|

March 19, 2007

ECONOMIC EFFECTS OF THE PAY-AS-YOU-GO RULE

by Aviva Aron-Dine and Robert Greenstein

The budget resolution approved March 15 by the Senate Budget Committee would reinstate in the Senate the Pay-As-You-Go budget rule that was in force during the 1990s. (The House of Representatives reintroduced the PAYGO rule several months ago.) PAYGO requires that the costs of any legislation that increases entitlement spending or decreases revenues be offset. Thus, if adhered to, PAYGO would prevent Congress from enacting new entitlement or tax legislation that adds to federal budget deficits.

Supporters of reinstating the PAYGO rule have argued that by containing the size of the nation’s budget problems, PAYGO will improve the long-term economic outlook, as well as the long-term budget outlook. Some opponents of PAYGO, however, contend that PAYGO instead would hurt the economy because it would block Congress from extending the 2001 and 2003 tax cuts without paying for them. For example, White House Office of Management and Budget Director Rob Portman has stated, “we think that if you apply [PAYGO] on the tax side, and say that you cannot extend existing tax relief… that could have a very detrimental impact on our economy…”[1]

This analysis compares the economic consequences of adhering to PAYGO with the economic consequences of extending expiring tax cuts without paying for them. It reaches three main conclusions:

- If current budget policies (including recent deficit-financed tax cuts) are continued, the nation’s long-term budget problems will be severe and pose serious risks to the economy.

- Adhering to PAYGO will not eliminate the long-term budget shortfall, but that shortfall will be substantially smaller if Congress adheres to PAYGO than if it extends expiring tax cuts without paying for them. As a result, adhering to PAYGO would likely have significant economic benefits.

- The claim that PAYGO will hurt the economy assumes that extending the tax cuts would boost economic performance even if doing so adds trillions to federal deficits and debt. However, studies of the economic effects of deficit-financed tax cuts have reached the opposite conclusion, finding that unpaid-for tax cuts are likely to harm the economy in the long run.

1. The Long-Term Budget Problem and the Economy

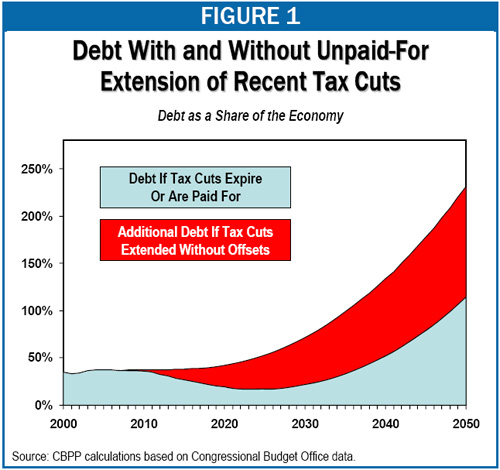

Long-term budget projections issued by the Congressional Budget Office, the Government Accountability Office, the White House Office of Management and Budget, and the Center on Budget and Policy Priorities all point to the same conclusion: current budget policies are unsustainable. Under the CBPP projections (which are based on CBO data and assume that current laws governing Medicare, Social Security, and other programs remain unchanged, the 2001 and 2003 tax cuts are made permanent, and relief from the Alternative Minimum Tax is continued), federal budget deficits will reach 20 percent of the Gross Domestic Product by 2050.[2] Federal debt will grow explosively and exceed 230 percent of GDP by 2050.

Our projections also show that, well before reaching that point, deficits and debt would grow to levels widely recognized to be damaging to the economy. By 2035, the deficit would equal more than 9 percent of GDP, and the federal debt would reach nearly 100 percent of GDP, close to its highest level in U.S. history.

The Long-Term Budget Shortfall Poses Serious Risks to the Economy

Large, sustained budget deficits and high levels of federal debt negatively affect the economy because they reduce national saving.[3] National saving is the sum of private and public (government) saving. Budget surpluses constitute government saving; budget deficits constitute government dissaving (or negative saving). When the federal government runs a deficit, it pays for the shortfall by borrowing money from the private sector. This borrowing consumes a portion of private savings and lowers net national saving.

Decreases in national saving result in either or both of two outcomes. First, they may make fewer funds available for investment in the United States, which decreases the size of the U.S. capital stock: the total supply of equipment, buildings, and other productive assets. With less capital available, future workers are less productive, and the decreased productivity lowers national income. Second, a reduction in national saving may lead to an increase in U.S. borrowing from abroad and, thus, an increase in foreign investment in the United States. To the extent that reductions in national saving lead to increased foreign borrowing, they do not lower U.S. domestic investment or future U.S. labor productivity. However, they still reduce future national income, because the income earned on investments made by foreigner lenders accrues to those foreign lenders, rather than remaining in the United States.

Most likely, reductions in national saving produce a mix of both outcomes: some reduction in domestic investment and some increase in foreign borrowing. Regardless, they lower future U.S. living standards. (Some have claimed that deficits lead almost entirely to higher foreign borrowing, rather than lower domestic investment, and that this means they have no negative economic effects. As the above analysis makes clear, this is incorrect. For a more complete discussion, see the appendix.)

Lower national saving would have a corrosive effect on the economy over a long period of time. As Federal Reserve Chairman Ben Bernanke testified before the House Financial Services Committee, budget shortfalls like those projected for future years “reduce national saving and therefore imperil, to some extent, the future prosperity of our country.”[4] In addition, a number of experts have warned there is a serious risk that the large, sustained deficits projected under current policies could lead to a more sudden financial crisis (which could occur well before debt reached 200 percent of GDP). For example, former Treasury Secretary Robert Rubin, newly-appointed CBO Director Peter Orszag, and Wall Street economist Allen Sinai have written that “ongoing deficits may severely and adversely affect expectations and confidence, which in turn can generate a self-reinforcing cycle among the underlying fiscal deficit, financial markets, and the real economy.”[5] Such a cycle could produce a dramatic downturn in investment and a deep recession.

2. PAYGO Would Significantly Reduce the Size of the Long-Term Budget Problem

The long-term budget projections discussed above assume that recent tax cuts are extended without offsets. Even if the tax cuts are not extended — or are extended but with the costs being offset, as would be required under PAYGO — the long-term budget problem would be severe. But PAYGO would substantially reduce the size of the problem (see Figure 1). By 2050, debt would stand at about 115 percent of the economy — still a very high level, but about half what it would be if the tax cuts were extended without offsets.[6]

Decisions about expiring tax cuts will have such large effects on the long-term fiscal outlook because these choices will be made soon. Declining to extend the tax cuts, or offsetting the cost of doing so, would increase revenues (or reduce spending) by about 2 percent of GDP each year, beginning just a few years from now. The resulting fiscal improvement would reduce the debt — and interest payments on the debt — for many years, with the salutary fiscal effects growing larger every year due to the “magic of compound interest.” Over time, the effect on annual deficits would grow to be considerably larger than 2 percent of GDP.

3. The Economic Effects of Unpaid-For Tax Cuts

Given the size and significance of the long-term budget problem, one would think that the substantial improvement in the fiscal outlook that would result from adhering to PAYGO would benefit the economy. The Administration and other opponents of the PAYGO rule, however, have argued that PAYGO would on balance harm the economy, because it would prevent Congress from extending the 2001 and 2003 tax cuts without paying for them. A central question, therefore, is whether extension of the 2001 and 2003 tax cuts would benefit the economy even if deficit financed. Studies by economists at the Joint Committee on Taxation, the Brookings Institution, the Congressional Budget Office, and the University of California Berkeley suggest that the answer is no.

- In a 2005 study, the Joint Committee on Taxation examined the economic effects of reductions in individual and corporate tax rates and an increase in the personal exemption. It found, “Growth effects eventually become negative without offsetting fiscal policy [i.e. without offsets] for each of the proposals, because accumulating Federal government debt crowds out private investment.”[7]

- Also in 2005, Brookings economist William Gale and then-Brookings economist (now CBO director) Peter Orszag examined the effects that extending the 2001 and 2003 tax cuts without paying for them would have on incentives for investment. They found that, under most plausible assumptions, extending the tax cuts without paying for them would reduce incentives for investment.[8] In a separate analysis, Gale and Orszag concluded that making the tax cuts permanent without offsetting their cost would be “likely to reduce, not increase, national income in the long term.”[9]

- The Congressional Budget Office examined the economic effects of a 10 percent across-the-board cut in income-tax rates. It found that, if deficit-financed, the rate reduction could potentially reduce economic output. Notably, CBO’s study also debunked the argument that tax cuts need not be subject to PAYGO because they generate economic growth that increases revenues by enough to pay for the tax cut.[10] CBO found that, under certain assumptions, the increased deficits resulting from the tax cut would be enough of a drag on the economy that the tax cut actually would lose more revenue than if one assumed it had no effect on the economy. In other words, deficit-financed tax cuts could be even more expensive than officially “scored,” rather than less expensive or costless.[11]

- University of California Economics Professor Alan Auerbach simulated the economic effects of the 2001 reductions in marginal tax rates, increase in the child tax credit, “marriage penalty relief,” and AMT relief under various financing assumptions. He found that the only scenario under which the tax cuts increased the size of the capital stock and thus increased long-run economic output was one in which they were fully paid for with spending cuts at the time they were enacted. Auerbach concluded, “whatever its benefits, the tax cut [enacted in 2001] does not offer the promise of enhancing saving and expanding output in the long run.”[12]

|

Tax Cuts and the Economy in the Short Run

This analysis focuses on the impact of tax cuts on the economy over the long run. In the short run, deficit-financed tax cuts may actually prove beneficial to the economy, if it is in a recession. Deficit-financed tax cuts (and deficit-financed government spending) boost aggregate demand and stimulate the economy and may therefore be advisable in an economy in which output is below its potential level (although it should be noted that the Federal Reserve’s handling of business-cycle fluctuations is often more effective than fiscal policy).

Relatedly, one concern some have raised about letting the 2001 and 2003 tax cuts expire, or fully offsetting the cost of extending them, is that doing so might have negative short-term effects on the economy: the converse of the economic stimulus effects described above. This argument is distinct from claims about the tax cuts’ long-term economic effects. It may be a reason to consider phasing in any increase in revenue levels over several years (which Congress would be permitted to do under PAYGO provided that the phase-in was paid for over each of the time periods taken into account under the PAYGO rule). But it has no bearing on the question of what level of revenues is most appropriate in the long run, or whether the economy would benefit in the long term from making the tax cuts permanent without offsets.

For example, a recent Goldman Sachs analysis raised concerns about the short-term economic impact of allowing all of the tax cuts to expire abruptly at the end of 2010. But Goldman Sachs also commented that if the tax cuts expire (or are fully offset), “In the longer run, economic growth benefits from ‘crowding in.’ When the government runs a large deficit, ‘crowding out’ occurs in the capital markets… As a result, growth suffers and real interest rates rise. The opposite occurs [if the tax cuts expire]. Restoring better balance in the government’s books reduces the deficit and hence the growth in its debt. This frees funds that now flow to the private sector, allowing the capital stock to grow more rapidly and pushing down interest rates… This, eventually, raises output by about 1 percent above the level that would have prevailed without the tax increase.”*

* Goldman Sachs, “Fiscal Policy: Marking Time Until the Tax Cut Sunsets,” November 10, 2006. |

Conclusion

In its most recent analysis of the long-term budget situation, the Congressional Budget Office commented that the economic benefits associated with lower marginal tax rates “are small compared with the economic benefits of moving the budget onto a sustainable track.”[13] By substantially reducing the size of the long-term fiscal problem, reintroducing and adhering to PAYGO would make this considerably easier to do. It therefore would be a desirable step to take, not only because of its impact on the federal budget but also because of its likely beneficial effect on the U.S. economy.

Appendix: Deficits, National Saving, and Long-Run National Income

National saving is the sum of private and public (government) saving, and deficits are a form of government dissaving. Hence, all other things equal, when the government’s budget deficit increases, national saving falls.[14] As explained in the body of this analysis, reductions in national savings lead either to lower domestic investment — lower investment in the United States — or to increased borrowing from abroad.

There is some debate over whether or not reductions in national saving reduce domestic investment. This question is important because it is domestic investment that determines the size of the U.S. capital stock, and the size of the U.S. capital stock is a key determinant of the productivity of future U.S. workers. Some argue that, in today’s more global economy, increased government deficits simply lead to increased borrowing from — and thus, increased investment by — foreigners. They contend this means that deficits do not reduce domestic investment, and they sometimes imply that it means deficits have no negative economic effects.

This argument is flawed in two respects.

- The evidence suggests that, while a reduction in national saving does lead to some increased borrowing from (and investment by) foreigners, much of the reduction still translates into lower domestic investment. This conclusion emerges from each of two different approaches to studying this issue. First, studies have found that across countries, the level of domestic saving is highly correlated with the level of domestic investment, even in today’s more global economy.[15] This suggests that increased foreign investment offsets only a modest portion of reductions in national saving. Studies have also found evidence that higher U.S. government deficits lead to higher U.S. interest rates; higher interest rates lead to lower domestic investment.[16]

- Even if reductions in national saving do not reduce domestic investment, they still have economic costs. As Gale and Orszag explain, “The reduction in investment reduces the capital stock owned by Americans, and therefore reduces the flow of future national income. Either the domestic capital stock is reduced… or the nation is forced to mortgage its future capital income by borrowing from abroad… In either case, future national income is lower than it otherwise would have been” [emphasis added] .[17]

Federal Reserve Chairman Ben Bernanke summarized some of the issues surrounding the effects of deficits in a global economy in recent testimony to the House Budget Committee. He noted:

[I]f government debt and deficits were actually to grow at the pace envisioned… the effects on the U.S. economy would be severe. High rates of government borrowing would drain funds away from private capital formation and thus slow the growth of real incomes and living standards over time. Some fraction of the additional debt would likely be financed abroad, which would lessen the negative influence on domestic investment; however, the necessity of paying interest on the foreign-held debt would leave a smaller portion of our nation’s future output available for domestic consumption. Moreover, uncertainty about the ultimate resolution of the fiscal imbalances would reduce the confidence of consumers, businesses, and investors in the U.S. economy, with adverse implications for investment and growth.[18]

The increasingly open world economy thus is not a reason to be dismissive of the adverse effects of the large, persistent budget shortfalls projected under a continuation of current budget policies.

End Notes:

[1] Hearing before the House Budget Committee, February 6, 2007.

[2] For further discussion and an explanation of the CBPP projections, see Richard Kogan, Matt Fiedler, Aviva Aron-Dine, and James Horney, “The Long-Term Fiscal Outlook Is Bleak: Restoring Fiscal Sustainability Will Require Major Changes to Programs, Revenues, and the Nation’s Health System,” Center on Budget and Policy Priorities, January 29, 2007, https://www.cbpp.org/1-29-07bud.htm. For comparisons between our projections and those issued by other organizations, see Richard Kogan and Matt Fiedler, “The Technical Methodology Underlying CBPP’s Long-Term Projections,” Center on Budget and Policy Priorities, January 29, 2007, https://www.cbpp.org/1-29-07bud-meth.pdf.

[3] It should be noted that running deficits for a shorter period of time, while the economy is in a recession, may sometimes be economically beneficial. See box on page 5.

[4] Hearing before the House Financial Service Committee, February 15, 2006.

[5] Robert E. Rubin, Peter R. Orszag, and Allen Sinai, “Sustained Budget Deficits: Longer-Run U.S. Economic Performance and the Risk of Financial and Fiscal Disarray,” January 4, 2004.

[6] Our projections actually understate the benefits of adhering to PAYGO. We assume that only the portion of the cost of AMT relief due to the 2001 and 2003 tax cuts expires or is paid for; if the full cost of AMT relief were offset, the improvement in the fiscal outlook would be larger. Furthermore, some who oppose PAYGO because of the restraints it imposes on tax cuts also argue that, without restraints, Congress would enact major increases in entitlement spending. If this is the case, the fiscal impact of the PAYGO rule, relative to what would otherwise occur, is even greater.

[7] Joint Committee on Taxation, “Macroeconomic Analysis of Various Proposals to Provide $500 Billion in Tax Relief,” JCX-4-05, March 1, 2005, http://www.house.gov/jct/x-4-05.pdf.

[8] William Gale and Peter Orszag, “Deficits, Interest Rates, and the User Cost of Capital: A Reconsideration of the Effects of Tax Policy on Investment,” Urban-Brookings Tax Policy Center Discussion Paper No. 27, August 2005, http://www.urban.org/UploadedPDF/311211_TPC_DiscussionPaper_27.pdf.

[9] William Gale and Peter Orszag, “Bush Administration Tax Policy: Effects on Long-Term Growth,” Tax Notes, October 18, 2004, http://www.cbo.gov/ftpdocs/69xx/doc6908/12-01-10PercentTaxCut.pdf.

[10] Senate Budget Committee Ranking Member Judd Gregg, for example, has stated, “You have to pay for these tax cuts twice under these pay-go rules if you apply them, because these tax cuts pay for themselves.” Reported in Emily Dagostino, “Senate Budget Committee Passes Budget Resolution,” Tax Notes, March 10, 2006.

[11] Congressional Budget Office, “Analyzing the Economic and Budgetary Effects of a 10 Percent Cut in Income Tax Rates,” December 1, 2005, http://www.cbo.gov/ftpdocs/69xx/doc6908/12-01-10PercentTaxCut.pdf. CBO also found that, even in a best-case scenario, the tax cut would boost economic growth enough to offset only a fraction of its total cost.

[12] Alan J. Auerbach, “The Bush Tax Cuts and National Saving,” National Tax Journal, September 2002.

[13] Congressional Budget Office, “The Long-Term Budget Outlook,” December 2005.

[14] Deficits would not reduce national saving if, when the government ran a deficit, households increased their own saving enough to fully offset the government dissaving. But the empirical evidence suggests a far more limited private response, including in the case of deficit-financed tax cuts. See D. Andrew Austin, “Running Deficits: Positives and Pitfalls,” Congressional Research Service, September 20, 2006.

[15] In a recent paper, Martin Feldstein (who was Chairman of the Council of Economic Advisors under President Reagan) found that, while the correlation between domestic saving and domestic investment has fallen significantly over the past decade in smaller countries, the correlation remains quite strong in the larger OECD countries. Martin Feldstein, “Monetary Policy in a Changing International Environment: The Role of Capital Inflows,” National Bureau of Economic Research Working Paper No. 11856, December 2005.

[16] For a review of the literature, see William G. Gale and Peter R. Orszag, “The Economic Effects of Long-Term Fiscal Discipline,” Urban-Brookings Tax Policy Center Discussion Paper, December 17, 2002, http://www.urban.org/UploadedPDF/310669_TPC-DP8.pdf.

[17] William G. Gale and Peter R. Orszag, “The Economic Effects of Long-Term Fiscal Discipline.”

[18] Hearing before the House Budget Committee, February 28, 2007. |