Improving Transitional Medicaid to

Promote Work

and Strengthen Health Insurance Coverage

by Leighton Ku and Edwin Park

| PDF of this report Related Reports |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Transitional medical assistance (TMA) is an important element of both welfare and health insurance policy that strengthens incentives for welfare recipients to go to work and remain employed without losing health insurance coverage. Under TMA, most of those who leave welfare for work - and whose earnings would otherwise make them ineligible for Medicaid - may continue to get transitional coverage for up to a year longer.

The legislative authorization for TMA expires at the end of this fiscal year. As a result, Congress faces decisions about reauthorizing TMA and about whether to provide states with tools to enhance the program's effectiveness in accomplishing its dual mission of promoting work and averting the loss of health insurance.

The Bush Administration has proposed to reauthorize TMA, albeit for a single year. The one-year aspect of this proposal seems motivated by a desire not to show budgetary costs at this time beyond those associated with a one-year extension. The Administration has expressed support for the program and has given no indication it would wish to see the program end after 2003. To the contrary, given the strong bipartisan backing for TMA, its continuation well beyond one year seems assured.

Chairman Billy Tauzin of the House Energy and Commerce Committee plans to mark up legislation today reauthorizing TMA for one year, as the Administration has suggested. Others on Capitol Hill have suggested that TMA be extended for the same period of time as the Temporary Assistance for Needy Families (TANF) program, the basic welfare-reform block grant that also is up for reauthorization this year and is likely to be extended for a period of five years. The Senate Finance Committee appears more likely to follow that route.

Whatever the length of the TMA reauthorization, Congress could also consider changes to help ensure that eligible families maintain insurance coverage. Bipartisan proposals have been developed in the past couple of years to give states more flexibility to simplify and streamline TMA so it is easier to navigate for families leaving welfare for work and less cumbersome for states to administer. These proposals have generated support from governors, health policy experts, and members of both houses of Congress from both parties. In late 2000, for example, the House Energy and Commerce Committee approved a measure to give states options to simplify TMA. Bipartisan bills introduced last year by Senators John Breaux and Lincoln Chafee (S. 1269) and Reps. Sander Levin and Michael Castle (H.R. 2775) included the options approved by the Energy and Commerce Committee, along with additional simplification options. A welfare reauthorization bill that Senator Jay Rockefeller introduced in March 2002 (S. 2052) contains the same set of TMA proposals as the Breaux-Chafee and Levin-Castle bills.

Examination of research on these issues suggests that a long-term reauthorization of TMA, along with approval of measures to accord states more flexibility to simplify and streamline TMA procedures, would represent sound policy.

- Studies have found that a majority of low-income parents who leave welfare lose their Medicaid coverage. Yet most low-income parents who leave welfare for work cannot get employer-sponsored insurance coverage. As a result, about one-third of the families who leave welfare become uninsured. Research by the Urban Institute also indicates that a substantial share of welfare leavers have significant health problems and, as a consequence, a particular need for continued health coverage as they enter the workforce.

- Researchers have also shown that many welfare recipients are discouraged from leaving welfare for work because low-wage jobs often lack health insurance coverage for themselves and their children. By easing these disincentives, TMA supports the goals of welfare reform.

- While TMA can be an important source of Medicaid coverage for those who leave the welfare rolls, many eligible families do not enroll in it, in part because of rigid federal rules that govern the program.

- Other families initially enroll in TMA but do not retain TMA coverage for the full period for which they are eligible. The General Accounting Office found that complicated federally-prescribed paperwork requirements make it more difficult for families to retain TMA coverage after working their way off welfare.

- Policies like TMA that extend insurance coverage are generally cost-effective because the monthly cost of Medicaid coverage declines as people remain on Medicaid for longer time spans, as shown by new analyses conducted at the Center on Budget and Policy Priorities. Helping people maintain insurance coverage improves the use of preventive care, as well as the continuity and quality of health care received.

Background

In establishing TMA in the 1980s, Congress and the Reagan Administration determined that families that make the effort to find jobs and leave welfare should not have to worry that they or their children will lose health insurance. It has long been understood that the low-wage jobs taken by welfare recipients often do not offer employer-sponsored health insurance. Moreover, researchers found that the potential loss of Medicaid discourages some mothers from leaving welfare and taking a job, particularly if they or their children have chronic health problems.(1)

Without TMA, a mother can place her children and herself at medical risk if she leaves welfare for a job that lacks private health insurance coverage. If she or her children become ill and need medical care, she may be forced to quit her job and rejoin the welfare rolls to regain Medicaid coverage that covers the cost of health care or prescription drugs her family needs. To prevent this from occurring, Congress created TMA to support low-income families transitioning from welfare to work.

Current TMA policy was largely established in the Family Support Act of 1988, one of the final domestic initiatives of the Reagan Administration.(2) That legislation made those who exit welfare because of increased earnings eligible for an initial six months of Medicaid coverage through TMA and for a second six months of coverage if the family's income is below 185 percent of the poverty line, as is the case for the vast majority of families that have left welfare within the past year.(3) To qualify for TMA, a family must have received welfare for at least three of the six months immediately preceding its exit from the welfare rolls.

The 1996 federal welfare law also affected TMA eligibility, although to a lesser degree. That law "delinked" Medicaid from welfare eligibility. To qualify for TMA, a family no longer needs to have received welfare benefits for three of the last six months; instead, the family must have been poor enough to have qualified for Medicaid under the "Medicaid family coverage category" for three of the last six months.(4) This usually does not represent a major change, however, since most states set the income limit for the Medicaid family coverage category at the same level as the state's income limit for TANF-cash assistance. These income limits are typically well below the poverty line. In the median state, the income limit for the Medicaid family coverage category is 69 percent of the poverty line.

TMA was originally scheduled to expire on September 30, 2001. In December 2000, Congress reauthorized TMA for a year to extend the deadline to September 30, 2002 — the same date the TANF authorization expires — so TMA and TANF could be reauthorized together.

Those Who Leave Welfare Often Become Uninsured

National and state-level studies conducted since the enactment of the 1996 welfare law demonstrate that parents and children who leave welfare stand a substantial chance of becoming uninsured. Urban Institute researchers found, for example, that only 35 percent of single mothers who were off welfare for six to 11 months had Medicaid coverage. Some 37 percent of these mothers were uninsured. The Urban Institute also found that the insurance status of these mothers deteriorated over time; only 22 percent of mothers who had been off welfare for a year or more still had Medicaid coverage. Nearly half of such mothers — 49 percent — were uninsured.

The Urban Institute study found that only one-third of the ex-welfare recipients who were working gained employer-sponsored coverage, while one-third of those working retained Medicaid and the other third had no coverage at all.

Children in families that left welfare fared somewhat better, primarily because Medicaid eligibility is more generous for children and more were able to retain coverage. Even so, almost one-third of the children whose families had left welfare one year earlier — 29 percent — were uninsured.(5) An Urban Institute update of this study, using data on families that left welfare between 1997 and 1999, found that insurance coverage patterns for mothers leaving welfare remained about the same in the more recent period. Coverage for children improved somewhat, primarily because of the advent of the State Children's Health Insurance Program (SCHIP).(6)

In two recent reports, researchers reviewed dozens of state-level welfare-leaver studies. Both reviews reach similar conclusions: a large fraction of parents leaving welfare — typically about half — lost Medicaid coverage, and a substantial share of them became uninsured.(7) One of these reports, prepared for the Department of Health and Human Services, found that Medicaid participation among single mothers declined as the length of time they had been off welfare increased; 57 percent of such mothers were insured through Medicaid in the first quarter after they left welfare. By the fourth quarter, the share with Medicaid coverage had dropped to 45 percent. It should be noted that some of those shown as receiving Medicaid after leaving welfare were mothers who had returned to the welfare rolls. The percentage of welfare-leaver parents who were found to be enrolled in Medicaid was much smaller among those who remained off welfare. Paradoxically, remaining self-sufficient and staying off welfare increased the risk of losing Medicaid and thereby becoming uninsured.

Former welfare recipients often encounter difficulties securing private health insurance. Part of the reason for this is obvious: welfare recipients often take low-wage jobs that do not offer insurance coverage. Analyses of employer health plans reveal, however, that additional barriers face recent welfare recipients trying to get employer-based coverage. Even if their new employer offers insurance, former welfare recipients often must wait several months before they qualify for coverage; a recent study shows that many firms in which a significant share of the employees are low-wage employees require new employees to wait four months or more.(8) If former recipients are employed as part-time workers, the restrictions become more severe and many never become eligible for private insurance. In addition, when low-wage workers do become eligible for private health insurance, they often find it difficult to afford the employee share of the insurance premiums. The study also showed that firms with greater concentrations of low-wage workers tend to impose larger employee contribution requirements than firms with more highly paid workforces.

The Importance of Transitional Medicaid

As shown, a large share of parents and children who leave welfare lose their Medicaid coverage and join the ranks of the uninsured. Analyses of Medicaid eligibility data show the situation would be considerably worse if TMA were not available.

| Arkansas | California* | Florida | New Jersey | |

| Parents Who Left AFDC - after 3 months off - after 6 months off |

61% 38% |

17% 14% |

28% 24% |

51% 49% |

| Children Who Left AFDC - after 3 months off - after 6 months off |

54% 32% |

14% 11% |

30% 17% |

40% 38% |

| * The percentage in California

is particularly low because a large share of people leaving welfare are placed in a

special "pending" Medicaid category while their eligibility status is reviewed.

People may eventually be reclassified into TMA after a more thorough determination. Source: CBPP analyses of data from Ellwood and Irvin, 2000. |

||||

A study by Marilyn Ellwood and Carol Irvin provides insight into the role that TMA plays (see Table 1).(9) A large share of the low-income parents and children who retain Medicaid coverage after leaving welfare do so because of TMA.(10) For example, in Arkansas and New Jersey, roughly half of those who retained Medicaid did so as a result of enrolling in TMA. About one-quarter of Floridians who retained Medicaid did so through TMA, as did one-sixth of Californians who retained Medicaid. (The relatively low use in California is largely due to the fact that people leaving welfare are initially placed in a special "pending" Medicaid category while their eligibility is reviewed and redetermined. This pending category serves as a temporary substitute for TMA in that state.) If TMA were not available, the proportions of former welfare recipients losing Medicaid and becoming uninsured would be substantially greater.(11)

These data also show that fewer welfare-leaver families use TMA as time passes and that TMA participation rates are lower six months after leaving welfare than immediately after. Since TMA is available for one year after leaving welfare (except for the few former welfare recipients whose income rises above 185 percent of the poverty line), the attrition from TMA is a cause for concern.

Complicated paperwork requirements mandated by federal law make it more difficult for families to retain TMA coverage. To qualify for and then continue to receive coverage during the second six months after leaving welfare, a family must file reports about income in the fourth, seventh and tenth months. If a family fails to submit these reports promptly — for example because it moved after leaving welfare and the notice was not forwarded to its new address — it loses the TMA extension. Although states have options to simplify Medicaid procedures for other categories of beneficiaries, there is little flexibility in the case of TMA.

TMA is of special importance to the large share of former welfare recipients who work despite having chronic health problems. An Urban Institute study found that more than one-quarter of mothers leaving welfare but retaining Medicaid — many of whom received TMA — reported being in poor or fair health. Although those who left welfare appeared to be somewhat healthier on average than the mothers who stayed on welfare (one-third of whom reported poor or fair health status), a large share of the welfare leavers reported chronic health problems.(12)

Making TMA More Effective

As important as it is, TMA has not been as effective as it could be in ensuring that families leaving welfare for work do not lose health care coverage. Many eligible families fail to secure TMA upon leaving welfare despite being eligible for it. Many families that do receive TMA for their first six months off welfare do not have their TMA coverage renewed for the second six months despite continuing to qualify.

Federal policy could be improved to make TMA more effective in insuring these families and averting the loss of health care coverage among those who go to work. Four improvements contained in the bills offered by Senators Breaux and Chafee (S. 1269) and Reps. Levin and Castle (S. 2775) offer states options to strengthen their welfare-to-work efforts by simplifying and streamlining complicated and inflexible federal TMA rules.

- Simplify entry into TMA. One complication is the requirement that a family must have received welfare — or had an income low enough to qualify for Medicaid under the family coverage category — for three of the previous six months. Most state welfare reform programs now push TANF recipients to find jobs quickly under a "work first" philosophy. Some of the families that find work quickly, however, have not received welfare or Medicaid for three of the previous six months and thus are ineligible for TMA. TMA rules operate here at cross purposes with welfare reform efforts that stress quick attachment to the labor force. Federal rules could be modified to give states the option of dropping the three-out-of-six-months rule for those who move off welfare quickly or making them less restrictive.(13) This option would enable states to provide TMA to any family that works its way off welfare, without requiring the family to have stayed on welfare or received Medicaid for at least three months before leaving the rolls.

Such a change would eliminate the current disincentive that discourages welfare families from going to work. It would thereby promote welfare-reform goals. The current "three-months-out-of-six" rule is inconsistent with the goal of moving families quickly from cash aid to employment.

The Breaux-Chafee and Levin-Castle bills also stipulate that families exiting TANF be notified they may still be eligible for medical assistance, in order to ensure these families know they may apply for TMA or other coverage. In addition, these bills allow states to let outstationed eligibility workers accept TMA applications, so that people can apply at a health clinic or other location rather than at the welfare office.

- Make it easier to retain TMA coverage for a full year. Federal law limits state flexibility and establishes a complicated paperwork system that can create barriers to the full use of TMA. To help prevent the drop-off in TMA usage discussed above, states could be given the option to streamline and simplify program administration by waiving these reporting requirements or making them less onerous. This would enable states to offer up to 12 months of continuous eligibility to those who qualify for TMA after leaving welfare without having to receive and process detailed reports in the fourth, seventh, and tenth months.

The General Accounting Office has identified these reporting requirements as a major barrier to the use of TMA and has recommended simplifications in this area similar to those proposed in the Breaux-Chafee and Levin-Castle bills.(14) This would give states options for TMA comparable to options already available for other categories of beneficiaries.

- Recognize that more than one year of TMA may be needed. The Breaux-Chafee and Levin-Castle bills give states the option to extend TMA for a second 12- month period. This would allow families to receive coverage for up to two years after leaving welfare.

Many states are interested in extending TMA coverage and have already taken steps to offer coverage for two years or more. These states have recognized that some former welfare recipients still may be unable to secure private health insurance after being on the job for one year. These state initiatives are supported by research indicating that former welfare recipients are more likely to be uninsured a year or more after leaving welfare than six months after leaving welfare. The states that have extended TMA beyond 12 months have generally done so through waivers that are part of a larger package of welfare reform waivers these states developed prior to the enactment of the 1996 federal welfare law.(15)

This component of the Breaux-Chafee and Levin-Castle bills would provide a more direct option for states to extend TMA for a longer period.

- Offer flexibility for states that use other Medicaid policies. A number of states now offer regular Medicaid eligibility to families with incomes up to 185 percent of the poverty line (or in some cases, a modestly higher income level). These families need not have been on welfare previously in order to qualify. These states developed these policies using other Medicaid options, such as special "Section 1115" waivers or expansions permitted under the 1996 welfare law.

Since these states already serve families with incomes up to these levels, there is no particular need in these states for a separate TMA category for families whose earnings have gone over the welfare limit. The Breaux-Chafee/Levin-Castle bills give these states more flexibility to simplify their programs by according them the option of dispensing with a separate TMA category.

A final element of the Breaux-Chafee and Levin-Castle bills provides for annual reporting of transitional Medicaid participation, so that both state and federal officials can determine the extent to which beneficiaries are using TMA.

Extending Coverage Makes Medical Care Less Costly and Can Improve Medical Quality

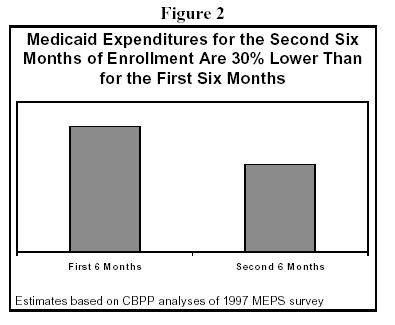

Enabling more low-income families to have health insurance coverage, as extending and strengthening TMA would do, offers significant health care advantages. New analysis indicates that helping people retain their Medicaid coverage for a longer period of time is cost-effective, because monthly health care costs tend to drop when people are covered for longer durations. We recently analyzed data from the nationally representative 1997 Medical Expenditure Panel Survey and found that average monthly Medicaid expenditures were significantly lower for people who stayed on the program for longer periods. As Figure 1 shows, Medicaid expenditures average approximately 30 percent less in the second six months of coverage than in the first six months.(16)

This is important from a budgetary perspective. It suggests TMA is less expensive than might otherwise be expected, because the period of extended coverage can have lower average monthly medical costs. Average medical expenditures decline over time for two reasons. First, people often join Medicaid because they have immediate and pressing medical problems, so medical expenses tend to be "front-loaded" and decline as people are insured for longer time spans. Second, providing coverage for longer periods helps people get preventive and primary health care services and avoid more costly trips to the emergency room, as well as costly inpatient hospitalizations. Numerous studies have found that improving continuity of coverage improves the quality of physician-patient relations and reduces unnecessary care.(17)

Reauthorization of TMA

It is widely expected that TMA will be reauthorized this year. Congress and the Administration will not let this important adjunct to welfare and Medicaid die. The chief questions are for how long it will be authorized and whether it will be simplified and improved.

The Administration has proposed reauthorizing TMA for one year with no changes. In addition, Chairman Tauzin of the House Energy and Commerce Committee plans to mark up legislation today containing a one-year reauthorization without changes. He hopes to see this incorporated into the TANF reauthorization bill (H.R. 4122).

There is no apparent reason, however, for limiting this reauthorization to one year. The motivating factor for the proposal for an extension of just one year seems to be Washington's increasingly fractious budget politics. A one-year extension avoids showing at this time the costs of operating TMA after 2003. That may carry certain modest advantages in budget debates. But all parties expect TMA to continue well beyond 2003. No one expects or is proposing that it actually cease operation after one year.

A more reasonable principle, which would be more straightforward in reflecting the expected budgetary costs, would be to extend TMA for the same length of time as the coming TANF reauthorization, which is expected to last five years, or to reauthorize TMA permanently. This would more accurately reflect the anticipated TMA costs and also keep TMA in line with other Medicaid and welfare provisions.(18)

Proposals to simplify and streamline TMA also merit consideration. Such proposals — which have modest costs — have won bipartisan support because they bolster insurance coverage and strengthen incentives to reduce welfare use. As noted, the House Energy and Commerce Committee passed a measure in late 2000 that included TMA simplification options. Last year, Senators John Breaux and Lincoln Chafee and Reps. Sander Levin and Michael Castle introduced legislation to reauthorize TMA permanently and accord states options to simplify it. TANF reauthorization legislation recently introduced by Senator Jay Rockefeller contains these TMA simplifications, along with a five-year TMA reauthorization. The National Governors Association recently reiterated its support for extending TMA as part of welfare reform.

The impending reauthorization of TMA reminds us that welfare policy and health insurance policy are intertwined. By extending and improving TMA, Congress can enable states to maintain and strengthen policies that help low-income families move from welfare to work, retain employment, and avoid the loss of health insurance coverage when they venture off the welfare rolls.

End Notes:

1. David Ellwood and Kathleen Adams, "Medicaid Mysteries: Transitional Benefits, Medicaid Coverage and Welfare Exits." Health Care Financing Review, 1990 Annual Supplement. Dec. 1990, pp. 119-131. Robert Moffitt and Barbara Wolfe, "Medicaid, Welfare Dependency, and Work: Is There a Causal Link?" Health Care Financing Review, 15:123-33, Fall 1993.

2. Prior TMA policies, established earlier in the decade, provided four months of transitional coverage to those leaving welfare due to earnings and five months of additional coverage to those meeting additional requirements.

3. Families can also qualify for four months of TMA if the receipt of child support payments makes their incomes exceed welfare limits.

4. The family coverage category replaced the earlier welfare eligibility category, under which all AFDC recipients were automatically eligible for Medicaid.

5. Bowen Garrett and John Holahan, "Health Insurance Coverage After Welfare," Health Affairs, 19(1): 175-84, January/February 2000. This study examined those leaving welfare between 1995 and 1997.

6. Pamela Loprest, "How Are Families That Left Welfare Doing? A Comparison of Early and Recent Welfare Leavers," New Federalism Report B-36, Urban Institute, April 2001.

7. Jocelyn Guyer, "Health Care After Welfare: An Update of Findings from State-Level Leaver Studies," Center on Budget and Policy Priorities, Aug. 16, 2000. Gregory Acs, Pamela Loprest and Tracy Roberts, Final Synthesis Report from ASPE "Leaver" Grants, Report to the Office of the Assistant Secretary for Planning and Evaluation, HHS, from the Urban Institute, Nov. 2001.

8. This study found that more than one-fifth of workers in firms in which 11 percent to 34 percent of the workers earned low wages had a waiting period of at least four months. See Jon Gabel, Jeremy Pickreign, Heidi Whitmore, and Cathy Schoen, "Embraceable You: How Employers Influence Health Plan Enrollment," Health Affairs 20(4):196-208, July/August 2001.

9. Marilyn Ellwood and Carol Irvin, "Welfare Leavers and Medicaid Dynamics: Five States in 1995," Report to the Office of the Assistant Secretary for Planning and Evaluation, HHS, from Mathematica Policy Research, April 2000.

10. There also are other eligibility pathways through which former welfare recipients, particularly children, may retain Medicaid. For example, all children in families with incomes below the poverty line are eligible for Medicaid, and in most states, children in families with incomes below 200 percent of the poverty line can be covered by Medicaid or separate state SCHIP programs.

11. The data from this study are from 1995 and pre-date the development of SCHIP and the other state efforts to help welfare recipients retain Medicaid. Nonetheless, these are the only data available that show the use of transitional Medicaid coverage by the months since leaving welfare. It is plausible that the proportions of former welfare recipients who are covered through TMA are somewhat smaller today than in 1995.

12. Bowen Garrett and John Holahan, "Do Welfare Caseload Declines Make the Medicaid Risk Pool Sicker?" Assessing the New Federalism Discussion Paper 00-06, Urban Institute, Sept. 2000.

13. States can bypass the three-out-of-six-months rule under current Medicaid procedures if they are willing to redesign their Medicaid eligibility rules for the "family coverage category" by using expansive earned income disregards to vitiate the three-out-of-six rule. Doing so can be complicated, however, and many states do not fully understand the option or have been reluctant to pursue this course. (Broaddus, et al. 2001.)

14. William Scanlon, General Accounting Office, Testimony to the House Subcommittee on Health, Committee on Energy and Commerce, "Medicaid: Transitional Coverage Can Help Families from Welfare to Work," April 23, 2002.

15. States also can extend Medicaid for a longer period through a more complicated route. They can disregard the earnings of welfare leavers in the Medicaid family coverage category on a time-limited basis and thereby make these families eligible for Medicaid under the family coverage category for a longer period. For example, a state can effectively provide coverage for two years after a family leaves welfare by disregarding earnings for coverage under the family eligibility category for the first year and then providing an additional year of TMA after that spell concludes. As of July 2000, some 14 states extended coverage for more than one year. Eight used Section 1115 waivers, five used the option mentioned, and one used state funds for the extension of TMA. (Matthew Broaddus, et al. Expanding Family Coverage: States' Medicaid Eligibility Policies for Working Families, Center on Budget and Policy Priorities, Dec. 2001.)

16. This analysis is based on a multivariate regression model in which we examined people who were on Medicaid for one or more month during 1997 and who had incomes below 200 percent of the poverty line. After controlling for age, gender, health status, race/ethnicity, rural-urban residence and months of non-Medicaid insurance coverage, each additional month of Medicaid coverage was associated with an average $6.49 reduction in monthly Medicaid expenditures. This was significant with 99 percent confidence. It was not possible to restrict the analysis to TMA recipients; the analysis pertains to those who are generally on Medicaid for longer versus shorter time periods. Our thanks to Emily Rothbaum of CBPP for help in these analyses. A Mathematica Policy Research study also shows that children with longer periods of enrollment have lower monthly costs. Carol Irvin, et al. "Discontinuous Coverage in Medicaid and the Implications for 12-Month Continuous Coverage for Children," Cambridge, MA: Mathematica Policy Research, Oct. 24, 2001.

17. For example, see A.S. O'Malley, et al. "Continuity of care and the use of breast and cervical cancer screening services in a multiethnic community." Arch Intern Med 157(13):1462-70, July 14, 1997 and J.M. Gill and A.G. Mainous "The role of provider continuity in preventing hospitalizations." Arch Fam Med, 7(4):352-7, Jul-Aug 1998.

18. It is an artifact of budget scorekeeping rules that there is any cost to extending TMA. Almost all of the other parts of Medicaid are permanently authorized, so most ongoing Medicaid costs are included in the budget "baseline." Because TMA expires, its ongoing costs are treated as an additional cost under budget scorekeeping rules. In any event, simply reauthorizing TMA permanently would not cost the federal government or states any more than they are now spending, as adjusted for the growth of health care costs over time or similar economic factors.