PROPERTY TAXES IN

PERSPECTIVE

By

David H. Bradley

| PDF of full report |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Summary

Some observers suggest that a property tax “crisis” is brewing because property tax collections nationwide as a share of income have risen somewhat over the last few years, and imply that a new round of property tax revolts might be the appropriate response. The data show, however, that there is no crisis. At most, there is a cyclical uptick in property tax collections relative to income that historically occurs in the aftermath of a recession and fiscal crisis. If the historical trend holds, property taxes will stabilize or decline over the next several years — without the need for tax revolt-type limitations.

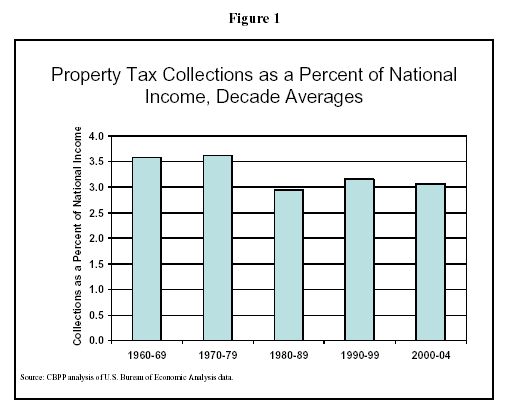

- Property tax collections, as a share of national income, are still low by historical standards of the last half century. In 2004, property taxes averaged 3.12 percent of national income, compared to 3.5 percent in the late 1970s. Property taxes are below average compared to the 1960s, 1970s, and 1990s and only slightly above the average level of the 1980s.

- The recent bump upwards in property tax collections as a share of income does not reflect a long-term trend, but rather a typical response to a recession. Property tax collections as a share of income are cyclical and tend to rise during and following economic recessions and remain relatively flat or fall during expansions.

- Property values are rising in many parts of the country, which also contributes to the uptick in property tax collections. Property tax rates, by contrast, have not risen much.

- Local policymakers have not been able to lower property tax rates as much as they might have desired as property values rose and incomes declined during the economic downturn because they faced underfunded mandates from the federal government and decreased state aid. For example, the cost to states and localities of underfunded federal mandates (such as the No Child Left Behind education law) exceeds the total amount of property tax increases over the past four years. Total property tax collections increased by $67 billion from 2000 to 2004, while unfunded mandates to state and local governments cost $73 billion from fiscal year 2002 through fiscal year 2005.

|

Measuring Property Tax Levels Advocates of tax revolts often express property tax changes in nominal dollars, to make it sound as if property taxes are growing rapidly. Expressed in nominal dollars, property taxes have increased from $254.6 billion in 2000 to $321.5 billion in 2004. That is a 26 percent increase, or an annual rate of increase of 6.0 percent. Viewed in isolation, such increases are misleading. Property taxes grow because the economy grows, causing new buildings to be built and increasing the value of existing buildings. Economic growth also leads to income growth. Thus it is far more appropriate to consider property tax levels as a percent of income. Measuring property taxes relative to income both acknowledges that economic growth appropriately increases revenues and reflects, on average, the ability of people to pay the tax. |

- As the economy improves and incomes again grow, property tax collections as a share of income are likely to stabilize or decline, as they have in other recoveries.

- Given the external factors driving property tax collections, blunt-instrument “reforms” such as a uniform property tax cap are not an appropriate response. Such caps carry ramifications that extend well beyond the problem they purport to address, and typically lead to long term inequities in property taxes paid by similarly situated households. Moreover, such limits often lead to greater than expected or desired reductions in vital public services funded by property taxes, such as K-12 education, police, and fire protection.

- Alternative methods of alleviating property tax burdens could include increased state aid to localities and targeted tax relief for low-income families most burdened by property taxes.

The Long Decline and Cyclical Nature of Property Tax Collections

Property tax collections by state and local governments today are low by historical standards. In 2004, Americans paid an estimated 3.12 percent of national income in property taxes — a lower percentage than the average amount paid in the 1960s, in the 1970s, or in the 1990s.[1]

By comparison, in the late 1970s, when California and other states faced a wave of Proposition 13-style tax revolts, property taxes as a share of income exceeded 3.5 percent — well above current levels.

Figure 1 illustrates the extent to which property tax collections today are below historical levels.

- From 1960 to 2004, property tax collections averaged 3.29 percent of national income, 5.6 percent higher than the 2004 level of 3.12 percent.

- Property tax collections today are below all periods except for the 1980s. From 2000 to 2004 property tax collections averaged 3.06 percent of national income, below the average of the 1960s, 1970s, and 1990s, and slightly above the 1980s average of 2.94.

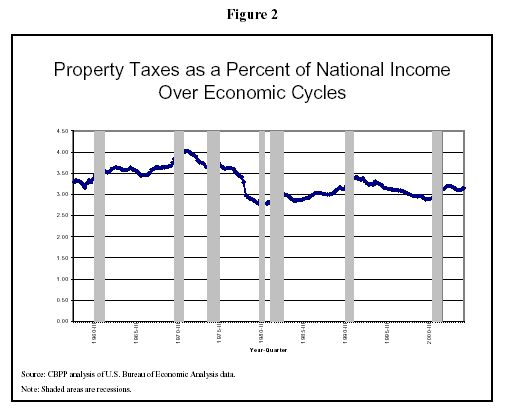

There has been a recent upturn in property taxes, but this appears largely to be a cyclical phenomenon, as Figure 2 shows. Since early 2000, when property tax collections as share of national income reached a 15-year low of 2.88 percent of national income, property tax collections have risen to 3.06 percent at the trough of the recession (late 2001) and to a current level (late 2004) of 3.16 percent of national income as the fiscal crisis lingers — an increase of about 9 percent.

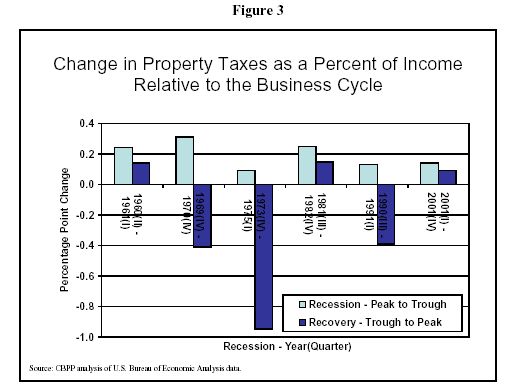

Increases in property taxes relative to income are common during and slightly after economic slowdowns, as illustrated in Figure 3. This is not surprising, since incomes tend to stagnate or decline during troubled economic times, while property values may remain stable or — as in the most recent downturn — continue to rise. During strong economic recoveries, property taxes have trended downward relative to income, generally canceling the increases that took place during weaker economic times. Even when property taxes have gone up between the end of an economic downturn and the peak of the following expansion, as in the 1960s and the 1980s, the rise has been modest compared to the declines in the previous period. For example, while property taxes increased somewhat in the 1980s’ economic expansion, the increase did not offset the sharp decline in the 1970s expansion. In the current period, the rise in property taxes thus far is much smaller than the decline in the 1990s recovery. If this historic trend holds in the future, we can expect that the recent recession-driven increase in property tax collections would moderate or even reverse course as the economic recovery gains strength.[2]

Several Factors Cause Changes in Property Tax Collections

One reason that property tax collections have risen recently is that the underlying values of residential and business property have risen. As a result, many local governments have been able to realize increased revenue from property taxes without raising rates.

High and rising property values in many parts of the country have kept property tax collections relatively strong. From 1999 to 2003, the median sales price of an existing single-family home in the U.S. increased 20 percent, while inflation-adjusted median household income fell by 3.6 percent from 1999 to 2003.[3] Falling income with rising property values can cause property tax collections as a share of national income to rise, even in the absence of any rate changes.

Rate increases, by contrast, appear to have played a relatively minor role in rising collections. Even as cities face increased but underfunded demands, the majority of cities are not raising property tax rates. For example, the National League of Cities noted recently that despite nearly 70 percent of cities reporting increased public safety spending in 2004, only 25 percent of cities increased property tax rates while 7 percent of cities decreased property tax rates in 2004.[4] The majority of cities left property tax rates unchanged in 2004.

Some critics assert that state and local policymakers should respond to increasing property values by reducing property tax rates more than they have, to offset the impact of increased property tax assessments on revenues. Many local governments have not been able to cut rates to compensate for increasing valuation, however, because over the last three years local governments have faced increased fiscal responsibilities and burdens as a result of state and federal actions.

Federal budget and tax actions have increased the fiscal pressure on states and localities through a variety of actions, including underfunding mandates. From fiscal year 2002 through fiscal year 2005, federal policies have cost states and localities more than $175 billion.[5]

- From fiscal year 2002 through fiscal year 2005 funding for the No Child Left Behind Act (NCLB) has been approximately $32 billion below the levels authorized in the Act. Many local governments have had to generate additional resources to meet this federal requirement.

- To put the recent rise of property tax collections into perspective, the total cost of Federal mandates from FY 2002 to FY 2005 was more than the increase in property tax collections from 2000 to 2004.[6]

The Federal government has also limited states and localities from raising adequate revenue through other types of taxes to pay for these rising costs, which has put upward pressure on the property tax. For example, the Federal government has not given states the power to collect sales taxes on items purchased on the Internet or through catalogs. By not allowing states to recoup revenue lost through catalog and on-line purchases, the Federal government has prevented the states and localities from collecting approximately $60 billion from fiscal year 2002 through fiscal year 2005. The Federal government also has preempted or made it difficult for states to maintain other revenue sources, through legislation such as the Internet Tax Freedom Act and the repeal of the estate tax.[7]

Moreover, state budget actions (which have resulted in part from federal actions and in part from states’ own-source revenue problems) have increased fiscal pressure on local governments by decreasing state aid for local governments, particularly for education funding.

- Between fiscal year 2002 and fiscal year 2004, localities in 35 states (accounting for 75 percent of total students) received a reduced amount of per student K-12 public school funding from their states, after adjustment for inflation.[8] In order to maintain funding in the face of declining state contributions and increasing federal demands, some of these local governments turned to greater reliance on property taxes to generate needed revenues. At best, school districts were in no position to lower property tax rates as incomes stagnated or declined during the downturn.

- Declines in general state aid to municipal governments also have caused significant fiscal stress. In a recent National League of Cities survey, 55 percent of responding cities reported that changes in state aid had a negative impact on their fiscal 2004 budgets.[9] From fiscal year 2003 to fiscal year 2004, 24 states reported reductions in aid to cities, amounting to a $2.3 billion decline (9.2 percent) in state aid.[10] The need to compensate for lost state aid is still another reason property tax rates could not be reduced during the fiscal crisis.

Overreacting to Property Tax Changes Could Reduce Public Services and Create Long-Term Inequities

The data presented above do not support claims of a current property tax crisis or notions that conditions similar to those of the late 1970s exist now. The recent uptick in property tax collections may tempt anti-tax interests, voter-initiative sponsors, and/or policymakers in some states into stoking voter resentment against property taxes, with the aim of sweeping cuts or caps on local property taxes. But the facts are at odds with the tax revolt rhetoric, since property tax collections as a share of income are well below levels in previous decades and since historical patterns suggest that property taxes are likely to decline again as the economic recovery gains strength.

Property taxes remain the single most significant source of revenue for most local governments, and therefore a crucial source of funding for local services like K-12 education, police, fire, and human services. If policymakers or sponsors of voter initiatives overreact to recent short-term changes in property tax levels by endorsing sweeping, permanent cuts in property taxes, the results are likely to be reductions in those services, increased burden in other taxes, or both.

There is some evidence that voters are well aware of the trade-offs between rigid property tax limitations and adequate public services. For instance, voters in Maine had the option on the November ballot to limit property taxes to one percent of assessed value and to limit increases in the future. Despite an initial lead in the polls, the ballot measure — Question 1 — failed by nearly a two-to-one margin. Facing losses of up to 40 percent in municipal and school district revenues if Question 1 had passed, Maine voters decided not to support a tax cap that would have decimated funding for local services.

The failed Question 1 in Maine was similar to California’s Proposition 13. Proposition 13, which froze property values and limited annual increases in assessments, passed in California at a time when the state could attempt to make up some of the several billion dollars lost in local revenue. In the current state fiscal environment — recovering from the worst fiscal crisis in 50 years — it is unlikely that any state could afford to make up such a large deficit in local revenue as would result from a Question 1-type cap.

In addition to damaging public services, blunt property tax caps create inequities for homeowners and may distort commercial development. A blanket property tax cap that uniformly limits the assessment ratio, constrains future increases in property tax liability, and allows for reassessment only when ownership changes — similar to the provisions of California’s Proposition 13 — will lead to similarly situated homeowners paying vastly different tax bills only because they bought their homes at different times. For example, the Santa Clara County assessor Larry Stone recently illustrated the inequities of Proposition 13 by pointing to different property tax bills for a house whose owners paid $90,000 in 1975 and an identical model in the same neighborhood purchased nearly 30 years later for $830,000. Property taxes were $1,600 for the home purchased in 1975 as compared to $8,300 for the home purchased in 2002. As Stone said, “now you have two houses, same builder, same year, same schools, same police, same fire, same street maintenance, yet one tax bill's much higher than the other.”[11]

Tax Relief Can be Targeted

Particular individuals and families with low incomes and high housing costs may face property tax bills that are higher than they can manage, despite the fact that property taxes on average are at historically low levels. It is possible to target property tax relief to those homeowners bearing the greatest burden. Property tax reform that takes into account a homeowner’s ability to pay, such as a so-called “property tax circuit breaker,” can better protect low-income homeowners from rising property taxes that accompany rising property values. Targeted property tax relief avoids sharp reductions in funding for locally provided public services and inequities based solely on date of purchase.

- A property tax circuit breaker prevents property taxes from “overloading” a taxpayer. Under a typical circuit breaker, the state sets a maximum percentage of income that an eligible family can be expected to pay in property taxes. If property taxes exceed this limit, the state then provides a rebate or credit to the taxpayer.

- Property tax circuit breakers do not reduce the local tax base, thus allowing for continued funding of local services, because they are state funded.

- Currently, of the 31 states and the District of Columbia with circuit breakers for homeowners, only six and the District of Columbia permit all households to participate in the program without regard to age. States could improve homeowner circuit breaker programs by expanding eligibility to all homeowners regardless of age.

There also are a variety of other property tax relief strategies that may be used to target property tax relief. These include homestead exemptions to exempt a certain amount of a home’s value from taxation, credits to rebate a certain percentage of taxes paid, and deferral programs to allow low-income elderly homeowners to defer payment of property taxes until property is sold.[12]

End Notes:

[1] Property tax data are from the U.S. Department of Commerce, Bureau of Economic Analysis and include property taxes paid by individuals and businesses. Because property tax data include collections from individuals and businesses, the national income data is the sum of all incomes, net of consumption of fixed capital. National income includes compensation of employees, proprietors’ income, rental income of persons, and corporate profits.

[2] Figure 3 shows property taxes relative to the national business cycle. While the national recession was over in 2001, the state fiscal crisis has lingered an unusually long time; about half of the states continue to face deficits for FY 2006. Thus from the point of view of states and localities, the downturn lingers.

[3] Home sales price data are from the National Association of Realtors. Household income data are from the U.S. Bureau of the Census.

[4] Michael A. Pagano, City Fiscal Conditions in 2004, National League of Cities, August 2004. By comparison, about the same percentage of cities reported raising property tax rates three years into the current recovery as raised rates three years into the 1990s recovery — 25 percent in 2004 versus 26 percent in 1994. Thus, at this point in the recovery rate increases appear no greater than in the 1990s recovery.

[5]

Iris J. Lav and Andrew Brecher,

Passing Down the Deficit: Federal

Policies Contribute to the Severity of the State Fiscal Crisis, Center

on Budget and Policy Priorities,

[6] Iris J. Lav and Andrew Brecher, Passing Down the Deficit: Federal Policies Contribute to the Severity of the State Fiscal Crisis.

[7] For more information on how Federal policies reduce state revenue, see Iris J. Lav and Andrew Brecher, Passing Down the Deficit: Federal Policies Contribute to the Severity of the State Fiscal Crisis

[8] Andrew Reschovsky, State Government Fiscal Crises and the Funding of Public Schools, University of Wisconsin-Madison, February 2004.

[9] Pagano, City Fiscal Conditions in 2004.

[10] Christopher W. Hoene and Michael A. Pagano, Fiscal Crisis Trickles Down as States Cut Aid to Cities, National League of Cities, September 2003.

[11] Larry Stone, quoted in “Proposition 13: Tax Revolt Turns 25,” http://www.metroforum.org/articles/item.php?id=10

[12] For additional details about circuit breakers see Liz McNichol and John Springer, State Policies to Assist Working-Poor Families, Center on Budget and Policy Priorities, December 2004. For information about a variety of property tax relief strategies, see National Conference of State Legislatures, A Guide to Property Taxes: Property Tax Relief, November 2002.