WILL THE ADMINISTRATION’S TAX CUTS GENERATE

SUBSTANTIAL ECONOMIC GROWTH?

by

Richard Kogan

Summary

| PDF of

this report HTM of fact sheet PDF of fact sheet A companion analysis evaluates related claims by some Administration officials and other tax-cut supporters that by boosting economic growth, the tax cuts ultimately would reduce budget deficits rather than enlarge them. |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Both the tax cut enacted in 2001 and the new tax cuts proposed by the Bush Administration are promoted, to a large degree, as having substantial positive effects on economic growth. This analysis evaluates claims that the 2001 tax cut and the Administration’s new “growth” package would significantly increase economic growth.

This analysis finds little support for claims made by Administration officials and other proponents of these tax cuts that either the 2001 tax cut or the new “growth” package would generate substantial improvements in long-term economic growth. The leading studies and analyses in the field suggest the opposite — that these tax cuts would have only a small effect on the economy over the long term and that the effect is as likely to be negative as positive. The studies conclude that the negative effects on economic growth of the enlarged deficits the tax cuts will engender are likely to cancel out most or all of the positive economic effects the tax cuts might otherwise have — and, in fact, may more than outweigh the positive effects, resulting in an overall negative impact on long-term growth.

- Institutions such as the Congressional Budget Office and respected mainstream economists who have evaluated the 2001 tax cut generally do not concur with claims that it would promote significant long-term growth. Studies they have conducted have concluded that the effects of the tax cuts enacted in 2001 on long-term growth will be relatively modest and will be largely or entirely offset by the adverse economic effects of the enlarged deficits that will result.

The Congressional Budget Office concluded that the economic effects of 2001 tax cut “are uncertain but will probably be small.” CBO estimated that the effect of the 2001 tax cut on the economy will be to make the economy no more than one-half of one percent bigger or one-half of one percent smaller by 2011. These are marginal effects, whether positive or negative.

- The leading analyses of the economic impact of the 2001 tax cut by mainstream economists have reached similar conclusions. A major study by William Gale and Samara Potter of the Brookings Institution found that the likely long-term effect would be small and is more likely to be negative than positive. “Our central conclusions,” they wrote, “are that EGTRRA [the 2001 tax cut] will reduce the size of the future economy, raise interest rates, make taxes more regressive, increase tax complexity, and prove fiscally unsustainable.”

- The two other major independent analyses by respected mainstream economists have reached similar conclusions. An analysis in 2002 by Douglas Elmendorff and David Reifschneider of the Federal Reserve concludes that income tax rate reductions bearing a close resemblance to those in the 2001 law are likely to reduce the size of the economy over the long term. An analysis by Alan Auerbach of the University of California finds the 2001 tax cut will ultimately reduce the size of the economy.

- Analyses of the likely economic effects of the Administration’s new “growth” package are reaching comparable conclusions. Macroeconomic Advisers, a well-known economics consulting firm that developed the economic model the President’s Council of Economic Advisers itself uses, has issued an analysis of the “growth” plan. Macroeconomic Advisers finds the “growth” package would help make the recession shorter through the short-term stimulus effects it would have, but would have slightly negative effects on the economy over the long term.

- The judgment that the “growth” package would be damaging, rather than beneficial, also is reflected in a statement issued recently by 10 Nobel Prize laureates in economics and the President of the American Economics Association, along with several hundred other economists. This represents the first time in recent memory (and perhaps ever) that 10 Nobel laureates in economics have joined in issuing a statement on economic policy.

It also should be noted that the current economic forecasts of CBO and the Administration’s own Office of Management and Budget show no signs of any significant boost in economic growth resulting from the tax cuts. Both OMB and CBO project averages rates of economic growth in the current decade that are no greater than the average growth rates for the 1990s or the 1980s. Furthermore, the CBO growth rate projection under current law and the OMB growth-rate projection that assumes enactment of the President’s tax-cut proposals are nearly identical.

Nor does historical evidence support the notion that such tax cuts result in substantial increases in economic growth. The 1980s were a period of large reductions in marginal tax rates. Congress approved major reductions in marginal income tax rates and other tax cuts in 1981 and enacted additional large reductions in marginal rates in 1986. (Unlike the 1981 rate cuts, the cost of the 1986 rate cuts was fully offset through measures that raised revenues by broadening the tax base.) The 1990s, by contrast, were a period of marginal tax rate increases; marginal rates on higher-income taxpayers were raised in both 1990 and 1993. Tax policies in the 1980s and the 1990s thus differed sharply. Ardent believers in supply-side tax cuts argued that the 1980’s tax cuts would ignite greater economic growth while the 1990 and 1993 changes would do significant damage to the economy. But the historical record does not bear out the supply-siders’ views. The average annual rate of economic growth was as high during the 1990s business cycle as during the business cycle of the 1980s.

In short, the analyses of CBO and other respected mainstream economists on the economic effects of the 2001 tax cut and the new tax-cut proposal, the historical data on economic growth in the 1980s and 1990s, and the CBO and OMB projections of future economic growth all belie the easy claims that the tax cuts will result in large boosts to long-term economic growth. These issues are examined in more detail in the remainder of this analysis.

CBO and Other Analysts Expect Little or No Long-term Economic Gain from the 2001 Tax Cut

The large tax cut enacted in 2001, the “Economic Growth and Tax Relief Reconciliation Act of 2001” (or EGTRRA), is often described by Administration officials and Congressional supporters as enhancing economic growth over the long term. Do independent analysts concur with that judgment?

By and large, institutions such as CBO and mainstream economists who have evaluated the 2001 law do not concur with such claims. These analysts have found that the effects of the tax provisions in promoting long-term growth would be relatively modest and would largely or entirely be offset by the adverse effects on long-term growth of the enlarged deficits that the tax cut would engender. The increased deficits would soak up capital that otherwise would be available for new investments.

CBO has concluded that “The cumulative effects of the new tax law on the economy are uncertain but will probably be small.” CBO stated that “Whether the tax cut will raise or lower real (inflation-adjusted) gross domestic product (GDP) in the long run is unknown, but any effect is likely to be less that half a percentage point [of GDP] in 2011.”[1] In other words, CBO estimates that the total size of the economy in 2011 will likely be somewhere between one-half of one percent larger and one-half of one percent smaller than it would have been without the tax cut, a very small change.

In January 2001, CBO had been expecting real economic growth to average about 3.08 percent per year through 2011. For the tax cut to result in the economy being somewhere between one-half of one percent larger and one-half of one percent smaller in 2011, average annual economic growth would have to be somewhere between 3.03 percent per year and 3.13 percent per year because of the tax cut, instead of 3.08 percent per year. These are tiny effects.

Other respected analysts have reached conclusions similar to CBO’s. William Gale and Samara Potter of the Brookings Institution, in a detailed and authoritative economic analysis of the 2001 tax cut, concur with CBO that the economic effect will be small and could be either a slight increase or a slight decrease in long-term economic growth.[2] Gale and Potter also found that the effect on long-term economic growth is more likely to be a small negative than a small positive. “Our central conclusions” they wrote, “are that EGTRRA will reduce the size of the future economy, raise interest rates, make taxes more regressive, increase tax complexity, and prove fiscally unsustainable.”

Similarly, Doug Elmendorf and David Reifschneider of the Federal Reserve Board modeled a tax cut closely resembling the income-tax rate cuts in the 2001 tax-cut package. They concluded that “In sum, … a sustained tax cut reduces output [GDP] in the long run and raises output by less than 50 cents per dollar of tax reduction in the short run.” [3]

Likewise, Alan Auerbach of the University of California conducted multiple simulations of the economic effects of EGTRRA. His analysis found that “In the long run, the level of capital and hence output [GDP] has been permanently reduced by the prolonged period of reduced national saving induced by the tax cut [because of the tax cut’s effect in swelling budget deficits]. … It is difficult to put together a combination of reasonable assumptions regarding household and government behavior under which this tax cut will increase national saving and capital formation.” [4]

The Long-term Economic Effects of the Administration’s “Growth” Package

Macroeconomic Advisers, an economic consulting firm, has issued an analysis of the President’s new “economic growth” package. Macroeconomic Advisers is a prominent economics consulting firm whose analysis is especially significant because the President’s Council of Economic Advisers uses the economic model that Macroeconomic Advisers developed. In its analysis, Macroeconomic Advisers concluded:[5]

“Initially the plan would stimulate aggregate demand significantly by raising disposable income, boosting equity values, and reducing the cost of capital. However, the tax cut also reduces national saving directly while offering little new, permanent incentive for either private saving or labor supply. Therefore, … the plan will raise equilibrium real interest rates, “crowd out” private-sector investment, and eventually undermine potential GDP. Our simulations suggest that by the end of 2003 the stimulus to aggregate demand associated with the plan would raise the level of real GDP by 1.6% and reduce the unemployment rate by 0.8 percentage point. However, by 2017 the effect would be to reduce the level of potential GDP by about 0.3% and raise long-term interest rates by about ¾ percentage point (emphasis added).”

Macroeconomic Advisers found the proposed tax cuts would help make the recession shorter and the recovery quicker by providing standard Keynesian stimulus. Once the economy is back on track, however, the positive and negative effects of the tax cuts would largely offset each other, with the negative effects ultimately outweighing the positive. The Macroeconomic Advisers analysis found that by 2007 (if not sooner), the total size of the economy would be about the same as it would have been without the tax cuts and that the long-term effect on the economy would be slightly negative.

Did the Tax Cuts of the 1980s Spur Significantly Faster Economic Growth?

In 1981, Congress approved large reductions in marginal income tax rates and also reduced individual and corporate income taxes by providing new exemptions, deductions, or preferences. (Some of the tax cuts were scaled back the following year.) In 1983, payroll taxes and gasoline taxes were increased. In 1986, additional large reductions in marginal income tax rates were enacted, but this time the revenue losses were fully offset by the elimination or reduction of some exemptions, deductions, or preferences. In 1990 and especially in 1993, marginal income tax rates on the very well-off were raised.

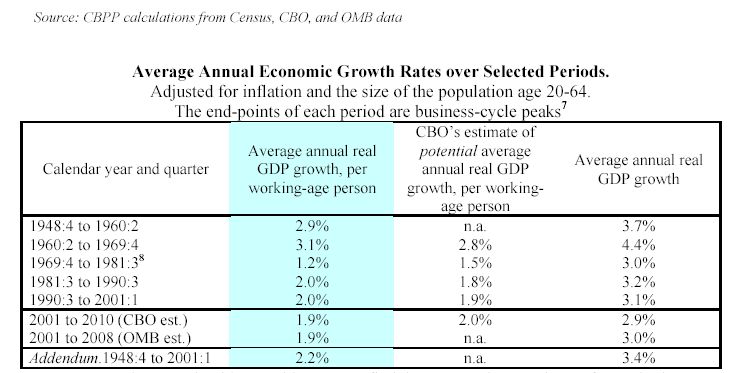

These significant changes in tax law permit us to use history as a laboratory to study the validity of supply-side claims that tax cuts of this nature spur substantial economic growth. If the claims of supply-side advocates are correct, one should have seen noticeably faster economic growth in the 1980s than in other decades; that was the decade in which marginal income tax rates were by far the lowest. But an examination of growth rates in recent decades, reflected in the table on the next page, does not show such a result.

This table presents the average annual rate of real economic growth during four periods over the last four decades. (“Real” economic growth is the rate of economic growth after adjusting for inflation.) It also shows current CBO and OMB projections for future years.

In this table, the starting and ending date for each period is a business-cycle peak. A business-cycle peak occurs when the economy stops expanding and starts contracting, so it represents the size of the economy just before the start of a recession. Economists routinely measure economic growth from one business-cycle peak to another to show the average economic growth rate over a period while avoiding distortions caused by the business cycle.

Columns 1 and 2 of the table have an important feature. Instead of featuring the total rate of real economic growth, they feature the rate of real economic growth per working-age person (here defined as the population age 20-64). In some periods, the size of the working-age population grows more quickly than in other periods, depending on past birth rates, current death rates, and patterns of immigration. Measuring economic growth on a real per-capita basis, as we do here, adjusts for changes in real economic growth that were caused solely by population growth. This also is the approach taken in much of the recently issued Economic Report of the President.[6]

An ardent supply-sider would expect to find that economic growth was fastest in the 1980s, when marginal tax rates (especially at the top of the income scale) were lowest. Supply-side theory maintains that reductions in marginal tax rates — the tax rate paid on the last dollar on income — will provide an incentive for people to work more hours or to choose to work (rather than to stay home with the children, for instance.) Supply-side theory also maintains that reductions in marginal tax rates will provide an incentive to save rather than spend a higher share of one’s income, ultimately leading to greater business investment and hence higher productivity. The total amount of work and the level of productivity (output per hour worked) together determine the size of the economy, which is why supply-side theory says that lower marginal tax rates should produce faster economic growth.

|

Why was Growth Worse in the 1970s? The table indicates that economic growth in the 1970s was worse than in the other four periods examined. The common explanation was that the OPEC oil embargo of 1973 was a main culprit, triggering both recession and inflation. But the data may suggest a different answer. If the data on economic growth had not been adjusted for the growth of the working-age population, the average annual growth rate in the 1970s would have been hardly distinguishable from the growth rates in the 1980s and 1990s or the projected rates for the current decade (see column 3 of Table 2). The 1970s looks worse only after adjusting for the rapid growth of the working-age population, which grew unusually quickly during that decade. This rapid population growth occurred because the baby-boom generation, born in the years following World War II, was just reaching working age. Because people just starting their careers are less experienced and productive than they will later become, the low per-capita economic growth rates of the 1970s can be explained partly by this sudden influx of inexperienced workers, pulling down the per-capita growth rate but not the total economic growth rate. Moreover, the 1970s were marked a very rapid increase in the rate of college attendance; some of the baby boomers who were entering working age (age 20-64) chose further education rather than immediate employment, again lowering the per-capita economic growth rate during the 1970s but likely raising it in subsequent decades. |

Measuring economic growth per working-age person, as the table does, is a direct examination of supply-side theory. If supply-side beliefs are correct, a reduction in marginal tax rates should result in a larger share of working-age population choosing to work (or to work longer hours, which produces the same result). Likewise, workers should become more productive as a result of increased levels of business investment. Real GDP growth per working-age person thus should be fastest when marginal tax rates are lowest.

But the table shows that history does not bear out such a belief. While growth rates were higher in the 1980s than in the 1970s, they were lower than in the 1950s and 1960s and the same as in the 1990s, when marginal tax rates were significantly higher on those in the top income brackets.[9] This is not to say that supply-side effects are non-existent; rather, the positive effects of supply side tax cuts have likely been quite modest and largely or fully offset by the negative effect on business investment of higher deficits caused by the tax cuts. Leading studies comparing the 1980s and 1990s have concurred that supply-side effects are modest.[10]

The table on page 6 also shows OMB projections from 2001 to 2008 and CBO projections through 2010. The 2001 tax cut — like the 1981 tax cut — featured major reductions in marginal income tax rates and was billed as a “pro-growth” tax cut. Yet both OMB and CBO project real, per-capita economic growth averaging 1.9 percent per year over these periods, no faster than the growth that occurred in the 1990s.

Neither historical data on economic growth nor the CBO and OMB projections of future economic growth suggest that supply-side tax cuts have clearly discernable, large effects on the economy. The higher deficits or smaller surpluses that the tax cuts generate slow long-term growth to some extent, counteracting the modest economic gains that supply-side tax cuts might otherwise produce.

Conclusion

Claims that the new “growth” package and the 2001 tax cuts would significantly increase long-term economic growth are being used to promote costly tax cuts in the face of projected deficits that would last as far as the eye can see. These claims are not supported by the leading studies in the field, which generally find the proposed tax cuts would have — or prior, similar tax cuts have had — only small effects on economic growth and that the effects could as well be negative as positive. Nor are these claims supported by either the historical record or budget projections. As a result, the tax cuts need to be evaluated primarily on the basis of their cost, their effects on long-term deficits and debt, their effects on the ability of government to meet basic commitments and priorities, and their fairness.

End Notes

[1] The Budget and Economic Outlook: Update, August 2001, page 34. Available at ftp://ftp.cbo.gov/30xx/doc3019/EntireReport.pdf.

[2] William G. Gale and Samara R. Potter, “An Economic Evaluation of the Economic Growth and Tax Relief Reconciliation Act of 2001,” National Tax Journal, March, 2002, also available at http://www.brook.edu/dybdocroot/views/articles/gale/200203.pdf.

[3] Douglas W. Elmendorf and David L. Reifschneider, “Short-Run Effects of Fiscal Policy with Forward-Looking Financial Markets,” National Tax Journal, September 2002.

[4] Alan J. Auerbach, “The Bush Tax Cut and National Saving,” National Tax Journal, September 2002.

[5] Macroeconomic Advisers, A Preliminary Analysis of the President’s Jobs and Growth Proposals. LLC, January 10, 2003.

[6] Council of Economic Advisers, Economic Report of the President, February 2003. In Chapter 6, “A Pro-Growth Agenda for the Global Economy,” the Report contains six graphs and one table of economic data, each of which portrays the data in real per-capita terms, i.e., after adjusting for inflation and population. Likewise, in Table 1-2 (page 66 of the Report), the first adjustment to real GDP growth is to account for changes in the population.

[7] The period of the 1970s included a recession starting in the fourth quarter of 1973. Likewise, the period from 1948 through 1960 included a recession starting in 1953 and another starting in 1957.

[8] The recession at the end of the 1970s was a “double-dip” recession, with economic peaks occurring in 1980:1 and 1981:3. For purposes of Table 2, we treat the second of the two peaks as the end of the 1970s and the start of the 1980s. Most economists use the first of the two peaks, however, and if we had done so, real per-person growth in the 1970s would have measured 1.4 percent (rather than 1.2 percent) and real per-person growth in the 1980s would have measured 1.6 percent (rather than 2.0 percent). Our choice of the second peak of the double-dip recession thus makes economic growth in the 1980s look better than if we had chosen the first peak. This choice, like others in this analysis, gives the benefit of the doubt to advocates of supply-side tax cuts.

[9] The table also shows CBO’s estimates of potential economic growth over the same time periods. When CBO calculates potential economic growth, it adjusts for the business cycle, allowing us to see the effect on economic growth of underlying factors. Those factors include the nature of the tax code and the size of the federal surplus or deficit. These projections represent CBO’s judgment of the underlying rate of economic growth when the economy is not affected by temporary conditions. CBO’s calculations of potential economic growth give the same basic result as the data on actual economic growth — the decade of the 1980s looked better than the 1970s, similar to the 1990s, and not as good as the 1960s.

[10] For example, “overall, labor supply is not greatly affected by taxes,” Joel Slemrod and Jon Bakija, Taxing Ourselves: A Citizen’s Guide to the Great Debate over Tax Reform, (MIT Press: Cambridge, 1996, page 106. Also, “saving is not very responsive to the after-tax rate of return,” B. Douglas Bernheim and John Karl Scholz, “Savings, taxes and,” in Joseph Cordes, Robert Ebel, and Jane Gravelle, eds., Encyclopedia of Taxation and Tax Policy, (Urban Institute Press: Washington, 1999), page 326. Overall, marginal tax rate reductions have “only modest effects on broad income,” Jonathan Gruber and Emmanual Seaz, “The Elasticity of Taxable Income: Evidence and Implications,” NBER Working Paper 7512, January 2000. For a more complete discussion of the academic literature on tax rates and economic growth, see Peter R. Orszag, “Marginal Tax Rate Reductions and the Economy: What Would Be the Long-Term Effects of the Bush Tax Cut?” Center on Budget and Policy Priorities, March 16, 2001, available at https://www.cbpp.org/3-15-01tax.pdf.