THE DECLINE OF CORPORATE INCOME

TAX REVENUES

By

Joel Friedman

Summary

| PDF of

this report HTML of fact sheet PDF of fact sheet |

| If you cannot access the files through the links, right-click on the underlined text, click "Save Link As," download to your directory, and open the document in Adobe Acrobat Reader. |

A weak economy, new tax breaks, and aggressive tax sheltering have pushed corporate income tax receipts down to historically low levels, both relative to the size of the economy and as a share of total federal revenues. According to the most recent budget projections of the Congressional Budget Office, corporate revenues will remain at historically low levels even after the economy recovers, and even if the large new corporate tax breaks enacted in 2002 and 2003 are allowed to expire on schedule.

Deficits over the next decade are now projected to be enormous in size. A joint analysis by the Center on Budget and Policy Priorities, the Concord Coalition, and the Committee for Economic Development projects deficits totaling $5 trillion through 2013. An analysis by Brookings economists reaches a very similar conclusion, while Goldman Sachs projects deficits totaling $5.5 trillion.[1] Despite the deteriorating fiscal outlook and the historically low corporate revenue collections we already face, Congress nonetheless seems poised to shower more tax breaks on corporations that would cause deficits to grow substantially larger over time (see box).

- Treasury Department figures show that actual corporate income tax revenues fell to $132 billion in 2003, down 36 percent from $207 billion in 2000.

- As a result of these low levels, corporate revenues in 2003 represented only 1.2 percent of the Gross Domestic Product (the basic measure of the size of the economy), the lowest level since 1983, the year in which corporate receipts plummeted to levels last seen in the 1930s.

- Corporate revenues represented only 7.4 percent of all federal tax receipts in 2003. With the exception of 1983, this represents the lowest level on record (these data go back to 1934).

|

Corporate Tax Cuts on the Congressional Agenda

Pressure to cut taxes for corporations is likely to intensify this fall as

Congress takes action to comply with a recent ruling by the World Trade

Organization that tax subsidies provided to

Repealing these export subsidies would raise about $50 billion in revenues over ten years, which creates an opportunity for supporters of corporate tax cuts to push for at least that much in new corporate tax breaks. Indeed, both the measure that the Senate Finance Committee adopted on October 1 (S. 1637) and the measure introduced by House Ways and Means Chairman Bill Thomas (H.R. 2896) would provide significantly more than $50 billion in new tax cuts to corporations. The Thomas bill would provide corporate tax breaks totaling $200 billion over ten years while offering revenue-raising offsets of only $72 billion. As a result, the package would cost $128 billion over the decade. Moreover, the measure includes a number of tax cuts that artificially expire before the end of the ten-year period; as a result, the true cost of the bill, assuming extension of these tax breaks (many of which, such as the popular research and experimentation tax credit, are sure to be extended) is substantially higher than the reported $128 billion. The package adopted by the Senate Finance Committee on October 1 is ostensibly deficit-neutral, with revenue-raising provisions in the bill that appear to equal the cost of the bill’s new corporate tax breaks over the 2004-2013 period. But the bill’s appearance of revenue neutrality rests upon gimmicks. Several of its new tax cuts do not become fully effective until late in the decade, which makes their cost in the ten-year budget window much smaller than the cost of continuing these tax cuts indefinitely. The result is a serious mismatch over time between the revenue raised by the “offsets” in the bill and the revenue lost by the tax cuts. This can be seen in Joint Tax Committee figures showing that the measure would lose more than $9 billion in the second half of the ten-year period and lose more than $4 billion in 2013 alone. Over the long run, the bill is not deficit neutral and would produce sizeable revenue losses, thereby enlarging long-term deficits that already are frightening in size.

Concerns about

the corporate tax-cut measures under consideration in both the House and

Senate extend beyond their high cost. Although a detailed analysis of

these measures is beyond the scope of this paper, both bills would further

erode the corporate income tax base and potentially distort the allocation

of economic resources. In an attempt to satisfy competing business

interests, these bills offer dozens of targeted tax breaks for

|

Corporate income tax revenues are sensitive to economic

conditions, and the recent slowdown in the economy has played a significant

role in the collapse of corporate revenues. But the economy explains only

part of the decline.

Corporate revenues are further diminished by

aggressive tax avoidance strategies, including the sheltering of corporate

profits overseas. No precise estimates of the extent of these tax shelter

activities exist. In testimony before the Senate Finance Committee in March

2000, the Joint Committee on

Long-term Decline in Corporate Revenues

Other recent analyses have examined the stunning deterioration in the budget outlook, as well as the large, persistent deficits that now loom as far as the eye can see and that will swell further as the baby boom generation retires. In this analysis, we seek to provide context for the upcoming Congressional debate on corporate tax cuts, by examining trends in corporate tax revenues over recent decades. The analysis includes the following findings:

- Although taxes paid by corporations, measured as a share of the economy, rose modestly during the boom years of the 1990s, they remained sharply lower even in the boom years than in previous decades. According to OMB historical data, corporate taxes averaged 2 percent of GDP in the 1990s. That represented only about two-fifths of their share of GDP in the 1950s, half of their share in the 1960s, and three-quarters of their share in the 1970s.

- The share that corporate tax revenues comprise of total federal tax revenues also has collapsed, falling from an average of 28 percent of federal revenues in the 1950s and 21 percent in the 1960s to an average of about 10 percent since the 1980s.

- The effective corporate tax rate — that is, the percentage of corporate profits that is paid in federal corporate income taxes — has followed a similar pattern. During the 1990s, corporations as a group paid an average of 25.3 percent of their profits in federal corporate income taxes, according to new Congressional Research Service estimates. By contrast, they paid more than 49 percent in the 1950s, 38 percent in the 1960s, and 33 percent in the 1970s.

- Corporate income tax revenues are lower in the

Corporate Income Taxes

According to the Internal Revenue Service, more than 27 million businesses, including farm businesses, filed tax returns in 2000. Of these businesses, only 2.2 million — or about 8 percent — were subject to the corporate income tax.

These corporations — known as “C” corporations — include both large and small businesses. More than half of all C corporations had assets of less than $100,000 in 2000. The 0.8 percent of corporations that had assets of more than $100 million, however, accounted for more than 95 percent of all C corporation assets. In addition, fewer than one percent of all C corporations accounted for more than 85 percent of all federal corporate income taxes paid in 2000.[5] (Note: The profits of businesses other than C corporations are subject to the individual rather than the corporate income tax.)

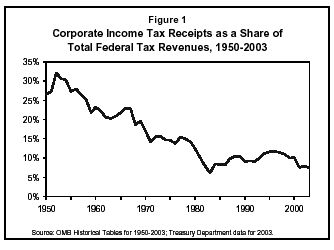

Looking over the post-World War II period (starting in 1950), the corporate income tax has been an important — but shrinking — source of federal revenue (see Figure 1).[6] It was the second largest source of revenue, behind the individual income tax, until 1968, when payroll taxes grew to be a larger share. In fact, there has been a virtually complete role-reversal between payroll taxes and corporate income taxes in terms of their contribution to federal receipts. Corporate income taxes reached a peak of 32 percent of federal tax receipts in 1952. In 2003, they equaled just over 7 percent of federal revenues. This decline was fairly steady, with corporate tax receipts equaling an average 21 percent of federal revenues in the 1960s, 15 percent in the 1970s, and less than 10 percent in the 1980s. After a brief rebound in the 1990s, when their share rose to nearly 12 percent in the middle of the decade, corporate receipts have now fallen to a percentage of federal tax collections not seen since the early 1980s. In contrast, payroll taxes represented about 10 percent of all federal tax receipts in 1952, but 40 percent in 2003.

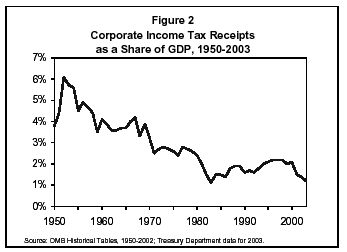

Corporate income tax revenues have declined not only in terms of the share of federal taxes that they comprise, but also when they are measured as a share of the economy (see Figure 2). Corporate revenues averaged nearly 5 percent of GDP in the 1950s and 4 percent in the 1960s, but then fell sharply to nearly 1 percent of GDP in 1983, reflecting the combination of tax cuts and economic conditions. After rising slightly above 2 percent of GDP during part of the 1990s, corporate receipts fell again after 2000, when the economy slowed. In 2003, actual corporate revenues dropped to 1.2 percent of GDP, the lowest level since 1937, except for 1983.[7]

As the economy recovers, CBO projects that corporate receipts will rise, but that they will still remain just under 2 percent of GDP by the end of the decade (i.e., 2009). But this estimate assumes that all of the recently enacted corporate tax breaks will expire by the end of 2004, as currently scheduled. If these tax breaks are extended — a distinct possibility given the intense pressure that exists to extend them and the fact that those who oppose extension are likely to be accused of seeking to raise taxes and of favoring a course that would injure the economy — corporate revenues would represent only 1.5 percent of GDP and 8.5 percent of all federal revenues during the second half of the decade, barely above today’s levels that have been depressed by the weak economy.

Table 1 on the following page shows corporate receipts both as a share of total federal receipts and as a share of the economy for the decades since 1950. The trend of shrinking corporate tax revenues is apparent in these data. Corporate income tax receipts recovered somewhat in the 1990s relative to the 1980s, when corporate receipts hit historic lows, but even in the 1990s, they remained far below the levels of previous decades. Now they have declined further. As noted, corporate revenues are expected to remain low over the coming decades, even after the economy has fully recovered.

|

||||||||||||||||||||||||||||||

Some argue that the weakness in corporate income tax revenues is, in part, a reflection of the decline in the number of C corporations, which peaked at 2.6 million in 1986. Offsetting this decline has been the rapid growth in another type of corporation, known as S corporations. S corporations do not pay corporate income tax, but rather pass through profits to their shareholders, who in turn include this business income on their individual income tax returns. As a result of liberalizations to the S corporation rules since 1986, some C corporations have converted to S corporations as a way to reduce their tax liabilities. But the precise impact of this shift on corporate revenues is unclear, as typically only smaller C corporations are in a position to change status. Limits on the number of S corporation shareholders, for instance, make it impossible for the large, publicly-traded C corporations to convert. As a result, the average C corporation in 2000 had assets that were 33 times larger than the assets held by the average S corporation. While the S corporation liberalization may have eroded the corporate income tax base when it comes to smaller corporations, it has not significantly affected the large corporations that account for the lion’s share of corporate income tax revenues.

Corporate Tax Rates

The corporate income tax rate is typically thought to be 35 percent. The reality is more complicated. The 35 percent rate is the highest statutory corporate rate; lower levels of corporate income are taxed at lower rates. The first $50,000 of taxable corporate income faces a 15 percent tax rate, and the next $25,000 is subject to a 25 percent rate. From $75,000 to $10 million of taxable profits, corporations pay a 34 percent rate. For taxable income above $10 million, the rate is 35 percent. These lower graduated rates phase out for corporations with larger incomes.[8]

In general, however, the share of corporate profits that is ultimately taxed is much lower than the maximum statutory rate of 35 percent. According to a new Congressional Research Service report, since 1993 (when the top statutory rate was set at 35 percent), the effective corporate tax rate — that is, the share of total corporate profits that is paid to the federal government in corporate income taxes — has averaged 26.3 percent for non-financial corporations, or about one-quarter lower than the 35 percent statutory rate.[9] CRS notes that the effective tax rate is “a better measure of the true burden of the [corporate income] tax.”

The effective rate is lower than the statutory rate not only because of the existence of a graduated corporate rate structure, but also because corporations receive a number of deductions, credits, and other benefits that reduce the income taxes they owe. For instance, the Joint Committee on Taxation estimates that in 2003, corporations will reduce their tax liabilities by $41 billion as a result of provisions that allow firms to write-off or depreciate the cost of equipment and buildings.[10] Moreover, these estimates likely understate the tax savings corporations will reap from these write-offs. Although the JCT estimates, which were released in December 2002, take into account an expansion of the depreciation tax break that was enacted in 2002, they do not reflect the significant additional expansion of this tax break that was enacted in May 2003, in hopes of encouraging more corporate investment amidst the economic slowdown.[11]

|

Recently Enacted Business Tax Cuts The tax cuts enacted since President Bush took office are typically described as benefiting individuals and not businesses. Businesses are often depicted as sitting on the sidelines, waiting patiently for their turn to have their taxes reduced. The last two tax-cut measures, however, included substantial tax cuts for businesses, including very generous write-offs for investments in plants and purchases of equipment. Under the package enacted in May 2003, businesses can immediately write off 50 percent of the cost of these new investments; businesses with smaller levels of new investments and purchases can immediately write off the full cost of new investments and purchases up to $100,000. These measures will provide businesses with tax breaks totaling more than $175 billion through 2005. Corporations, as distinguished from small businesses, are by far the largest beneficiaries of these tax breaks. Moreover, there is likely to be pressure to extend these provisions, which are officially slated to expire after the next few years, and ultimately to make them permanent. If extended throughout the decade, these business tax breaks would reduce federal revenues by extremely large amounts — by another $466 billion through 2013, according to the Joint Committee on Taxation. Beyond the tax breaks that directly reduce corporate income taxes, the May 2003 tax-cut package also included provisions that reduced the tax rate on corporate dividends and capital gains (at least half of which are paid on company stock). These provisions, which are slated to expire artificially after 2008, would cost $307 billion over ten years if they were made permanent. They were enacted with the goal of reducing the “double taxation” of corporate income, which occurs when corporate earnings are taxed first at the corporate level and then again at the individual level when the shareholder receives a dividend payment or sells stock for a gain. By reducing the overall tax on corporate income, these provisions are also a benefit to corporations and the owners of capital. |

The Joint Committee also estimates that the amount of corporate income tax revenue being foregone in 2003 as a result of various other major corporate tax breaks is as follows:

- $11 billion from tax breaks available to multinational firms operating overseas;

- $9 billion from tax breaks to promote research and experimentation; and

- $5 billion from subsidizing

The revenue losses from these tax breaks add up. Just the four tax breaks listed here — not an exhaustive list — total more than $60 billion in lost revenue in 2003. This figure is not exact since there are some interaction effects between the tax breaks. Nevertheless, it gives a sense of the magnitude of these provisions.

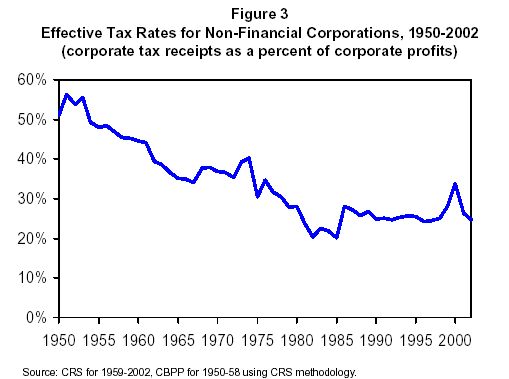

Figure 3 shows much the same declining trend in the federal effective corporate tax rate over the post-World War II period as has occurred with regard to corporate revenues both as a share of total federal revenues and as a share of GDP. The Congressional Research Service data on the federal effective corporate tax rate cover the period from 1959 to 2002; we have applied the CRS methodology to years from 1950 to 1959, so that the data on effective tax rates cover the same time period as other data presented in this analysis.

Part of the reason for the decline in the effective corporate tax rate has been the decline in the corporate tax rate set in statute. The statutory corporate income tax rate exceeded 50 percent for much of the 1950s and 1960s, and was set at 48 percent for most of the 1970s and 46 percent for the 1980s up until enactment of the Tax Reform Act of 1986. But the effective corporate tax rate declined faster than the statutory rate for most of this period, indicating that the tax breaks available to corporations were expanding.

In particular, depreciation write-offs for investments were made more generous in the mid-1950s and again in the 1960s, with the introduction of the investment tax credit. The sharpest decline in the effective tax rate relative to the statutory rate occurred in the early 1980s, with the enactment of the “accelerated cost recovery system” — which, according to the late Brookings Institution tax scholar Joseph Pechman, “broke the precedent with prior laws by severing the connections between the useful life of an asset and the period over which it was depreciated for tax purposes.”[12]

This trend was reversed with the 1986 Tax Reform Act. With the enactment of the 1986 act, the corporate rate was lowered to 34 percent, but at the same time tax breaks were eliminated; as a result, the effective corporate tax rate increased in the years immediately following these changes, closing some of the gap between the statutory rate and the effective rate. With the creation of more corporate tax breaks in recent years, however, the gap has widened again. (In addition, the rise in the number of S corporations, noted earlier, has contributed to widening this gap; these firms do not pay corporate income taxes but their earnings are included as part of total corporate income.) This gap would likely be even larger if the figures were able to take into full account the impact of tax sheltering by corporations, as discussed below.[13]

Corporate Tax Shelters

In recent years, there has been considerable concern about the increasingly aggressive use of tax shelters by corporations to avoid paying taxes. The impact of these tax shelters — which, by definition, are designed to hide income — are not captured in the Congressional Research Service data on effective tax rates, because those data rely on corporate income that has been reported to the IRS. If the income hidden through tax shelters could be estimated and a more accurate estimate of total corporate income derived as a result, the effective corporate tax rate would be shown to be lower — possibly substantially lower — than is depicted here.

For instance, a study by the Institute on

Further, the study by the Institute on

No precise estimate exists of the amount of income that

corporations shelter from income tax. As noted, the Joint Committee on

More recently, in testimony before the Senate Finance Committee on IRS efforts to curb abusive tax shelters, the General Accounting Office confirmed that the IRS believes that tens of billions of dollars have been lost to tax shelters.[16] GAO cited a database maintained by the IRS that shows that through 2003 about $85 billion in revenues have been lost as a result of known tax shelters (used by businesses and wealthy individuals) that IRS has officially classified as abusive or that have characteristics of abusive transactions. These revenue losses date back to 1989, but the majority occurred in years after 1993. Another analysis, which was conducted by a contractor at the request of the IRS, concluded that the revenue losses from corporate tax shelters alone were even higher, estimating an average annual loss of between $11.6 billion and $15.1 billion for the period 1993 through 1999. The estimates also show that the size of the abusive shelter problem grew in each year analyzed, with the revenue loss reaching between $14.5 billion and $18.4 billion in 1999. Although the GAO and IRS expressed some concerns about the methodology used in the study, it is possible that the estimates understate the problem because the analysis reflects only the tax losses associated with sheltering by large corporations and because it relied on a conservative definition of abusive shelter.

Beyond this evidence, another sign that corporate tax sheltering is on the rise is the divergence between the “book” income that corporations report to their shareholders and the income that these corporations report to the IRS for tax purposes. A number of studies conducted in recent years have identified very large gaps between “book” and “tax” income, including a 1999 Treasury Department analysis that concluded that tax shelter activity was one of the factors causing this divergence.[17]

A more recent National Bureau of Economic Research study reached similar conclusions. It found that this gap has grown and that in 1998, some $154 billion — or more than half of the gap between “book” and “tax” income for that year — could not be explained by the traditional accounting differences. The author concluded that “the large unexplained gaps between tax and book income that have arisen during the late 1990s are at least partly associated with increased sheltering activity.”[18]

International Comparisons

While the data show a large reduction over time in the tax burdens

of

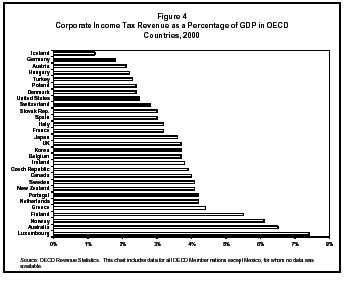

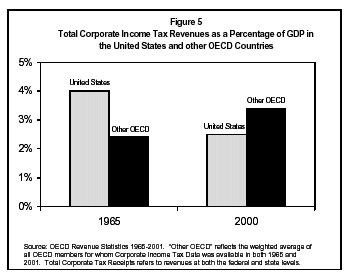

Figure 4 presents data from the Organization of Economic

Cooperation and Development on corporate income tax revenues as a share of the

economies for 29 OECD countries in 2000. Based on these data, nearly

three-quarters of these OECD countries collect more in corporate revenues

relative to the size of their economies than the

Some assert that

The Joint Committee on Taxation has concluded,

however, that “no country uses a pure worldwide or territorial system, … [and

that] all systems share at least some features of worldwide and territorial

approaches.”[19]

The

According to this analysis, assuming no change in corporate

business practices, switching from a worldwide to a territorial system would

increase the taxes that

Conclusion

Recent Congressional Budget Office estimates show corporate income tax revenues falling to historically low levels in 2003. Whether measured as a share of the economy or in terms of their contribution to total federal receipts, corporate revenues are now a mere fraction of the levels seen in the 1950s and 1960s. Further, CBO projects that corporate revenues will remain at historically low levels throughout the decade, even after the economy has fully recovered and even if the corporate tax cuts enacted in 2002 and 2003 expire as scheduled. Although difficult to measure, corporate tax shelters are a significant problem, according to studies by the Treasury Department and the Joint Committee on Taxation, and have contributed to this decline in corporate revenues.

Despite these low levels of corporate income tax receipts and recent projections showing massive deterioration in the long-term fiscal outlook, Congress is scheduled to consider more corporate tax cuts this fall. The corporate tax-cut bill recently adopted by the Senate Finance Committee and the measure recently introduced by House Ways and Means Chairman Bill Thomas would dig the long-term deficit hole even deeper, since the corporate tax breaks contained in these measures would ultimately outstrip the bills’ revenue-raising offsets.

End Notes:

[1]

Center on Budget and Policy Priorities, Committee for Economic

Development, and

[2]

Joint Committee on

[3] Charles Rossotti, “Report to the IRS Oversight Board Assessment of the IRS and the Tax System,” September 2002.

[4]

Michael Brostek, “Internal Revenue Service: Challenges Remain in

Combating Abusive

[5]

These IRS data can be found in Joint Committee on

[6] Although the corporate income tax was established in 1913, the modern tax system took shape during World War II, when the role of the individual income tax was expanded.

[7]Corporate revenues have also been affected by timing shifts that were included in the tax-cut measures enacted since 2000. Receipts were higher in 2002 and lower in 2003 as a result of these shifts. These timing shifts, however, do not affect the underlying trends. Corporate receipts in 2002 and 2003, absent these shifts, would still have been at their lowest levels in six decades, except for 1983.

[8] As a result of these phase outs, corporations with taxable income between $335,000 and $10 million effectively face a flat 34 percent rate, and those with income above $18.3 million are effectively subject to a flat 35 percent rate.

[9]

Steve Maguire, “Average Effective Corporate Tax Rates: 1959-2002,”

Congressional Research Service,

[10]

Joint Committee on Taxation, “Estimates of Federal Tax Expenditures for

Fiscal Years 2003-2007, JCS-5-02,

[11] The 2002 measure permitted corporations to write-off 30 percent of the cost of new investments through September 2003. In May 2003, the amount of new investments that could be written-off was increased to 50 percent, and the provision was extended through the end of 2004.

[12] Joseph Pechman, Federal Tax Policy, Brookings Institution, 1987.

[13] For a discussion of the divergence between the statutory and effective tax rates since 1980, see U.S. Treasury Department analyst James Mackie, “The Puzzling Comeback of the Corporate Income Tax,” National Tax Association 92nd Annual Conference, 1999.

[14]

Robert S. McIntyre and T.D. Coo Nguyen, “Corporate Income

[15]

Robert S. McIntyre, “Testimony Before the Committee on the

[16]

Michael Brostek, “Internal Revenue Service: Challenges Remain in

Combating Abusive

[17]Treasury

Department, “The Problem of Corporate

[18] Mihir Desai, “The Corporate Profit Base, Tax Sheltering Activity, and the Changing Nature of Employee Compensation,” NBER Working Paper 8866, April 2002.

[19]

Joint Committee on

[20] Harry Grubert, “Enacting Dividend Exemption and Tax Revenue,” National Tax Journal, December 2001.