|

April 3, 2008

ALMOST ALL LARGE IOWA MANUFACTURERS ARE ALREADY SUBJECT

TO "COMBINED REPORTING" IN OTHER STATES:

Fears of Job Flight from Reducing Corporate Tax Avoidance Are Unwarranted

by Michael Mazerov and Katherine Lira

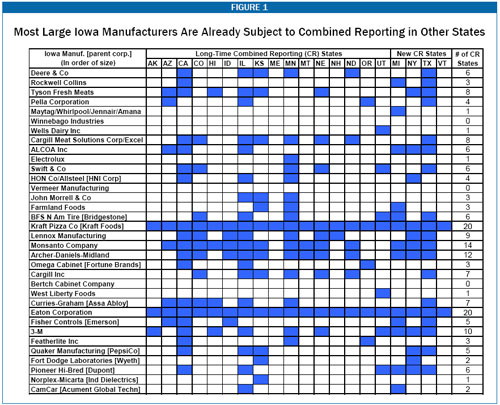

For the second year in a row, Governor Chet Culver has recommended that the Iowa legislature enact an important reform in the state corporate income tax known as “combined reporting.” Some Iowa corporations have opposed this change, claiming that it would result in some companies leaving the state or shunning Iowa for new investment. However, several of the companies that have been cited in the media as among the most outspoken opponents of this policy actually maintain facilities in numerous combined reporting (CR) states. John Deere and Alcoa have facilities in 6, Tyson has facilities in 8, Monsanto has facilities in 14, and Kraft has facilities in all 20 of the existing CR states.Most large corporations consist of a parent corporation and its subsidiaries. Combined reporting effectively treats the parent and most or all of its subsidiaries as a single corporation for state income tax purposes. In doing so, combined reporting nullifies a wide array of tax-avoidance strategies large multistate corporations have devised to artificially move profits out of the states in which they are earned and onto the books of subsidiaries located in states that will tax the income at a lower rate — or not at all.[1]

Some 16 states have used combined reporting for at least two decades and four more have put it into effect in the last four years.[2] Nonetheless, many members of the Iowa legislature appear reluctant to support the governor’s recommendation. Representatives of some major multistate corporations doing business in Iowa have expressed opposition to combined reporting, claiming that it will increase their tax liability in the state and/or subject them to difficult and costly tax compliance burdens. Some legislators therefore are concerned that adopting combined reporting will lead to job losses as major employers leave Iowa or reject the state for future investments. For example, State Senator Mark Zieman has written, “Combined reporting for corporations will affect companies, such as CamCar, Norplex, John Deere, Alliant, and many others; this will encourage companies to locate in other states.”

This study presents compelling evidence that such concerns are unwarranted. It summarizes the results of a careful examination of the states in which the 32 largest Iowa manufacturers (and two smaller ones cited by Senator Zieman) have physical facilities and therefore are subject to the state’s corporate income tax. Manufacturers were chosen as the focus of the research because, in theory, they have a greater ability than do retailers and service businesses to locate in states far away from their customers to take advantage of what they view as more favorable state tax policies. As documented in Figure 1, the study finds that:

- 31 of the 34 Iowa manufacturers examined maintain facilities in at least one combined reporting state or are a subsidiary of a corporation that has a facility in at least one combined reporting state. The “compliance burdens” and tax liabilities arising from combined reporting cannot be that great if these manufacturers — or the parent corporation that controls their decision-making — have willingly maintained a facility in one or more combined reporting states.

-

Most of the corporations examined maintain facilities in multiple combined reporting states. 24 of the 34 companies have facilities in three or more combined reporting states, 17 have facilities in five or more such states, and 5 companies have facilities in 10 or more CR states.

-

Several of the companies have long-maintained their headquarters in combined reporting states, including John Deere, Kraft, Cargill, Archer-Daniels-Midland, 3-M, and Quaker.

Taken together, these facts provide compelling evidence that Iowa’s adoption of combined reporting would not lead these companies to remove facilities or shun Iowa as a location for future investments. The data presented in Figure 1 also suggest the following observations:

-

As noted above, several of the companies that have been cited in the media as among the most outspoken opponents of combined reporting maintain facilities in numerous CR states. John Deere has facilities in 6, Tyson has facilities in 8, Monsanto has facilities in 14, and Kraft has facilities in all 20 CR states.

-

Four companies have what appears to be a single facility in a single, long-time combined reporting state; none of those facilities appears to be the corporate headquarters.[4] If combined reporting were truly sufficiently onerous to induce a company to abandon a state, it would seem that these facilities would have been prime candidates for such action. The fact that they are maintained is further evidence that a state’s adoption of combined reporting is unlikely to affect corporate location decisions.

-

There are four states that have implemented combined reporting only since 2004, and in two of them it did not go into effect until 2008. It might therefore be argued that the presence of facilities in those states cannot be cited as evidence that combined reporting does not affect corporate location because companies have not had enough time to react to the change by moving their plants. In fact, as shown in Figure 1 (where these four states are isolated in the right-most columns), 30 of the 31 companies with a facility in at least one CR state have a facility in one of the CR states that enacted this policy prior to 1985.

It would take considerable effort to determine when the facilities identified in this report were sited in combined reporting states, and such an investigation is beyond the scope of the study. However, given that 16 states have mandated the use of combined reporting for 20 years or longer, it seems reasonable to assume that many of these manufacturers sited their facilities in CR states after the state adopted combined reporting. It also seems reasonable to assume that many of these same plants have been expanded and/or modernized since the initial siting decision was made. In other words, not only have 31 of the 34 companies chosen not to abandon CR states, it seems likely that many or most of them have chosen to locate or expand in CR states fully cognizant of the fact that the state had implemented this policy. If this is true, it provides further evidence that Iowa would not be harming its economic prospects by enacting this important corporate income tax reform. Combined Reporting and State Economic Development: Additional Evidence There is no denying the fact that some large multistate corporations oppose combined reporting. Combined reporting is likely to result in increased corporate income tax payments for corporations that have put aggressive tax shelters in place. Its enactment also sharply limits the ability of large corporations to avoid a state’s income tax going forward.

|

Table 1:

Manufacturing Job Change,

1990-2007

7 of 8 States with Net Job Gains Had Combined Reporting (CR) in Effect |

|

North Dakota (CR) |

66.7% |

|

Idaho (CR) |

26.0 |

|

Utah (CR) |

23.3 |

|

Iowa |

4.8 |

|

Montana (CR) |

4.6 |

|

Kansas (CR) |

4.5 |

|

Nebraska (CR) |

4.1 |

|

Arizona (CR) |

2.9 |

|

Oregon (CR) |

0.0 |

|

Minnesota (CR) |

-0.1 |

|

Texas |

-1.4 |

|

New Mexico |

-2.4 |

|

Oklahoma |

-3.5 |

|

Wisconsin |

-4.3 |

|

Kentucky |

-6.2 |

|

Alaska (CR) |

-7.1 |

|

Indiana |

-9.2 |

|

Louisiana |

-10.5 |

|

Arkansas |

-13.7 |

|

Colorado (CR) |

-14.0 |

|

Vermont |

-15.7 |

|

Georgia |

-17.6 |

|

Alabama (Median State) |

-18.4 |

|

New Hampshire (CR) |

-20.9 |

|

Florida |

-21.8 |

|

Tennessee |

-23.4 |

|

Missouri |

-23.6 |

|

California (CR) |

-25.5 |

|

Mississippi |

-26.1 |

|

Illinois (CR) |

-26.1 |

|

Hawaii (CR) |

-26.2 |

|

Ohio |

-27.1 |

|

Delaware |

-27.1 |

|

Virginia |

-28.0 |

|

West Virginia |

-28.0 |

|

South Carolina |

-28.1 |

|

Pennsylvania |

-30.7 |

|

Maryland |

-33.5 |

|

North Carolina |

-34.6 |

|

Connecticut |

-36.4 |

|

Maine (CR) |

-36.5 |

|

Massachusetts |

-38.5 |

|

New Jersey |

-40.9 |

|

New York |

-43.7 |

|

Rhode Island |

-46.6 |

The question, however, is whether the dislike that some multistate corporations harbor toward combined reporting will actually result in harm to the economy of a state that adopts it. Would its adoption by Iowa cause existing corporations to leave the state or reject it as a location for future investments? Would corporations not presently doing business in Iowa be dissuaded from doing so by combined reporting? The data on the facility location decisions of major Iowa manufacturers discussed above provide significant evidence that the answer to both questions is “no.” This conclusion is supported by the job-creation track record of the combined reporting states and by academic studies as well. Combined reporting states are well-represented among the most economically-successful states in the country. Since 1990, for example, only eight states that levy corporate income taxes have managed to achieve net positive growth in manufacturing employment. Seven of those eight states — Arizona, Idaho, Kansas, Montana, Nebraska, North Dakota, and Utah — had combined reporting in effect throughout the 1990-2007 period. (Iowa was the eighth state with positive manufacturing job growth; see Table 1.)[5] California is the state that has used combined reporting the longest and enforces it most aggressively, yet it was able to give birth to Silicon Valley in the 1990s. The presence of combined reporting has not been a barrier to Intel Corporation’s maintenance of its headquarters in California and its decision to place the bulk of its expensive chip fabrication plants in Oregon, Arizona, and Colorado — all combined reporting states.

In citing these data and anecdotes, no claim is being made that combined reporting contributes to these states’ economic successes. They do suggest, however, that the burden of proof ought to lie with combined reporting opponents to demonstrate that the policy has an actual negative impact on state economic growth and not just business “perceptions.” That burden of proof has not been met to date — in Iowa or in any other state in which the adoption of combined reporting has been contemplated. It may seem illogical to acknowledge that some multistate corporations oppose combined reporting yet argue that it has no measurable impact on where they choose to locate. The apparent contradiction can be easily reconciled, however. All state and local taxes paid by corporations represent less than two and one-half percent of their total expenses on average, and the state corporate income tax represents on average less than 10 percent of that amount — or less than one-quarter of one percent of total costs.[6] A state’s decision to adopt combined reporting increases that small corporate tax load only slightly.[7] The potential influence on corporate location decisions of state corporate tax policies is simply overwhelmed in most cases by interstate differences in labor, energy, and transportation costs, which comprise a much greater share of corporate costs than state corporate income taxes do and often vary more among the states than effective rates of corporate taxation. It comes as no surprise, then, that a recent study by economists Robert Tannenwald and George Plesko, which measured interstate differences in overall state and local tax costs for corporations in a particularly rigorous way, found that there was not a statistically-significant (inverse) correlation between those costs and state success in attracting business investment.[8] In other words, higher state and local business taxes did not impede business investment. Helping Small Businesses

Opponents of combined reporting also ignore potential benefits of this policy. Small (often family-owned) corporations doing most or all of their business in the state in which they are located generally do not have the resources to set up “Delaware Holding Companies,” “captive REITs,” and other tax shelters that exploit the absence of combined reporting in the state.[9] But their large, multistate corporate competitors do. By nullifying the corporate tax savings from aggressive tax-avoidance, combined reporting could benefit Iowa’s economy by preventing large out-of-state corporations from under-pricing the state’s small businesses or attracting investment capital at a lower cost — thereby letting economic efficiency and not tax planning determine which businesses succeed in the marketplace. Perhaps this phenomenon explains in part why a recent study financed by the federal Small Business Administration found that: "States with more aggressive corporate income taxes, specifically including combined reporting . . . tend to have higher entrepreneurship rates.”[10]

Maintaining Services Businesses Need

Finally, the enactment of combined reporting could benefit Iowa’s economy by preserving the long-term viability of the corporate income tax. This revenue source makes an important contribution to the ability of the state to finance education, transportation infrastructure, public safety, health care, and other vital services. Businesses need these services to provide a productive, well-trained workforce, to protect their facilities, and to ensure that they can obtain their supplies and transport their products to their customers expeditiously. Numerous economic studies confirm that the quality of these services in particular locations has a significant impact on where businesses choose to invest.[11] Failing to enact combined reporting could harm the state’s economy by allowing the erosion of the state’s corporate tax base to continue, squeezing the ability of the state to furnish services that the private sector needs.

Conclusion

Combined reporting is a key tax policy choice needed to ensure that multistate corporations pay their fair share of the Iowa corporate income tax, just as small Iowa businesses must do. Having failed to enact combined reporting or any other meaningful measures to attack aggressive corporate tax avoidance techniques, Iowa’s corporate income tax remains vulnerable to serious, ongoing erosion.

This report has presented compelling, Iowa-specific evidence refuting the key objection to combined reporting, that its enactment will harm the state’s economic prospects. However much they may object to combined reporting rhetorically, the vast majority of the state’s major manufacturers have willingly submitted and adapted to combined reporting-based income taxes in other states, usually in numerous other states. Iowa policymakers can confidently join those in a growing number of states that are enacting this critical corporate income tax reform without worry about negative impacts on the state economy.

Appendix: Data Sources

The manufacturing corporations whose facility locations were investigated for this report were included in a list of the 129 largest Iowa employers (measured by the number of employees) published by the Iowa State Department of Employment Services.[12] All of the manufacturers in that list were included in the study. As noted above, only manufacturers were studied because they are generally considered to be the type of enterprise that is potentially the most mobile in reaction to what are perceived as unfavorable state tax policies and practices. In contrast, a company like Wal-mart (Iowa’s largest for-profit employer) obviously could not continue to serve its Iowa customers at its current scale if it removed its retail stores from the state. It would therefore bias the conclusions of this study to cite Wal-mart and similar businesses with retail facilities in their customers’ states as evidence that combined reporting does not have a significant impact on where corporations choose to locate.

The two principal sources of information used to identify the states in which the manufacturers have facilities were the annual “10-K” reports filed by publicly-traded corporations with the Securities and Exchange Commission and the company’s own Web sites. Every Form 10-K has a section titled “Properties” in which the corporation describes its major facilities. Although this section sometimes contains a generic description, in the majority of cases specific states are named.

Form 10-K information was supplemented by an examination of company Web sites. Many companies have a section of their Web sites listing their locations, often in connection with a description of their “good corporate citizen” activities. For those companies that did not have such a page, it was sometimes possible to use the Web pages aimed at assisting prospective employees find job openings. Companies often list all of their locations on the job vacancy sections of their Web sites; where they did not, states were included in Figure 1 only if there was a job listing for that state.

The data presented in this report on the number of states in which Iowa manufacturers and their parent companies maintain facilities should be viewed as the minimum number of combined reporting states in which they are taxable. States were counted only if it was possible to gather written evidence authored by the company itself that it had a facility in a specific combined reporting state. It is quite possible that the information obtained was incomplete. For example, the annual report of PepsiCo, parent corporation of Iowa manufacturer Quaker, indicates that Quaker and its sister subsidiaries Frito Lay and Pepsico Beverages North America own or lease almost 2000 facilities. However, hard data could only be obtained to document PepsiCo or Quaker plants in five combined reporting states. Thus, Quaker is listed in Figure 1 as having facilities in only five CR states despite the likelihood that PepsiCo, a huge multinational food manufacturing conglomerate, has facilities in many more. In addition, as noted above, for some companies the only source of information was a listing of locations at which there were current job vacancies. It is possible that those companies had facilities in other combined reporting states that did not have current vacancies and accordingly were not identified in Figure 1.

End Notes:

[1] See: Michael Mazerov, “State Corporate Tax Shelters and the Need for ‘Combined Reporting’,” Center on Budget and Policy Priorities, October 26, 2007, www.cbpp.org/10-26-07sfp.pdf.

[2] A fifth state, West Virginia, has enacted combined reporting and will implement it in 2009.

[3] Ed Tibbetts, “Businesses Lining Up Against Tax Code Plan,” Quad City Times, February 13, 2008.

[4] The companies are Wells Dairy, Electrolux, West Liberty Foods, and Norplex-Micarta. Maytag also has a facility in Michigan, but Michigan switched to combined reporting only at the beginning of 2008.

[5] Table 1 also indicates that the ninth and tenth best-performing states in manufacturing job growth were both combined reporting states. Oregon had a small net gain of manufacturing jobs in the 1990-2007 period that rounded down to zero. Minnesota had a small net loss of manufacturing jobs. Table 1 also shows that there were 11 combined reporting states that had better manufacturing job performance than the median state, Alabama, and only 5 combined reporting states that had steeper manufacturing job declines than Alabama.

[6] According to 2005 data published by the Internal Revenue Service (the most recent available), corporations deducted $473 billion in federal, state, and local taxes on their 2005 federal tax returns. This amount represented 2.0 percent of total expense deductions of $23.6 trillion. (The data are available at www.irs.gov/pub/irs-soi/05sb1ai.xls.) Since corporations have a strong financial incentive to deduct from their otherwise taxable profit every state and local tax payment for which they are liable, IRS statistics arguably are the most accurate source of information concerning state and local taxes incurred by corporations.

The Council on State Taxation (COST), an organization representing major multistate corporations on state tax matters, has taken issue with using IRS data to evaluate the relative importance of state and local tax costs in influencing corporate location decisions. (See: Joseph R. Crosby, “Just How ‘Big’ Are State and Local Business Taxes?” State Tax Notes, June 20, 2005, pp. 933-935.) Crosby correctly notes that the line-item for taxes deducted on federal returns omits a major category of state and local taxes paid by businesses — sales taxes paid on equipment and supply purchases. (Such taxes are hidden in other expense line-items in the IRS data.) However, as noted above, the line-item also includes a number of federal taxes paid by corporations that are deductible on federal returns — such as the federal telecommunications excise tax and unemployment compensation taxes for some corporate employees. If one were to add a reasonable estimate of the omitted state and local sales taxes and subtract a reasonable estimate of the inappropriately-included federal taxes, the resulting estimate for total state and local taxes incurred by corporations might not differ significantly from the $473 billion IRS figure for total deducted taxes.

In fact, COST has commissioned its own estimate of the total amount of state and local taxes paid by businesses. The figure for state fiscal year 2006 is $553.7 billion. (See: Robert Cline, Tom Neubig, and Andrew Phillips (Ernst & Young LLP), “Total State and Local Business Taxes, 50-State Estimates for Fiscal Year 2006,” February 2007; available at www.statetax.org/WorkArea/DownloadAsset.aspx?id=67460.) This figure represents the estimated taxes paid by all businesses, not just corporations. But even if one assumed that all of these costs were incurred by corporations and substituted this figure for the IRS data for taxes deducted, it still results in an estimate that state and local taxes represent 2.3 percent of total corporate expenses (of $23.6 trillion) — not significantly different from the 2.0 percent figure arrived at using only the IRS data.

More importantly, COST also takes issue with the use of the $23.6 trillion IRS figure for total corporate expenses used in the denominator. COST argues that the relevant analysis is an examination of the share of total final economic output produced by private businesses that is absorbed by state and local taxes paid by such businesses. COST asserts that using the $23.6 trillion of corporate expenses is inappropriate because that figure includes multiple sales of the same item from (for example) a manufacturer to a wholesaler and then from the wholesaler to a retailer. In contrast, using total U.S. gross state product produced in the private sector (otherwise known as private sector “value-added”) measures the value only of final production.

COST’s preferred denominator of gross state product produced by private businesses might be appropriate for evaluating the total “burden” of state and local business taxes on final production in the economy. It is inferior, however, in evaluating the issue under discussion here — the role played by state and local corporate tax costs in influencing corporate location decisions as compared to the role played by other corporate expenses for labor, energy, and transportation. For each actor in the supply chain described above (manufacturer, wholesaler, retailer), the influence of state and local tax expenses on its location decisions is determined in relation to the other expenses incurred in its business that also vary among locations. How many times its inputs may have been resold prior to its purchase of them and how many times its outputs may be resold prior to reaching their final purchasers is irrelevant in influencing its location decisions. What is true for the individual economic actors is true for the supply chain as a whole. Thus, the relative importance of state and local taxes in influencing corporate location decisions in the overall economy is best illustrated by looking at those expenses as a share of total corporate expenses, not the total value of final corporate production or value-added.

In sum, it is entirely reasonable to argue that state and local taxes have a relatively minor impact on corporate location decisions because they constitute only 2.3 percent or less of total corporate expenses and their potential influence is overwhelmed by interstate differences in labor, energy, transportation, and other costs of production that account for almost 98 percent of total corporate production expenses.

[7] The adoption of combined reporting is estimated by Governor Culver to boost corporate tax receipts by $75 million in FY09. That would represent an 18 percent increase over the currently-forecasted FY09 corporate income tax baseline of $416.5 million.

[8] George A. Plesko and Robert Tannenwald, “Measuring the Incentive Effects of State Tax Policies Toward Capital Investment,” Federal Reserve Bank of Boston Working Paper 01-4, December 3, 2001.

[9] For a detailed description of some of the tax-avoidance strategies to which non-combined reporting states are most vulnerable, see the source cited in Note 1.

[10] Donald Bruce and John Deskins, “State Tax Policy and Entrepreneurial Activity,” November 2006. Available at www.sba.gov/advo/research/rs284tot.pdf.

[11] For a recent summary of these studies in the context of Massachusetts’ debate on combined reporting, see: Robert G. Lynch, William Schweke, Nicholas W. Jenny, and Noah Berger, “Building a Strong Economy: The Evidence on Combined Reporting, Public Investments, and Economic Growth,” 2007. Published by the Economic Policy Institute and the Massachusetts Budget and Policy Center, June 2007. Available at www.massbudget.org/BuildingStrongEconomyJune07.pdf.

[12] The data are available as a downloadable Excel file at www.iowaworkforce.org/lmi/empstat/coveredemp.html.

|