Many States Could Avoid an Unnecessary Revenue Loss During the Current Fiscal

Crisis by Disallowing Business Operating Loss Carrybacks

by Michael Mazerov

Summary

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

As governors and legislators in a large number of states continue to struggle with the most serious fiscal crisis they have experienced in decades, many are looking for ways to raise additional revenue. Tax breaks provided to businesses are being subjected to particular scrutiny in a number of states. There is growing recognition among policymakers that eliminating tax breaks that are no longer achieving their aims or that fail a cost/benefit test is an alternative to increasing tax rates across the board.

One business tax break that warrants reevaluation is the so-called net operating loss (NOL) “carryback” provision granted by slightly less than half the states with personal and/or corporate income taxes. This provision allows businesses to file amended income tax returns for past years in which they were profitable, use current year business losses to offset those profits, and receive refunds of excess taxes paid in past years. During recessions, when tax payments by businesses tend to fall in any case, refunding business taxes paid in past years compounds states’ fiscal problems.

Twenty states (see the text box at right) could

avoid some loss of corporate and/or personal income tax revenue during the

current fiscal crisis — and future recessions — if they disallowed NOL

carrybacks.[1]

(Personal income tax revenues would be affected because businesses

organized as sole proprietorships and partnerships are also permitted to

carry back NOLs.)

|

Which States Allow NOL

|

The underlying objective of permitting an NOL

carryback deduction is, arguably, a valid one. The provision allows a

business to calculate taxable profit by averaging its income — including

negative income — over several years.

This income-averaging policy can be substantially achieved, however, by permitting “loss carryforwards” — allowing businesses to deduct any losses they suffer against future profits. The tax savings provided by carrybacks and carryforwards is essentially the same, with the principal difference being a matter of timing. Given that the objective of loss carrybacks can largely be achieved by allowing losses to be carried forward, it is ill-advised for states to compound their fiscal difficulties by issuing refunds for previously-paid taxes at a time when their current-year personal and corporate income tax collections are being affected adversely by an economic slowdown or recession. Loss carrybacks conflict with state balanced budget requirements, which force states to balance current year budgets even though the economy is weak, revenues are flagging, and service needs are rising.

A majority of states already apparently

recognize the advantages of limiting income averaging by businesses to

prospective deductions; 26 states and the

If states act quickly, it might even be possible to disallow the carryback of 2002 losses, particularly losses incurred by corporations. Such action would still be timely; the vast majority of corporations did not file their income tax returns prior to April 15th but rather will do so toward the end of this summer or even later. Disallowing the carryback of 2002 operating losses would significantly reduce the amount of refunds states will have to issue during their 2004 fiscal years as a result of the NOL carryback provision. Quick action is important because corporate profits were especially high in 2000 and most states that permit carrybacks allow a two-year carryback period.

How Loss Carrybacks Work

In most cases, states allow NOL carrybacks because they piggyback their basic personal and corporate income tax structures on the federal Internal Revenue Code (IRC). At present, the IRC generally allows a business experiencing an operating loss in the most recent tax year to file amended tax returns for the two prior years and deduct that loss against any profits earned in those two years.[2] Any unused losses that remain after being carried back can be deducted against profits earned in any of the next 20 years.

Take, for example, a corporation that earned $1,000 in profit in both 2000 and 2001 and then experienced a loss of $3,000 in 2002. The federal loss carryback provision allows this corporation to file amended returns for 2000 and 2001 and use $2,000 of the 2003 loss to offset the $1,000 profit earned in each of those two years. In this circumstance, the corporation would receive a refund of all taxes paid in 2000 and 2001, since the NOL carryback deduction would bring taxable profit in both years down to zero. The unused $1,000 of 2002 loss not carried back to 2000 or 2001 could be deducted against any profits earned in tax years 2003 through 2022.

Most states that allow loss carrybacks allow them for the same two-year period provided for in the IRC. While all states with personal and/or corporate income taxes allow losses to be carried forward, a number of them limit carryforwards to shorter periods than the 20 year period allowed for federal tax purposes (for example, limiting the carryforward period to five or ten years). A few states cap the dollar amount of losses that can be carried forward or back to any one tax year.

The Rationale for Allowing Losses to Be Carried Forward and Back

The basic rationale for allowing losses to be carried forward and back flows from a recognition that businesses generally are established with the goal of making a profit over the life of the business rather than in any particular year. Many new businesses that ultimately prove to be successful and profitable lose money for a number of years before they cross over into profitability. The same long-term profitability goal applies to activities a business initiates subsequent to its initial formation. If the company is entering a new line of business or expanding into a new geographic area, it might experience substantial personnel and other costs before the new line of business or branch even begins operating, and still more costs before it becomes profitable. In some circumstances, these additional costs might cause the entire company to experience one or more years of loss. Finally, of course, profitable businesses may experience unprofitable years periodically due to downturns in the overall economy or factors that affect their particular industry (for example, a temporary spike in energy costs).

The aim of allowing losses to be deducted against past and future profits is to measure profitability for tax purposes over a time horizon that more closely corresponds to a business’ investment horizon than would a strictly annual accounting of profits. Without this form of income averaging, a business that was never truly profitable in an economic sense could be subject to tax on its “profit” merely because of the timing of its receipts and expenses. Without income averaging, for example, a business that experienced losses for 5 years of $1,000 per year followed by profits of $1,000 per year for 5 years would pay income taxes in the latter period. In contrast, a business that exactly broke even in each of those 10 years (experiencing neither losses nor profits) would have no income tax liability in any of those years. Of course, neither business actually earned a profit over the 10-year period taken as a whole. Thus, it arguably would be inequitable for the first business alone to have positive income tax liability merely because of the timing of its losses and profits. (That is not to say, however, that only profitable businesses should pay state taxes; see the text box.)

Even If Averaging Business Income over Time

Can Be Justified,

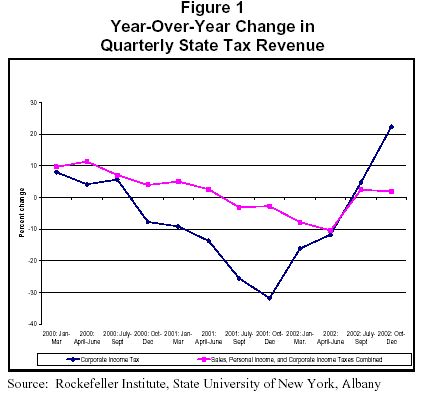

Business profits are highly volatile over the course of the business cycle. Profits are often a fairly narrow “wedge” between a business’ receipts and its expenses. Because many of those expenses cannot be cut back quickly or easily when a business notices its sales slowing, a relatively small decline in a business’ sales due to an economic downturn or slowdown often leads to a much larger proportionate drop in profits. For example, between the second quarter of 2000 (when pre-tax corporate profits hit a pre-recession peak) to the fourth quarter of 2001 (when corporate profits hit bottom) corporate profits fell by 25 percent. Over that same period, nominal Gross Domestic Product actually posted a small, 3.4 percent gain.

If business profits decline sharply during economic downturns, state taxes on business profits are likely to decline sharply as well. That has been the states’ experience during the recent recession. Figure 1 compares the quarterly changes in state corporate income tax receipts since the beginning of 2000 with the changes in state sales tax, personal income tax, and corporate income tax receipts combined. It shows that at the depths of the recession, quarterly corporate income tax revenues fell 32 percent from their year-earlier amounts, whereas all three major taxes combined fell only 10 percent at their deepest trough.

|

Unprofitable

Corporations Benefit from State Services The basic rationale for imposing income taxes on businesses is the “benefits received principle” — the notion that some taxes can be viewed as payment for services rendered by government to the taxpayer. The owners of businesses benefit from state programs and activities that make possible or facilitate the operation of the business. These services include public education (which provides the business with a productive workforce), the maintenance of a legal and regulatory system that enforces business contracts and discourages commercial fraud, and the provision of public transportation networks that enable businesses to obtain inputs and get their products to market. The benefits received principle holds that business owners can be expected to pay state taxes to compensate the state for services like these that are provided to the business. While in theory these taxes could be imposed on business owners directly (and in some instances are), the practical difficulties of taxing out-of-state owners of corporations has led most states to impose taxes on the corporations directly rather than seek to tax non-resident stockholders. Taxing profits is only one possible approach to taxing businesses for the state services they — or their owners — receive. Because businesses benefit from state services like education and roads whether they are profitable or not, it is entirely reasonable for states to impose some type of general business tax that does not depend upon business profitability. Some 13 states, for example, impose a corporate minimum tax that is a fixed number of dollars — ranging from $10 in Oregon to $2000 in New Jersey. At least seven states go further, and require businesses to pay the higher of a tax calculated as a percentage of profit (which of course is zero when the business has no profit) and a tax calculated on some other basis. (In Texas that alternative base is the business’ net worth, in New Hampshire it is “value-added” within the business, and in New Jersey it is the business’ gross receipts.) Still other states impose both a corporate profits tax and a non-profits-based tax. All three of these categories of taxes serve as a form of “alternative minimum tax” that ensures that all businesses pay something to support the public services from which they benefit, even if they are not profitable in a particular year. Allowing businesses to average taxable profits and losses over a number of years arguably is reasonable income tax policy. Such a policy ensures that businesses that are not truly profitable over an extended period of time are not liable for income taxes merely because they have a profitable year or two. Accepting such a policy does not mean, however, that unprofitable businesses should have no state tax obligations. Again, the “benefits received principle” applies to profitable and unprofitable businesses alike. |

Plummeting corporate tax revenues have worsened state fiscal problems during the current downturn and most previous recessions. Such revenue declines occur at a time when the need for state services and programs financed by business taxes not only does not recede, but, in fact, often increases. For example, workers who lose jobs and the income and benefits that come with them often need state-financed medical care, income supplements, housing assistance, and job training. These services are financed in most states by the General Fund, into which state personal and corporate income tax receipts usually flow.

Given the need to maintain or increase spending during economic recessions, it is surprising that some 20 states compound the fiscal problems that arise at such times from declining business tax receipts by permitting businesses to file for refunds of previously-paid taxes. There is little justification for such a self-inflicted fiscal wound; states can provide substantially the same tax savings to businesses by allowing them to carry their net operating losses forward and deduct them against future profits. While it is true that business cash flow would be improved by obtaining refunds of state income taxes paid in the past, a business that needed the cash for investment purposes likely would be able to borrow it on the capital market. Interest rates tend to be favorable during recessions, precisely the time when most net operating loss carrybacks would be claimed. Because of their balanced budget requirements, however, states generally would be unable to borrow money to offset the revenue they lose by allowing businesses to claim loss carrybacks. Thus, faced with a choice between improving business cash flow and avoiding further impairment of their ability to maintain services during recessions, a majority of states have appropriately chosen to limit businesses to claiming NOL carryforwards.

For the federal tax system, on the other hand, a deduction for loss carrybacks arguably is appropriate. Unlike the states, the federal government is not required to balance its budget annually. Most economists would argue that it is desirable for the federal government to allow deficits to increase during recessions in order to stimulate the economy. Enabling firms to receive income tax refunds by carrying back their losses to previous years in which they were profitable improves business cash flow and may enable businesses to cut prices or finance new plant and equipment — both of which would tend to stimulate economic growth. Moreover, the vast majority of both the economic stimulus and the tax savings to businesses flowing from loss carryback deductions would be associated with federal personal or corporate tax payments. The federal corporate tax rate is 34 percent, and the top federal personal income tax rate is 38.6 percent. In contrast, state corporate tax rates are generally in the 8-10 percent range, as are top state personal income tax rates. State policymakers contemplating repealing a carryback should not hesitate to give their own cash flow needs priority; as long as the federal government continues to allow loss carrybacks, businesses in their states incurring losses will receive considerable tax benefits during difficult economic times.

Repealing the NOL Carryback Deduction: Timing

If states amended their tax laws to

disallow carrybacks of net operating losses experienced by businesses in the

2003 tax year now underway, it would prevent businesses in most states from

obtaining refunds of some or all of their tax year 2001 and 2002 tax

payments.[3]

Most of these refunds would not actually be issued until some time in the

states’ 2005 fiscal years, however. States generally follow federal rules

that would require the 2003 tax return to be filed before the prior-year

refunds could be claimed. Most corporations would not be expected to file

their 2003 tax returns until after

Nonetheless, a large number of states are still struggling to close large gaps in their FY04 budgets. Accordingly, states may also wish to consider acting quickly to disallow the ability of corporations to carry back their 2002 losses to obtain refunds of taxes paid in tax years 2000 and 2001. Relatively few large corporations have filed their 2002 tax returns. Most will not do so until September or October. Although it would require states to devote some resources to preparing educational materials and distributing them to corporate tax managers making clear that 2002 losses could not be carried back, this should not be very difficult; state revenue departments have well-developed channels for informing tax practitioners about changes in tax laws, regulations, and policies.[5]

|

Repealing the NOL Carryback Deduction: Mechanics How a state would need to amend its tax law in order to disallow NOL carrybacks depends upon how that law links to the Internal Revenue Code. In some states allowing NOL carrybacks, state law defines state taxable income as federal taxable income before the deduction of net operating losses (often line 28 on the federal corporate income tax return), and then explicitly authorizes a further deduction for net operating loss carryforwards and carrybacks. In such a state, it is generally only necessary to strike the language referring to loss carrybacks. In North Dakota (which recently repealed NOL carrybacks), it was only necessary to strike eight words that referred to carrybacks.* Pending legislation to disallow NOL carrybacks in Illinois (H.B. 272/S.B. 79) achieves a similar result by adding five words clarifying that the provision for NOL carrybacks is not available for tax years that terminate on or after December 31, 2003. In states that define state taxable income as federal taxable income after NOL deductions (line 30 of the federal corporate tax return), it generally would be necessary to add somewhat lengthier language providing for the adding back of NOL carrybacks deducted on the federal return. Arizona’s statute, for example, provides for an add-back of all net operating loss deductions (Section 43-1121), and then allows a subtraction of just loss carryforwards (Section 43-1123). Losses that have already been carried back for federal tax purposes will never appear on the federal return as carryforwards. Some states’ laws may provide that the amount of losses to be carried forward for state purposes is the amount deducted on the federal return. In such states, it may be necessary to add language clarifying that losses disallowed as carrybacks on the state return can still be carried forward notwithstanding the fact that they have not been deducted as carryforwards on the federal return. *H.B. 1471, Section 3, signed by the Governor on April 6, 2003. The law struck two additional words and added seven to clarify the effective date of the disallowance. |

Delaying the ability of a corporation to obtain an anticipated tax refund only a few months before the refund was to be paid may appear to be a rather extreme, disruptive measure. Many families and individuals, however, have already experienced or face even more serious disruptions of their financial circumstances as a result of the state fiscal crisis. For example, 1.7 million people are at risk of losing state-financed medical coverage next year.[6] State university students in 19 states had their 2002-03 academic year tuition increased by more than 10 percent, and six states actually increased second semester tuition after the 2002-2003 academic year had already begun.[7] Disallowing the carrying-back of 2002 NOLs could enable states to avoid subjecting some additional number of families and persons to financial and perhaps physical harm. Given that corporations would still be able to reap the tax saving from 2002 losses in future years, policymakers could reasonably choose to act quickly and disallow carrybacks of 2002 corporation losses. States disallowing carrybacks could extend the carryforward period to allow businesses a longer period of time in which to utilize their losses.

End Notes:

[1] John C. Healy and Michael S. Schadewald, 2003 Multistate Corporate Tax Guide, Aspen Publishers.

[2] NOL carrybacks can also be claimed for federal tax purposes on forms specially designed for that purpose; it generally is not necessary to file a full-blown amended return. The federal Job Creation and Worker Assistance Act of 2002 extended the carryback period from two years to five years for net operating losses that occurred in taxable years ending in 2001 and 2002. The large majority of states that allow carrybacks decoupled from that provision, however, retaining the permanent two-year carryback period.

[3]

[4] Some of the avoided revenue losses likely would be FY04 revenue losses. Small business owners eligible for refunds from NOL carrybacks would find it in their interest to file their 2003 tax returns as early as possible, and many likely would do so before June 30, 2004, when most states’ 2004 fiscal years end.

[5] Such a policy change should not require any change to the 2002 tax instructions or forms, since the carryback would require filing amended returns for 2000 and 2001.

[6]

Melanie Nathanson and Leighton Ku,

Proposed State Medicaid Cuts Would

Jeopardize Health Insurance Coverage for 1.7 million People: An Update,

Center on Budget and Policy Priorities,

[7]