieved savings of this magnitude without reducing the level or quality of public services. Moreover, it is risky to spend "efficiency savings" before they materialize.

| Table 1 Surpluses and Deficits Under Council Tax Proposal Assuming Deferral of Long-Term Debt Repayments (Millions of dollars) |

||||

| Fiscal Year |

Annual Surplus |

Fund Balance Before Tax Cut |

Annual Tax Reduction Cost |

Net Surplus or Deficit |

| 1997 | $(332.4) | $(332.4) | ||

| 1998 | $444.8 | 112.5 | 112.5 | |

| 1999 | 199.8 | 312.3 | 312.3 | |

| 2000 | 101.4 | 413.7 | $123.8 | 289.9 |

| 2001 | 112.9 | 402.8 | 279.7 | 123.1 |

| 2002 | 124.8 | 247.9 | 418.8 | (170.9) |

| Surpluses are from the Fiscal Year 2000 Financial Plan and are the sum of the budget basis surplus (line 33) and the amounts set aside for the Mayor's tax restructuring plan (line 7). Note that the annual surplus for 1998 includes a one-time $198 million payment from the federal government. | ||||

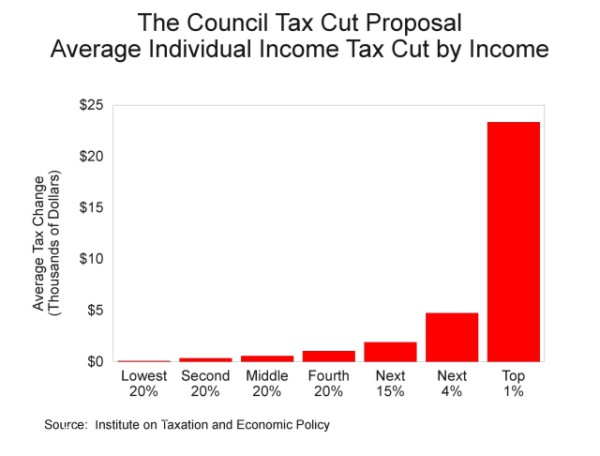

- The plan sponsors indicate that the individual income tax would be cut by $236 million, giving individuals 56 percent of the benefits of the tax plan. The individuals that would benefit, however, are disproportionately the District's best-off residents, according to analysis by the nonprofit research group The Institute for Taxation and Economic Policy. As noted, nearly two-thirds (65 percent) of the benefits would enrich the highest-income 20 percent of all District residents.

- Families with incomes between $13,000 and $28,000, for example, would get an average tax cut of $343 each. By contrast, the highest-income one percent of District families, with incomes exceeding $500,000, would get a tax cut averaging $23,000 apiece.

- The annual cost of the individual income tax cut is likely to exceed the estimated $236 million the sponsors indicate would be the cost in 2002. A $236 million cost would represent a 23 percent reduction from expected 2002 individual income tax revenues of $1,037 million. But the plan would cut the top individual income tax rate by 31.6 percent, and the other rates would be reduced by 37.5 percent and 50 percent respectively. With an average rate cut of 33 or 34 percent, a 23 percent reduction in revenue would seem to be a significant underestimate.

- One out of every six dollars the District would lose as a result of the proposed income tax cut would not benefit District residents but instead go to enrich the federal treasury. District residents who itemize their deductions for federal tax purposes would have a smaller state and local tax deduction and thus would pay higher federal income taxes.

- Extensive research on the relationship between taxes and economic development was commissioned, evaluated, and reported recently by the District of Columbia Tax Revision Commission. The Commission, which made its final report in June 1998, was appointed by the mayor and the city council to review and recommend changes in the District's revenue system that would enhance revenue productivity, stability, efficiency, equity, simplicity, and competitiveness. The research prepared for the Commission finds little support for the contention that cutting taxes on higher-income individuals and corporations, as proposed in the Council plan, would increase District population or employment or make the District more "competitive." Indeed, such tax cuts risk just the opposite, since there is evidence that the levels of public services such as schools and roads do influence private sector employment growth.

- There are a number of areas in which District taxes could be improved and reduced, within the limits of what can be afforded without squeezing the services that District residents expect and need. Reducing the property tax rate on residential rental buildings to a level equal to the residential homeowner rate, for example, is a provision of the Council proposal that also was endorsed by the D.C. Tax Revision Commission — subject to the availability of revenues to finance the change.

For the individual income tax, however, the Commission found problems with the structure of the tax that would not be addressed by the rate cuts in the Council plan. These include the extraordinary high burden the District imposes on working families with incomes modestly above the poverty line, for whom the income tax burden jumps from zero to several hundred dollars when family income rises by one dollar over the amount exempted by the low-income credit.

The Tax Commission made a number of recommendations for tax reform on a revenue-neutral basis, that is, reforming taxes without increasing or decreasing revenues. With respect to the individual income tax, the Commission addressed the problem of taxes on near-poor families and other problems in the structure of the income tax by conforming the District income tax to the federal definition of taxable income. Even if the District finds it can afford to cut individual income tax rates, it should first implement reforms such as those Commission recommended to fix longstanding problems in its tax code. These structural changes alone — without lowering rates — would reduce taxes on the low- and moderate income families that make up 60 percent of the District's residents.

If the District decides to reduce taxes, there are a number of possible ways to do so that are more equitable and more affordable than the Council's plan, and that would not risk a return of deficits or service reductions at a time when the District is finally reaching a sound financial footing and residents are counting on service improvements.

High Cost Likely to be Unaffordable

It can be easy for a government to feel "rich," that is, well-funded, when the economy is humming and stock prices are soaring. The federal government and most states with an income tax are running surpluses this year, largely as a result of higher than expected capital gains taxes. The District of Columbia, expecting to take in $200 million more than it is spending for the fiscal year ending September 1999, is no exception. This will be the second consecutive year of surplus, following five years of deficits that resulted in an accumulated debt of more than $500 million.

This good economic and fiscal news has led a number of members of City Council and others to conclude that the District can afford a large tax cut. The Council tax cut proposal would reduce annual revenue by approximately $419 million a year by fiscal year 2002 — according to the figures supplied by the Council sponsors.

As noted in the box on page 7, this may be an understatement of the cost. The individual income tax reduction is estimated by the sponsors to reduce revenues by 23 percent, even though the rate reductions are far deeper, ranging from 50 percent in the lowest bracket to 31.6 percent for the top bracket. These rate reductions imply loss of about one-third of total individual income tax revenue.

The first few years of this tax cut seem affordable both because the cost is phased in over three years and because accumulated surpluses from prior years would be used to support its cost. Under current projections, however, the tax cut would bring back budget deficits by 2002.

Table 1 shows that surpluses accumulated in the years 1998 through 2000 are used to finance the first two years of the tax cut. This is a key point; the annual size of the tax cut exceeds reasonable expectations of annual surpluses. Its financing depends on utilizing surpluses built up over the past few years. By the third year, however, the accumulated surpluses are fully expended. The tax cut in its third year would result in a deficit of more than $170 million for fiscal year 2002. Were the tax cut to be maintained in future years, the size of the deficit would grow in years subsequent to fiscal year 2002.

The annual surpluses shown in Table 1 are taken from the District's fiscal year 2000 Financial Plan. To avoid confusion, these surpluses are computed in exactly the same way as was used to derive the surpluses shown in the press release for the Council plan. The difference is that the Council plan press release looks at the cost of the tax cut package and the surpluses available to support that tax cut only through fiscal year 2000. Table 1 extends those calculations, using the same methodology, through 2002.

A couple of points are worth noting about the surpluses shown in the Mayor's financial plan. First, the surpluses depend on an assumption of significant savings from managing the District government more efficiently. In fiscal year 2000, efficiency savings of $72 million are assumed. The assumed savings grow to over $100 million in fiscal year 2001 and to nearly $140 million in fiscal year 2002. If these efficiency savings cannot, for whatever reason, be accomplished, there would little if any surplus available for a tax cut.

Is $419 Million the Full Cost of the Plan? The press release the Council issued on April 15, 1999 states: "When fully implemented, District taxpayers will realize an annual tax savings of approximately $419 million, with individuals enjoying 56 percent of the benefits for a total of $236 million." The $236 million refers to the cost of the personal income tax cut, as shown on the chart accompanying the press release. Common sense, as well as analysis, suggests that the proposed personal income tax cut would cost more than $236 million when fully implemented.

|

In addition, the financial plan assumes a reduction in debt service costs for long-term debt of $50 million a year in fiscal years 2000 through 2004. This would be accomplished by refinancing a portion of the debt in order to lengthen the number of years over which the debt would be repaid and thus to defer costs to future years. Given the District's recent fiscal history, it is far from certain that this refinancing will be found acceptable. If those debt payments are not deferred, the deficit shown in Table 1 would rise to $321 million in fiscal year 2002.

Since the District has no means to cover such deficits, it is reasonable to suppose that a tax reduction of $419 annually would require major reductions in expenditures for District programs and services. For 2002, the Mayor's financial plan estimates tax collections and other District-source revenue will total $3,303 million. The Council tax plan would reduce that figure to $2,884 million eliminating about one dollar of revenue out of every eight the District raises. In the practical experience of jurisdictions around the country, revenue reductions of that magnitude have rarely been accommodated without cutting programs.

Beyond avoiding deficits and the attendant service reductions, there is the question of how much the District should have on hand as a "rainy day" reserve before tax reductions are contemplated. The financial plan, on which these surpluses are based, includes no specific allocation for reserves. If the entire surplus and more is spent on tax reduction, the District will have no rainy day reserve.

The lack of any reserve funds is out of line with accepted, prudent fiscal practice. The National Conference of State Legislatures, the National Association of State Budget Officers, and Wall Street bond houses all cite five percent as the minimum reserve a jurisdiction should hold. In these good economic times, most states are holding reserves equivalent to five to 10 percent of a year's expenditures. The National Association of State Budget Officers reports that at the end of fiscal year 1998, some 20 states had reserves exceeding 10 percent of expenditures, and another 20 states had reserves of between five percent and 10 percent of expenditures. These reserves provide a cushion for emergencies and other unforeseen costs, and provide some resources that can be tapped when the economy begins to turn down and revenues flag. Given the District's recent financial history, it would be prudent to be seen as being within the mainstream of state fiscal practice with respect to reserves.

A "Supply-Side" Response?

Some would contend that expenditures — government programs and services — would not have to be cut to afford this tax cut because the tax cut would result in increased population and business activity which, in turn, would increase tax revenue. As in the early 1980s, when the tax cuts enacted under President Ronald Reagan spawned huge federal budget deficits and drove up federal interest costs, this is more likely to be wishful thinking than reality. Mainstream economic literature supports no such phenomenon.

The economic studies commissioned by the D.C. Tax Revision Commission concluded that "...a policy of cutting taxes to induce economic growth is not likely to be efficient or cost effective in the general case." (p. 46) Investigating whether the District's specific taxes and rates have an influence on population growth or business location, the economic analyses found no effect on population growth and limited effect of certain taxes on business activity. Of all the taxes the District levies, the report found some evidence that reducing only the sales tax or the personal property tax could increase employment growth. The evidence suggested that reducing other D.C. taxes would not result in increased employment or other economic activity. Finally, the economic analyses found that increasing local public expenditures could increase employment, although that conclusion was less definitive than the others (p. 76).

In short, the expert research on the District's taxes and economy specifically rejects the idea that revenues could increase appreciably as a result of reductions in the income tax, real property tax, or business taxes other than the personal property tax. (The Council proposal makes a small change to the personal property tax, exempting the first $50,000 of property.) Given this specific evidence, it is not responsible budgeting to assume that economic growth will cover the large cost of this proposed tax cut.

Who Would Benefit?

The Council proposal includes three main pieces: a reduction in individual income tax rates, a reduction in corporate and unincorporated business income tax rates, and a reduction in property taxes on commercial and residential rental property.

Although some individuals who rent apartments ultimately would benefit from the reduction in the property tax on residential rental property, the personal income tax cut is the piece that would directly benefit individual District residents the most.

The District's current individual income tax has three rates. The first $10,000 of taxable income is taxed at six percent, the next $10,000 of taxable income is taxed at eight percent, and all additional taxable income is taxed at 9.5 percent. The proposal would reduce the District's personal income tax by cutting each of the three marginal tax rates by three percentage points, phased in over three years. The top personal income tax rate of 9.5 percent would drop to 6.5 percent, the eight percent rate to five percent, and the six percent rate to three percent. No other changes are made to the income tax.

This type of proposal sounds fair, because all rates are cut equally. The actual effect, however, is to disproportionately benefit the District's higher-income taxpayers because the rate reduction is more valuable to them. A family of four with total income of $27,500 and taxable income of $20,000 would get a tax cut of $600. A similar family with total income of $240,000 and taxable income of $200,000 would get a $6,000 tax cut, an amount ten times as great.

The tax cut also would represent a somewhat greater percentage of income for higher-income District taxpayers than for less affluent ones. This is because the personal exemption and standard deduction — deductions of $1,370 per person plus $2,000 per family — eliminate a larger share of tax liability relative to income for lower-income families than for higher income taxpayers. In the example above, the tax cut would represent less than 2.2 percent of income for the lower-income family and 2.5 percent of income for the higher-income family.

An analysis of the personal income tax proposal by The Institute for Taxation and Economic Policy shows that 65 percent of the benefits would go to the highest income 20 percent of District households. Two dollars in every five the District would give up as a result of the individual income tax cuts — that is, 40 percent of these tax cuts — would go to the highest-income five percent of District households, those with incomes exceeding approximately $150,000.

If the proposed tax cut had been fully in effect for 1999, the average tax cut for families in the second 20 percent of the income distribution, those with incomes between $13,000 and $28,000, would be $343. By contrast, the highest-income one percent of District families — those with incomes exceeding $500,000 — would get an average tax cut of more than $23,000 each.

Some of the dollars the District would give up in individual income tax revenues would enrich the federal treasury rather than District residents. For taxpayers who claim itemized deductions on their federal tax returns, state and local income tax payments can be deducted from income. A taxpayer who pays less District income tax has a lower deduction and thus a higher federal tax bill. As a result of this interaction, one out of every six dollars the District loses in revenues goes to increase federal revenues. Out of the $330 million annual cost, $55 million would go to the federal government.

More Modest, Better Targeted Cut?

The D.C. Tax Revision Commission identified a number of areas in the tax system that could and should be reformed. For the D.C. individual income tax, the Commission recommended changing the structure to conform to the federal definition of taxable income. This would simplify the tax, would raise the income level at which the top tax rate begins to apply, and would remove an anomaly in the D.C. individual income tax in which one additional dollar of income for low-income families can result in several hundred additional dollars of tax liability.

This last point requires some further explanation. The District uses a low-income tax credit to exempt working poor taxpayers from the income tax. The credit is structured to offset 100 percent of the taxes owed by families with incomes at or below a certain level. For near-poor families with income slightly above the ceiling for the low-income credit, however, the District levies income taxes that are among the highest in the country. Families above the ceiling are not eligible for any portion of the low-income credit, and thus are liable for the full amount of D.C. income tax. For example, a two-parent family of four with income up to $17,900 had no D.C. tax liability in 1998. (The ceiling is set at the level that equals the total amount of the federal standard deduction and personal exemptions to which a family is entitled.) If the same family had income of $17,901, its tax liability would have been $634. The extra dollar of income would have triggered $634 in tax liability.

This situation creates a work disincentive for families just emerging from poverty. It also is incompatible with the goal of welfare reform, which is to help families earn sufficient amounts to support their families and escape from poverty.

In addition to the high tax burden that D.C. imposes on families just working their way out of poverty, this feature of the D.C. tax system causes unnecessary administrative complexity. With the jeopardy of just one dollar of additional income moving a family from no tax liability to several hundred dollars in tax liability, D.C. must withhold income tax from workers earning relatively low wages. So while D.C. does not require anyone who does not have to file a federal return to file a D.C. return, tens of thousands of poor D.C. workers do have to file returns to receive the refund to which they are entitled.

The Council plan would, of course, lower the tax liability of these families. But it would leave in place the "cliff" whereby one dollar of additional income triggers hundreds of dollars of tax liability, and it would leave in place tax burdens on the near-poor that are well above those of other states, including Maryland. If the District can afford a tax cut, it would seem that relieving tax burdens on these moderate income working families should take precedence over handing an average of $23,000 to each of the highest-income one percent of District residents.

Addendum to From Rags to Riches to Rags?

An April 30 report to Council members from Jack Evans, Chair of the Committee and Finance and Revenue, put forth an amended version of the tax plan and an example scenario for financing it.

The revised tax plan is more costly than the original version because additional tax cuts are added. For fiscal year 2002, the report indicates the cost would be $431 million rather than $419 million. In 2003, the annual cost is said to be $459 million.

The report presents the following scenario for covering the cost of the tax cut.

- Reducing Spending. The scenario calculates available funding using the Mayor's "alternative budget." Spending on appropriated programs and services in the alternative budget is $137 million below spending in the Financial Plan. Although the report does not explicitly say so, this means a portion of the tax cut would be financed by lowering expenditures.

- Refinancing Debt. A portion of the tax cut would be paid for by refinancing some of the District's long-term debt, stretching out the number of years over which the debt would be repaid. The Financial Plan contemplates "saving" $50 million a year over the next several years by refinancing debt. The scenario for financing the tax cut would raise the annual refinancing "savings" to $80 million. Refinancing has the effect of lowering debt-service costs in the short run but raising the total interest costs paid over the life of the debt.

- Using reserve funds. Over the four years, all of the $150 million a year reserve funds included in the "alternative budget" would be used to finance the tax cut.

- Leaving a gap. According to the scenario presented in the report, additional funding to support the tax cut would be required by fiscal year 2002. The report suggests this could come from increasing other revenues, further decreasing expenditures, or drawing down accumulated surpluses.

If the annual costs of the tax cut are greater than estimated by the Council — that is, if the cost of the personal income tax cut has been underestimated — problems in financing the tax cut could emerge sooner than the third year.

*Iris Lav is the deputy director of the Center on Budget and Policy Priorities. She also served as a member of the D.C. Tax Revision Commission. She has more than 25 years experience working on federal, state and local public finance issues throughout the country.