OVERALL FEDERAL TAX BURDEN ON MOST

FAMILIES — INCLUDING MIDDLE-INCOME FAMILIES — AT LOWEST LEVELS IN MORE THAN TWO

DECADES

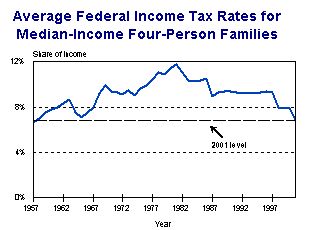

Income Taxes for Median Family of Four at Lowest Level in 44 Years

by Isaac Shapiro(1)

| PDF of this report |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Traditionally, around the April 15th filing date for income taxes, stories about mounting tax burdens — and calls by politicians for more tax cuts — occur with regularity. Yet the percentage of income that most families pay in federal taxes (referred to here as their "tax rate" or "tax burden") has been falling in recent years rather than rising, a trend well established even before the 2001 tax cut. This analysis, based on an update of Congressional Budget Office data on overall federal tax burdens from 1979 to 2000 and Treasury data on income tax burdens from 1955 to 1999, includes the following findings:

- Even before last year's tax cut was enacted, overall federal tax burdens for middle- and low-income taxpayers were lower, on average, than they had been in most years of the past several decades. This was largely a result of income tax burdens having fallen fairly sharply. The Treasury data show that in 1999, the typical family of four with two children was paying a smaller percentage of its income in federal income taxes than at any time since 1966.

- The tax cut enacted last year has reduced tax burdens further. This analysis' update of the Treasury data shows that in 2001, the year for which Americans are now filing income tax returns, a median family of four will pay a smaller share of its income in federal income taxes than in any year since 1957.

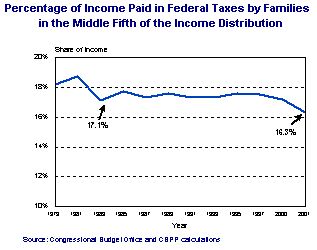

- Similarly, this analysis' update of the CBO data on overall federal tax burdens finds that when households' total federal tax burdens are considered — including their payroll, excise, and other taxes, along with the income taxes they pay — most categories of households will face a lower average tax burden in 2001 than in any year from 1979 to the present. (1979 is the first year these CBO data cover.) For example, the middle fifth of taxpayers will pay an average of approximately 16.3 percent of income in total federal taxes in 2001, the lowest percentage during the 22 year period examined. The second-lowest percentage occurred in 1983, when such households paid an average of 17.1 percent of income in federal taxes.

One often-cited statistic may appear to be at odds with these trends. The total amount of taxes the federal government collects, measured as a percentage of the Gross Domestic Product, hit a post-World War II high in 2000 and was at a higher-than-average level in 2001. This statistic is sometimes cited as evidence that the percentage of income that average or typical families are paying in federal taxes is rising, not falling. As Federal Reserve Chairman Alan Greenspan recently noted, however, it is not valid to use this statistic (i.e., federal tax receipts as a percentage of GDP) as a measure of the tax rates that families face. At a recent Congressional hearing, Greenspan responded to a question whose premise was that average taxes are now at high levels by stating: "you can't use tax receipts over nominal GDP as a tax rate." He gave one reason such an approach is improper: while capital gains taxes are counted as part of federal tax receipts, the capital gains income on which such taxes are paid is not counted in GDP. As a result, when capital gains income — and thus capital gains taxes — rise substantially, as they did at least through 2000, federal taxes necessarily increase as a share of GDP. But that increase is overstated, and does not mean middle-class families are paying more in taxes.

A second reason that an increase in total tax receipts as a percentage of GDP does not mean typical or average middle-income families are paying more in taxes is that this measure increases when the share of national income going to high-income individuals rises. Because of the progressive nature of the federal tax system, high-income taxpayers pay a larger share of their income in taxes than middle- and lower-income people do. When income becomes more concentrated at the top, high-income households bear a larger share of the taxes — and since they pay taxes at higher rates, overall federal tax receipts edge up as a share of GDP.

This is precisely what has happened in recent decades, as the Congressional Budget Office and numerous other analysts have reported. By the end of the 1990s, the latest period for which reliable data are available, income before taxes was more concentrated at the top of the income spectrum than at any time since the Great Depression. High-income taxpayers consequently have been paying a larger share of federal taxes than in the past, and this has resulted in an increase in tax receipts as a share of GDP. This does not mean, however, that taxes

on middle-income taxpayers have climbed. Nor does it mean that high-income taxpayers are being unfairly burdened. To the contrary, as this analysis shows, the average tax burdens of middle-class families have declined; meanwhile, CBO data show that in 1997, the latest year for which these data are available, the share of the national income that high-income households received even after federal taxes are taken into account was at the highest level on record. (These CBO data, as well, go back to 1979.) The CBO data also show that increases in after-tax income during the 1980s and 1990s were much larger among high-income households than among middle- and lower-income households.

Recent Trends in Income Tax Burdens

In 1998, the Treasury Department issued an analysis examining changes over time in the income tax rates paid by families of four with two dependents.(2) The Treasury projected that in 1999, the percentage of income the median family of four with two children would pay in income tax would be at its lowest level since the mid-1960s. (The median-income family is the family exactly in the middle of the income spectrum; half of families have income higher than the median family does, while the other half of families have income lower than the median family.) The Treasury's methodology is easy to replicate; this analysis does so and extends the data in the Treasury analysis through 2001. The results show:

- The median four-person family with two dependents will pay 6.8 percent of its income in federal income tax in 2001. This is the lowest percentage since 1957.

- This 6.8 percent income tax rate is about one-third lower than the average income tax rate of 10.3 percent that these median four-person families paid during the 1980s.

Trends in Total Federal Tax Burdens

The best data on trends in overall federal tax burdens come from the Congressional Budget Office.(3) These CBO data provide extensive information for the years from 1979 through 1997. This analysis updates these data through 2001.

- The average percentage of income that households in the middle fifth of the income spectrum paid in total federal taxes in 2000, before last year's tax cut was enacted, was close to the lowest on record for the period from 1979 to the present. These households paid an estimated average of 17.2 percent of their income in federal taxes in 2000, only slightly higher than the low point of 17.1 percent of income in 1983.(4)

- The tax cut enacted in 2001 was tilted toward high-income taxpayers, but many of the provisions of most benefit to that group were delayed for several years or more. By contrast, most of the tax cuts that benefit those in the middle of the income distribution took effect almost immediately in whole or significant part, reducing these households' tax burdens noticeably in 2001 and somewhat further in 2002.(5)

In 2001, the middle fifth of households will pay an estimated average of 16.3 percent of income in federal taxes.(6) This is the lowest percentage on record for the period from 1979 to the present.

The public, of course, pays state and local taxes as well. Unfortunately, there are no data that would allow determination of the level or trend in total state and local taxes borne by middle-income households. Data on total state and local taxes as a percentage of the economy, however, suggest these taxes have been stable in recent years. Commerce Department data show that state and local taxes amounted to 10.3 percent of Net National Product in nearly every year from 1995 through 2000 and edged up slightly to 10.4 percent in 2001. This Commerce Department measure of state and local taxes has been remarkably stable over time; it was at almost the same level in 2001 as it was throughout the 1990s, as well as in 1977.(7)

Trends in Taxes as a Percentage of GDP Provide Misleading Picture of Changes in Average Families' Tax Burdens

Some have argued that federal taxes and the "average tax burden" are at historic highs. To make this argument, they cite total federal tax collections measured as a percentage of the economy (or GDP). Federal tax receipts as a percentage of the economy did rise to a post-World War II high in 2000. Due to the tax cut and the economic slowdown, this percent decreased in 2001, and according to the Congressional Budget Office, will drop further in 2002.

Yet taxes as a percentage of the economy are not a good yardstick for measuring the federal tax burdens that American families face. As the Greenspan statement cited earlier indicates, taxes paid on capital gains income are counted as part of total tax collections, but the capital gains income on which these taxes are paid is not counted as part of GDP. As a result, when capital gains income and capital gains tax collections rise sharply, as occurred in the latter half of the 1990s, tax receipts measured as a percentage of GDP rise more rapidly than tax burdens are actually increasing.

The increases in taxes as a percentage of GDP through 2000 bear little relation to the changes in the tax burdens of most American families. These increases were primarily due to an extraordinary increase in capital gains income and other income that high-income taxpayers received during the latter half of the 1990s. As Lawrence Lindsey, now head of President Bush's National Economic Council, noted in Congressional testimony in 1999: "A disproportionate share of this extra revenue is coming from upper income taxpayers through higher income tax payments. The likely reason for these payments is the booming stock market. The extra revenue is in part due to higher capital gains realizations due to higher stock prices, but is probably even more dependent upon higher bonuses being paid to upper bracket individuals."(8)

In short, increases in taxes as a percentage of GDP do not signify an increase in the proportion of income that middle-income families pay in taxes. The recent evidence shows at the same time that taxes were rising as a percentage of GDP in the late 1990s, the taxes of typical middle-income families were declining. Those who cite increases in tax receipts as a percentage of GDP as evidence that the tax burdens on middle-class families have increased are misusing the data. Various publications issued by the Tax Foundation suffer from this error. (See the text box on the final page of this analysis for more detail.)

Increased Concentration of Taxes among High-income Households Not a Sound Justification for Reducing Their Taxes

Some have argued that the increased concentration of taxes among high-income individuals — and especially among the top one percent of the population — means their taxes need to be reduced sharply. Recent income and tax trends do not support this contention.

- A recent paper from the National Bureau of Economic Research shows that in 1998, the top one percent of the population received a larger percentage of the before-tax income in the nation than in any year since 1936. (This finding includes capital gains income. If capital gains income is excluded, the share of before-tax income the top one percent of the population received in 1998 was the largest since 1941.)(9)

- CBO data show that the top one percent of the population holds an exceptionally large share of the national income even after federal taxes are taken into account. In 1997, the last year for which these data are available, the top one percent of the population received a larger share of the national after-tax income than in any other year for which these data are available. These data go back to 1979.

| Average after-tax income gains, 1979-97 | |

| Top 1% | $414,200 |

| Middle fifth | $3,400 |

| Bottom fifth | -$100 |

- The CBO data also show that after-tax income rose tremendously among the top one percent of the population in the 1980s and 1990s, with the gains that high-income individuals made far outpacing the gains of other Americans. From 1979 to 1997 (the years CBO studied), the average after-tax income of the richest one percent of households climbed 157 percent, or $414,000. Among the middle fifth of households, average after-tax income rose a much more modest 10 percent, or $3,400. (The figures in this paragraph are adjusted for inflation and expressed in 1997 dollars.)

CBO has not yet released comprehensive data for the years after 1997, but the CBO study concluded that the "rapid rise in the share of income going to the top of the distribution" continued at least into 1998 and 1999.(10)

Finally, the percentage of income that the top one percent of taxpayers pays in federal taxes does not appear to be at unusually high levels. It appears to be lower today than it was during most of the 1990s and the late 1970s. It is above the levels of the 1980s, when the budget was marked by large deficits and the national debt grew rapidly.

The Tax Foundation's Average Tax Measure Does Not Reflect What Typical Middle-Class Families Pay in Taxes Each year around April 15, the Tax Foundation issues a report about what it calls "Tax Freedom Day." Last year, the Tax Foundation claimed that "the nation's taxpayers" had to work until May 3, 2001 to pay their taxes for 2001. In making this claim, the Tax Foundation relies on a measure of tax receipts as a percentage of the economy; the Foundation takes what it says is the total amount paid in federal, state, and local taxes and divides this amount by its estimate of the total amount of income in the nation. It portrays the resulting figure as the percentage of income that average Americans pay. The Tax Foundation calculation is a severely flawed measure, however, of the percentage of income that most Americans pay in taxes. Furthermore, the Tax Foundation's presentation of these figures invites middle-income taxpayers to believe they pay considerably more of their income in taxes than the data show they actually do. Average tax figure misleading. Dividing total tax receipts by total national income can provide an "average tax burden." This figure, however, does not represent the tax burden that middle-class families pay. Most middle-class families pay far less than this "average burden." Suppose four families that each have incomes of $25,000 each pay $1,250 in income tax — five percent of their income — while one wealthy family with $500,000 in income pays $125,000 in income tax, or 25 percent of its income. On average, these five families pay 22 percent of income in federal income taxes; their total income tax payments of $130,000 divided by their total income of $600,000 equals 22 percent. But this 22 percent figure is misleading if used to portray middle-class tax burdens. The four moderate-income families are paying five percent of their income in income tax, not 22 percent. Using averages for the population as a whole when talking about tax burdens for the average middle-class family produces skewed results. It ascribes to middle-class families average amounts of such taxes as the estate tax and the corporate income tax, even though these taxes are paid solely or primarily by taxpayers at considerably higher income levels. The Congressional Budget Office and the Joint Tax Committee have both found that average federal tax burdens for the middle fifth of the population are much lower than the federal tax burdens that the Tax Foundation reports highlight. Taxes counted, but taxed income not counted. The tax measure the Tax Foundation uses in its "Tax Freedom Day" report counts capital gains taxes as part of the taxes that people pay, but fails to count as income the capital gains income on which these taxes are levied. Counting taxes while failing to count the income on which the taxes are paid makes taxes appear larger as a percentage of income than they truly are. Non-tax items counted. Exacerbating these problems, the Tax Foundation also counts as taxes items that are not taxes. These include: optional Medicare premiums that older Americans pay if they wish to receive coverage for physicians' services under Medicare; intra-governmental transfers that are solely bookkeeping devices and not taxes; and rental payments that individuals or businesses pay to state or local governments to rent property those governments own. These flaws in the measurement of taxes and income have led the Tax Foundation to claim in recent years that taxes on average families have been rising, when data from CBO and the Joint Tax Committee show that tax burdens on typical middle-income families have been declining, not increasing. (See Iris Lav and Joel Friedman, "Tax Foundation Figures Lead to Inaccurate Impression of Middle-Income Tax Burdens," Center on Budget and Policy Priorities, forthcoming.) |

End Notes:

1. The author would like to thank Robert Greenstein, Iris Lav, Andrew Lee, and Peter Orszag for their contributions to this analysis.

2. "Average and Marginal Federal Income, Social Security and Medicare, and Combined Tax Rates for Four-Person Families at the Same Relative Positions in the Income Distribution, 1955-1999," Office of Tax Analysis, Department of the Treasury, January 15, 1998.

3. Effective Federal Tax Rates, 1979-1997, Congressional Budget Office, October 2001.

4. When CBO issued its latest report on these issues last year, the data that CBO compiles on household incomes were not yet available for years after 1997. CBO did have information, however, about federal tax law in 2000. CBO applied 2000 tax law to 1997 income levels and estimated that the middle fifth of households would pay an average of 16.7 percent of income in federal taxes in 2000. Actual income levels in 2000 were higher than they had been in 1997. Due to the progressivity of the tax code, this means that average tax burdens in 2000 were higher than CBO estimated when it applied 2000 tax law to 1997 income levels. Applying a "linear interpolation" method to the tax rates paid by households at different income levels in 1997 under 2000 law, this analysis estimated that the middle fifth of households paid an average of 17.2 percent of income in federal taxes in 2000.

5. Congress' Joint Committee on Taxation found that for taxpayers with incomes between $30,000 and $40,000 (which translates to taxpayers with incomes between the 43rd and 55th percentiles of the income distribution), the average percentage of income paid in federal taxes in 2001 would have been 16.1 percent without the tax cut and will be 15.1 percent when the tax cut is taken into account. These households' average tax rate will fall further, to 14.8 percent, in 2002. The Joint Tax Committee data show modestly lower overall federal tax burdens than CBO does due to methodological differences; the Joint Tax Committee data, for instance, do not account for corporate income taxes, while the CBO data do.

6. Without the tax cuts enacted in 2001, the federal tax rate on the middle fifth of the population would have risen slightly from its 2000 level, from 17.2 percent of income to 17.3 percent.

7. U.S. Department of Commerce, Bureau of Economic Analysis, National Accounts Data, various years.

8. Lawrence B. Lindsey, Federal Tax Policy, testimony before the Senate Budget Committee, January 20, 1999.

9. Thomas Piketty and Emmanuel Saez, "Income Inequality in the United States, 1918-1998," NBER Working Paper 8467, September 2001, Tables A1 and A3.

10. CBO, op. cit.