FISCAL CRISIS IS SHRINKING STATE BUDGETS

By

Elizabeth C.

McNichol

|

PDF of full report |

|

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

States faced gaps of more than $150 billion in their combined fiscal year 2003 and 2004 budgets. Since all states but one are required by constitution or law to balance their budgets, they have taken a variety of actions to close these gaps. In the process, states have cut spending dramatically. The continuing state fiscal crisis is causing state government to shrink and is putting important state services at risk.

States Cut Their Budgets

In December, the National Association of State Budget Officers released their annual report on general fund spending for the 2002 and 2003 fiscal years and appropriations for fiscal year 2004. The Center analyzed this information and found:

-

Nominal state spending increased by just 0.6 percent from fiscal year 2002 to fiscal year 2003. State spending is budgeted to grow by 2.0 percent – in fiscal year 2004.

-

When adjusted for population and inflation to reflect better the ability of states to continue to provide services to its residents, state spending declined by 2.6 percent from 2002 to 2003, and is budgeted to decline by 0.7 percent in fiscal year 2004. (See box for discussion of population and inflation adjustment.)

-

In over two-thirds of the states — 34 states — per person spending declined between fiscal year 2002 and fiscal year 2004 after adjusting for inflation.

-

These recent declines are part of a trend that began in fiscal year 2002 when the effects of the economic downturn first hit state revenue collections. State spending adjusted for inflation and population growth is estimated to be 5.4 percent lower in fiscal year 2004 than in 2001.

- As a result, significantly more resources than states budgeted — an additional $25 billion in 2003 and $30 billion in 2004 — would have been required to maintain state spending at the same level as 2001 after adjusting for inflation and increases in population. An even larger amount of resources would have been required in fiscal year 2004 — $73 billion — if state spending had grown at an average rate between fiscal year 2001 and fiscal year 2004.

- State employment has been declining. State employment was lower in each month of 2003 than in the corresponding month of the previous year.

- Spending has declined because tax revenues have declined. State and local taxes as a percent of Gross Domestic Product are at their lowest levels since the late 1980s.

Figure 1

This decline in spending is particularly problematic in the current economic climate. Many state programs are designed to be counter-cyclical: their costs rise during economic downturns as they assist families that have lost jobs or income. States also are facing higher costs at this time for fulfilling federal policies and mandates, such as costs for homeland security and for implementing the No Child Left Behind policies. Most states have not been able to come up with enough resources to maintain existing programs at pre-recession levels, much less to meet their expanded responsibilities.

|

Adjusting State Spending For Population and Inflation While state spending changes from year to year often are compared using nominal dollars, such comparisons do not accurately measure the ability of states to continue providing their current level of services. That ability is steadily eroded both by inflation (which increases the number of dollars needed to provide a given service to a given individual) and by population growth. Population growth — especially growth in specific expensive-to-serve populations such as school-age children and the elderly — increases the number of individuals who are eligible for programs and services or who otherwise must be served. Thus, the appropriate measure of changes in state spending is one that assesses whether a given state can continue to provide existing services. The simplest way to look at the buying power of state dollars is to adjust spending for overall inflation and total population changes, as has been done in this report. It also is conceptually possible but difficult in practice to adjust more precisely for buying power by using specific inflation rates — for expenditures such as healthcare, since a large proportion of state spending goes for health care and health care inflation has been much more rapid than general inflation — or to adjust for growth in specific population segments relative to the services that must be provided to those population groups. The population-plus-inflation adjustment used in this paper, therefore, should be considered only a partial adjustment for the true cost of providing a constant level of public services. |

State Budget Cuts

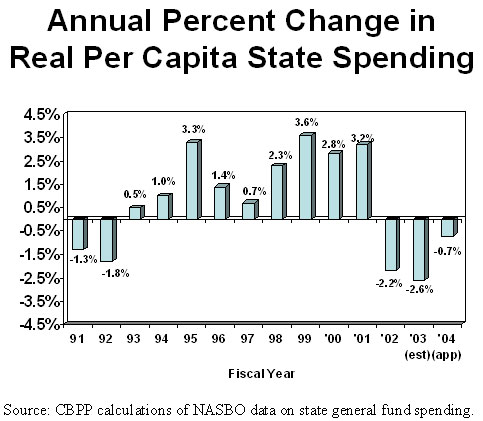

Figure 1 shows that state spending began to decline in real terms in fiscal year 2002 when the effect of the recession on state revenue first was felt. Spending declined further in the most recent fiscal years. For fiscal year 2003, state spending declined by 2.6 percent after adjusting for population and inflation. Based on adopted budgets, state spending is continuing to decline in the 2004 fiscal year — by 0.7 percent.[1]

Significantly more resources than states budgeted would have been required to maintain state spending at the same level as 2001 after adjusting for inflation and increases in population. State spending per person equaled $1,789 in 2001. After adjusting for inflation, state spending per person dropped 2.2 percent in 2002. As noted above, spending per person also declined in 2003 and in 2004. State spending in 2003 was $25 billion below the level needed to maintain real per capita spending at the 2001 level. Appropriations for 2004 are $30 billion below the amount that would be required to maintain the 2001 spending level after adjusting for inflation and population changes.

In addition, as noted in the box above, state spending generally increases more than population and inflation combined. (This is the result of the specific cost pressures states face as well as public demand for services.) The amount that states have budgeted for fiscal year 2004 is $73 billion less than the amount that would be required if state spending had grown at an average rate between fiscal years 2001 and 2004.

Figure 2

| Notes: The General Fund spending figures reported by NASBO for California, Minnesota, Oregon, Pennsylvania and Taxes were adjusted to reflect more recent information. California – See box. Minnesota – Close to $1 billion of the difference in fiscal year 2002 and 2003 expenditures relate to the state takeover of local property taxes for education. While this is new general fund spending for the state, it does not represent an overall increase in resources for education. Oregon – Oregon budgets on a biennial basis. The figures used for individual fiscal year spending were estimated by the legislative and executive budget offices. |

State budget cuts have been widespread. Some 34 states have adopted cuts that are causing low-income families to lose health insurance. Most of the cuts have affected children and parents in families in which the parents work at low-wage jobs. For example, Texas will end coverage under the Children's Health Insurance Program for nearly 160,000 children in working families, and Connecticut reduced Medicaid eligibility for parents with incomes from 100 to 150 percent of poverty, with about 20,500 parents affected. Six states — Alabama, Colorado, Florida, Maryland, Montana and Utah — have stopped enrolling eligible children in their State Children’s Health Insurance Program (SCHIP.) New or higher copayments for public health insurance services were imposed by 21 states for fiscal year 2004; the previous year 17 states added or increased copayments. Research has shown that copayments are a significant deterrent to the use of essential medical care and prescription drugs among low-income populations, and that there are adverse health consequences when such treatment is foregone or delayed.

Figure 3

Since January 2001, some 23 states have made policy changes that reduce the availability of child care subsidies for low-income working families. In about half the states, low-income families who are eligible for and need child care assistance are either not allowed to apply or are placed on a waiting list. As of December 2003, there were some 47,000 children on the child care waiting list in Florida. Tennessee no longer even accepts child care applications from families that do not receive TANF cash assistance. In many cases, a child care subsidy is necessary to make it possible for a parent to work.

While states usually show great reluctance to cut K-12 education, 11 states made cuts for fiscal year 2004, following 9 that did so the previous year. In 34 states, real per-pupil aid to school districts has declined since 2002; in 19 states the decline exceeds 5 percent. This has resulted in imposition of new or higher fees for textbooks and courses, shorter school days, reduced personnel, reduced transportation, and a variety of other types of cutbacks. And states throughout the country are cutting higher education, leading to double digit increases in public college and university tuition and significantly reduced course offerings, creating barriers to a higher education for low- and moderate-income families.

Overall, state spending, adjusted for inflation and population growth, is estimated to be 5.4 percent lower in fiscal year 2004 than in 2001.

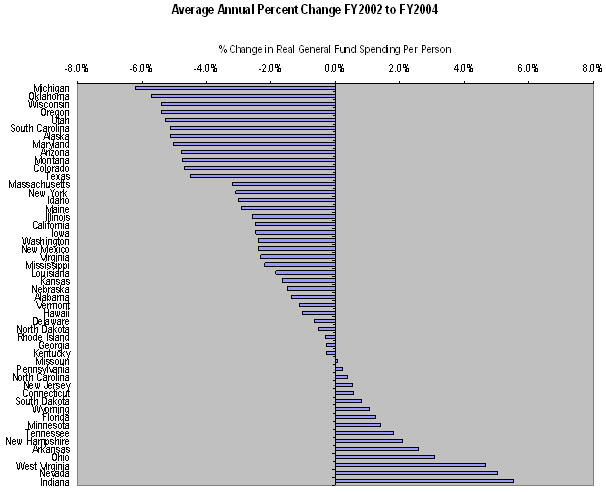

Figure 2 shows changes in real per capita spending by state from fiscal year 2002 to fiscal year 2004. It shows that spending increased in less than one-third of the states. The largest declines in spending were in Michigan, Oklahoma, Wisconsin, Oregon, Utah, South Carolina, Alaska, Maryland, Arizona and Montana. (See Appendix Table 1 for state-by-state data.)

In over two-thirds of the states — 34 states — per person spending declined between fiscal year 2002 and fiscal year 2004 after adjusting for inflation. In 17 of those states, nominal spending for 2004 was less than the amount spent two years earlier in 2002.

State Taxes are Declining

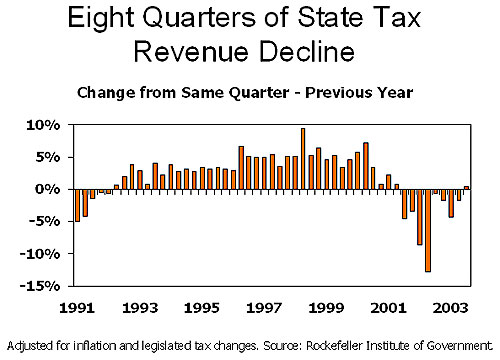

State budgets are shrinking because state tax collections were hard hit by the economic downturn. State tax revenues declined relative to the same quarter of the prior year for eight straight quarters — more than two complete fiscal years — according to data collected from state revenue departments by the Rockefeller Institute of Government adjusted for inflation and tax law changes. (See Figure 3.) In real per capita terms, state tax revenue remains far below the levels of 2001.

One reason for the revenue decline is the economic downturn. The sales tax and the income tax are the main sources of state tax revenue. The job losses of the recession and continued weak economy resulted in reduced incomes for families and reduced spending which, in turn, depressed sales tax collections. The decline in incomes had a direct effect on state income tax collections. In addition, most states tax the realization of capital gains and the decline in income tax revenues was particularly pronounced because of the dramatic stock market decline that accompanied the recession.

Another reason for the revenue decline is the ongoing erosion of state tax bases. Sales tax collections make up about one-third of state tax revenues. Most states mainly tax the consumption of goods, not services. Sales tax collections have lagged economic growth as untaxed services have become an increasing portion of overall economic activity.

The tax cuts of the 1990s also played a role in reducing state revenues. Despite the fact that the surge in revenues in the 1990s was temporary, many states enacted permanent tax cuts with the resulting surpluses. As a result, state revenues have not been sufficient to sustain services now that the economy has slowed. Since 2001, some 29 states have responded by raising taxes, but these tax increases have not been sufficient to offset the earlier cuts.

State and local tax revenues as a share of Gross Domestic Product are at their lowest levels since the late 1980s. In 2002 and 2003, state and local taxes were about 8.8 percent of GDP — or roughly three-tenths of a percentage point lower than the level of taxes in the economic downtown of the early 1990s. (Three-tenths of one percent of GDP equals about $32 billion.)

State Employment is Declining

During the 1970s and 1980s, state employment grew somewhat as a share of total employment. In part this was in response to a shift in certain responsibilities from the federal to the state levels. In addition, the public demand for services provided by states grew. State higher education expanded; more prisons were built; and the number of health care employees grew.

This trend ended in the 1990s when state employment declined relative to private employment. More recently, as their budgets are squeezed, states have laid off workers or chosen not to fill vacant positions. As a result of recent actions as well as slow growth during the 1990s, state employment is at a 30 year low.

- For the period from July 2002 to June 2003 — fiscal year 2003 for most states — state employment as a share of total employment equaled 3.8 percent — the same percentage as in fiscal year 1973.

- At the onset of the economic downturn, state employment continued to grow slowly while private sector employment declined. More recent data, however, show declining state employment. State employment was lower in each month of 2003 than in the corresponding month of 2002.

Conclusion

The current fiscal crisis is a revenue crisis, for which even states with the most well-stocked reserve funds were unprepared. Because of the magnitude of the crisis and the reluctance of many states to raise taxes, states are being forced to close their budget shortfalls through significant spending cuts. These cuts risk harming vulnerable populations such as poor, elderly and disabled individuals. They also put in jeopardy the investments states made in education, health care and law enforcement during the 1990s.

|

Methodology The state spending data in this paper were published by the National Association of State Budget Officers in the December 2004 Fiscal Survey of the states — the most recent edition. The information presented is on general fund spending. All states maintain other funds in addition to the general fund. The other funds are used to account for spending from specific revenue sources such as federal funds or tobacco settlement revenues, or to account for spending on specific purposes such as state employee pensions or transportation projects that are supported by dedicated taxes or bonds. State general fund spending makes up about half of total state spending on average. Trends in general fund spending are particularly important to tracking and understanding state finances for a number of reasons. • In the typical state major non-dedicated taxes such as income and sales taxes are deposited in the state’s general fund. • The general fund is usually used to finance the state’s share of health programs, grants to local government for education and other purposes, the costs of higher education and the costs of other government services common to most states. By contrast, special funds tend to have dedicated revenue sources that must be spent for narrowly defined purposes. • The general fund is the part of a state’s budget over which policymakers have the most discretion. It also is the part of the budget to which balanced budget requirements usually apply. • Current information is more readily available on general fund spending than on spending from all state funds. • Moreover, while general fund spending comprises only a portion of all state spending, historical studies show that changes in general fund spending over time follow very similar patterns to trends in spending from all funds.* Occasionally, a state will put revenues or expenditures in a special fund that more appropriately belong in the general fund. For example, New Jersey places its income tax collections in a fund that is used for aid to local governments. Both this revenue source and spending would be in the general fund in most states. In most cases, if the state treats this type of special fund as an add-on to the general fund in its budget deliberations and published budget documents, we and the other two organizations that track general fund spending — the National Conference of State Legislatures and the National Association of State Budget Officers — treat the sum of spending from these funds and the general fund as general fund spending. Other situations where a special fund exists that should be part of the general fund are not sufficiently frequent or large as to suggest that analysis of general fund spending trends materially distorts the picture of state spending. Spending figures were adjusted for inflation using the CPI-U index. The Congressional Budget Office inflation projections were used for 2004. Population figures are from the Census Bureau. *See, for example, Sources of Data About State Government Revenues and Expenditures, David Merriman, Urban Institute, 2000; “Receipts and Expenditures of State Governments and Local Governments,” 1959-2001; Survey of Current Business, Bureau of Economic Analysis, June 2003. |

Appendix

State General Fund Spending

End Notes:

[1] See box on page 5.