Governor Sundquist's Revised Tax Proposal

Would Address

Long-Standing Problems with Tennessee's Tax System

by Elizabeth

C. McNichol

While different in many respects, Governor Sundquist's revised tax proposal announced on March 29 is similar to his original proposal in that it would make Tennessee's tax system more fair and provide a revenue structure for the state that would grow appropriately with the state's economy.

Under Governor Sundquist's March 29 proposal, food purchased for home consumption would be exempted from state sales taxes. Local governments could continue to tax food. Architectural and engineering services would be included in the sales tax base. In addition, state taxation of businesses would be significantly changed. The bases of the current Excise and Franchise taxes would be expanded. Both corporations and unincorporated businesses would be subject to the expanded Franchise and Excise taxes.

- Exempting food from the sales tax would eliminate the most regressive element of the sales tax. The sales taxes paid by all families would be reduced. The tax savings for a typical family of four with income of $45,000 would be approximately $350 a year. Low-income families would see the largest tax cut as a share of income; households with income below $20,000 spend five times as much on food as a share of their income than households with income above $70,000.

- Taxing all businesses regardless of how they are organized will make the business tax more fair. Currently, many profitable businesses are structured in ways that avoid state business taxes. The ability of businesses to organize in ways that avoid paying Franchise and Excise taxes poses greater problems for Tennessee than for other states. In most states, personal income taxes on salaries or personal service income of business owners would substitute to some degree for business taxes. But because Tennessee has no broad-based personal income tax, much of this income remains untaxed. As a result, the tax treatment of similarly-situated businesses is not equal.

The Tax Reform Act of 1999

Note: The estimate of revenue raised is based on statements from the Department of Finance and Administration and the Fiscal Year 1999-2000 budget. Credits are subtracted from the Excise tax estimate. |

- Broadening the bases of the Franchise and Excise taxes would better match the amount of tax a business pays to the level of benefits received from the state. One major reason states tax businesses is to support the services businesses receive from state government. Broadening the base of the state business tax from taxes on profits and net worth to taxes encompassing profits, net worth, gross receipts and some compensation would measure the amount of activity a business conducts in Tennessee in a variety of ways. As a result, the amount of tax a business pays would better match the benefits it receives from state government. The level of tax-financed benefits business receives from the state — such as access to a judicial system, police and fire protection, roads, and schools — is determined more by the level of business activity undertaken in the state than by the profits earned in a particular year.

- Expanding the base of the Franchise and Excise taxes could add complexity to the state's business taxes. While there are many benefits to expanding the base of Tennessee's business taxes, care must be taken in the design of the taxes to minimize administrative complexity. For example, exemptions from the Franchise and Excise tax for small businesses reduce administrative complexity without significant revenue loss.

- The combination of eliminating food from the sales tax base

and broadening the base of the business tax would result in a revenue structure that would

grow more appropriately with the state's economy. Tennessee's current fiscal

problems — revenue declines and a $400 million shortfall in the Governor's proposed

budget — result from the failure of the state's tax collections to grow with the

state's economy. Tennessee relies heavily on the sales tax — the base of which is

composed mainly of goods not services. Spending patterns have been changing with a greater

share of consumption being made up of services. As a result, sales tax growth lags growth

in the economy. This problem is especially pronounced in the states — including

Tennessee — that tax food because food consumption has been steadily declining.

Assuming the downward trend continues, exempting food from the sales tax base would

improve the future growth of the sales tax.

In addition, one of the reasons for the decline in Franchise and Excise tax collections is the failure to tax Limited Liability Companies, partnerships, and sole proprietorships. These businesses tend to be service businesses and excluding them from the tax base excludes one of the fastest growing sectors of the economy. When state tax collections grow at a much slower rate than the economy, periodic rate increases or cuts in public services are required to compensate for diminished revenue.

- Tennessee will remain a low tax state. Tennessee has ranked last or second to last in state and local taxes as a share of personal income in fiscal years 1994, 1995 and 1996, the three most recent years that state and local Government Finance data are available from the Census Bureau. The net tax increase of approximately $400 million that would result from this proposal would not have changed these low rankings.

Exempting Food From the Sales Tax

Currently, food for home consumption is subject to both state and local sales taxes in Tennessee. The state sales tax rate is 6 percent. In addition, local governments may levy sales taxes of up to 2.75 percent.

Under the Governor's proposal, food for home consumption would be exempted from state sales taxation. The sales taxes paid by all families in the state would be reduced. The tax savings for a typical family of four earning $45,000 would be approximately $350 a year.(1)

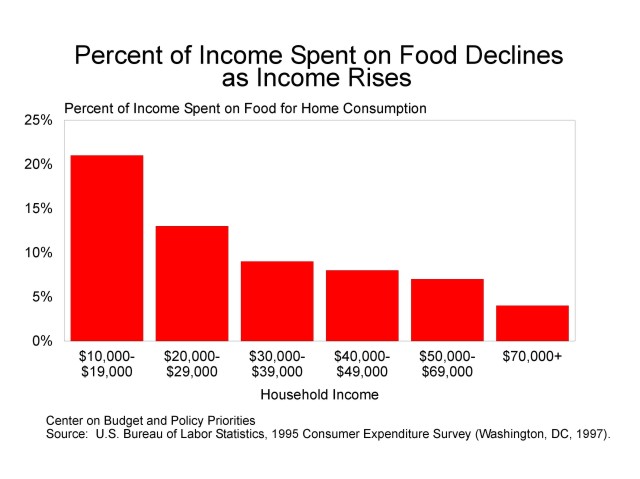

Low-income families would receive the largest benefit from the elimination of the food tax. They would see the largest tax cut as a share of income because food purchases consume more of the income of low-income families than of higher-income families. The Consumer Expenditure Survey shows that households with income between $10,000 and $20,000 spend five times as much on food as a share of their income than households with income above $70,000. (See Figure 1.)

Under federal law, states may not charge sales tax on food purchased with food stamps. Since most recipients of food stamps are poor, some analysts argue that this law protects low-income families from the sales tax on food. For most poor families, however, the food stamp exemption covers only a portion of all grocery purchases. In addition, many poor people sufficiently needy to qualify for food stamps do not receive them. (See Appendix I.)

Excluding food from the sales tax base would bring Tennessee's tax treatment of food in line with most other states. Two-thirds of the states with a general sales tax do not tax food or tax it at a lower rate than other purchases. (See Appendix II.)

In 1998, the taxation of food accounted for approximately $400 million of the total $4.1 billion state sales tax collections according to the Tennessee Department of Administration and Finance. The exemption of food would reduce state revenues by approximately this amount. In addition, local governments collected an estimated $150 million in sales tax on food which would continue under the plan.

Business Tax Equity — Unincorporated Businesses

Currently only corporations are subject to Tennessee's Franchise and Excise taxes. As a result, many profitable companies doing business in Tennessee are structured to avoid the state business taxes. For example, Limited Liability Companies, partnerships and sole proprietorships are not subject to the Franchise and Excise taxes.

Limited Liability Companies are a hybrid form of business organization that combine the protections from individual financial risk available in a corporation with the tax treatment of a partnership. Under federal tax law, the income of Limited Liability Companies — like that of partnerships — is allocated directly to business owners. The owners add the LLC profits to their income from other sources. Under the federal tax system and in most states, the owners pay personal income taxes on their total incomes including LLC profits. But because Tennessee has no broad-based personal income tax, much of this income remains untaxed.

Limited Liability Companies are engaged in many types of business in the state. A recent survey of LLC's in Tennessee found the largest number of LLC's were in Real Estate (27 percent of all LLC's), Construction (10 percent) and Retail trade (13 percent). There were some LLC's engaged in almost every type of business activity from manufacturing to auto repair to operating hotels and motels.

The ability of companies to escape Tennessee's business taxes by organizing as Limited Liability Companies has already eroded the state's tax base and could result in serious problems in the future. This form of business organization is not limited to small companies. For example, retail or grocery chains can and have organized individual outlets as Limited Liability Corporations. These individual corporations are tied to a central corporation located in another state. As a result, many of the assets of the chain are transferred out of state; the individual outlets are exempt from the Franchise and Excise taxes and, as a result, the business largely escapes Tennessee's current business taxes. National figures show a dramatic increase in this form of business organization. The Internal Revenue Service reported an increase of 87 percent in the number of LLC's between 1995 and 1996.

Partnerships are another form of business organization exempt from Tennessee's business taxes. A partnership is a business owned by two or more persons that is not organized as a corporation. The profits of partnerships are "passed through" to individual owners who add those profits to their incomes from other sources and pay federal individual income taxes on the total.

Partnerships exist in many industries. They are especially common in the finance, insurance and real estate sectors and in the medical and health and legal services industries.

A sole proprietorship — also not taxed under the Franchise and Excise taxes — is a form of business in which one person owns all of the assets of the business and the business is not a corporation. Sole proprietorships are common in retail trade, construction and business and personal services but exist in most industries.

Because Tennessee has no broad-based personal income tax, much of the income of Limited Liability Companies, partnerships and sole proprietorships remains untaxed.

Business Tax Equity — Financing State Services to Businesses

One of the major reasons states levy taxes on businesses is to generate revenue to support the services provided to businesses by state government. The ability of businesses to operate profitably benefits from state government services such as a judicial system, police and fire protection, roads, and schools. The benefits these government services confer on businesses, in turn, flow through to individuals through their roles as consumers of the products of the business or as employees or shareholders of the business. In Tennessee, as in every state, many of the individuals who benefit from Tennessee businesses do not reside in the state. For example, the shareholders of a company doing business in Tennessee could live in any state in the country. In addition, many of the products of Tennessee companies are sold out of state.

In order to ensure that both residents and non-residents who benefit from state services share in financing the costs of those services the state levies taxes on businesses. The tax levied on a business becomes a cost to the business. This cost may reduce the profits of the business, resulting in lower dividends to shareholders both in and out of the state. Some of the cost may result in higher prices for non-resident as well as resident consumers of the business's products. It is only through taxing businesses that a state can recoup some of the cost of providing services to businesses from non-residents who benefit from those services.

Currently, Tennessee taxes businesses through the Franchise tax, which taxes net worth, and the Excise tax, which taxes corporate profits. In recent years the Excise tax has accounted for approximately 66 percent of state business tax collections. The proposed legislation would retain the current Excise tax of 6 percent of profits and would expand the definition of profits to include compensation paid that exceeds $72,000 annually. In addition, the rate of the current Franchise tax would be reduced from $.25 per $100 of net worth to $.125 per $100 and the base would be expanded to include gross receipts. Considered together, the proposed business taxes would tax businesses on a variety of different bases.

The current Excise tax is a profits tax levied based on the "ability-to-pay" principle. It taxes profits — the revenues remaining after subtracting business costs. While basing taxes on "ability-to-pay" can be an important principle, especially in the case of individual taxpayers, it is not necessarily the most equitable way of allocating the costs of state services to businesses. An alternative way to tax business is to base the tax on a measure of the business's level of activity in the state. This level can be measured in many ways including compensation, net worth, gross receipts or the value added by a business.

Under the proposal, the definition of profits would be expanded to include compensation in excess of $72,000 paid by businesses to individuals. This change would address one of the ways that businesses could potentially avoid paying the current profits tax. The definition of profits for corporate income tax purposes is the total income of a business reduced by its costs including compensation. Businesses can reduce their taxable profits by increasing the compensation of high-earning employees, managers, and owners. Taxing compensation that exceeds a set level guarantees that these profits are taxed whether recorded as profits or shifted to high-earning employees and owners.

This method of taxing compensation could also improve the fairness of Tennessee's tax system. This portion of the Excise tax would be paid by businesses to the state. However, as with all business taxes, the payments made to the state will either be passed on the shareholders or owners of the business through reduced profits, be paid by consumers through higher prices or by workers through reduced wages. How the cost is passed on to individuals will be determined in part by the design of the tax but also by the market for the business's products and by the labor market. It cannot be assumed that all of the cost will be passed on the workers simply because compensation is used as a measure of business activity in the tax base. However, given the design of the tax, it is likely that any portion of the tax that is passed on through lower wages is likely to serve to reduce the wages of higher-earning employees. These are the individuals that pay the smallest share of their income in taxes under the current tax system.

Including gross receipts in addition to net worth in the base of the Franchise tax will provide an additional measure of business activity. The total amount of sales of a business is a measure of its scale of operations or size. The level of services the state provides to a business is often related to the size of the business.

One concern with gross receipts taxes is that they tend to impose relatively higher tax burdens on high-volume, low-profit industries such as grocery stores than on businesses with fewer, high-cost sales and higher profit margins such as jewelry stores. This concern, however, is not significant when the rate of the gross receipts tax is as low as the one proposed.

The amount of tax-financed benefits that a business receives from the state is more closely related to the level of business activity in the state than to the amount of profits it generates in a given year. The proposed business taxes represent a significant shift from primary reliance on the Excise tax, a corporate profits tax, to reliance on a variety of measures of the level of business activity in the state.

Appropriate Growth

Tennessee is one of very few states experiencing revenue shortfalls and a budget deficit in the current healthy economic times. Projected revenue for fiscal year 1999-2000 under the current tax structure falls over $400 million short of the amount needed to finance spending under the Governor's proposed budget.

The state's fiscal problems are not the result of a failure of the state to share in the current expansion. Tennessee's economy has been growing at a healthy rate since the end of the recession of the early 1990's. Employment growth and personal income growth have been above national rates and Tennessee's unemployment rate is below the U.S. average. Nevertheless, Tennessee's reserves are among the smallest of all the states relative to the size of the state's budget; the state has not been able to take advantage of the healthy economy to develop a cushion against future adversity.

Tennessee's fiscal problems lie with the failure of the state's taxes to grow with the economy. Tennessee relies heavily on the sales tax. As in other states, the base of the sales tax is composed mainly of goods rather than services. Spending patterns have been changing with a greater share of consumption being made up of services. As a result, sales tax revenue growth lags growth in the economy. This problem is especially pronounced in the states — including Tennessee — that tax food, because food consumption as a share of total consumption has been declining steadily.

The purchase of food for home consumption is a shrinking sector of the economy. In 1960 the average U.S. family spent 17 cents of each consumption dollar on food for home consumption; by 1995 the average family spent only eight cents of each dollar on food eaten at home.(2) Assuming the downward trend continues, exempting food from the sales tax base would improve the future growth of the sales tax.

Exempting food helps a state to counteract the gradual decline in sales tax revenues as a share of the state's economy. Except for those very few states that also broadly tax services, states that tax food find that their sales tax revenue grows at a much slower rate than personal income, requiring either periodic tax rate increases or cuts in public services to compensate for diminished revenue. States that exempt food, on the other hand, generally find that their sales tax revenue grows more rapidly, in many cases enabling them to maintain public services with less frequent tax increases.

Another major cause of Tennessee's current fiscal problems is the decline in collections from the Franchise and Excise taxes. For fiscal year 1999, Franchise and Excise tax collections appear to be falling $100 million below original projections. Revenue from these taxes are not expected to grow in fiscal year 2000 despite continued growth in the state's economy. One reason for this decline is the failure to tax Limited Liability Companies, partnerships and sole proprietorships under the Franchise and Excise taxes. These businesses tend to be service businesses and excluding them from the tax base excludes one of the fastest growing sectors of the economy.

Moreover, corporate profits taxes have a tendency to fluctuate significantly from year to year. In Tennessee, the ability of businesses to organize in order to escape Franchise and Excise taxation has contributed to the instability of these revenues. Broadening the base of the business taxes to include some compensation and gross receipts as well as including unincorporated businesses will provide a more stable revenue source for the state.

Tennessee Will Remain a Low Tax State

Tennessee is currently a very low tax state. For the three most recent years that state and local government finance data are available from the Census (fiscal years 1994, 1995 and 1996), Tennessee has ranked last or second to last in state and local taxes as a share of personal income. The net tax increase of approximately $400 million that would result from the Fair Business Tax would not have changed these low rankings.

Despite its overall low taxes, Tennessee places the heaviest tax burden on low-income families. According to a 1996 study by Citizens for Tax Justice and the Institute on Taxation and Economic Policy, taxes consumed a smaller share of income in Tennessee than on average in the United States for non-elderly couples at all income levels with one exception — the fifth of families with the lowest incomes. By removing the sales tax from food, this plan would direct substantial tax relief to these families.

Food Stamp Purchases Provide Only Partial Exemption from the Sales Tax

The federal food stamp program provides many low-income families with vouchers or electronic accounts with which to buy groceries. Under federal law, states may not charge sales tax on food purchased with food stamps. The law thus protects many low-income families from some of the tax on food.

For most poor families, however, the food stamp exemption covers only a portion of all grocery purchases; taxable cash expenditures remain a major portion of families' total food spending.

- Food stamp recipients are expected to spend 30 percent of their own income (both earned income and payments like Social Security, minus certain deductions) on groceries. Fewer than one-quarter of food stamp recipients have no "countable" income to spend and thus receive the maximum food stamp benefit amount. For the rest, food stamps cover only the difference between 30 percent of the recipient's income and a specified minimum grocery budget based on family size. Most households participating in the program consequently spend a significant portion of their cash income on food, both because they receive less than the maximum food stamp allotment and because the specified minimum budget may be less than the actual cost of purchasing sufficient food for their families.

- In addition, many poor people sufficiently needy to qualify for food stamps do not receive them because they do not know they are eligible, because they are embarrassed to be seen using food stamps, or for some other reason. According to U.S. Department of Agriculture estimates for 1995, of the 15.5 million households that met the income and asset standards for the program, about 33 percent did not apply. Other families with incomes low enough to qualify for the program may be disqualified because they own cars or other items whose value exceeds the program's strict limit on assets.

Federal law also bars taxation of food purchased with vouchers from the Supplemental Nutrition Program for Women, Infants and Children, but these WIC vouchers cover a much smaller share of low-income families' food purchases than do food stamps.

Food in State Sales Taxes

Forty-five states and the District of Columbia levy general sales taxes. A majority of those states have in some way eliminated, reduced, or offset the tax as applied to food for home consumption. The relief strategies include full or partial exemptions from the sales tax for food purchased for home consumption and credits or rebates to offset the food tax. Of the states with sales taxes:

- Twenty-six states and the District of Columbia exempt most food purchased for consumption at home from the state sales tax.

- Four states tax groceries at lower rates than other goods; they are Illinois, Louisiana, Missouri, and North Carolina. (As of May 1, 1999, North Carolina's state sales tax on food will be completely repealed.)

- Six states — Hawaii, Idaho, Kansas, Oklahoma, South Dakota, and Wyoming — tax groceries fully but offer credits or rebates to offset some of the taxes paid on food by some portions of the population. These credits or rebates usually are set at a flat amount per family member. As structured, these credits give eligible households only partial relief from sales taxes paid on food purchases.

- Nine states continue to apply their sales tax fully to food purchased for home consumption without providing any type of relief for low- and moderate-income families. They are Alabama, Arkansas, Mississippi, New Mexico, South Carolina, Tennessee, Utah, Virginia, and West Virginia. (One of those states, Virginia, has passed legislation to begin phasing out its state sales tax on food January 1, 2000, with the tax scheduled to be completely phased out by April 1, 2003.)

Local governments, which in many states levy their own sales taxes, usually follow state policy on the food exemption. The major exceptions are local governments in Arizona, Colorado and Georgia. While those three states are among the 26 states that exempt food at the state level, many cities and counties in those states tax grocery food purchases.

End Notes:

1. This estimate is based on applying the state sales tax rate of 6 percent to food purchases for a family earning $45,000 annually. The amount spent on food purchases is derived from the Consumer Expenditure Survey and is adjusted upwards to reflect systematic under-reporting of food purchases in the survey.

2. For more information see Should States Tax Food? Examining the Policy Issues and Options, Center on Budget and Policy Priorities, April, 1998.