ESTATE TAX REFORM COULD RAISE MUCH-NEEDED REVENUE:

Some Reform Options With Low Tax Rates Raise Very Little Revenue

By

Joel Friedman and Ruth Carlitz

Summary

|

PDF of

full report Fact Sheet: HTM | PDF

Related Report: |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

Under current law, the estate tax will be repealed in 2010, and then will be reinstated in 2011. This strange sequence of events will occur because the tax cuts enacted in 2001, including those related to the estate tax, expire after 2010, restoring the law that was in effect prior to 2001. The Administration has called for making the repeal of the estate tax permanent after 2010. The Joint Committee on Taxation estimates that this would reduce revenues by $290 billion through 2015, including $72 billion in 2015 alone. But this estimate essentially captures only the cost of four additional years of estate tax repeal; the revenues losses associated with 10 more years of repeal — for the period 2012 through 2021 — are much higher, about $745 billion. And when the associated $225 billion in higher interest payments on the debt are taken into account, the total cost of repealing the estate tax for a decade would be nearly $1 trillion.

This high cost, at a time when the nation faces serious long-term budget problems, is making some in Congress reassess the feasibility of eliminating entirely this source of revenue. Yet a stalemate that permits the return of pre-2001 law, which set the estate tax exemption level at $1 million and the top tax rate at 55 percent, is viewed by most as undesirable as well.

This paper examines potential estate tax reform options between these two extremes — full repeal and the pre-2001 law — primarily by focusing on the effects of continuing the estate tax laws in place in either 2008 or 2009. In 2008, the exemption level will be $2 million for an individual ($4 million for a married couple); in 2009, it rises to $3.5 million for an individual ($7 million for a couple). In both years, the top estate tax rate will be 45 percent. The major findings of this analysis, which are based on estimates prepared by the Urban Institute-Brookings Institution Tax Policy Center, are as follows:

- Raising the exemption level by modest amounts significantly reduces the number of estates that would be subject to the estate tax. Compared with the number of estates subject to tax in 2011 under the $1 million exemption level set in current law, raising the exemption level to $2 million would reduce the number of taxable estates by 61 percent. Raising the exemption level to $3.5 million would reduce the number of taxable estates by 84 percent.

- At these higher exemption levels, very few small businesses and farms would be subject to the estate tax. With a $1 million exemption, there would be 760 taxable estates nationwide in 2011 in which a small farm or small business comprises a majority of the estate and thus creating the situation where the estate may have too few assets beyond the farm or business to pay the estate tax without selling some or all of the farm or business. With a $2 million exemption, there would be 210 estates in 2011 where a small farm or business represents more than half of the value of the estate. At a $3.5 million exemption level, there would only be 50 such estates in the nation, an average of one per state.

- While sharply reducing the number of estates subject to the estate tax, these higher exemption levels, with a 45 percent estate tax rate, would still yield a reasonable amount of revenue. Continuing repeal of the estate tax past 2010 would lose all estate tax revenue that would be collected under current law with a $1 million exemption and 55 percent top rate. In contrast, a $2 million exemption and a 45 percent rate would maintain 68 percent of the estate tax revenue that would be lost under repeal, and a $3.5 million exemption would maintain 44 percent of the revenue.

- In addition to preserving a significant portion of estate tax revenues, these reforms would improve the budget outlook in two other ways. First, because of interactions between the estate tax and the income tax, retaining a reformed estate tax prevents a substantial loss of income tax revenues that the Joint Committee on Taxation estimates will result when the estate tax is repealed (see box on page 7). Second, the cost of the added interest payments on the debt would be significantly less under a reform that maintained a reasonable level of estate tax revenues than under repeal of the tax, yielding further budget savings.

- The actual percentage of an estate paid to the federal government in estate taxes — known as the effective tax rate — is far less than the top rate of 45 percent. The effective tax rate is lower both because of the exemption of the first million or more dollars in assets and because of the deductions available for charitable bequests and for estate taxes paid to state governments. The Tax Policy Center estimates that, under a federal estate tax with a $2 million exemption and a 45 percent top rate, taxable estates would, on average, pay an effective tax rate of only 18 percent in 2011. Even very large estates valued at over $20 million would pay an average of 22 percent of the total value of the estate in federal estate tax, or less than half of the top 45 percent rate.

- Lowering the top estate tax rate from 45 percent to 15 percent would reduce the revenues raised under these two reform options by about two-thirds, while having almost no effect on the number of estates subject to the tax, including estates with small businesses and farms. Despite these relatively modest effective tax rates, some argue that a top tax rate of 45 percent is too high and suggest that the estate tax rate be reduced sharply to 15 percent, equal to the tax rate on capital gains income. With a $2 million exemption, dropping the top tax rate from 45 percent to 15 percent would result in the effective tax rate falling from an average of 18 percent to 6 percent. As a result, this option would maintain only about one-fifth of the revenue that would be lost under repeal. Setting the exemption at $3.5 million while lowering the rate to 15 percent would maintain only 13 percent of the revenue that would be lost under repeal — in other words, it would lose 87 percent of the revenue that would be foregone under repeal. Further, the vast majority of the benefits of lowering the rate from 45 percent to 15 percent would flow to the largest estates.

|

Table 1 |

||

|

How Much Estate Tax

Revenue Would |

||

|

If the top tax rate |

… and the exemption level were: |

… the share of estate tax revenue that would be preserved is: |

|

45% |

$2.0 million |

68 percent |

|

45% |

$3.5 million |

44 percent |

|

15% |

$2.0 million |

21 percent |

|

15% |

$3.5 million |

13 percent |

|

Source: Tax Policy Center |

||

- Some have called for both high exemptions and low rates. Such reforms raise virtually no revenue and are not materially different than repeal. A recent Wall Street Journal editorial suggested a potential reform that would tax estates at the capital gains rate and raise the exemption level to $10 million.[1] Such a reform would recover a mere 6 percent of the estate tax revenue lost under repeal — that is, it would lose 94 percent of the revenue that would be lost under repeal. Even setting the exemption level at $5 million, with a 15 percent rate, would lose 90 percent of the revenues lost under repeal.

The budget that the Administration has proposed, as well as the budget plans that Congress is considering, include significant cuts in a wide range of domestic programs. Supporters of these cuts argue that they are needed to address the nation’s long-term fiscal problems. While proposed cuts in education, health care, and environmental protection programs, among others, will affect a broad section of the American public, changes to the estate tax will affect only a small number of the most affluent people in the nation. These budgetary trade-offs are what have prompted some to question the affordability of repealing the estate tax.

These budget policy issues also deserve to be at the heart of any debate over estate tax reform. Reforms that rely on low tax rates have the same inherent problem as repeal of the estate tax: they result in a massive loss of revenue.

Number of Taxable Estates

The 2001 tax-cut law reduces the estate tax by increasing the amount of an estate that is exempt from taxation (the exemption level[2]) and by lowering the top tax rate applied to the taxable portion of the estate. In 2005, the exemption level is $1.5 million and the top rate is 47 percent. As Table 2 shows, the top tax rate declines to 45 percent and the exemption level rises to $2 million and then $3.5 million until, in 2010, the estate tax is repealed altogether[3]. (It is worth noting that when the estate tax is repealed, certain assets that appreciated in value during the decedent’s life may be subject to the capital gains tax when sold by heirs.[4]) At the end of 2010, all of the tax cuts enacted in 2001 expire, including the changes made to the estate tax. As a result, in 2011, the estate tax reverts back to the laws that were in place prior to enactment of the 2001 tax cut. Under that law, the estate tax exemption is set at $1 million and the top rate at 55 percent.[5]

|

Table 2 |

||

|

Estate Tax Rates and Exemptions |

||

|

|

Exemption Level |

Top Rate |

|

2005 |

$1.5 million |

47% |

|

2006 |

$2 million |

46% |

|

2007 |

$2 million |

45% |

|

2008 |

$2 million |

45% |

|

2009 |

$3.5 million |

45% |

|

2010 |

Repeal |

Repeal |

|

2011 |

$1 million |

55%* |

|

*For estates between $10 million and $17

million, a 5 percent surcharge applies in 2011. |

||

A stalemate in the policy process for addressing the estate tax thus will result in the estate tax reverting back to prior law. Even those who oppose repeal of the estate tax generally do not favor going back to the pre-2001 law, viewing the $1 million exemption as too low and the 55 percent top tax rate as too high. The Urban Institute-Brookings Institution Tax Policy Center has analyzed the impact of alternative estate tax policies in 2011. One option assumes a $2 million exemption (equal to the exemption level in place in 2006 through 2008). Another option involves a $3.5 million exemption (equal to the exemption level in place in 2009, the year before repeal). Both options assume a 45 percent top tax rate.

The Tax Policy Center analysis finds:

- Under the current law exemption of $1 million in 2011, 53,800 estates would be subject to the estate tax, representing about 2 percent of the 2.6 million people expected to die in that year. Of the 53,000 estates that would be taxable, nearly half — or 46 percent — would have assets of less than $2 million, and nearly three-quarters would be valued at less than $3.5 million.

- Raising the exemption level from $1 million to $2 million would shrink the number of taxable estates to 21,000, reducing by 61 percent the number of estates that would face the estate tax in 2011. In addition to eliminating the need for all estates worth $2 million or less to pay estate tax, it also would eliminate the tax on a significant number of estates worth more than $2 million. Some larger estates would have less than $1 million subject to the estate tax in 2011 once the $1 million exemption available under current law and other deductions are taken into account. Raising the exemption by $1 million (from $1 million to $2 million) also would exempt those estates from paying any estate tax.

- Raising the exemption to $3.5 million would further reduce the number of taxable estates in 2011 — to 8,500 — and thereby exempt from the estate tax 84 percent of the estates that would be taxable under the current-law exemption level of $1 million. These 8,500 taxable estates represent about 0.3 percent of all the persons who will die in 2011. In other words, the estates of 997 of any 1,000 people who die would be totally exempt from the tax.

|

Table 3 |

|||

|

Number of Taxable

Estates in 2011, |

|||

|

Size of Gross Estate |

Number of taxable estates when |

||

|

$1 million |

$2 million |

$3.5 million |

|

|

$1.0 - $2.0 million |

24,800 |

0 |

0 |

|

$2.0 - $3.5 million |

15,280 |

8,880 |

0 |

|

$3.5 - $5.0 million |

5,870 |

4,790 |

2,060 |

|

$5.0 - $10.0 million |

5,130 |

4,830 |

4,030 |

|

$10.0 - $20.0 million |

1,910 |

1,690 |

1,660 |

|

Over $20 million |

830 |

790 |

700 |

|

All taxable estates |

53,820 |

20,970 |

8,450 |

|

Taxable estates as percent of all deaths |

2.0% |

0.8% |

0.3% |

| Source: Tax Policy Center | |||

Higher Exemption Relieves Virtually All Small Businesses and Farms from Estate Tax

Relatively few small businesses and farms face the estate tax. The Tax Policy Center data identify those estates in which farm and business assets represent a majority of the assets. Because the majority of the assets of these estates are in a farm or business, these are the only estates that might face the prospect of having to liquidate the farm or business to pay estate taxes. In estates where the farm or business represents a minority of the estate, other assets in the estate generally can be used to pay the estate tax and thereby protect the business from liquidation.

The Tax Policy Center uses a definition for small businesses and farms that includes all businesses and farms with assets worth up to $5 million. Under this definition, the Tax Policy Center estimates that under current law in 2011 — that is, with a $1 million exemption and a 55 percent top rate — there would be 760 taxable estates that year in which a small farm or business comprises a majority of the estate. With a $2 million exemption, there would be only 210 estates nationally where a small farm or business represented more than half of the value of the estate.

With a $3.5 million exemption, only 50 taxable estates in the country in 2011 would have small business or farm assets that represent a majority of the estate. This amounts to less than 1 percent of all taxable estates in that year, and less than three-one-thousandths of all deaths in the nation. In other words, only two of every 100,000 people who die in 2011 would have estates that would be subject to any estate tax and in which small business or farm assets would comprise the majority of the estate. [6]

Estate Tax Revenues

The Joint Committee on Taxation estimates that making permanent the repeal of the estate tax after 2010, rather than reverting back to pre-2001 law as current law would entail, would cost $290 billion through 2015. Because the estate tax is not due until at least nine months after a person dies, most of the cost of repealing the estate in 2011 only shows up in the 2012 estimates. As explained in more detail in the box on page 7, the Joint Tax Committee estimates that the revenue lost in 2012 from repeal of the estate tax is $55 billion. This exceeds the $43 billion estimate of the amount of estate and gift tax revenues expected to collected that year under current law (that is, under an estate tax with a $1 million exemption and 55 percent top rate). The additional $12 billion of lost revenue reflects a reduction in income tax revenues that the Joint Tax Committee estimates would result primarily because taxpayers would sell fewer appreciated assets — and thereby pay less in capital gains tax — in response to repeal of the estate tax.

The Tax Policy Center is not able to model the behavioral effects reflected in the Joint Committee on Taxation estimates. As a result, the Tax Policy Center estimates only the static impact of changes in estate tax policy on estate tax revenues, excluding any effects of policy changes on income taxes or gift taxes.

- The Tax Policy Center estimates that the laws in place in calendar year 2011 — a $1 million exemption and a 55 percent top rate — would yield estate tax revenues of $39 billion.

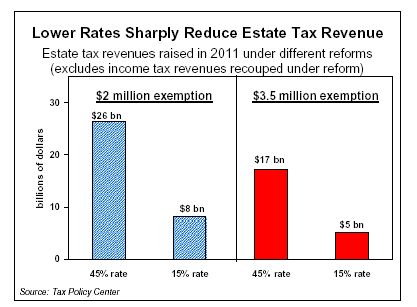

- If the estate tax exemption were set at $2 million and the top rate at 45 percent (consistent with the law that will be in place in 2007 and 2008), the Tax Policy Center estimates that the estate tax would collect $26 billion in estate tax revenue in 2011. That is, this reform option would retain 68 percent of the revenue that would be lost if the estate tax were repealed.

- As noted in the previous section, increasing the exemption eliminates all estate tax for 61 percent of the estates that will be subject to the tax in 2011 under current law. Therefore, while it would eliminate the tax on three-fifths of the estates that would otherwise owe it, this option would retain 68 percent of the revenue that would be foregone under repeal (see Table 4).

|

Impact of Estate Tax Repeal on Income Tax Revenues The Joint Committee on Taxation estimates that extending the repeal of the estate tax beyond its scheduled expiration at the end of calendar 2010 would reduce revenues by $290 billion between fiscal years 2006 and 2015. The bulk of the revenue loss over that ten-year period would occur after fiscal 2011, because estate taxes do not have to be paid until at least nine months after the death of a decedent. Over the four years from fiscal 2012 through fiscal 2015, the Joint Tax Committee estimates that the total revenue loss would be $252 billion (see table below). Over that same period, the estimate of the estate and gift tax revenue that would be collected under current law (with a $1 million exemption level and 55 percent top rate) is only $198 billion.* Thus, repeal of the estate tax (and associated changes to the gift tax) would reduce revenues by more than the total amount of estate and gift taxes projected to be collected under current law. The additional $54 billion of lost revenue, accounting for about 20 percent of the total revenue loss, reflects a reduction in income tax receipts. The Joint Tax Committee has not issued a detailed technical explanation of these income-tax losses, but the largest component of the losses is understood to reflect a fall-off in capital gains receipts. Economic research has shown that the estate tax has the effect of reducing the “lock-in effect” with respect to assets that have increased in value. (The “lock-in effect” refers to the propensity of many taxpayers to hold rather than sell assets that have increased in value; only when appreciated assets are sold do they generate capital gains revenues.) Repeal of the estate tax is believed to increase the “lock-in effect,” with the result that fewer assets would be sold and less capital gains tax would be collected. It is these lower capital gains revenues that account for much of the additional income tax revenue that will be lost when the estate tax is repealed.

______________ *Note that the Congressional Budget Office prepares the projections of revenue collected under current law, while the Joint Committee on Taxation estimates the cost of different tax proposals. They both rely on a common set of economic and technical assumptions. |

||||||||||||||||||||||||||||||

- If the exemption were set at $3.5 million and the top rate at 45 percent (consistent with the 2009 law), the total estate tax revenue raised would be $17 billion in 2011, according to Tax Policy Center. Even at this higher exemption level, which would exempt 84 percent of taxable estates from the estate tax in 2011, 44 percent of the revenue that would be lost under repeal would be preserved.

The Tax Policy Center estimates that the amount of revenue a particular reform option would maintain in 2011 (relative to repeal) would hold over time. The option consisting of a $2 million exemption and a 45 percent rate thus would recover 68 percent of the estate tax revenue that would be lost under repeal both in 2011 and in succeeding years. As a result, this reform option would have a significantly smaller impact on the deficit than repeal. It also would result in lower interest payments on the debt than would occur under repeal.

|

Table 4 |

||||

|

Impact of Reform Options

on the Number of Taxable Estates |

||||

|

Exemption level |

$1 million |

$2 million |

$3.5 million |

Repeal |

|

Top estate tax rate |

55 percent |

45 percent |

45 percent |

|

|

Percent change in number of taxable estates |

0% |

-61% |

-84% |

-100% |

|

Percent of current law revenues preserved |

100% |

68% |

44% |

0% |

|

Source: Tax Policy Center |

|

|

|

|

Reform Options With A Lower Tax Rate Lose Substantial Revenue

Some argue that the tax rates imposed on estates under these reform options are too high. They mistakenly believe that about half of someone’s estate goes to the government when the individual dies. As noted, not only do a very small percentage of people who die each year face any estate tax at all, but even with top estate tax rates of close to 50 percent, those estates that do face the estate tax pay a much smaller percentage of the estate in tax — typically closer to one-fifth than one-half. This is because of the availability of various deductions (see box on page 9).

Nevertheless, some have called for reducing the top estate tax rate to 15 percent, setting it equal to the top capital gains rate. Such a change would have a dramatic impact on the amount of revenue that the estate tax could raise. Compared with a 45 percent rate, a 15 percent rate would raise only about one-third the revenue, according to Tax Policy Center estimates. Yet unlike raising the exemption level, lowering the rate has almost no effect on the number of estates subject to the estate tax, including the number of estates with small business and farm assets.[7]

Tax Policy Center data show that:

- With a $2 million exemption, moving from a 45 percent rate to a 15 percent rate would reduce estate tax revenues by two-thirds, from $26 billion in 2011 to $8 billion. With a 15 percent rate, an estate tax with a $2 million exemption would retain only one-fifth of the revenue that would be lost under repeal; four-fifths of the revenue would still be lost.

- With a $3.5 million exemption, moving from a 45 percent rate to a 15 percent rate would reduce the estate tax revenue raised from $17 billion in 2011 to $5 billion. This option would preserve only 13 percent of the revenue lost under repeal; 87 percent of the lost revenue would still be forgone.

|

Effective Estate Tax Rates Are Much Lower than the Top Rate Prior to 2001, the top estate tax rate was 55 percent. This rate led some to conclude that when someone dies, half of their estate goes to the government, fueling the portrayal of the estate tax as a “confiscatory” tax. However, given the availability of a sizeable up-front deduction for all estates, as well as allowable deductions for charitable bequests and estate taxes paid to states, combined with estate planning strategies, taxpayers have the opportunity to shield a large share of their estates from taxation. As a result, the actual proportion of an estate that goes to pay the estate tax — the effective rate of taxation — is significantly less than the top tax rate. The most recent estate tax return data from the Internal Revenue Service show that in 2003, taxable estates faced an average effective tax rate of only 18.8 percent. Estates in the $5 million to $10 million range faced the highest effective tax rates — about 29 percent. The largest taxable estates, those worth over $20 million, had an effective rate of 16.5 percent, primarily because of the size of their charitable bequests. These 2003 data primarily reflect estate tax paid under the 2002 law (because of the nine month lag in the payment of estate taxes), which set the exemption level at $1 million and the top rate at 50 percent. The following example illustrates how exemptions and deductions lower marginal rates. Consider an estate tax with a $2 million exemption and a top rate of 45 percent in 2011, as shown in Table 5. Now, consider the case of a $7 million taxable estate. First, the exemption amount is subtracted from the value of the gross estate, which reduces the taxable estate to $5 million. Next, estates are permitted to deduct any estate taxes paid at the state level; for a $7 million estate, state taxes would typically amount to about $635,000.* Further, such large estates generally leave a portion to charity. The average charitable contribution for estates of this size, plus other smaller deductions and credits, are estimated to total about $1.1 million in 2011. All of these deductions together reduce the taxable estate to $3.3 million. Applying the 45 percent rate to this amount yields a tax liability of $1.5 million. The effective tax rate is thus 21 percent ($1.5 million divided by $7 million), or less than half the 45 percent top rate.

_________________ *Starting in 2006, state estate taxes are treated as a deduction. Prior to 2006, a credit was provided, based on a schedule in the federal code. Many states use this schedule to determine their estate taxes, so we used it to estimate the deduction in the example above. |

||||||||||||||||||||||

- The Tax Policy Center estimates that at even higher exemption levels, a 15 percent rate yields only tiny amounts of revenue. An estate tax with a $5 million exemption and a 15 percent rate would lose 90 percent of the revenue that would be lost with repeal. With a $10 million exemption and a 15 percent rate, 94 percent of the revenue would be lost.

- Further, none of these revenue estimates take into account the additional revenue losses from tax-avoidance schemes that may result at such low rates. Leonard Burman, a co-director of the Tax Policy Center and a senior fellow at the Urban Institute, has warned that dropping the estate tax rate to 15 percent “would invite unproductive tax shelter schemes, much as the differential between tax rates on capital gains and ordinary income does under the regular income tax.”[8]

A clear indication of the impact of a 15 percent rate on estate tax revenues can be seen when one compares the effective tax rates under a 45 percent rate and a 15 percent rate. As noted, the effective rate is considerably lower than the top rate, given the availability of certain deductions.

- The two-thirds drop in the top rate from 45 percent to 15 percent shows up in a drop in the effective rate, which falls from 18 percent to 6 percent, assuming a $2 million exemption (see Table 5).

- Even for the largest estates, those with assets in excess of $20 million, the average effective rate would be only 7 percent.

These low effective tax rates are an indication of how little revenue an estate tax with a 15 percent rate would generate.

Finally, it is important to point out that the benefits of going to lower estate tax rates flow primarily to the largest estates. Raising the exemption by itself provides a benefit that is essentially capped — for example, with a 45 percent tax rate, increasing the exemption by $1 million yields a maximum tax reduction of $450,000 ($1 million x 45 percent). As a result, raising the exemption level confers fairly equal benefits upon all estates. Indeed, nearly 60 percent of the benefit of raising the exemption from $1 million to $2 million (and lowering the rate from 55 percent to 45 percent) would flow to the three-quarters of estates worth less than $3.5 million.

In contrast, a reduction in the tax rate would provide a benefit proportional to the amount of estate tax being paid. The wealthiest estates that pay the most in estate tax would receive the largest benefits. Thus, if the estate tax rate were reduced from 45 percent to 15 percent (with a $2 million exemption), the 4 percent of taxable estates worth over $20 million would receive 36 percent of the benefits, saving these very large estates about $8 million apiece. Some 55 percent of the benefit would go to the 12 percent of estates worth over $10 million. More than 80 percent of the benefit would flow to the 35 percent of estates worth over $5 million.

Estate Tax Reform Needed to Address Long-Term Fiscal Issues

The cost of extending the repeal of the estate tax past its scheduled expiration at the end of 2010 is very high. Ten more years of repeal would reduce revenues by about $745 billion.[9] In addition, these lower revenues would increase the deficit and add to the debt, requiring higher interest payments of about $225 billion over the decade. Thus, the total cost of repealing the estate for another 10 years is nearly $1 trillion.

This high cost is raising questions among policymakers about whether complete repeal of the estate tax is affordable. Indeed, the fate of the estate tax is being considered at a time when the President and Congress are proposing significant cuts in a wide range of domestic programs. These cuts are being promoted because the nation faces daunting long-term fiscal problems. The tradeoffs in the budget that the Administration has proposed and in the budgets that Congress is now considering are clear — while the cuts in domestic programs affecting education, health care, environmental protection, and a number of other programs will affect a broad section of the American public, changes to the estate tax will affect only a small number of the nation’s most affluent families.

Although it is a positive step that some are beginning to question whether complete repeal of the estate tax is affordable, some of the “compromise” proposals to retain the estate tax also would lose massive amounts of revenue, with the result that the nation’s fiscal condition would be little better than under repeal. This is particularly true of reforms that advocate a 15 percent estate tax rate.

Proponents of using a 15 percent rate for the estate tax typically argue that this low rate is appropriate, given that a significant percentage of large estates reflects appreciated assets that have never been taxed (known as “unrealized capital gains”). On the one hand, this argument acknowledges the role that the estate tax plays as a backstop to the income tax, taxing income that that was not taxed during a decedent’s lifetime. On the other hand, this focus on the capital gains tax rate as the appropriate level for setting the estate tax rate misses the larger context in which this debate is occurring and the need to generate an adequate level of estate tax revenues. Dropping the estate tax rate from 45 percent to 15 percent reduces the revenues collected under the estate tax by about two-thirds. Moreover, a majority of the tax benefits of lowering the rate to 15 percent would flow to estates valued at more than $10 million.

The impact on the budget of setting the estate tax rate at 15 percent rather than 45 percent would grow over time. Over first ten years that repeal is extended, the loss would amount to more than $330 billion (assuming a $2 million exemption) in foregone estate tax revenues and increased interest payments.

|

Table 5 |

||

|

Effective Estate Tax

Rates |

||

|

Size of Gross Estate |

$2 million exemption in 2011, with top rate of: |

|

|

45 percent |

15 percent |

|

|

$2.0 - $3.5 million |

8.6% |

2.9% |

|

$3.5 - $5.0 million |

14.4% |

4.8% |

|

$5.0 - $10.0 million |

20.9% |

6.8% |

|

$10.0 - $20.0 million |

21.6% |

6.6% |

|

Over $20 million |

21.9% |

6.9% |

|

Average, all taxable estates |

18.3% |

5.9% |

|

Source: Tax Policy Center |

||

Finally, the argument on behalf of the 15 percent rate ignores the fact that under a 45 percent rate, and with a $2 million exemption, the effective tax rate for all taxable estates would average only about 18 percent in 2011, according to Tax Policy Center estimates. These effective estate tax rates are not very different than the capital gains rate.

Dropping the top estate tax rate to 15 percent, however, would lower the average effective tax rate to only 6 percent with a $2 million exemption. Even estates valued over $20 million would pay only 7 percent of the value of their estates in estate taxes.

Conclusion

New estimates from the Urban-Brookings Tax Policy Center show it is possible to design an estate tax that relieves large numbers of estates from paying the estate tax, while at the same time continuing to generate much needed revenues that would be lost under repeal. A key to these reform options is retaining the estate tax rate at a reasonable level, such as 45 percent (consistent with the top rate in 2007 through 2009, under current law). Lower rates, such as 15 percent rate, would dramatically shrink estate tax revenues. In addition, the benefits of lower rates would be concentrated among the largest estates.

End Notes:

[1] “Not So Permanent,” Wall Street Journal, February 11, 2005

[2] Technically, the exemption is calculated as a credit. See Nonna A. Noto, "Calculating Estate Tax Liability During The Estate Tax Phasedown Period, 2001-2009, "Congressional Research Service, RL31092, August 31, 2001.

[3] Note that between 2005 and 2009, the estate tax is essentially a flat tax levied at the top tax rate on the taxable portion of the estate. The estate tax technically has a graduated rate structure, but the high level of the exemption in these years cancels out the effects of the lower rates.

[4] See John Buckley, “Estate Tax Repeal: More Losers Than Winners,” Tax Notes, February 14, 2005.

[5] In addition to the rate and exemption level, the 2001 tax-cut package also changed other aspects of estate and gift taxation. These are not discussed here, but they also revert back to the pre-2001 law, starting in 2011.

[6] Even when estates with larger businesses and farms — those valued over $5 million — are included, the number of estates that would face the estate tax would remain very small. Assuming a $2 million exemption level, there would be 390 taxable estates in the nation where business or farm assets, no matter the size, represented more than half of the estate’s value; with a $3.5 million exemption, there would be 220 such estates.

[7] Some estates that receive credits for gift taxes that have been previously paid would have their estate tax liability eliminated under the 15 percent rate.

[8] Leonard Burman, William Gale, and Jeffrey Rohaly, “Options to Reform The Estate Tax,” Urban-Brookings Tax Policy Center, forthcoming.

[9] This ten-year estimate uses the Joint Committee on Taxation estimates of repeal for fiscal 2012 through 2015, and then holds the 2015 cost of repeal ($72 billion) constant as a share of the economy over the next six years. In constant 2006 dollars, this ten-year revenue loss would be $589 billion (or $763 billion with interest).